Financial Feasibility Report: Pinto Ltd Machinery Investment Analysis

VerifiedAdded on 2021/12/16

|5

|1541

|75

Report

AI Summary

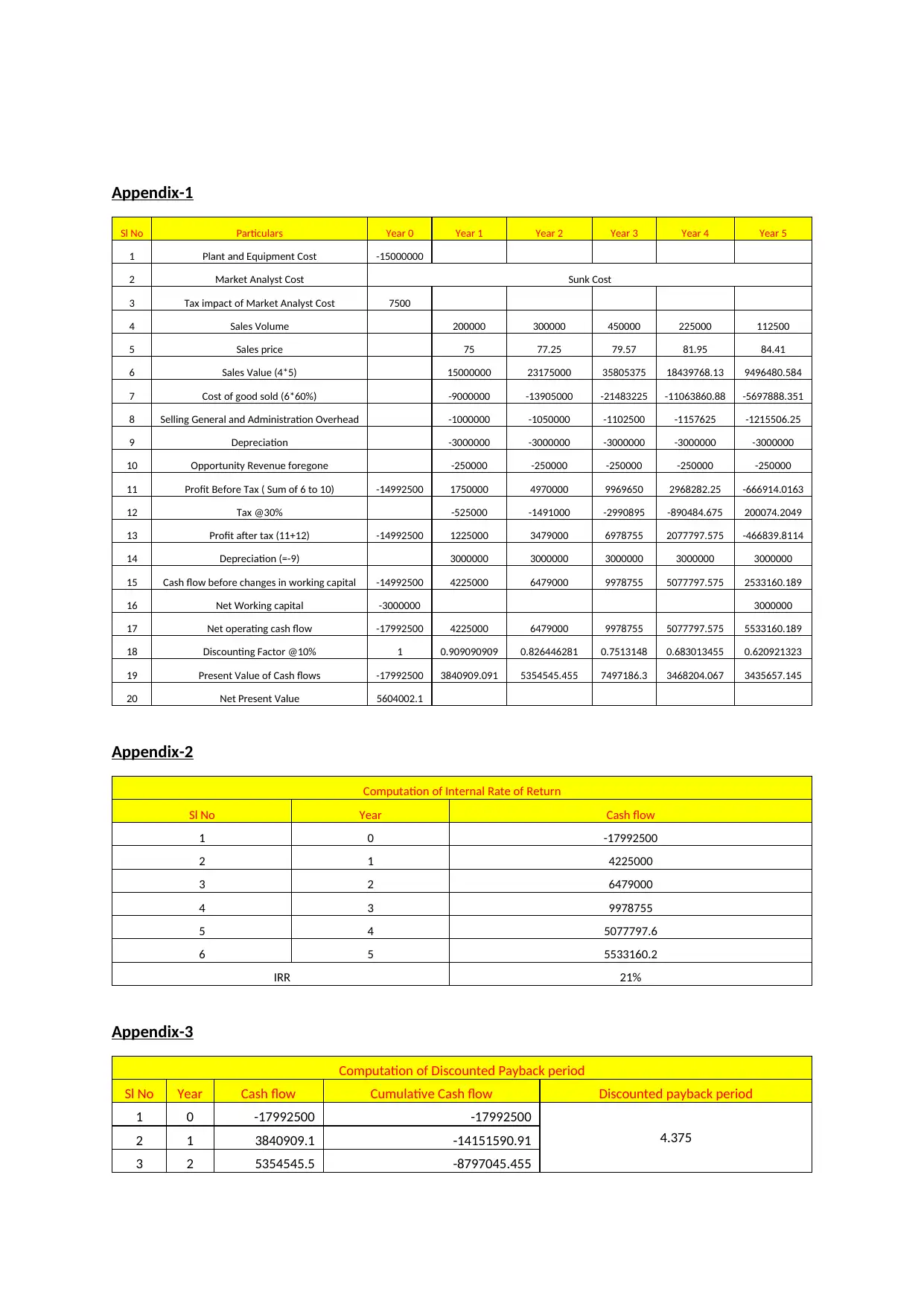

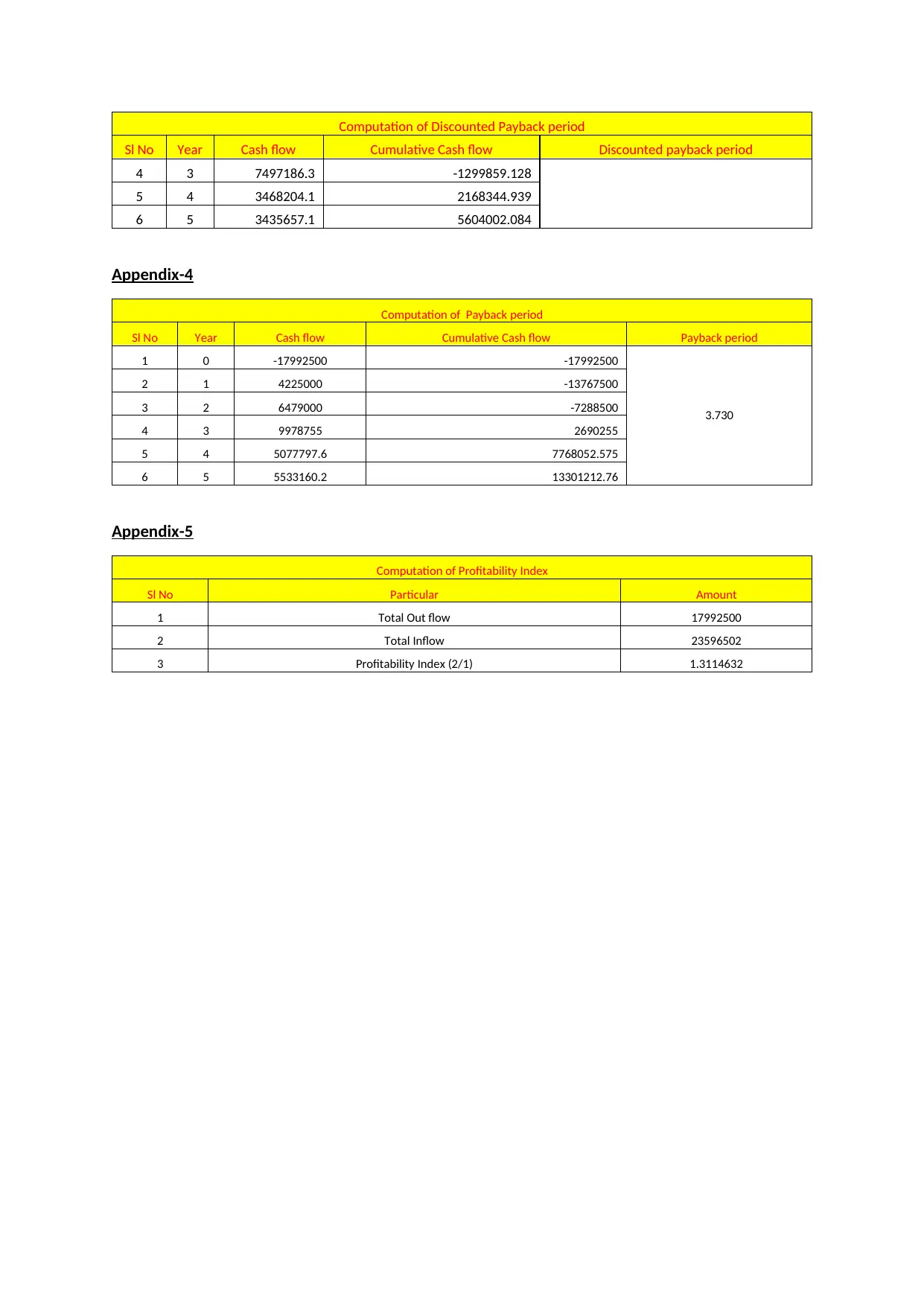

This report presents a financial analysis of Pinto Limited's proposed machinery investment, undertaken to combat competition. The analysis employs several financial tools, including Net Present Value (NPV), Internal Rate of Return (IRR), Payback Period, Discounted Payback Period, and Profitability Index, to assess the project's feasibility. Assumptions include an initial investment of $15 million, a 5-year project life, and projections for sales volume, sales price, cost of goods sold, and operating expenses. The analysis calculates an NPV of $5,604,002, an IRR of 21%, a discounted payback period of 4.38 years, a payback period of 3.73 years, and a profitability index of 1.32, leading to a conclusion that the project is financially viable and should be accepted. The detailed computations for each financial metric are provided in the appendices, offering a comprehensive assessment of the investment's potential.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.