Management Accounting System Evaluation in Pharmacy2U Company

VerifiedAdded on 2023/06/18

|17

|4170

|240

Report

AI Summary

This report provides a detailed analysis of management accounting (MA) practices at Pharmacy2U, an online pharmacy in the UK. It covers essential requirements of different management accounting systems such as cost accounting, inventory management, and price optimization, along with methods for management accounting reporting including budget reports, performance reports, and cost managerial accounting reports. The report also examines the principles of MA and its role in decision-making, including data provision, analysis, communication, and control facilitation. Furthermore, it discusses income statements under variable and absorption costing, the reasons for differences between them, and a critical evaluation of the MA system and reporting integration within Pharmacy2U, highlighting the benefits and potential drawbacks. The report also compares planning tools like cost accounting, marginal costing and cash flow analysis. The report concludes with recommendations for Pharmacy2U to enhance its financial decision-making through effective MA implementation.

Unit – 5 MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

Management accounting and essential requirements of different types of management

accounting system........................................................................................................................3

Meaning of Management Accounting.........................................................................................3

Essential requirement of different types of management accounting system..............................3

Methods used for management accounting reporting..................................................................4

Principles of management accounting.........................................................................................4

Role of management accounting & MA systems........................................................................5

Income statement under variable and absorption costing............................................................6

Income statement under absorption costing.................................................................................7

Income statement under marginal costing..................................................................................8

Reason of difference between Marginal and Absorption costing................................................8

Critical evaluation of management accounting system and reporting integration within the

Pharmacy2U company.................................................................................................................8

Benefits of the function of management accounting to Pharmacy2U industry...........................9

Conclusion on application of management accounting...............................................................9

PART 2..........................................................................................................................................10

Comparison of three planning tools used in management accounting......................................10

.......................................................................................................................................................13

Comparison of ways in which management accounting is effective in dealing with financial

problems by preventing it..........................................................................................................13

CONCLUSION AND RECOMMENDATIONS:.........................................................................15

........................................................................................................................................................16

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

Management accounting and essential requirements of different types of management

accounting system........................................................................................................................3

Meaning of Management Accounting.........................................................................................3

Essential requirement of different types of management accounting system..............................3

Methods used for management accounting reporting..................................................................4

Principles of management accounting.........................................................................................4

Role of management accounting & MA systems........................................................................5

Income statement under variable and absorption costing............................................................6

Income statement under absorption costing.................................................................................7

Income statement under marginal costing..................................................................................8

Reason of difference between Marginal and Absorption costing................................................8

Critical evaluation of management accounting system and reporting integration within the

Pharmacy2U company.................................................................................................................8

Benefits of the function of management accounting to Pharmacy2U industry...........................9

Conclusion on application of management accounting...............................................................9

PART 2..........................................................................................................................................10

Comparison of three planning tools used in management accounting......................................10

.......................................................................................................................................................13

Comparison of ways in which management accounting is effective in dealing with financial

problems by preventing it..........................................................................................................13

CONCLUSION AND RECOMMENDATIONS:.........................................................................15

........................................................................................................................................................16

REFERENCES................................................................................................................................1

INTRODUCTION

Management accounting (MA) is also termed as managerial accounting is a process of

identify, estimate, analyse, interpret & communicate the financial information to managers of the

company for successfully achieving organizational goals (Ax and Greve, 2017). This report is

based on Pharmacy2U founded by pharmacist Daniel Lee in November 1999. It is an online

pharmacy located in UK. This report will study about principle of management accounting & the

role of MA. Moreover, it will study about income statement using absorption & marginal costing

method to present the co. financial statement & position. This report will also discuss the

function of MA & its advantages and disadvantages. Study will also further focus towards

planning tools of MA or case studies with example for compare the ways in which MA is

applied. Report will also give conclusions and recommendations to the company.

PART A

Management accounting and essential requirements of different types of management

accounting system

Meaning of Management Accounting

The institute of Cost and Management Accountants, MA is the preparation of financial

information by implementing of professional knowledge & skill. This information help in a way

to guide manager in the formulation of various policies and also help in planning and controlling

of the company's operation for achieving sustainable growth (Qian, Hörisch and Schaltegger,

2018).

Essential requirement of different types of management accounting system

The basic management accounting system which is required to be followed and apply by

Pharmacy2U are as follows:

Cost Accounting

Cost accounting direct the manager to evaluate the company's total cost of production including

variable costs & fixed costs for production of per unit. For ex. Pharmacy2U co. use cost

accounting system to know the cost of each capsule which involve cost of drugs, any chemical

solution, or plastic body, packaging and so on. It assists the managers to take decision about the

price of per capsule.

Management accounting (MA) is also termed as managerial accounting is a process of

identify, estimate, analyse, interpret & communicate the financial information to managers of the

company for successfully achieving organizational goals (Ax and Greve, 2017). This report is

based on Pharmacy2U founded by pharmacist Daniel Lee in November 1999. It is an online

pharmacy located in UK. This report will study about principle of management accounting & the

role of MA. Moreover, it will study about income statement using absorption & marginal costing

method to present the co. financial statement & position. This report will also discuss the

function of MA & its advantages and disadvantages. Study will also further focus towards

planning tools of MA or case studies with example for compare the ways in which MA is

applied. Report will also give conclusions and recommendations to the company.

PART A

Management accounting and essential requirements of different types of management

accounting system

Meaning of Management Accounting

The institute of Cost and Management Accountants, MA is the preparation of financial

information by implementing of professional knowledge & skill. This information help in a way

to guide manager in the formulation of various policies and also help in planning and controlling

of the company's operation for achieving sustainable growth (Qian, Hörisch and Schaltegger,

2018).

