Taxation Law Assignment: Mr. Phillips Land Sale and Taxation

VerifiedAdded on 2020/04/07

|10

|1777

|34

Homework Assignment

AI Summary

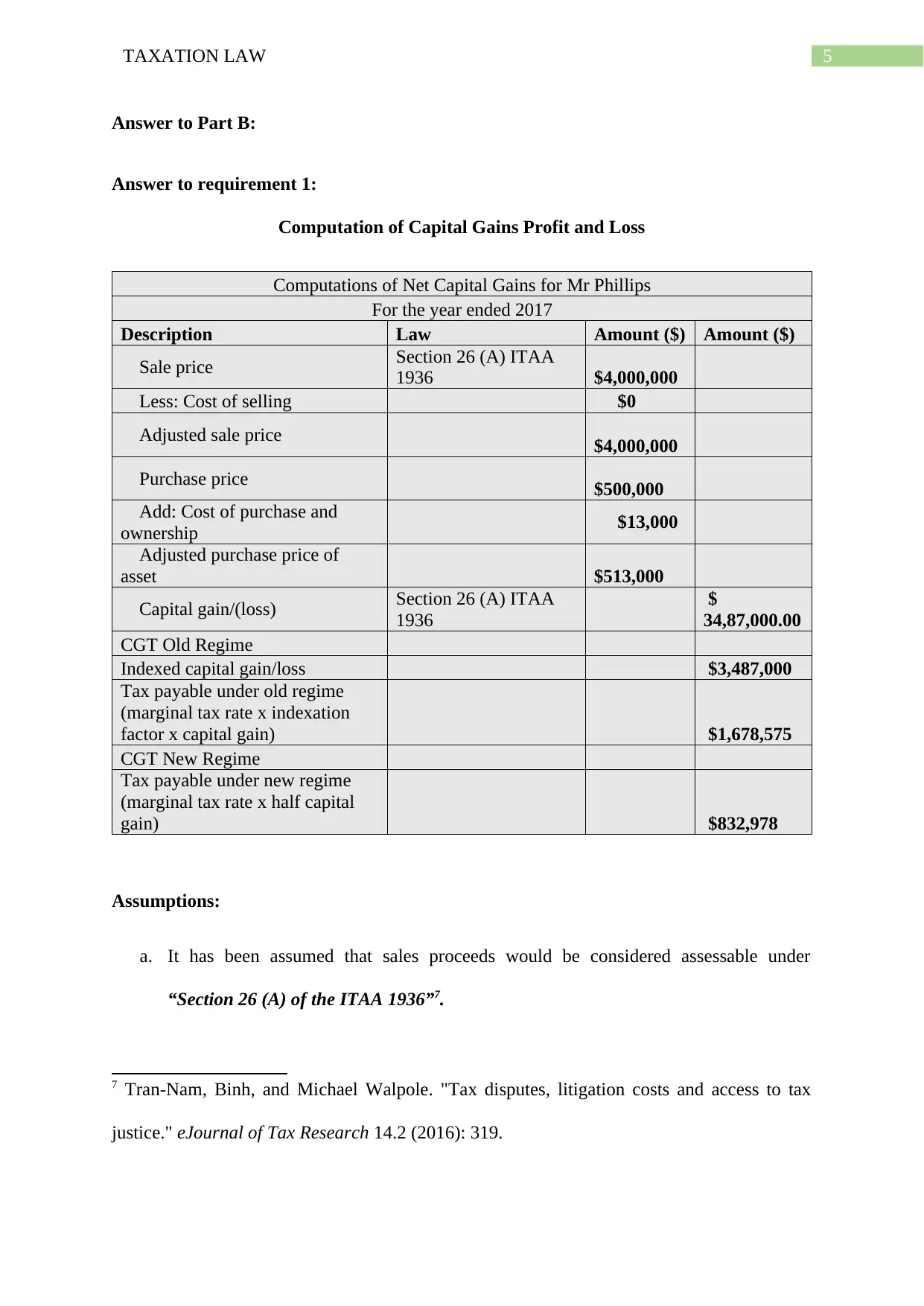

This assignment analyzes a taxation law case concerning Mr. Phillips and the sale of his land, exploring whether the transaction constitutes a mere realization or an isolated transaction subject to taxation under the ITAA 1936. It delves into the application of Taxation Ruling TR 92/3 and relevant case law, such as FC of T v The Myer Emporium Ltd (1987), to determine the tax implications. The assignment includes a capital gains tax (CGT) calculation under both old and new regimes, considering the sale price, purchase price, and associated costs. It also addresses the subdivision of land and its impact on CGT, referencing guidelines from the Australian Taxation Office and relevant sections of the ITAA 1997. The document concludes by determining whether the profits derived by Mr. Phillips would be assessed under Section 26 (a) and 25 (1) of the ITAA 1936, and includes a comprehensive reference list of relevant legal texts and rulings.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.