Management Accounting Systems: Planning Tools and Financial Solutions

VerifiedAdded on 2024/05/20

|19

|3937

|155

Report

AI Summary

This report provides a comprehensive analysis of management accounting systems, focusing on cost analysis, budgetary control, and financial planning. It begins by explaining management accounting and its essential requirements, highlighting the benefits of management accounting systems and their application in organizational contexts. The report delves into different methods for management accounting reporting, including cost reports, operational and cash reports, departmental reports, and performance appraisal reports. It includes calculations of costs using marginal and absorption costing techniques to prepare income statements. Furthermore, the report discusses the advantages and disadvantages of various planning tools used in budgetary control, such as ABC analysis and variance analysis, and analyses their application for preparing and forecasting budgets. The report also compares how organizations adapt management accounting systems to respond to financial problems and evaluates planning tools for addressing these issues, ultimately aiming to provide Zylla Company with recommendations for improved management accounting practices to enhance business and financial performance. Desklib offers further resources and solved assignments for students.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction...........................................................................................................................................2

P1 Explain management accounting and give the essential requirements of different types of

management accounting........................................................................................................................3

M1 Benefits of management accounting system and their application in organisational context..........4

D1 A critical evaluation of how management accounting systems and reporting are integrated within

organisational processes........................................................................................................................5

P2 Explain different methods used for management accounting reporting............................................6

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement using

marginal and absorption costing............................................................................................................7

P4 Explain the advantages and disadvantages of different types of planning tools used in budgetary

control.................................................................................................................................................10

M3. Analyse the use of different planning tools and their application for preparing and forecasting

budgets................................................................................................................................................13

P5 Compare how organisations are adapting management accounting systems to respond to financial

problems..............................................................................................................................................14

M4 Analyse how management can lead to sustainable success...........................................................14

D4 Critically evaluate planning tools for responding to financial problems........................................15

Conclusion...........................................................................................................................................16

References...........................................................................................................................................17

2

Introduction...........................................................................................................................................2

P1 Explain management accounting and give the essential requirements of different types of

management accounting........................................................................................................................3

M1 Benefits of management accounting system and their application in organisational context..........4

D1 A critical evaluation of how management accounting systems and reporting are integrated within

organisational processes........................................................................................................................5

P2 Explain different methods used for management accounting reporting............................................6

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement using

marginal and absorption costing............................................................................................................7

P4 Explain the advantages and disadvantages of different types of planning tools used in budgetary

control.................................................................................................................................................10

M3. Analyse the use of different planning tools and their application for preparing and forecasting

budgets................................................................................................................................................13

P5 Compare how organisations are adapting management accounting systems to respond to financial

problems..............................................................................................................................................14

M4 Analyse how management can lead to sustainable success...........................................................14

D4 Critically evaluate planning tools for responding to financial problems........................................15

Conclusion...........................................................................................................................................16

References...........................................................................................................................................17

2

Introduction

This report aims at providing information to the Finance Director of Zylla Company for

further submission to the Board of Directors to the company. The information included in this

report relates to the comprehensive changes which are required to be made in the

management accounting system of the company in order to support the company to deal with

the changes that took place in the business over the time. The information is based on the

review of the existing management accounting system of the company and the research

conducted with regards to the developments in the methods and techniques of management

accounting used by the organisations all over the world. The report includes the details of

management accounting systems and processes, techniques used for determining the costs of

business, planning tools used in management accounting and the techniques and tools used

for resolving the financial problems by the organisations. The recommendations are provided

to Zylla Company through application of management accounting in an improved manner.

3

This report aims at providing information to the Finance Director of Zylla Company for

further submission to the Board of Directors to the company. The information included in this

report relates to the comprehensive changes which are required to be made in the

management accounting system of the company in order to support the company to deal with

the changes that took place in the business over the time. The information is based on the

review of the existing management accounting system of the company and the research

conducted with regards to the developments in the methods and techniques of management

accounting used by the organisations all over the world. The report includes the details of

management accounting systems and processes, techniques used for determining the costs of

business, planning tools used in management accounting and the techniques and tools used

for resolving the financial problems by the organisations. The recommendations are provided

to Zylla Company through application of management accounting in an improved manner.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P1 Explain management accounting and give the essential requirements of

different types of management accounting.