Essential requirement of different types of management accounting system

The basic management accounting system which is required to be followed and apply by

Pharmacy2U are as follows:

Cost Accounting

Cost accounting direct the manager to evaluate the company's total cost of production including

variable costs & fixed costs for production of per unit. For ex. Pharmacy2U co. use cost

accounting system to know the cost of each capsule which involve cost of drugs, any chemical

solution, or plastic body, packaging and so on. It assists the managers to take decision about the

price of per capsule.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management system

This system is used for calculating the value of inventory by using various methods such as

LIFO, FIFO, AVCO. For ex. Pharmacy2U can use inventory system to evaluate the need of

quantity of products such as drugs, chemical solution, aluminium & plastic for packaging etc. so

that the overstock of material is ignored (Ngo, 2020).

Price-optimization system

Price-optimization is used to calculate the price according to the changing market demand of the

product at different price levels. It helps companies to decide their price at that level they earn

maximum profit. For ex. Pharmacy2U use this system to calculate the price according to the

particular demand of the medicine.

Methods used for management accounting reporting

The different methods of MA that need to be used by Pharmacy2U finance and account manager

are as follows:

Budget reports

Budget reports are very critical in evaluating company performance. An estimated budget is

made based on historical data & then according to that budget company's actual performance is

compared (Andriani and Suhartini, 2020). For ex. Pharmacy2U used cash budget to know the

cost of raw materials and on the basis of that plan their future prices to earn maximum profit.

Performance reports

These reports are used to create the performance review of a company as a whole. Each

employee performance are analysed by this report which help company to know that which

employee underperform & need training.

Cost managerial accounting reports

These reports help the company to analyse their cost of production including all direct and

indirect cost such as raw material cost, overhead, labour etc. For ex. These methods used by

Pharmacy2U to identify their cost including drugs, chemical solution, plastic & aluminium and

so on.

Principles of management accounting

The principles of MA that Pharmacy2U need to be followed are described below:

This system is used for calculating the value of inventory by using various methods such as

LIFO, FIFO, AVCO. For ex. Pharmacy2U can use inventory system to evaluate the need of

quantity of products such as drugs, chemical solution, aluminium & plastic for packaging etc. so

that the overstock of material is ignored (Ngo, 2020).

Price-optimization system

Price-optimization is used to calculate the price according to the changing market demand of the

product at different price levels. It helps companies to decide their price at that level they earn

maximum profit. For ex. Pharmacy2U use this system to calculate the price according to the

particular demand of the medicine.

Methods used for management accounting reporting

The different methods of MA that need to be used by Pharmacy2U finance and account manager

are as follows:

Budget reports

Budget reports are very critical in evaluating company performance. An estimated budget is

made based on historical data & then according to that budget company's actual performance is

compared (Andriani and Suhartini, 2020). For ex. Pharmacy2U used cash budget to know the

cost of raw materials and on the basis of that plan their future prices to earn maximum profit.

Performance reports

These reports are used to create the performance review of a company as a whole. Each

employee performance are analysed by this report which help company to know that which

employee underperform & need training.

Cost managerial accounting reports

These reports help the company to analyse their cost of production including all direct and

indirect cost such as raw material cost, overhead, labour etc. For ex. These methods used by

Pharmacy2U to identify their cost including drugs, chemical solution, plastic & aluminium and

so on.

Principles of management accounting

The principles of MA that Pharmacy2U need to be followed are described below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Designing and compiling

MA system is designed accounting information in such a way that helps managers to solve

various problems. Accounting information is easily altered according to the requirement of

managers.

Accounting for inflation

To know the value of capital given by the owner of the company in term of real value of money

it is necessary to evaluate through revaluation accounting. In this inflation rate is considered to

know the real success of the business.

Forward looking approach

Management accounting helps the company to analyse the future problems with the help of

standard costing techniques. Future problems may be avoided to arise (Burger and Middelberg,

2018).

Role of management accounting & MA systems

The role of MA of the Pharmacy2U in decision-making process of organization are as follows:

Provides data

For every co. data is important for analyse the company performance. MA provides data to the

organization about the past achievements of the co. that help them to forecasts for the future

plans. Without the reference of data no MA planning is successfully done.

Analysis and interpretation of data

The financial data is not easily understandable for any manager of the co. MA helps in

rearranged data with proper analysis in that way the data is meaningful interpreted. Data is

arranged with the help of ratio analysis, P&L account, balance sheet and so on (Gonçalves and

Gaio, 2021).

Communication

Management accounting play the role of communicator of data. Each and every member of the

company needs data MA provide information as per the need of various level of management

such as top, middle, and lower levels. For ex. The top-level manager needs critical information

for long term planning.

Facilitate control

MA system is designed accounting information in such a way that helps managers to solve

various problems. Accounting information is easily altered according to the requirement of

managers.

Accounting for inflation

To know the value of capital given by the owner of the company in term of real value of money

it is necessary to evaluate through revaluation accounting. In this inflation rate is considered to

know the real success of the business.

Forward looking approach

Management accounting helps the company to analyse the future problems with the help of

standard costing techniques. Future problems may be avoided to arise (Burger and Middelberg,

2018).

Role of management accounting & MA systems

The role of MA of the Pharmacy2U in decision-making process of organization are as follows:

Provides data

For every co. data is important for analyse the company performance. MA provides data to the

organization about the past achievements of the co. that help them to forecasts for the future

plans. Without the reference of data no MA planning is successfully done.

Analysis and interpretation of data

The financial data is not easily understandable for any manager of the co. MA helps in

rearranged data with proper analysis in that way the data is meaningful interpreted. Data is

arranged with the help of ratio analysis, P&L account, balance sheet and so on (Gonçalves and

Gaio, 2021).

Communication

Management accounting play the role of communicator of data. Each and every member of the

company needs data MA provide information as per the need of various level of management

such as top, middle, and lower levels. For ex. The top-level manager needs critical information

for long term planning.

Facilitate control

MA helps companies in facilitate control of the activities through preparing of budgets and

standard costing. According to that estimated budget and standard costing actual performance of

the company is compared and any deviation is arisen then take corrective measures to control the

activity.

