Business Finance Report: 10-in and 12-in Pipe Production Analysis

VerifiedAdded on 2020/03/16

|16

|3033

|49

Report

AI Summary

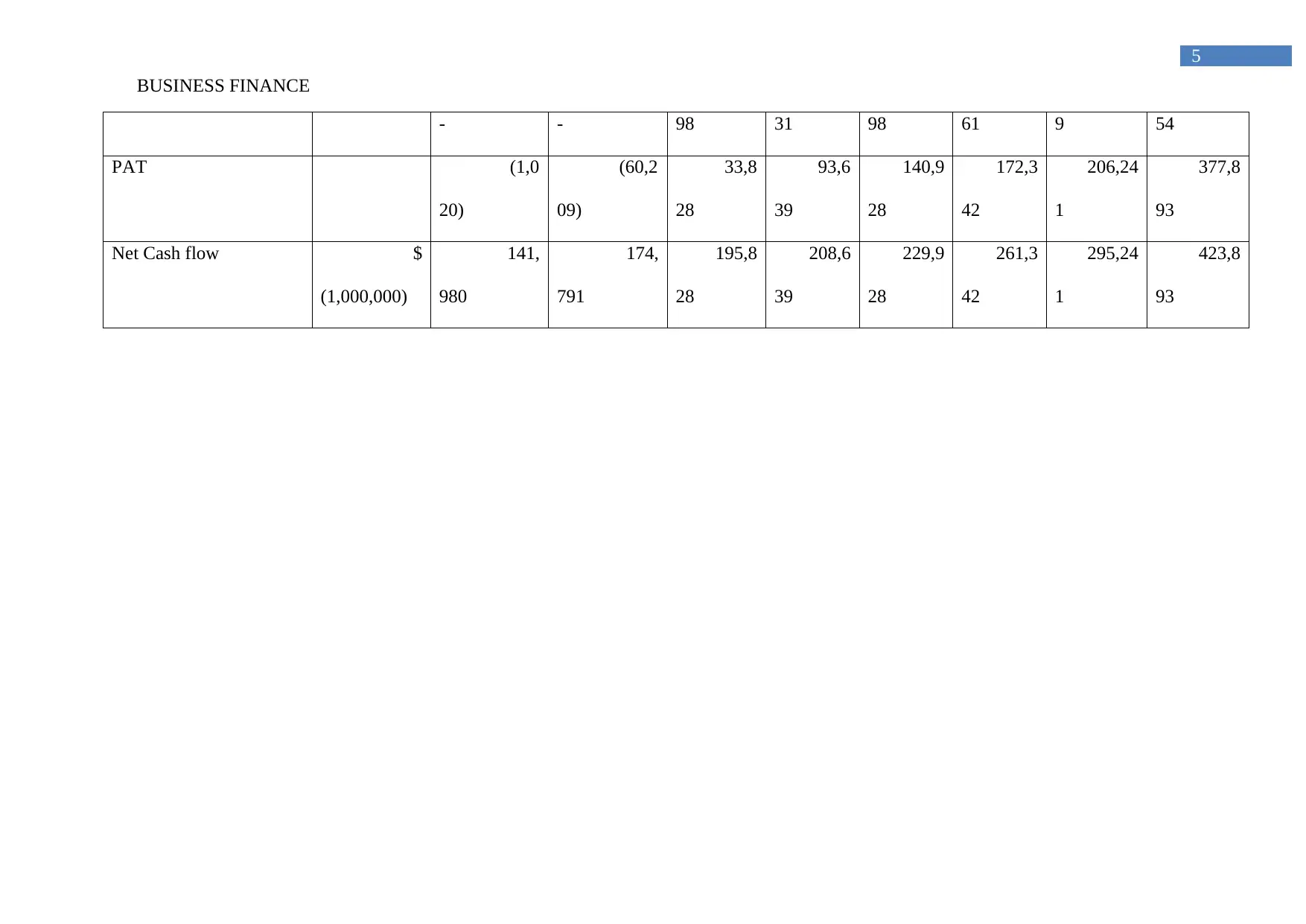

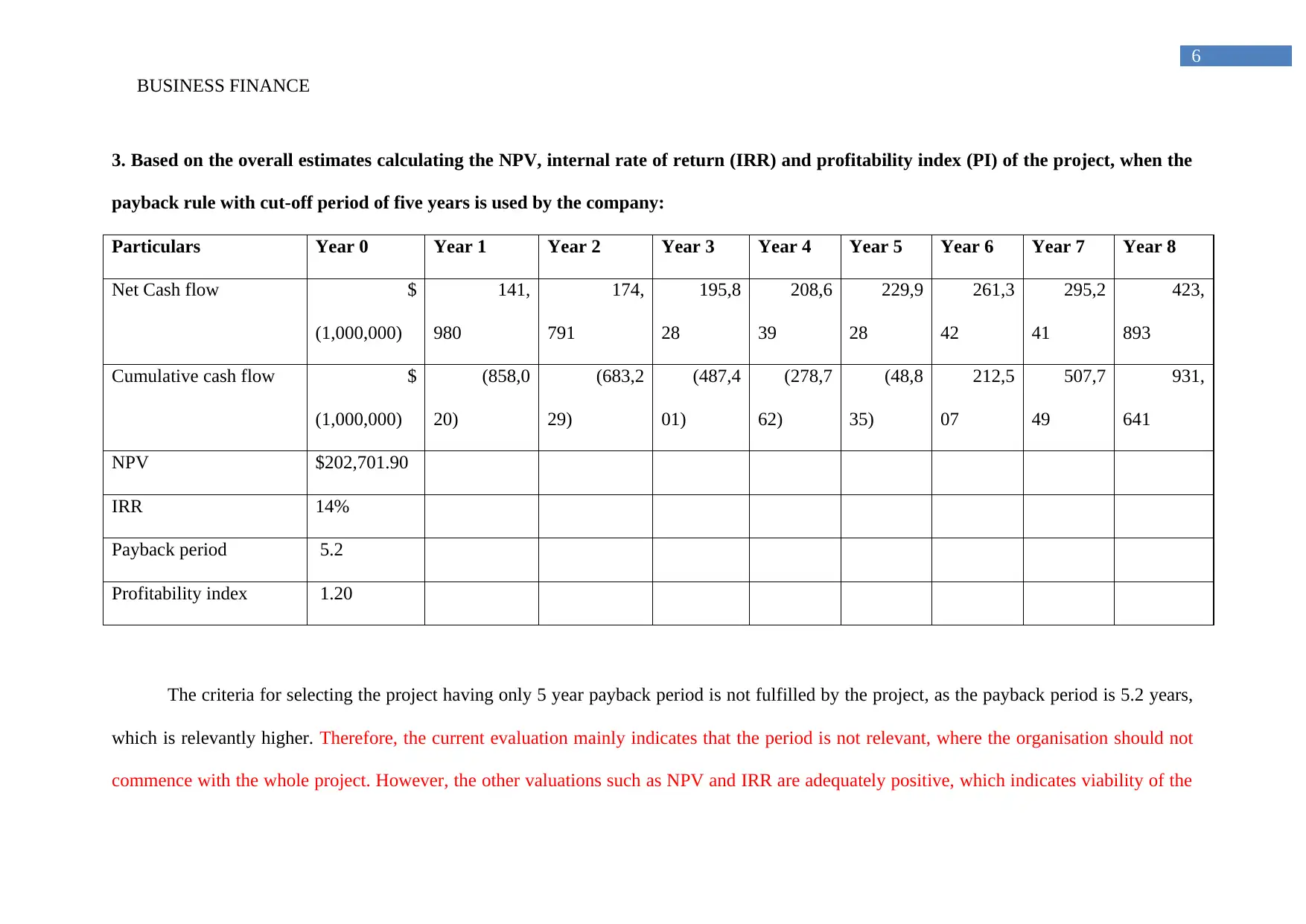

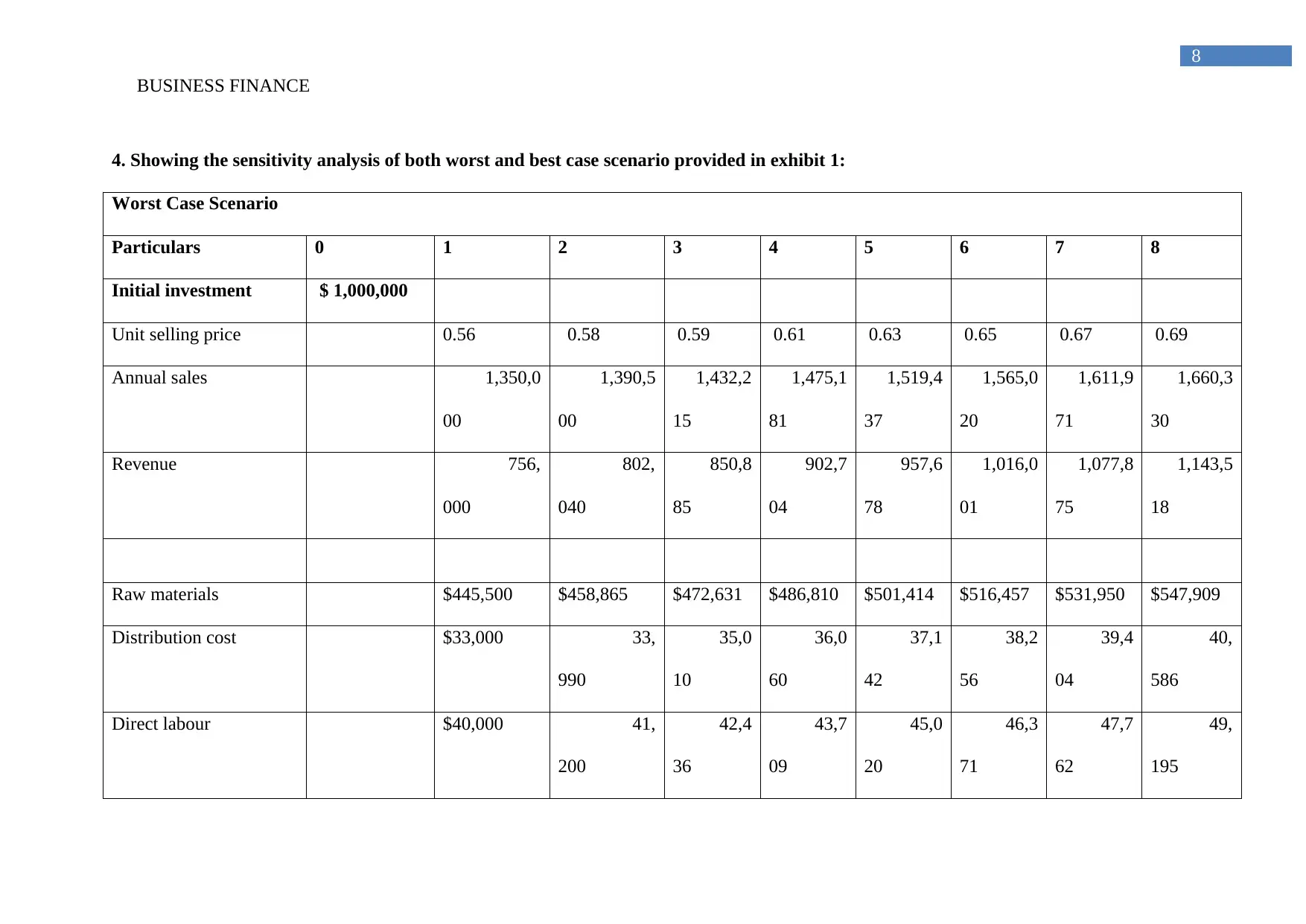

