Report on Financial Accounting Issues and Solutions for Pewter Ltd

VerifiedAdded on 2020/07/23

|12

|1826

|39

Report

AI Summary

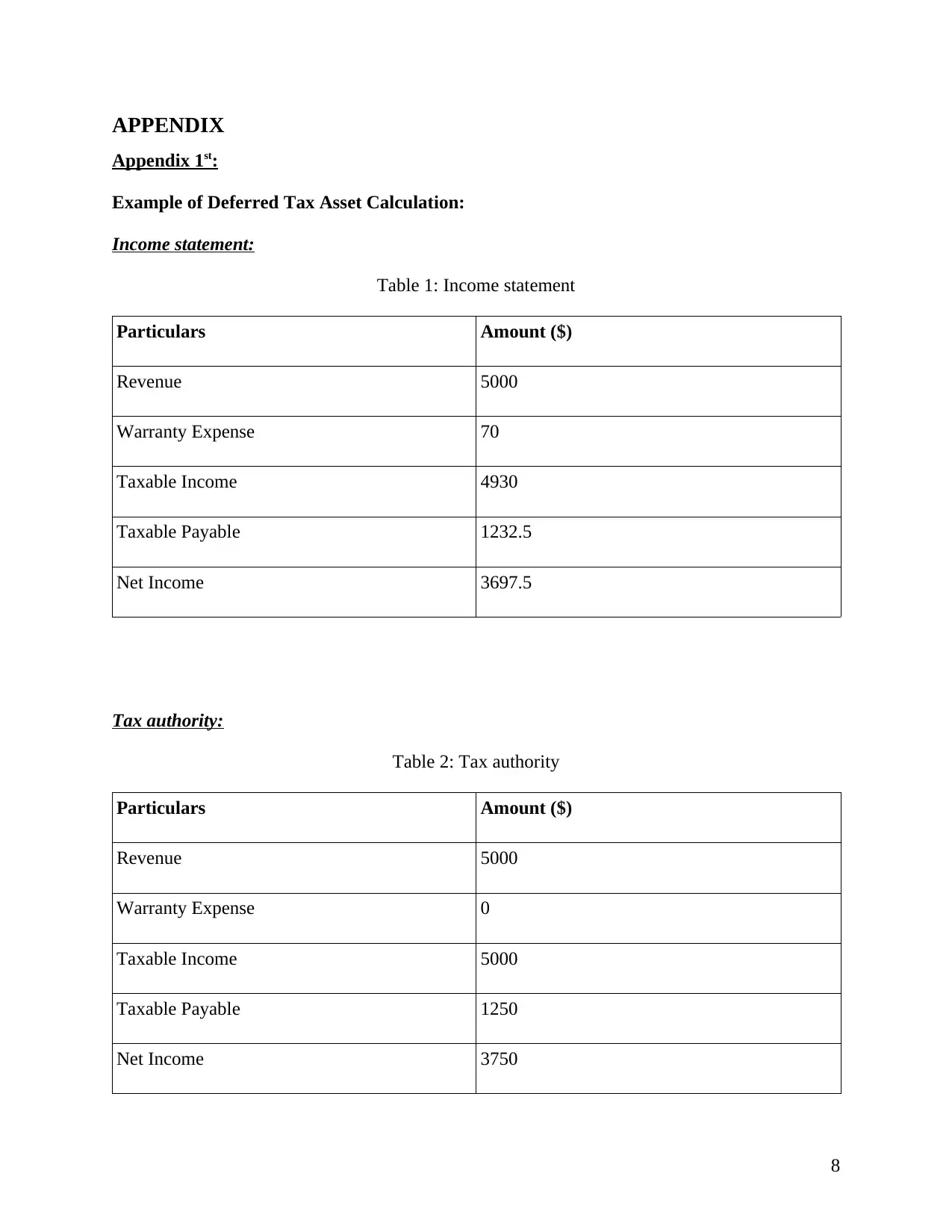

This report provides a comprehensive analysis of the financial accounting and reporting issues encountered by Pewter Ltd. It delves into the complexities of accounting for deferred tax assets (DTA) and deferred tax liabilities (DTL), highlighting the time consumption and financial costs associated with these processes. The report also examines the challenges related to accounting for sales revenue adjustments and inventory returns from retailers, including the recording of expenses incurred on product advertisement. Through a detailed examination of these issues, the report offers suggestions for improvement, including the importance of accurately recording financial transactions and the significance of maintaining comprehensive financial records. A business letter from a management accountant at Mckenzie and Associates is included, providing practical advice and recommendations to address the identified problems. The report concludes by emphasizing the critical role of financial accounting in determining an organization's economic position and supporting informed decision-making for future business operations. The appendices include examples of DTA calculations and illustrations of the impact of tax changes.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.