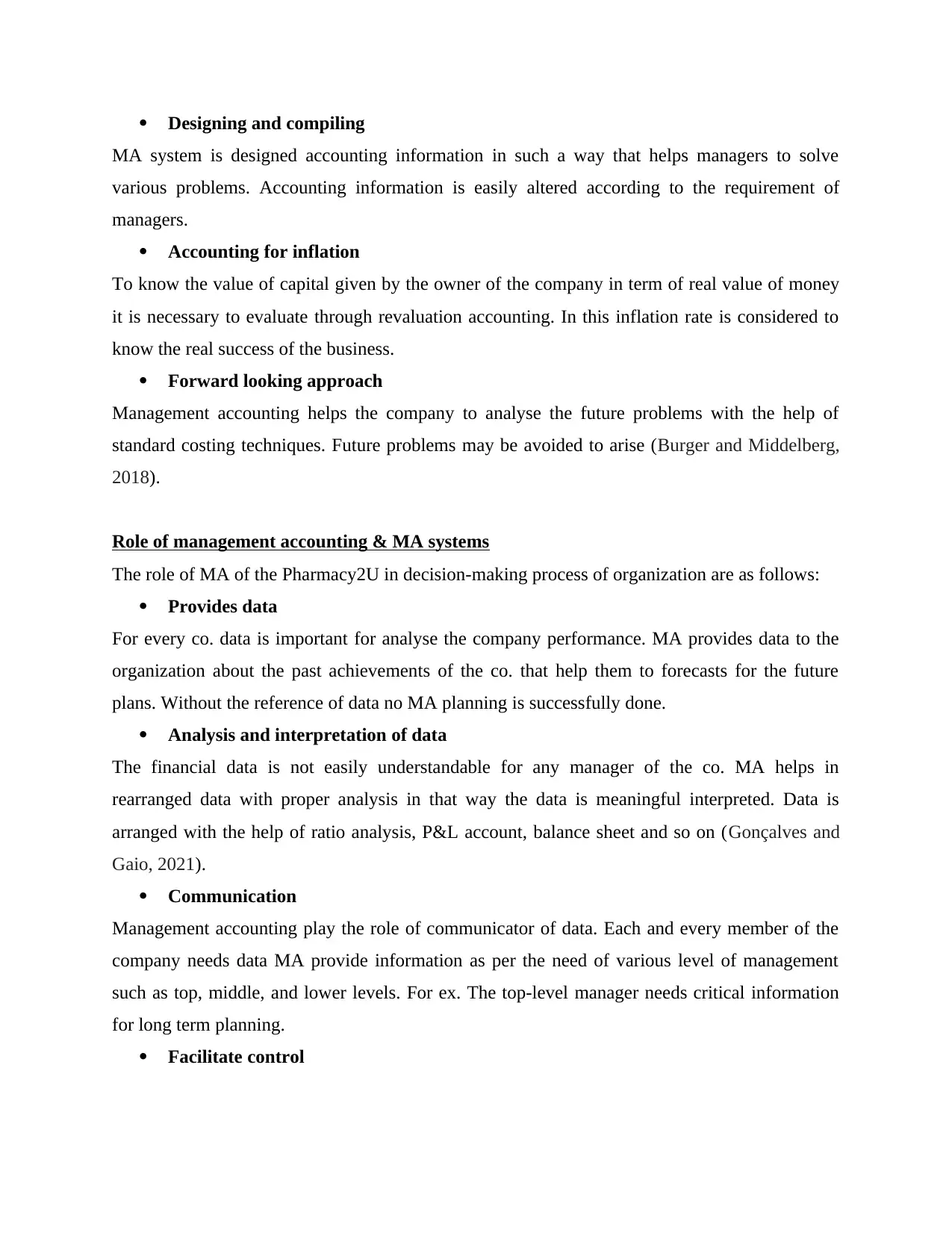

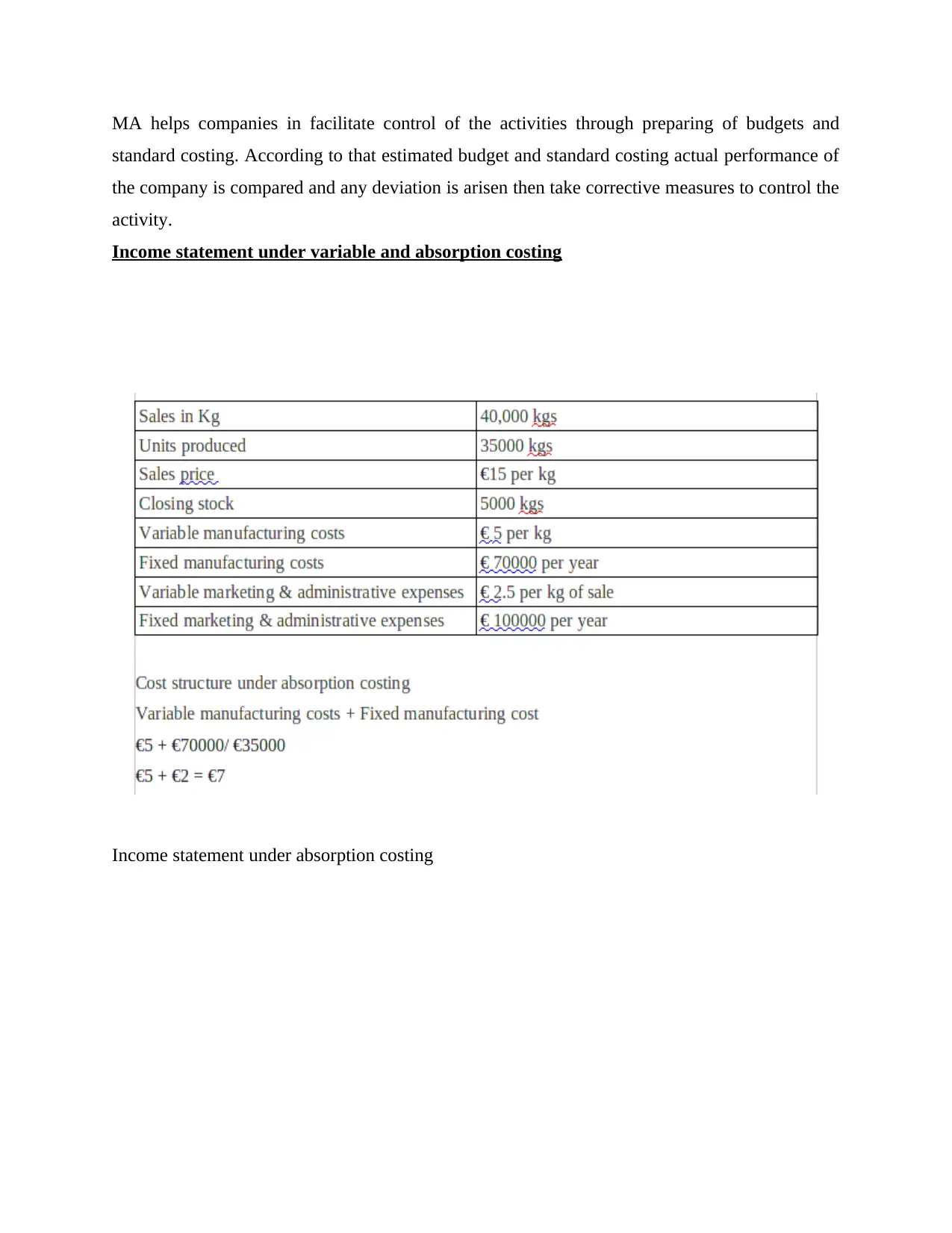

Income statement under variable and absorption costing

Income statement under absorption costing

standard costing. According to that estimated budget and standard costing actual performance of

the company is compared and any deviation is arisen then take corrective measures to control the

activity.

Income statement under variable and absorption costing

Income statement under absorption costing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