Management accounting is defined as the process which is used as the framework for

processing and reporting the internal business information to support the internal decision

making within the organisation (Black & Al-kilani, 2013). Management accounting uses he

financial information presented by the organisations to the users for decision making in order

to generate and present the reports to the mangers of the organisation. Management

accounting provides the business organisations with a number of tools and techniques which

support the companies in improving their business and financial performance and achieve the

goals and objectives of the business in alignment with its strategy and vision.

Management accounting is an accounting framework ad its implementation within the

business functions and operations of an organisation involves a number of pre-requisites to be

completed by the organisations. The essential requirements for the implementation of

management accounting methods and techniques are the effective cost management and

proper decision making approach explained as follows:

Cost management – An organisation is required to have in place effective cost

management and cost control system which supports the implementation of cost

calculation and cost allocation methods such as activity based costing, process costing,

standard costing, marginal costing etc. Also the effective management systems within the

operations of the organisation support the budget preparation and planning process

(Vasile & Croiteru, 2013).

Decision-making approach – The proper decision making approach with defined

authorities and responsibilities are essentially required for the effective implementation of

management accounting systems within the organisation. Management accounting

generates reports for the decision making of mangers and if the decision making process

of an organisation is not appropriate; the objective of implementing the management

accounting systems within the organisation will not be achieved.

4

different types of management accounting.

Management accounting is defined as the process which is used as the framework for

processing and reporting the internal business information to support the internal decision

making within the organisation (Black & Al-kilani, 2013). Management accounting uses he

financial information presented by the organisations to the users for decision making in order

to generate and present the reports to the mangers of the organisation. Management

accounting provides the business organisations with a number of tools and techniques which

support the companies in improving their business and financial performance and achieve the

goals and objectives of the business in alignment with its strategy and vision.

Management accounting is an accounting framework ad its implementation within the

business functions and operations of an organisation involves a number of pre-requisites to be

completed by the organisations. The essential requirements for the implementation of

management accounting methods and techniques are the effective cost management and

proper decision making approach explained as follows:

Cost management – An organisation is required to have in place effective cost

management and cost control system which supports the implementation of cost

calculation and cost allocation methods such as activity based costing, process costing,

standard costing, marginal costing etc. Also the effective management systems within the

operations of the organisation support the budget preparation and planning process

(Vasile & Croiteru, 2013).

Decision-making approach – The proper decision making approach with defined

authorities and responsibilities are essentially required for the effective implementation of

management accounting systems within the organisation. Management accounting

generates reports for the decision making of mangers and if the decision making process

of an organisation is not appropriate; the objective of implementing the management

accounting systems within the organisation will not be achieved.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M1 Benefits of management accounting system and their application in

organisational context

The benefits of management accounting systems in their application within the business

operations and functions of Zylla Company can be explained as follows:

Management

Accounting System

Benefits

Inventory

management

systems

It helps in reducing the storage and handling cost of business

inventory which leads to the cost control of the business

(Kumar, 2014).

It supports the supply chain and value chain by placing order

for procurement of inventory in an efficient manner.

Price optimisation

systems

These systems help in positioning the products of the company

in the market effectively so as to attract the customers and

establish the business in the market.

It supports the mangers in decisions with regards to price

determination.

Job costing systems These systems help the business in proper allocation of costs to

the product so that accurate cost of producing each unit can be

calculated.

The job costing system helps the business in segregating the

costs to the jobs or batches resulting in performance evaluation.

D1 A critical evaluation of how management accounting systems and

reporting are integrated within organisational processes.

Management accountings systems and methods of management accounting reporting can be

integrated within the business of Zylla Company through its policies and procedures for

5

organisational context

The benefits of management accounting systems in their application within the business

operations and functions of Zylla Company can be explained as follows:

Management

Accounting System

Benefits

Inventory

management

systems

It helps in reducing the storage and handling cost of business

inventory which leads to the cost control of the business

(Kumar, 2014).

It supports the supply chain and value chain by placing order

for procurement of inventory in an efficient manner.

Price optimisation

systems

These systems help in positioning the products of the company

in the market effectively so as to attract the customers and

establish the business in the market.

It supports the mangers in decisions with regards to price

determination.

Job costing systems These systems help the business in proper allocation of costs to

the product so that accurate cost of producing each unit can be

calculated.

The job costing system helps the business in segregating the

costs to the jobs or batches resulting in performance evaluation.

