Assignment: Manage Physical Assets (Finance) - University Name

VerifiedAdded on 2023/06/06

|37

|6268

|409

Homework Assignment

AI Summary

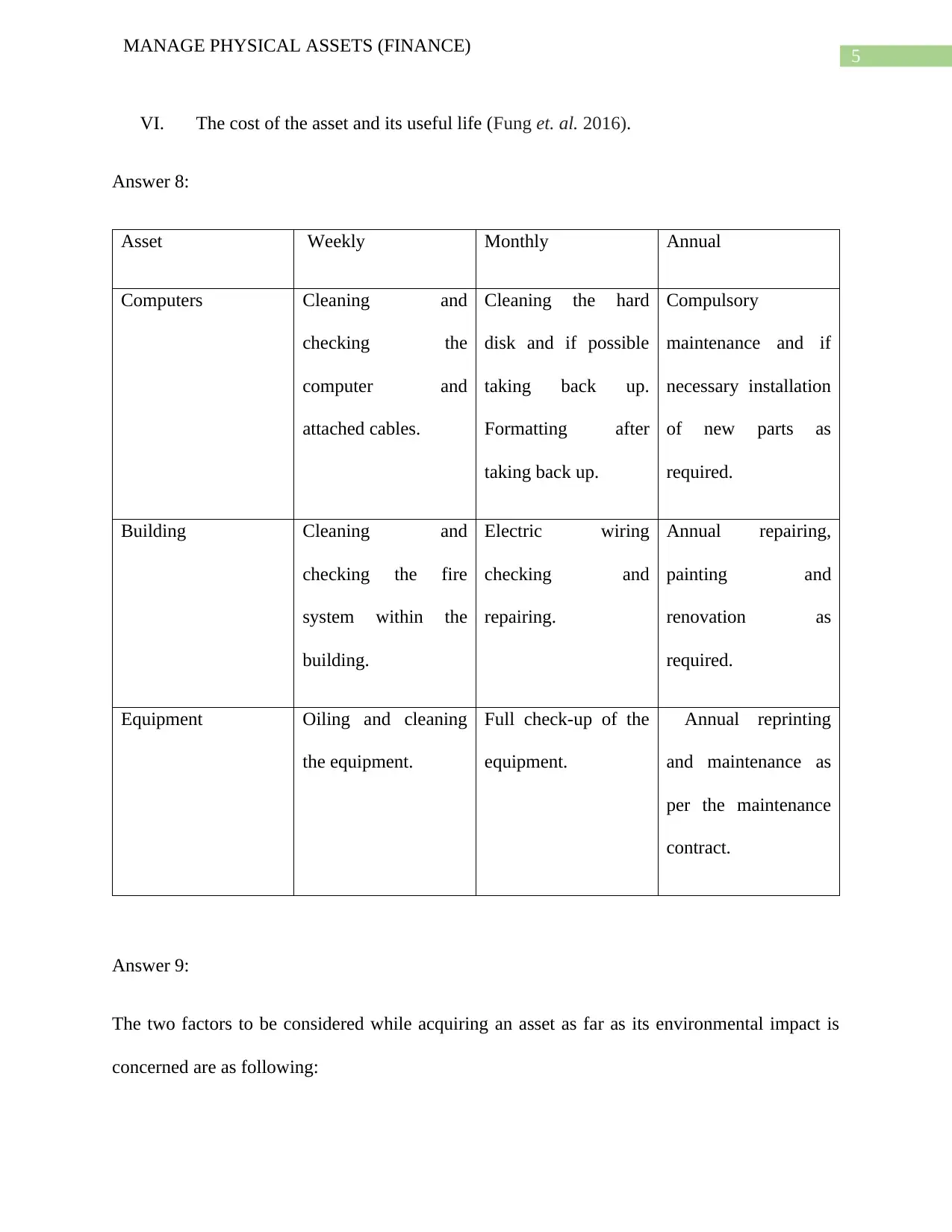

This assignment provides a comprehensive overview of managing physical assets within a financial framework. It begins by identifying various physical assets common in organizations, such as land, buildings, equipment, and vehicles. The assignment then explores the importance of asset registers, detailing the information they contain and the methods of depreciation applicable to different asset types. It delves into maintenance programs, comparing fix-on-fail, comprehensive, and preventive approaches, and outlines the factors to consider when establishing such programs. The assignment further examines environmental impacts, acquisition processes, and the role of financial statements in asset management decisions. It assesses the impact, effectiveness, and long-term performance of assets, along with techniques for reporting and identifying problems. The assignment also covers operational requirements, design specifications, supplier communication, and the benefits and drawbacks of asset purchases versus leasing, providing a thorough understanding of the financial aspects of physical asset management.

1 out of 37

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.