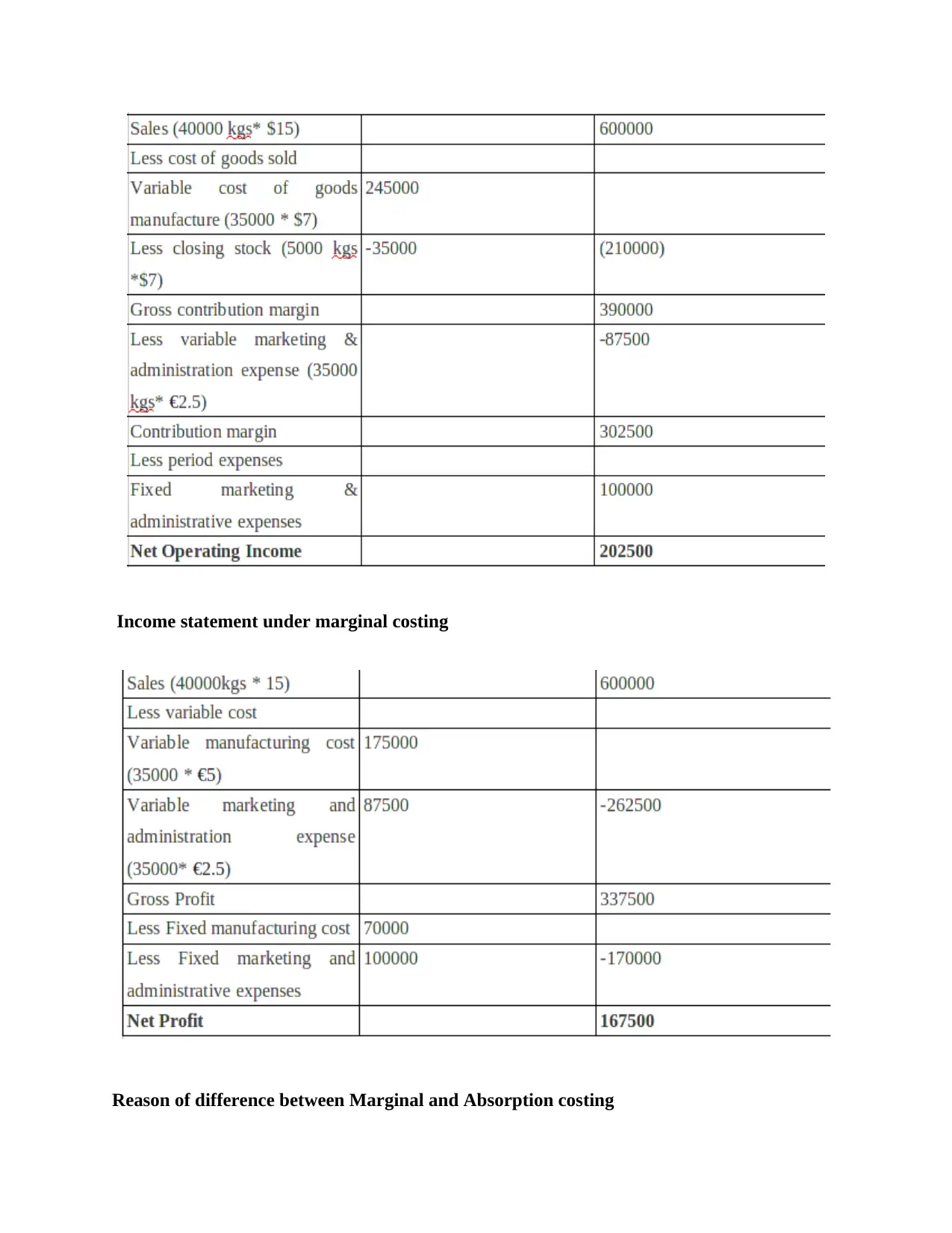

Income statement under marginal costing

Reason of difference between Marginal and Absorption costing

Reason of difference between Marginal and Absorption costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The main reason of difference between marginal & absorption costing is treatment of

fixed cost of production. In absorption costing both fixed and variable cost are considered in cost

of goods sold (COGS) whereas in the marginal costing method only variable costs are included

in COGS (Childers and Maggard-Gibbons, 2018).

