Detailed Capital Budgeting Analysis for Pinto Ltd Project

VerifiedAdded on 2021/06/17

|6

|1206

|31

Report

AI Summary

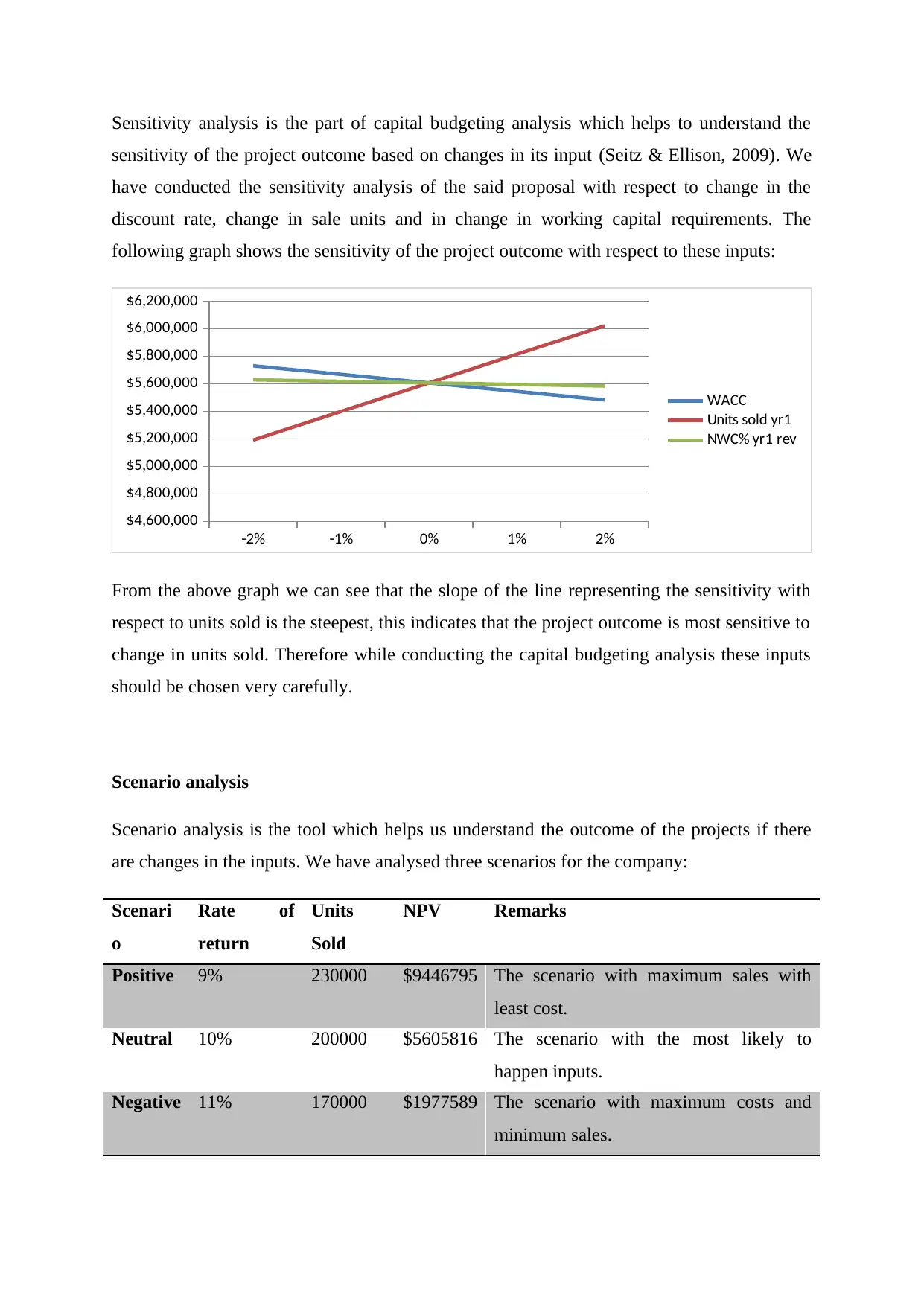

This report, addressed to the CEO of Pinto Limited, presents a comprehensive capital budgeting analysis of a proposed project. The analysis includes base case evaluations using metrics such as Net Present Value (NPV), Payback Period, Discounted Payback Period, Profitability Index (PI), and Internal Rate of Return (IRR). The report also incorporates uncertainty analysis, sensitivity analysis (examining the impact of changes in discount rate, sales units, and working capital), and scenario analysis to assess the project's robustness under different conditions. The conclusion, based on the detailed financial analysis and the positive outcomes across various metrics, is a recommendation to accept the proposed project, as it is expected to generate positive cash flows and returns exceeding the costs, provided the assumptions made hold true.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.