Pinkerton Case Solution: Financial Analysis and Recommendation

VerifiedAdded on 2023/06/04

|10

|658

|275

Case Study

AI Summary

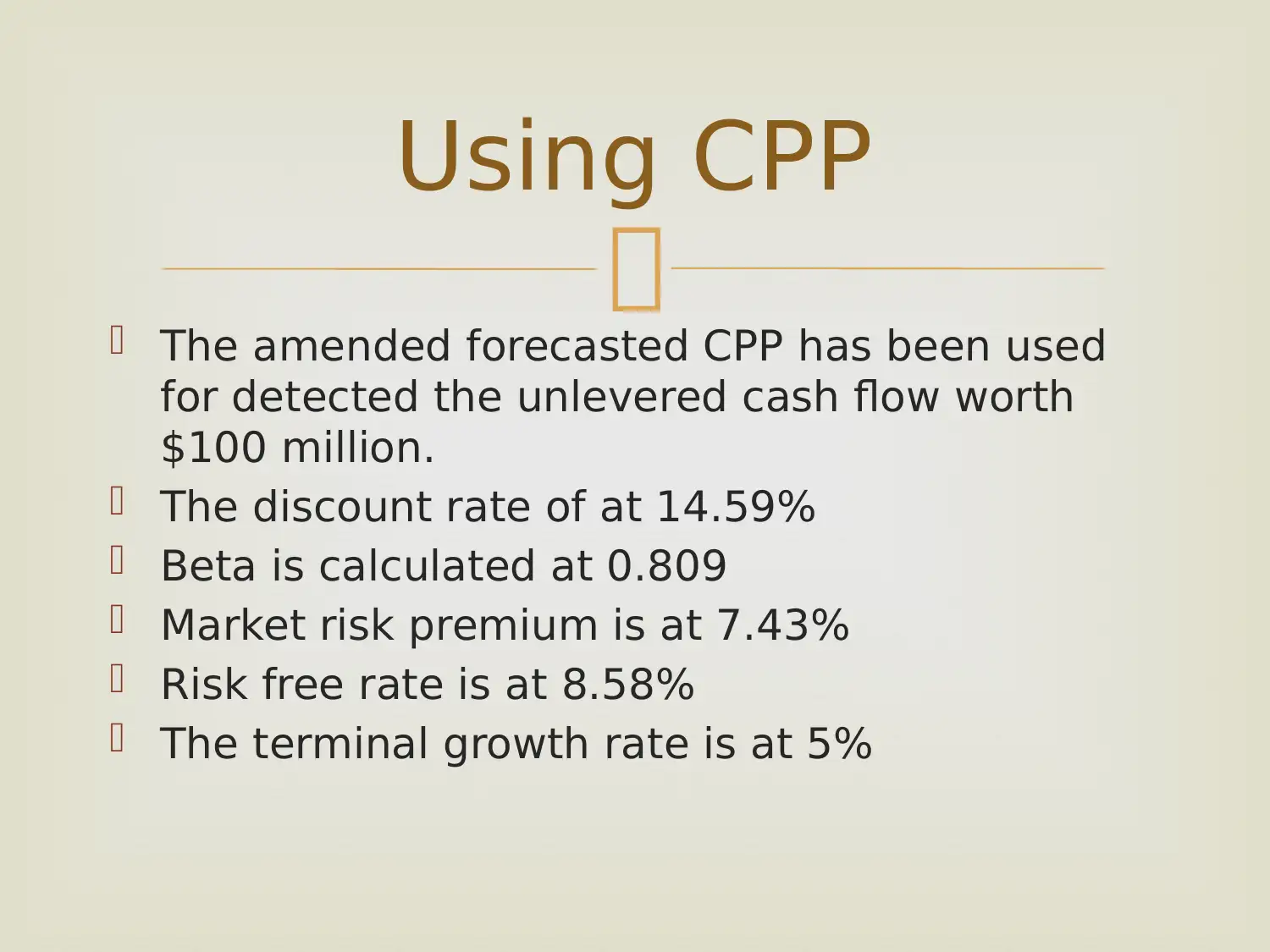

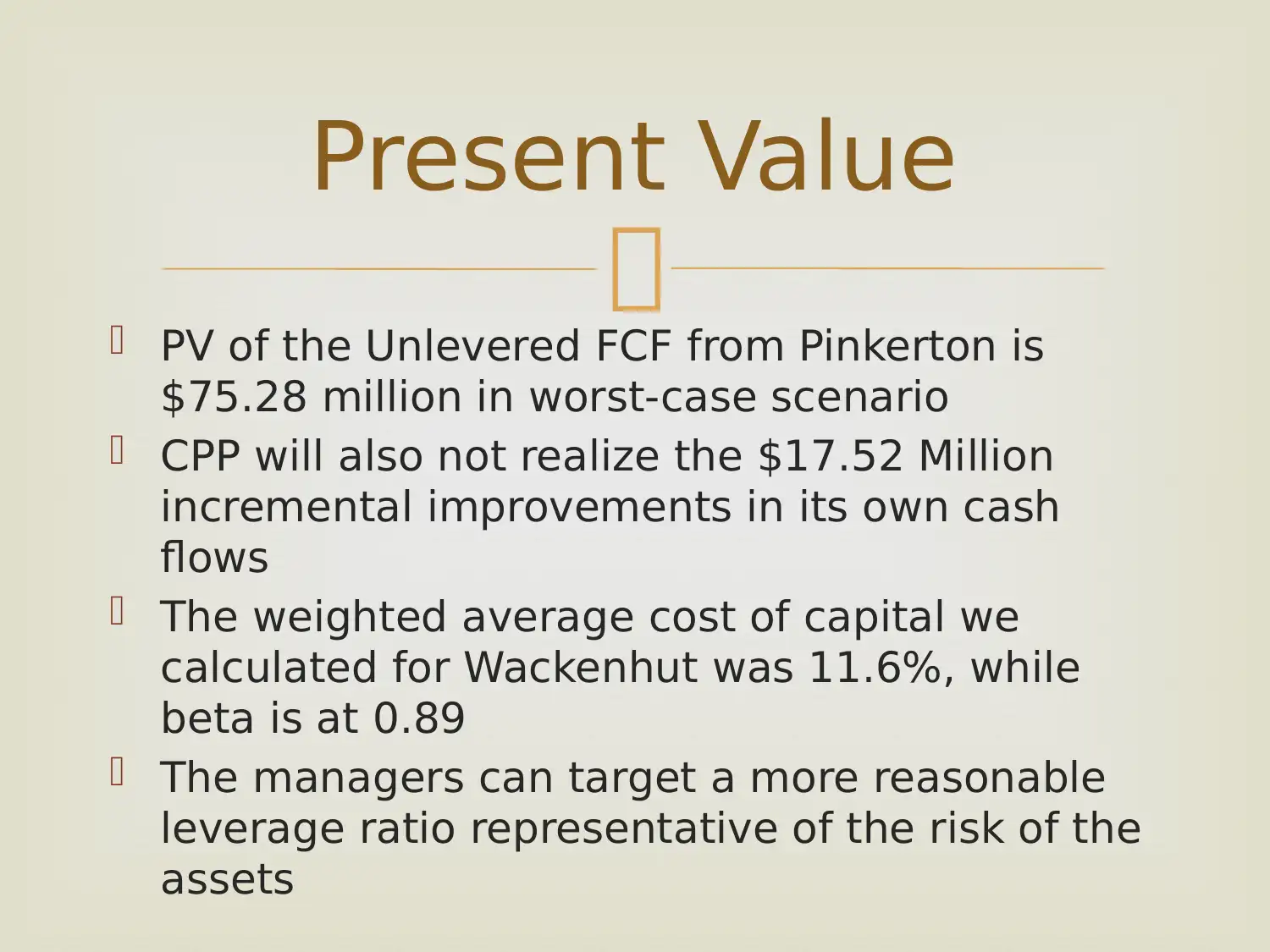

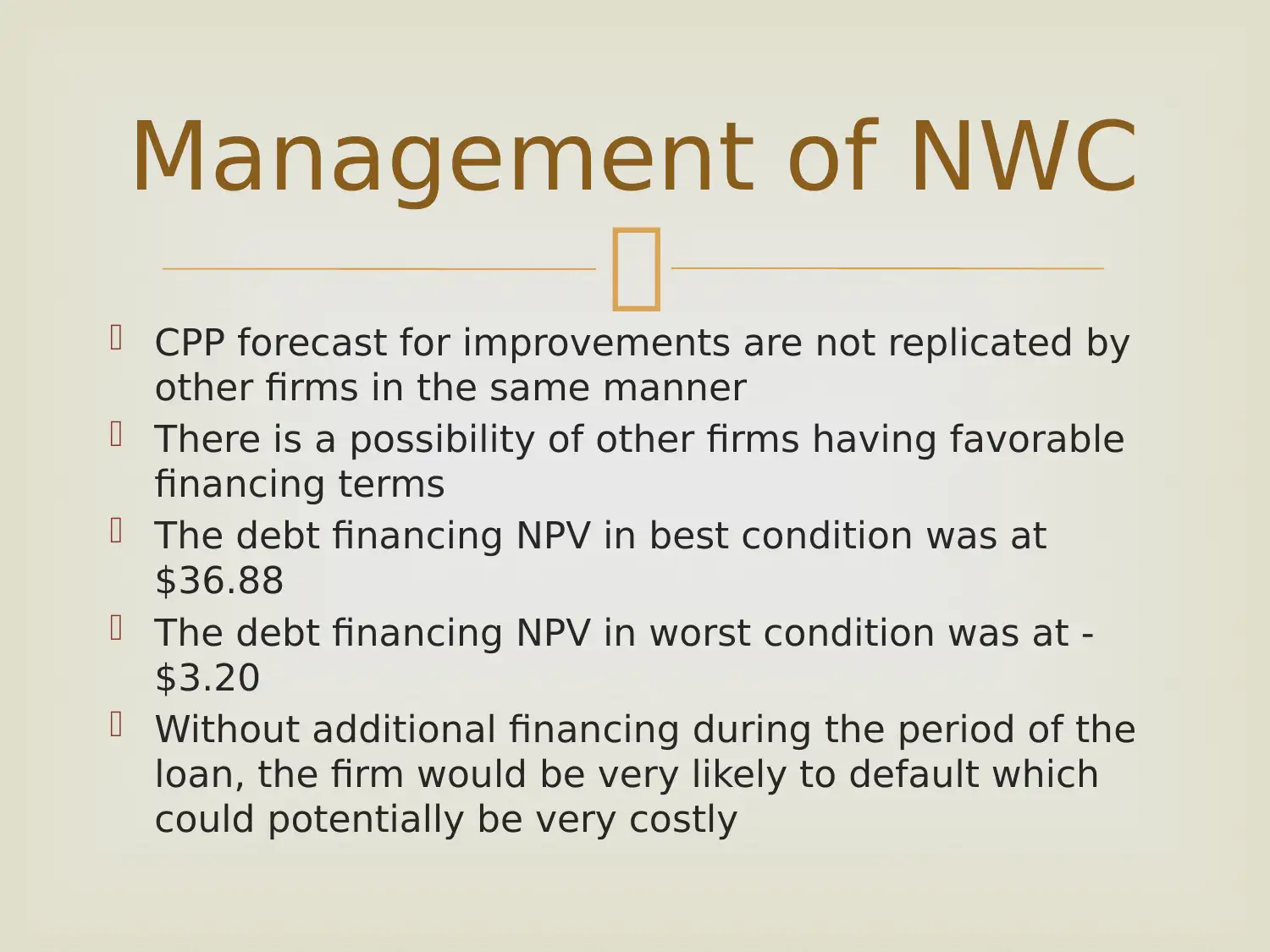

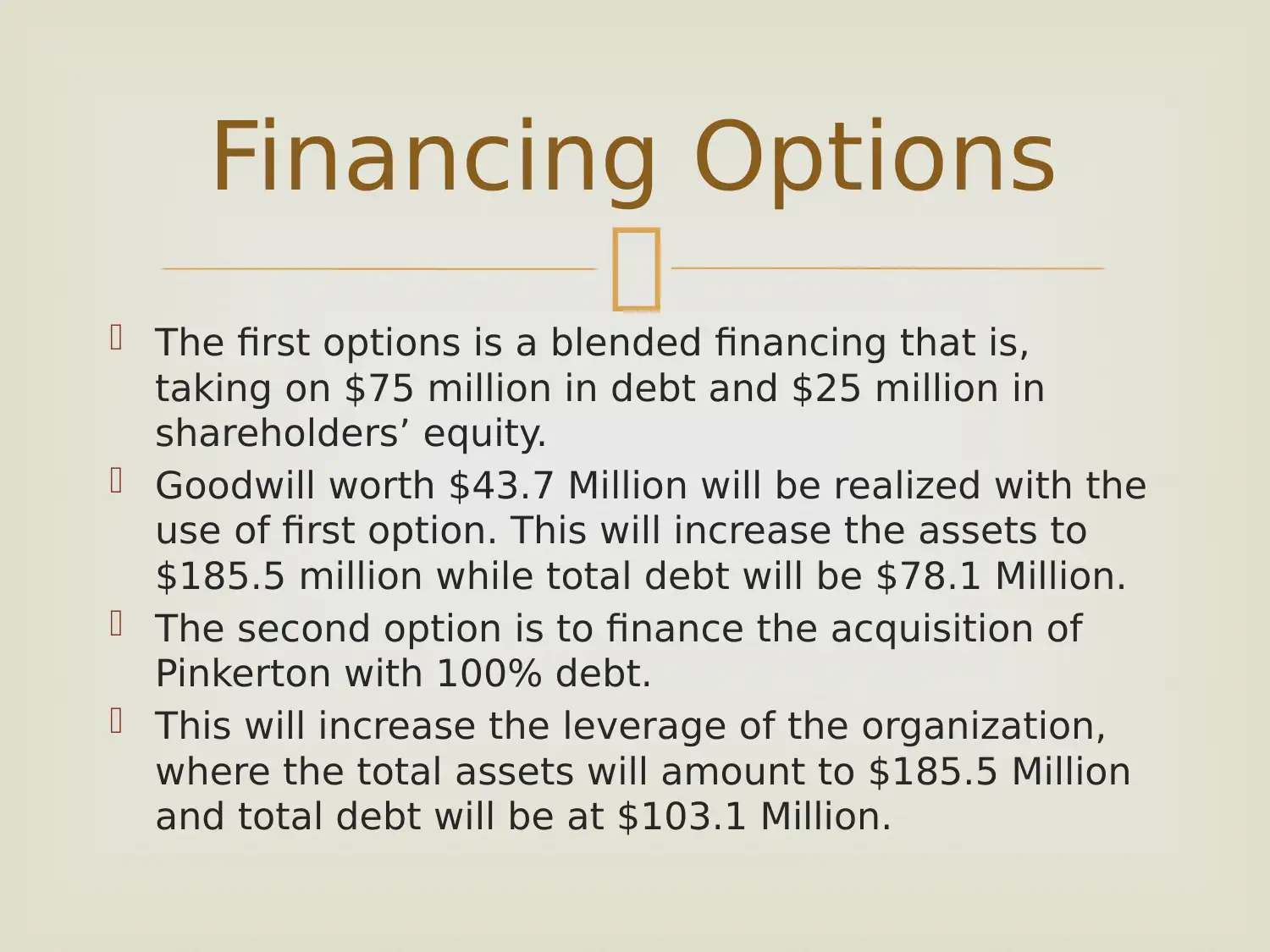

This case study solution analyzes the Pinkerton acquisition from a financial perspective, focusing on Wathen's strategic decisions. The analysis includes the calculation of the unlevered cash flow, discount rates, and the weighted average cost of capital (WACC) to determine the present value (PV) of the acquisition. The solution explores the impact of different financing options, including blended financing and 100% debt financing, on the net present value (NPV) and the company's leverage. It also examines the management of net working capital (NWC) and the potential risks associated with the forecasted improvements. The solution recommends renegotiating the offers and highlights the importance of considering various loan structures to mitigate risks and maximize the NPV. Finally, the analysis also emphasizes the importance of understanding the impact of tax and operational profits and making a final recommendation based on the analysis.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.