Critical evaluation of management accounting system and reporting integration within the

Pharmacy2U company

Management accounting system assists the Pharmacy2U industry managers to make

decisions concerning future plans. It also helps managers in formulation of policies for planning

& controlling the operations of the firm. MA requires high professional knowledge & skills for

formulation of financial and accounting information in that way through which management

takes necessary decisions. Understand this with various types of MA such as inventory valuation

help the manager to know the actual cost of production and it also identifies its economic order

quantity so the Pharmacy2U give their products to the customer at its best price. Cash flow

analysis assist the company about the working capital which used to run business operations and

complete transactions (Yousefizadeh and Molanazari, 2018).

But it is always advisable to the company before take any decision as per the basis of MA

system business need to understand their objectives. Because MA need to hire professional

person who has an knowledge about that and it is costly for small & medium-sized companies.

MA system are based on past records and estimation that not proven always right & if company

fails to achieve their goals according to their budgeted plan then they might suffer huge financial

losses.

Benefits of the function of management accounting to Pharmacy2U industry

In case, if Pharmacy2U company adopt management accounting tools and techniques along with

system within the organization, then they will enjoy the following benefits:

MA helps the company in determined their break-even point through the margin analysis

technique. Break-even point is the point that show company's equity point where co.

cover its total cost of production. It helps in determine optimal sales mix of the products

& manage its profitability.

Variance analysis show the manager of the company about the difference between

estimated budgets and actual performance of the co. Budgets are formulated on an

fixed cost of production. In absorption costing both fixed and variable cost are considered in cost

of goods sold (COGS) whereas in the marginal costing method only variable costs are included

in COGS (Childers and Maggard-Gibbons, 2018).

Critical evaluation of management accounting system and reporting integration within the

Pharmacy2U company

Management accounting system assists the Pharmacy2U industry managers to make

decisions concerning future plans. It also helps managers in formulation of policies for planning

& controlling the operations of the firm. MA requires high professional knowledge & skills for

formulation of financial and accounting information in that way through which management

takes necessary decisions. Understand this with various types of MA such as inventory valuation

help the manager to know the actual cost of production and it also identifies its economic order

quantity so the Pharmacy2U give their products to the customer at its best price. Cash flow

analysis assist the company about the working capital which used to run business operations and

complete transactions (Yousefizadeh and Molanazari, 2018).

But it is always advisable to the company before take any decision as per the basis of MA

system business need to understand their objectives. Because MA need to hire professional

person who has an knowledge about that and it is costly for small & medium-sized companies.

MA system are based on past records and estimation that not proven always right & if company

fails to achieve their goals according to their budgeted plan then they might suffer huge financial

losses.

Benefits of the function of management accounting to Pharmacy2U industry

In case, if Pharmacy2U company adopt management accounting tools and techniques along with

system within the organization, then they will enjoy the following benefits:

MA helps the company in determined their break-even point through the margin analysis

technique. Break-even point is the point that show company's equity point where co.

cover its total cost of production. It helps in determine optimal sales mix of the products

& manage its profitability.

Variance analysis show the manager of the company about the difference between

estimated budgets and actual performance of the co. Budgets are formulated on an

estimated basis that directs the future actions of the company. Analysis of variances helps

the company to make informed decision (Iravani, Akbari and Zohoori, 2017).

It assists the manager of Pharmacy2U co. about the hurdles and bottlenecks with the help

of constraint analysis technique. It analyses the impact of this in revenue-generating

capacity & profit of the company.

Rate of return technique of MA helps the manager in determining the most profitable

project or proposal. The project that give higher profit is selected.

Manager makes a decision regarding future capital investments of the company such as

fixed assets & equipment. These decisions are made with the help of capital budgeting

analysis that shows the capital availability of the company.

Conclusion on application of management accounting

The report has concluded that if Pharmacy2U company want to take various decision for

growth & success of the organization. With the earning of maximum profit then company need

to follow various MA system & methods. The report has examined in detail about the principles

of MA which directs the co. to follow right procedure. It has also studied about the role of MA &

its system. The report has also concluded about the various MA tools and functions with its

implementation in the Pharmacy2U industry. It has also researched about the benefits of

financial reporting & statements and critically evaluate the MA system & reporting.