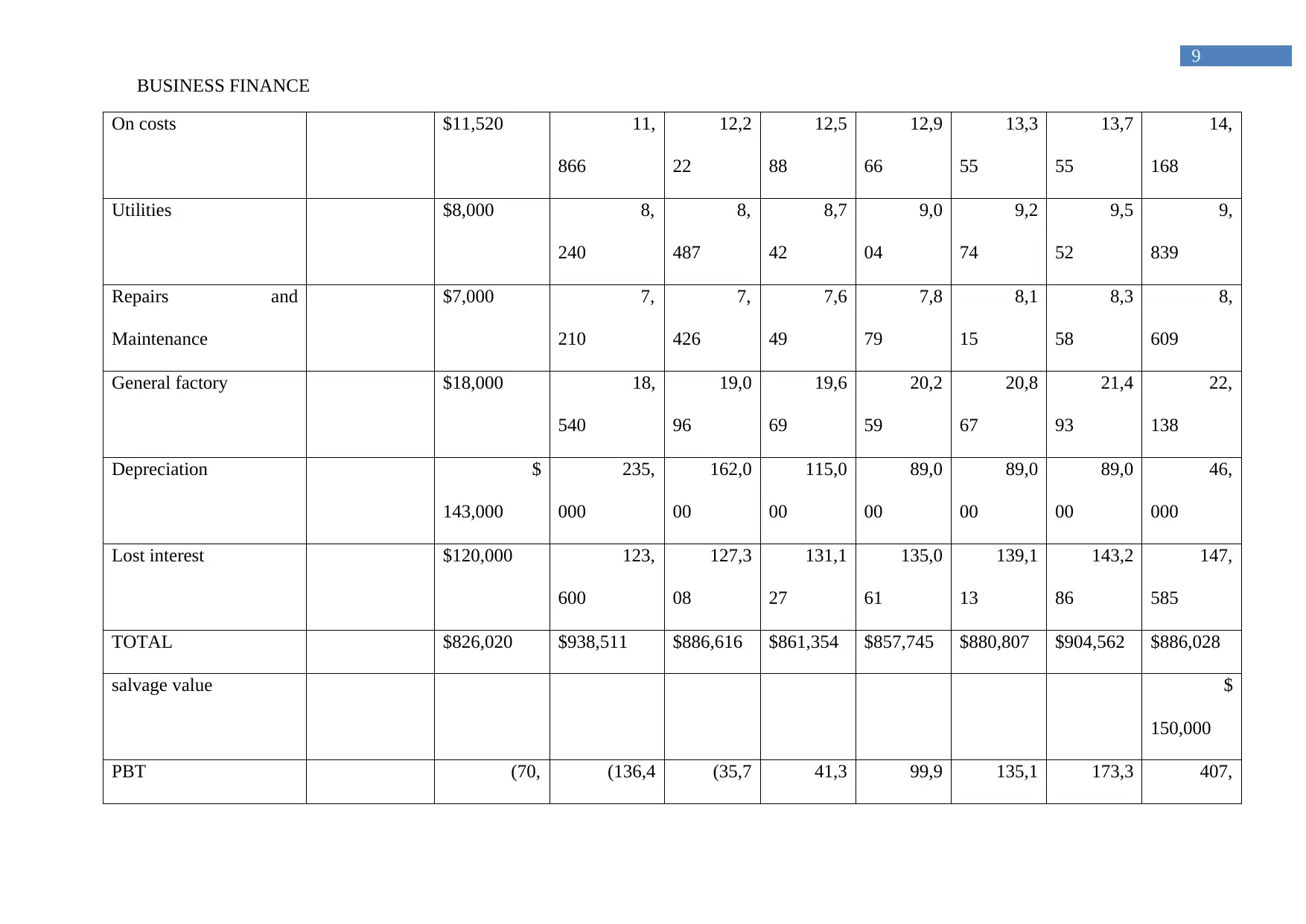

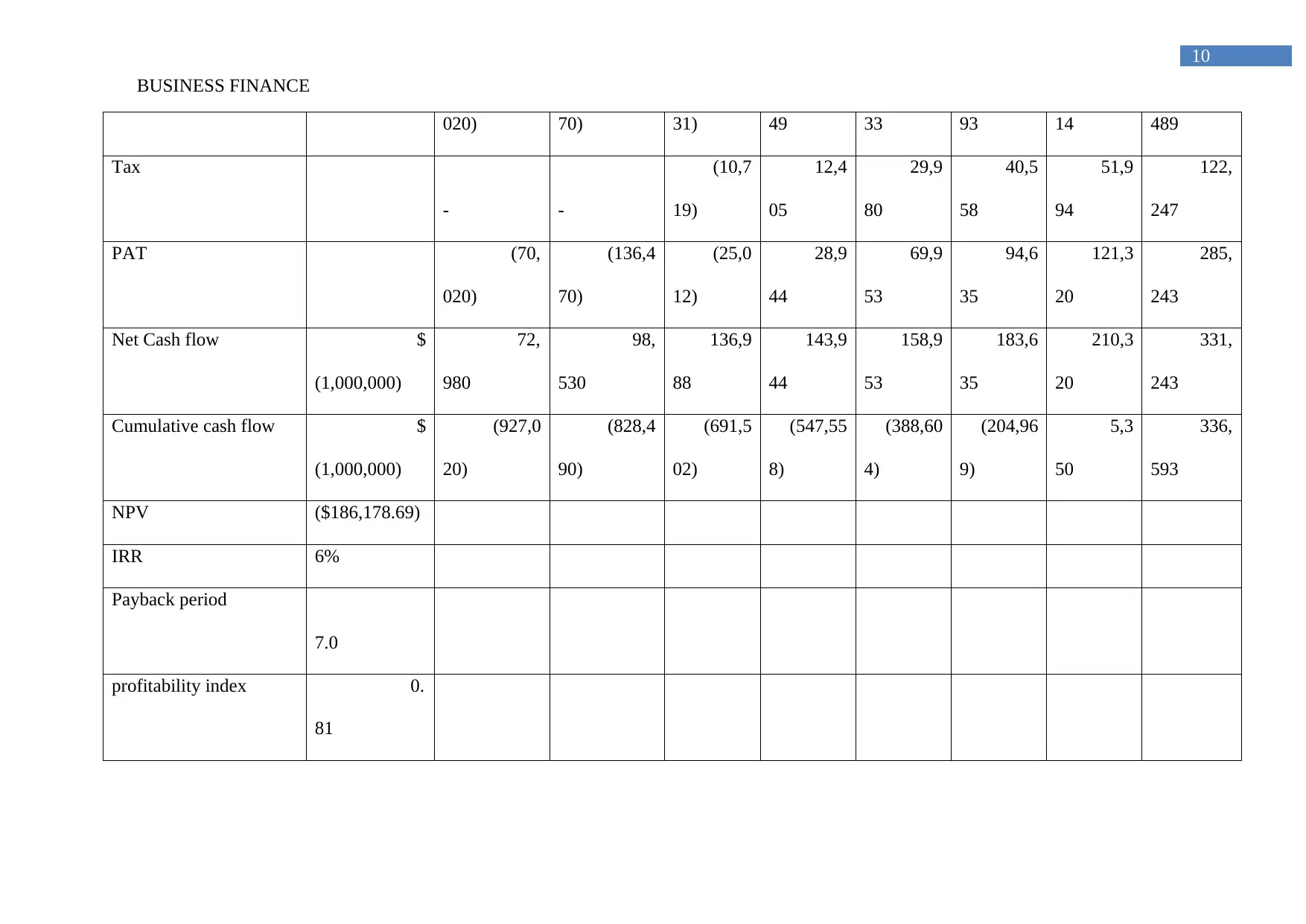

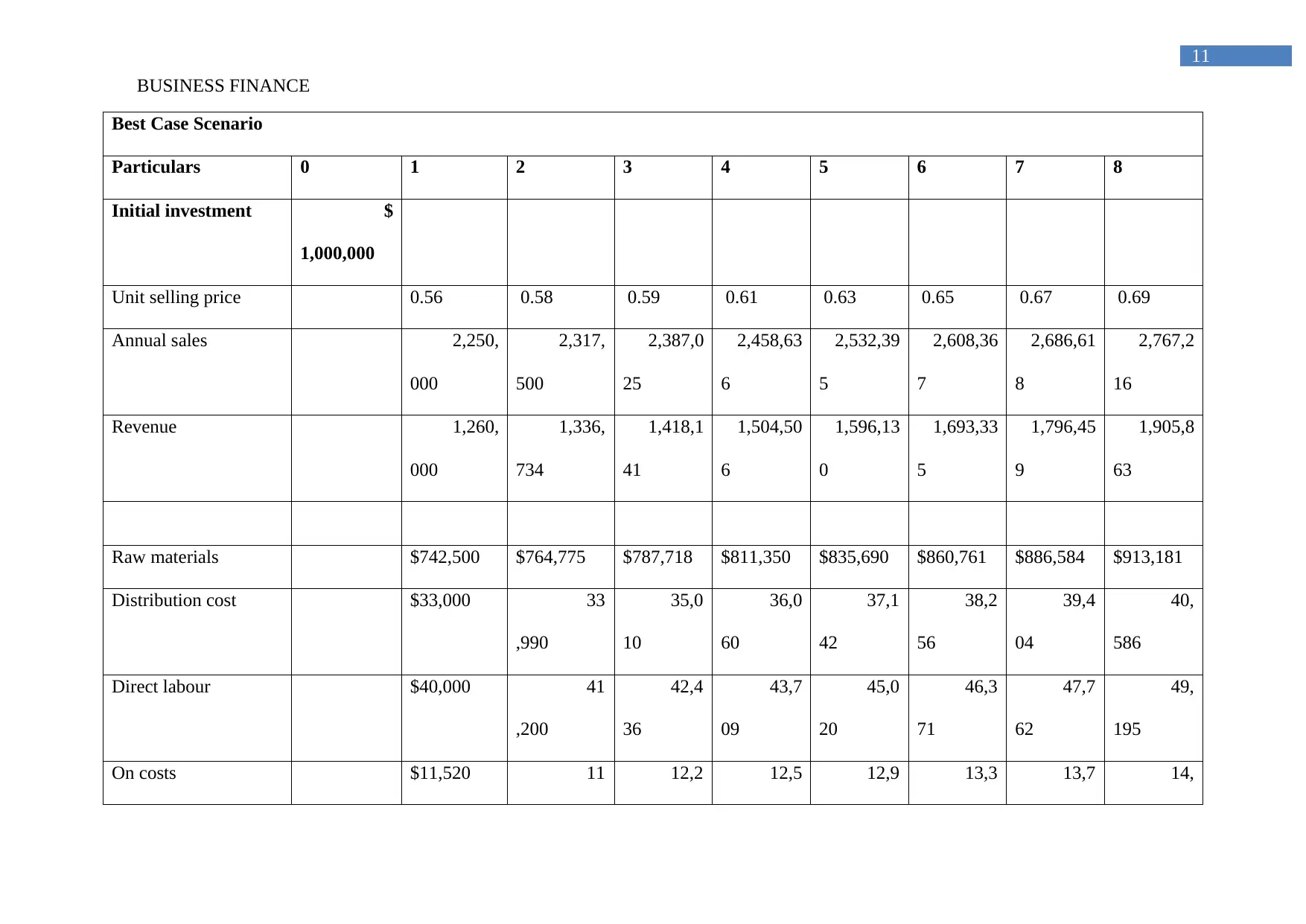

This report presents a comprehensive financial analysis of a proposed pipe production project, evaluating its viability through various investment appraisal techniques. The analysis includes the identification of omitted items, preparation of incremental cash flow tables under the most likely scenario, and calculation of Net Present Value (NPV), Internal Rate of Return (IRR), and Profitability Index (PI). Furthermore, sensitivity analyses were conducted to assess worst and best-case scenarios. The report also derives expected sales, standard deviation, and coefficient of variation from sales quantity data. Recommendations are provided regarding the production of 10-in and 12-in pipes, considering the impact of a high discount rate and the potential for increased sales. The analysis concludes that the project is generally viable and provides positive NPVs in most scenarios, indicating a potentially profitable investment. The report emphasizes the importance of investment appraisal techniques in determining project viability and return potential.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.