D1 A critical evaluation of how management accounting systems and

reporting are integrated within organisational processes.

Management accountings systems and methods of management accounting reporting can be

integrated within the business of Zylla Company through its policies and procedures for

5

conducting the business operations. Management accounting systems such as inventory

management can be implemented by the stores and production department by adopting the

strategies of EOQ, FIFO, and LIFO etc. Similarly the price optimisation method can be

adopted by the sales department for company for determining the prices of its products. The

finance department of the company can implement the cost management systems so that the

optimum use of financial resources for the business operations can be made. In order to

integrate the reporting methods, the management of the company will be required to frame

the policies for generating the reports and preparing and presenting them to the relevant

authority in an efficient manner. The decision making approach of the company shall be

based on the reporting framework.

6

management can be implemented by the stores and production department by adopting the

strategies of EOQ, FIFO, and LIFO etc. Similarly the price optimisation method can be

adopted by the sales department for company for determining the prices of its products. The

finance department of the company can implement the cost management systems so that the

optimum use of financial resources for the business operations can be made. In order to

integrate the reporting methods, the management of the company will be required to frame

the policies for generating the reports and preparing and presenting them to the relevant

authority in an efficient manner. The decision making approach of the company shall be

based on the reporting framework.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P2 Explain different methods used for management accounting reporting

The different types of methods which are used under the process of management accounting

reporting are explained as follows:

Cost reports – These reports are based on the cost volume and profit analysis of the

business conducted using the techniques such as break-even analysis, trend line and

forecasting, activity based costing, marginal costing etc. In this method the costs of the

business operations are estimated and reported in a systematic manner with the details of

likely increase and types and nature of cost elements (Weygandt, et.al, 2010).

Operational and cash reports - The details about the business transactions, cash

transactions and fund movement into the operations are presented in the operational

reports. These reports are used by the managers of the company for making decisions

with regards to the procurement and disbursement of financial resources in order to

conduct the business operations in an optimum manner.

Departmental reports – In this method of reporting the performance reports are prepared

by the different departments of a company including the details of the financial

performance and other details of the respective departments such as sales, marketing,

production, administration etc. These reports are used by the top level management for

decision making.

Performance and appraisal reports – In this method of reporting, the appraisal reports

for the departments or the employees of the organisation are prepared in order to evaluate

the individual performance and make the decisions accordingly. The performance and

appraisal reports are also used by the top level management of accompany for evaluating

and appraising the best performers within the company.

7

The different types of methods which are used under the process of management accounting

reporting are explained as follows:

Cost reports – These reports are based on the cost volume and profit analysis of the

business conducted using the techniques such as break-even analysis, trend line and

forecasting, activity based costing, marginal costing etc. In this method the costs of the

business operations are estimated and reported in a systematic manner with the details of

likely increase and types and nature of cost elements (Weygandt, et.al, 2010).

Operational and cash reports - The details about the business transactions, cash

transactions and fund movement into the operations are presented in the operational

reports. These reports are used by the managers of the company for making decisions

with regards to the procurement and disbursement of financial resources in order to

conduct the business operations in an optimum manner.

Departmental reports – In this method of reporting the performance reports are prepared

by the different departments of a company including the details of the financial

performance and other details of the respective departments such as sales, marketing,

production, administration etc. These reports are used by the top level management for

decision making.

Performance and appraisal reports – In this method of reporting, the appraisal reports

for the departments or the employees of the organisation are prepared in order to evaluate

the individual performance and make the decisions accordingly. The performance and

appraisal reports are also used by the top level management of accompany for evaluating

and appraising the best performers within the company.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P3 Calculate costs using appropriate techniques of cost analysis to prepare

an income statement using marginal and absorption costing

Cost analysis is the process which relates to calculation of total costs of business operations

and bifurcation of the cost to the cost elements so as to make the decisions with regards to

cost control and cost reduction. There are two methods which can be used by the multi-

national manufacturing organisations like Zylla Company for management accounting

reporting in relation to costs and profits of the business viz. absorption costing and marginal

costing. These costing techniques help in the cost allocation and cost calculation on the basis

of which the net profits of the business can be calculated.

Absorption costing is the method in which the total cost of production is calculated on the

basis of overall absorption rate which is calculated by dividing the total cost of all the

material labour and overheads used in production process by the number of units produced.