PART 2

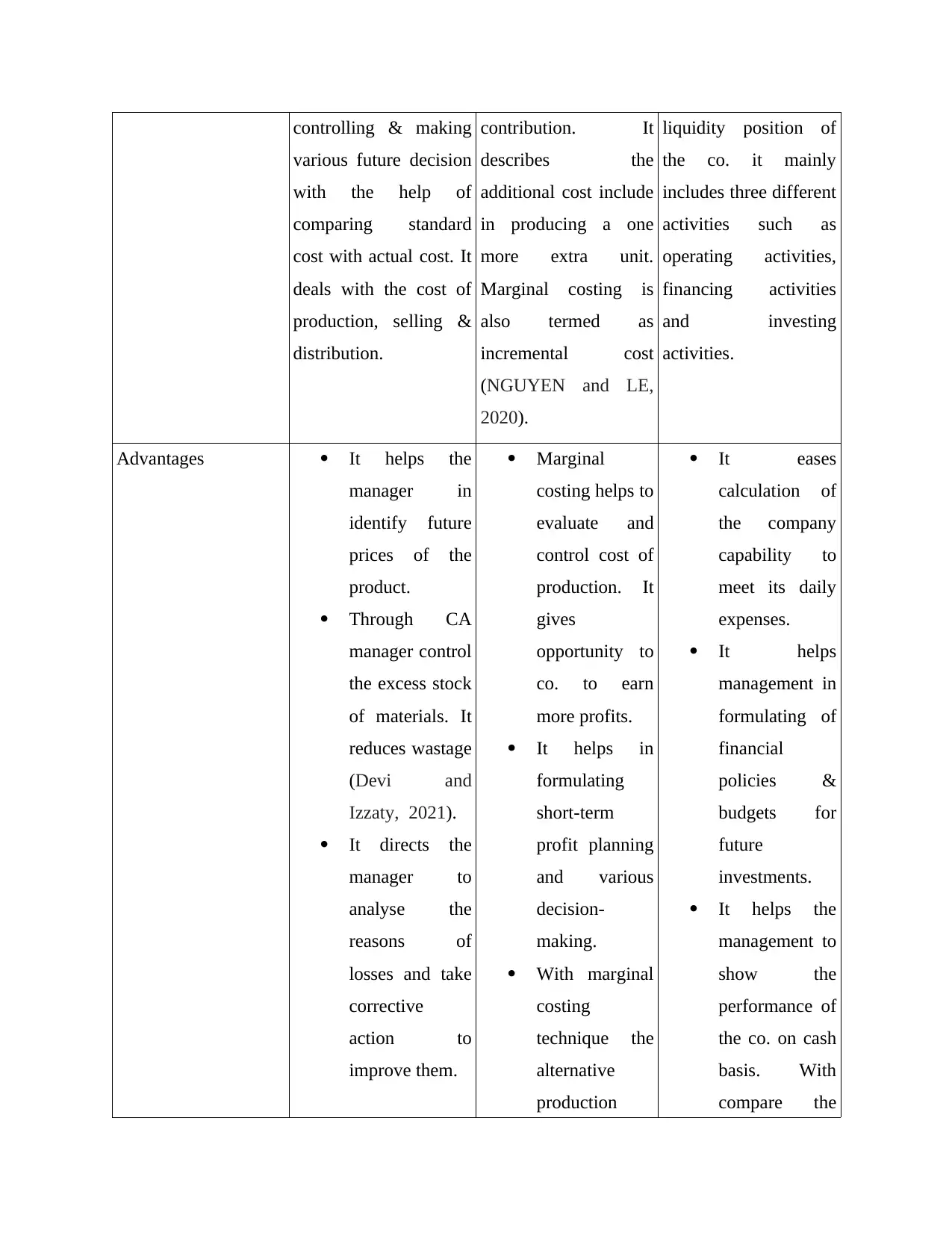

Comparison of three planning tools used in management accounting

Particulars Cost Accounting Marginal Costing Cash Flow Analysis

Meaning Cost accounting (CA)

is the process of

identifying the total

cost of production

including fixed cost or

variable cost. It helps

the managers in cost

Marginal costing is the

technique in which

only variable cost is

considered as the cost

of production. While

fixed cost is fully

written off against the

Cash flow analysis is a

technique that used to

know the cash inflows

and outflows of the co.

It is used by investors

and managers to

analyse the actual

the company to make informed decision (Iravani, Akbari and Zohoori, 2017).

It assists the manager of Pharmacy2U co. about the hurdles and bottlenecks with the help

of constraint analysis technique. It analyses the impact of this in revenue-generating

capacity & profit of the company.

Rate of return technique of MA helps the manager in determining the most profitable

project or proposal. The project that give higher profit is selected.

Manager makes a decision regarding future capital investments of the company such as

fixed assets & equipment. These decisions are made with the help of capital budgeting

analysis that shows the capital availability of the company.

Conclusion on application of management accounting

The report has concluded that if Pharmacy2U company want to take various decision for

growth & success of the organization. With the earning of maximum profit then company need

to follow various MA system & methods. The report has examined in detail about the principles

of MA which directs the co. to follow right procedure. It has also studied about the role of MA &

its system. The report has also concluded about the various MA tools and functions with its

implementation in the Pharmacy2U industry. It has also researched about the benefits of

financial reporting & statements and critically evaluate the MA system & reporting.

PART 2

Comparison of three planning tools used in management accounting

Particulars Cost Accounting Marginal Costing Cash Flow Analysis

Meaning Cost accounting (CA)

is the process of

identifying the total

cost of production

including fixed cost or

variable cost. It helps

the managers in cost

Marginal costing is the

technique in which

only variable cost is

considered as the cost

of production. While

fixed cost is fully

written off against the

Cash flow analysis is a

technique that used to

know the cash inflows

and outflows of the co.

It is used by investors

and managers to

analyse the actual

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

controlling & making

various future decision

with the help of

comparing standard

cost with actual cost. It

deals with the cost of

production, selling &

distribution.

contribution. It

describes the

additional cost include

in producing a one

more extra unit.

Marginal costing is

also termed as

incremental cost

(NGUYEN and LE,

2020).

liquidity position of

the co. it mainly

includes three different

activities such as

operating activities,

financing activities

and investing

activities.

