ACC00716 Finance: Investment Appraisal of Pinto Limited Project

VerifiedAdded on 2023/06/12

|8

|1837

|213

Report

AI Summary

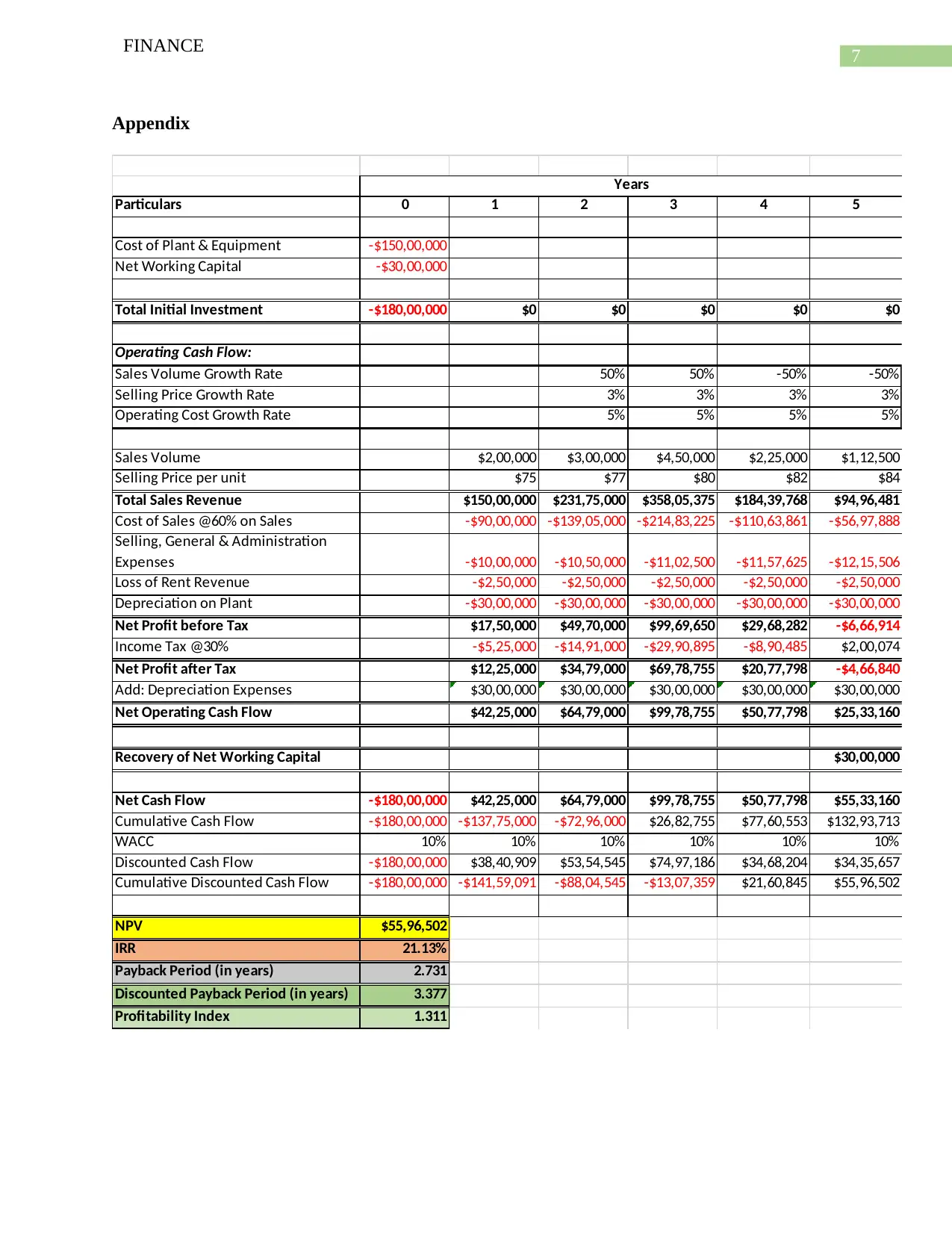

This report presents a financial analysis of Pinto Limited's proposed project, which involves entering a new product market. The analysis employs various capital budgeting techniques, including NPV, Profitability Index, Payback Period, Discounted Payback Period, and IRR, to assess the project's viability. The initial investment required is $180 million, covering plant and machinery and additional working capital. The analysis assumes increases in sales volume, sales price, and operating costs. The findings suggest that the project is financially sound, with a positive NPV of $55,96,502, a favorable Profitability Index, a payback period of 2.731 years, a discounted payback period of 3.377 years, and an IRR of 21.13%. The report recommends that Pinto Limited proceed with the project, while also suggesting strategies to enhance its profitability, such as cost reduction and aggressive sales strategies. Desklib provides students access to similar solved assignments.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.