Evaluation of Pinto Limited's Project: Financial Analysis Report

VerifiedAdded on 2021/05/30

|7

|1337

|32

Report

AI Summary

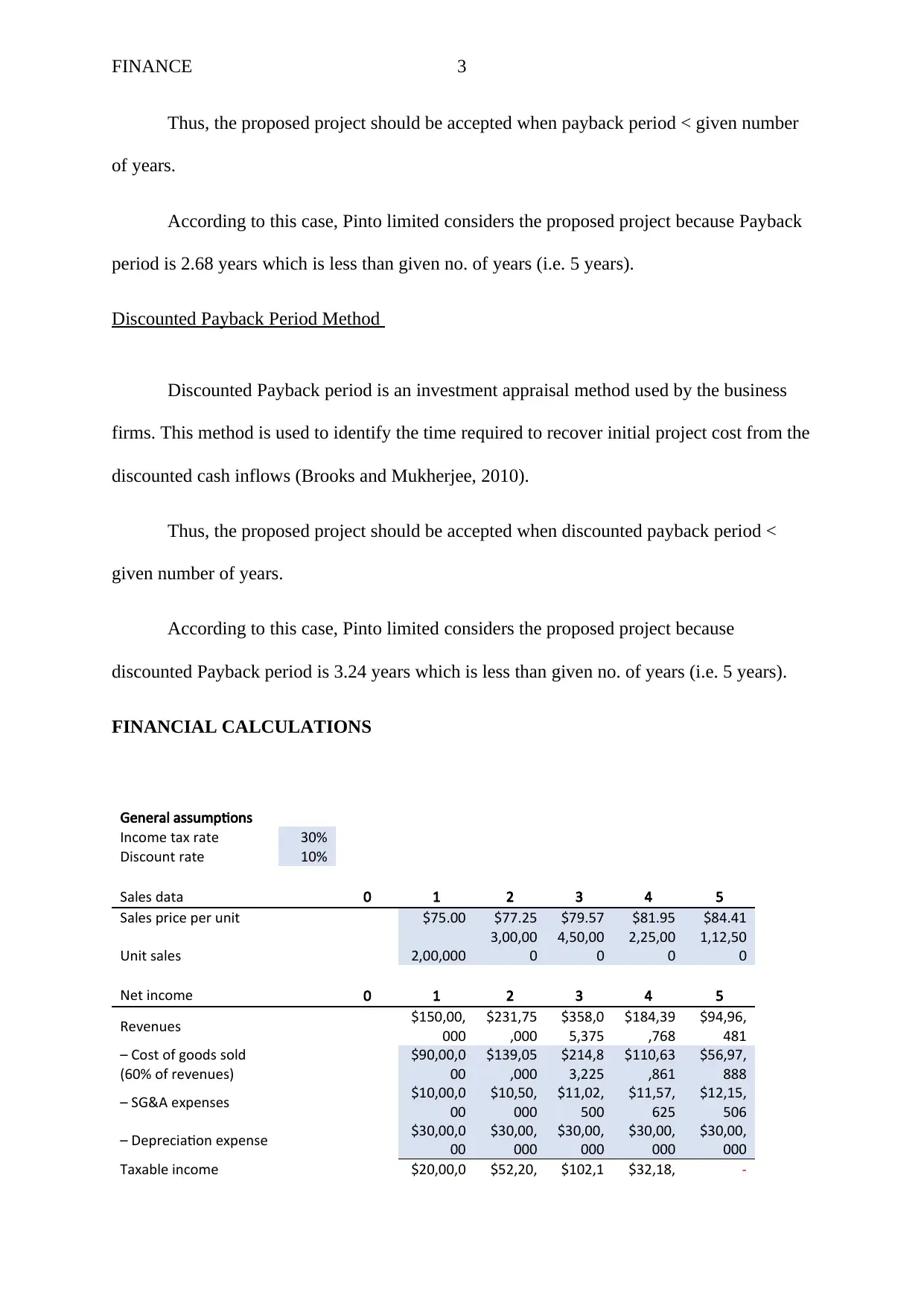

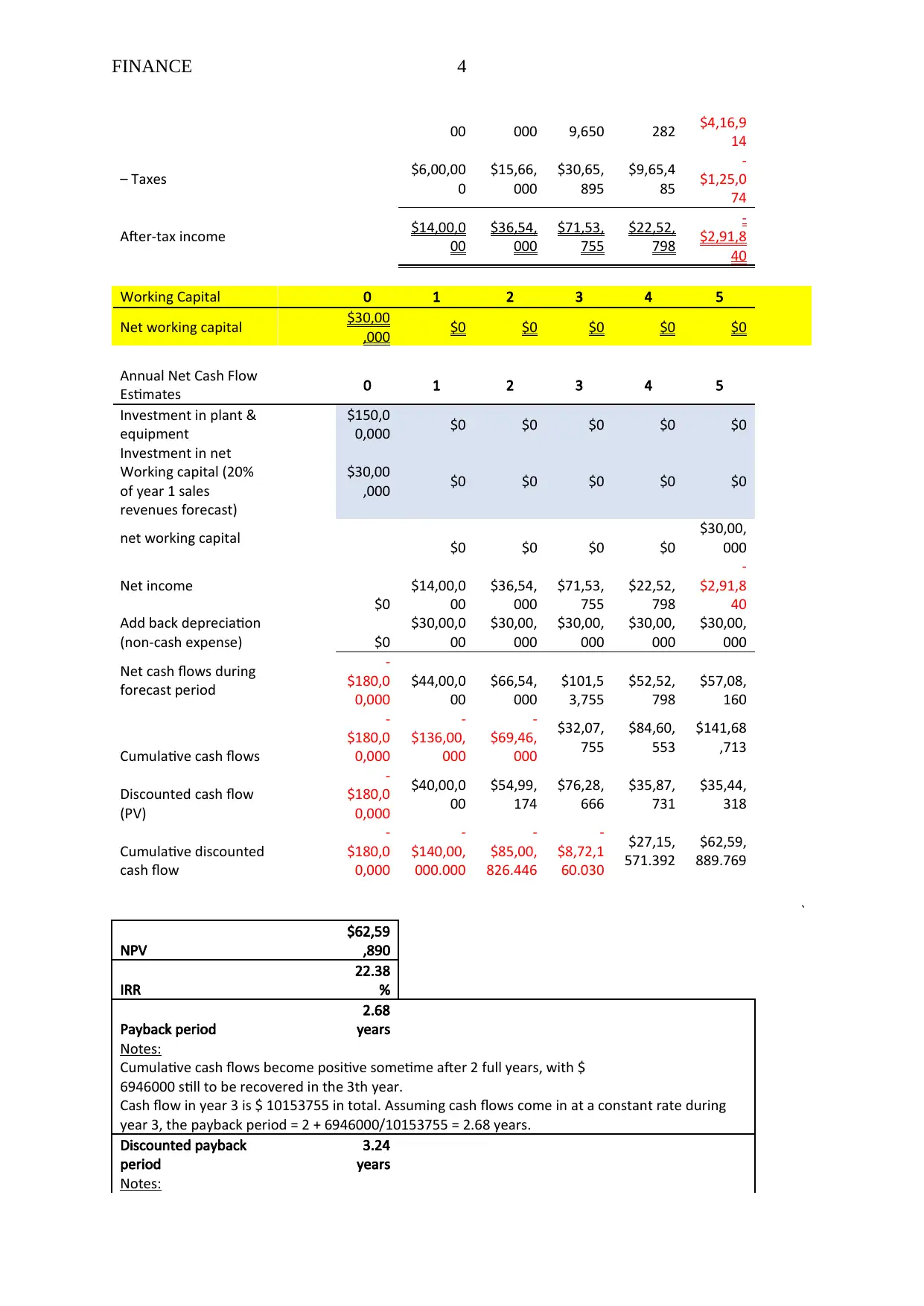

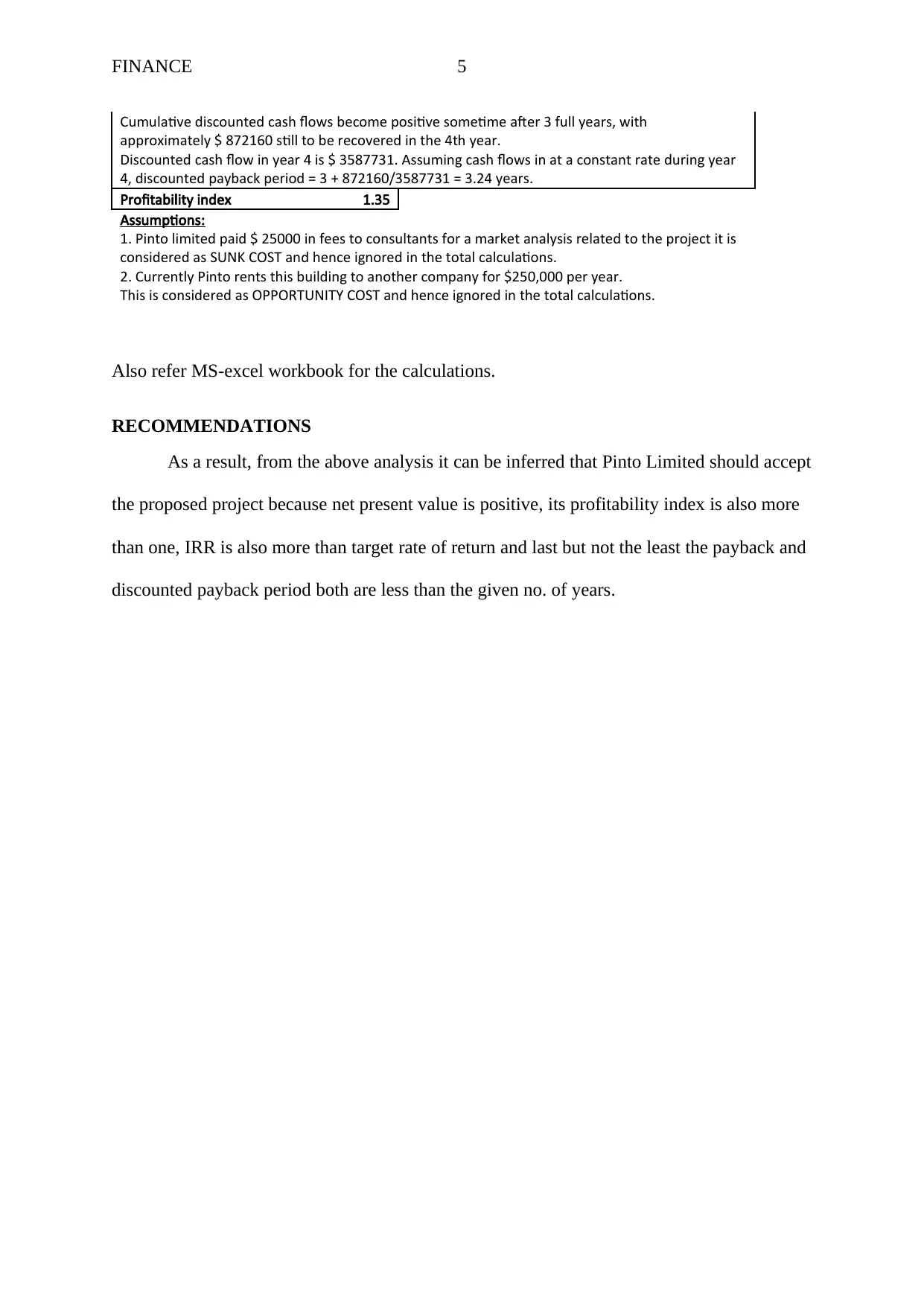

This report evaluates a prospective project for Pinto Limited through a comprehensive financial analysis. It employs several investment appraisal methods, including Net Present Value (NPV), Internal Rate of Return (IRR), Profitability Index (PI), Payback Period, and Discounted Payback Period. The analysis includes detailed financial calculations, such as sales data, cost of goods sold, SG&A expenses, depreciation, and tax implications, to determine net income and cash flows over a five-year period. The report presents the calculations for each method, providing insights into the project's financial viability and profitability. The analysis concludes with recommendations based on the results obtained from each method, with the final recommendation that Pinto Limited should accept the proposed project based on its positive NPV, PI greater than one, IRR exceeding the target rate of return, and acceptable payback periods.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.