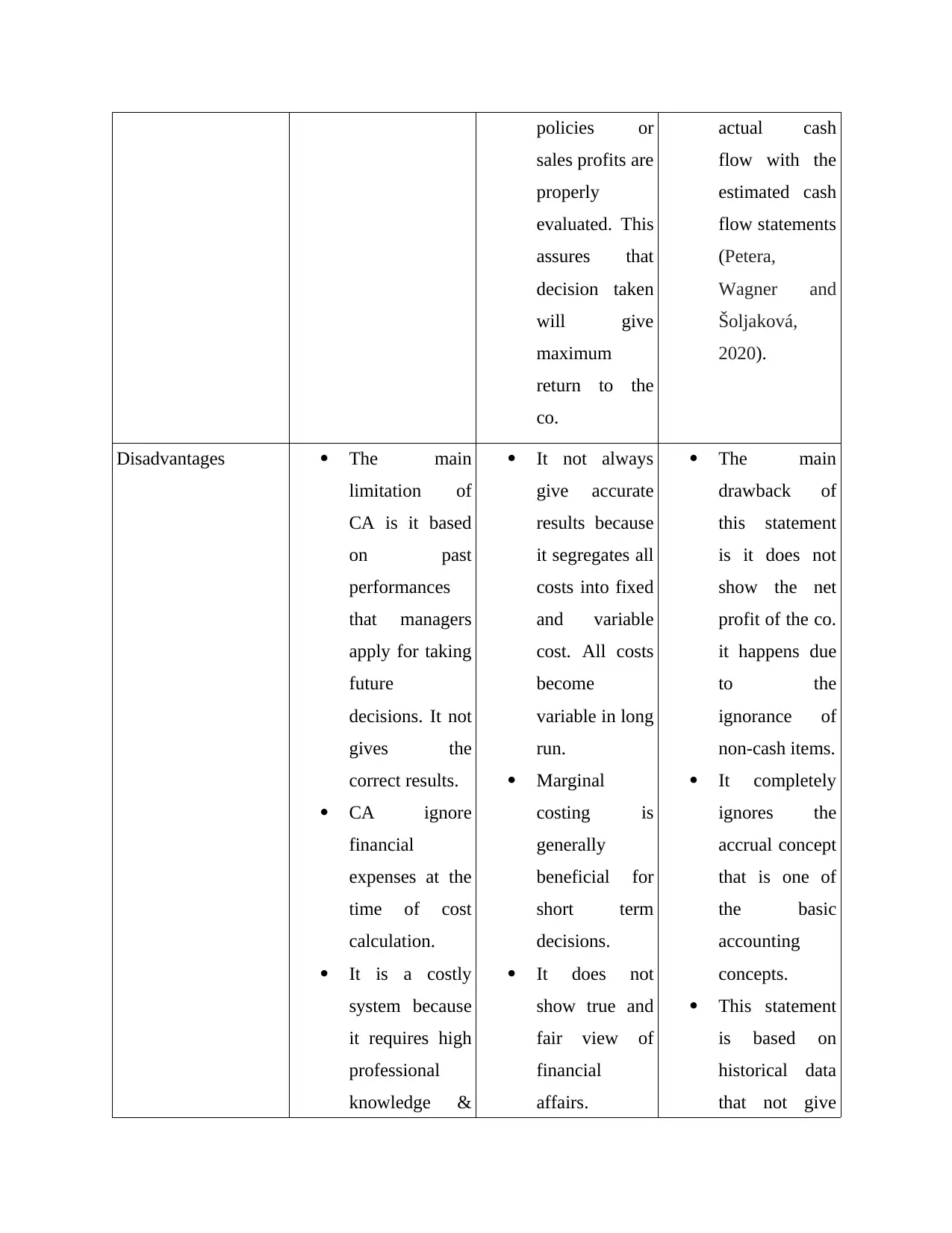

Advantages It helps the

manager in

identify future

prices of the

product.

Through CA

manager control

the excess stock

of materials. It

reduces wastage

(Devi and

Izzaty, 2021).

It directs the

manager to

analyse the

reasons of

losses and take

corrective

action to

improve them.

Marginal

costing helps to

evaluate and

control cost of

production. It

gives

opportunity to

co. to earn

more profits.

It helps in

formulating

short-term

profit planning

and various

decision-

making.

With marginal

costing

technique the

alternative

production

It eases

calculation of

the company

capability to

meet its daily

expenses.

It helps

management in

formulating of

financial

policies &

budgets for

future

investments.

It helps the

management to

show the

performance of

the co. on cash

basis. With

compare the

various future decision

with the help of

comparing standard

cost with actual cost. It

deals with the cost of

production, selling &

distribution.

contribution. It

describes the

additional cost include

in producing a one

more extra unit.

Marginal costing is

also termed as

incremental cost

(NGUYEN and LE,

2020).

liquidity position of

the co. it mainly

includes three different

activities such as

operating activities,

financing activities

and investing

activities.

Advantages It helps the

manager in

identify future

prices of the

product.

Through CA

manager control

the excess stock

of materials. It

reduces wastage

(Devi and

Izzaty, 2021).

It directs the

manager to

analyse the

reasons of

losses and take

corrective

action to

improve them.

Marginal

costing helps to

evaluate and

control cost of

production. It

gives

opportunity to

co. to earn

more profits.

It helps in

formulating

short-term

profit planning

and various

decision-

making.

With marginal

costing

technique the

alternative

production

It eases

calculation of

the company

capability to

meet its daily

expenses.

It helps

management in

formulating of

financial

policies &

budgets for

future

investments.

It helps the

management to

show the

performance of

the co. on cash

basis. With

compare the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

policies or

sales profits are

properly

evaluated. This

assures that

decision taken

will give

maximum

return to the

co.

actual cash

flow with the

estimated cash

flow statements

(Petera,

Wagner and

Šoljaková,

2020).

Disadvantages The main

limitation of

CA is it based

on past

performances

that managers

apply for taking

future

decisions. It not

gives the

correct results.

CA ignore

financial

expenses at the

time of cost

calculation.

It is a costly

system because

it requires high

professional

knowledge &

It not always

give accurate

results because

it segregates all

costs into fixed

and variable

cost. All costs

become

variable in long

run.

Marginal

costing is

generally

beneficial for

short term

decisions.

It does not

show true and

fair view of

financial

affairs.

The main

drawback of

this statement

is it does not

show the net

profit of the co.

it happens due

to the

ignorance of

non-cash items.

It completely

ignores the

accrual concept

that is one of

the basic

accounting

concepts.

This statement

is based on

historical data

that not give

sales profits are

properly

evaluated. This

assures that

decision taken

will give

maximum

return to the

co.

actual cash

flow with the

estimated cash

flow statements

(Petera,

Wagner and

Šoljaková,

2020).

Disadvantages The main

limitation of

CA is it based

on past

performances

that managers

apply for taking

future

decisions. It not

gives the

correct results.

CA ignore

financial

expenses at the

time of cost

calculation.

It is a costly

system because

it requires high

professional

knowledge &

It not always

give accurate

results because

it segregates all

costs into fixed

and variable

cost. All costs

become

variable in long

run.

Marginal

costing is

generally

beneficial for

short term

decisions.

It does not

show true and

fair view of

financial

affairs.

The main

drawback of

this statement

is it does not

show the net

profit of the co.

it happens due

to the

ignorance of

non-cash items.

It completely

ignores the

accrual concept

that is one of

the basic

accounting

concepts.

This statement

is based on

historical data

that not give

skill. Because it

excludes fixed

cost from

valuation of

stock that also

impact the

profit of the

company.

accurate

results.

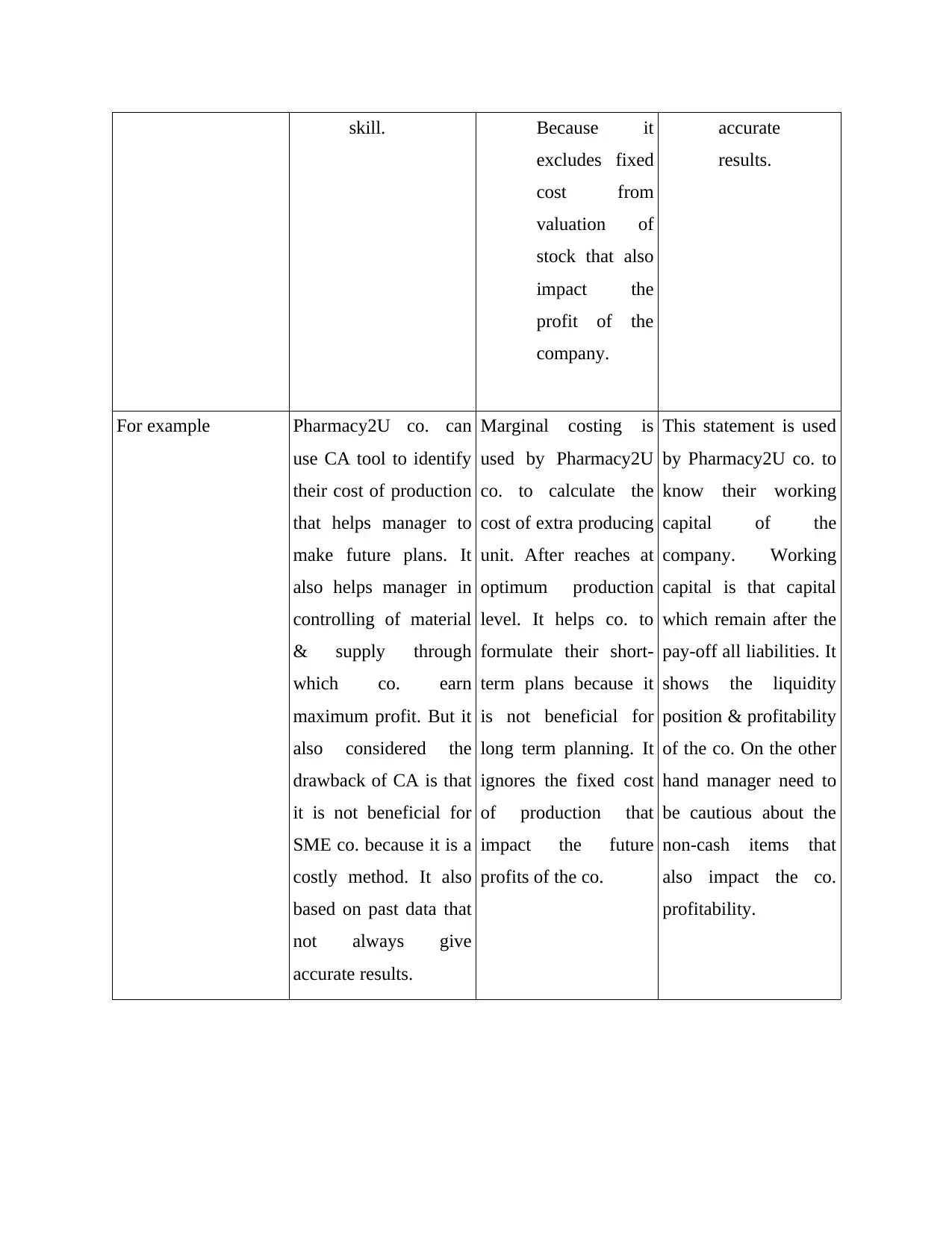

For example Pharmacy2U co. can

use CA tool to identify

their cost of production

that helps manager to

make future plans. It

also helps manager in

controlling of material

& supply through

which co. earn

maximum profit. But it

also considered the

drawback of CA is that

it is not beneficial for

SME co. because it is a

costly method. It also

based on past data that

not always give

accurate results.

Marginal costing is

used by Pharmacy2U

co. to calculate the

cost of extra producing

unit. After reaches at

optimum production

level. It helps co. to

formulate their short-

term plans because it

is not beneficial for

long term planning. It

ignores the fixed cost

of production that

impact the future

profits of the co.

This statement is used

by Pharmacy2U co. to

know their working

capital of the

company. Working

capital is that capital

which remain after the

pay-off all liabilities. It

shows the liquidity

position & profitability

of the co. On the other

hand manager need to

be cautious about the

non-cash items that

also impact the co.

profitability.

excludes fixed

cost from

valuation of

stock that also

impact the

profit of the

company.

accurate

results.

For example Pharmacy2U co. can

use CA tool to identify

their cost of production

that helps manager to

make future plans. It

also helps manager in

controlling of material

& supply through

which co. earn

maximum profit. But it

also considered the

drawback of CA is that

it is not beneficial for

SME co. because it is a

costly method. It also

based on past data that

not always give

accurate results.

Marginal costing is

used by Pharmacy2U

co. to calculate the

cost of extra producing

unit. After reaches at

optimum production

level. It helps co. to

formulate their short-

term plans because it

is not beneficial for

long term planning. It

ignores the fixed cost

of production that

impact the future

profits of the co.

This statement is used

by Pharmacy2U co. to

know their working

capital of the

company. Working

capital is that capital

which remain after the

pay-off all liabilities. It

shows the liquidity

position & profitability

of the co. On the other

hand manager need to

be cautious about the

non-cash items that

also impact the co.

profitability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.