The same rate of absorption is used for calculating the value of the inventory of business

(Raiborn & Kinney, 2013). It is also known as the traditional method of management

reporting.

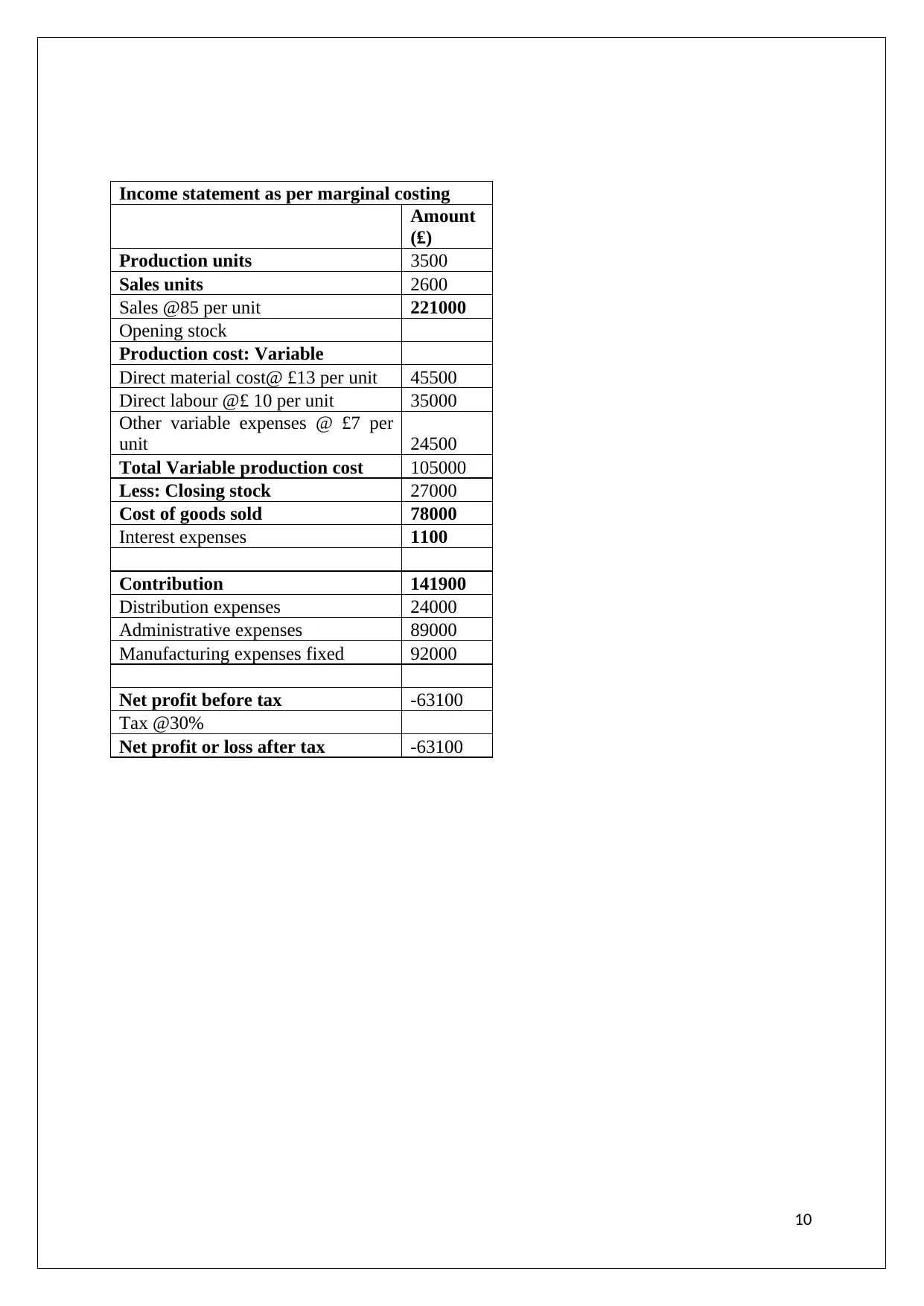

The method of calculating and reporting costs by the management accountants in which the

total variable costs of the business are added to arrive at the total cost for calculating the

contribution made by each product to the business is known as marginal costing method. In

this method the variable overheads including production, administration and sales are added

and the total is deducted from the revenue. The fixed expenses are deducted from

contribution to calculate net profit.

The calculation of costs using absorption and marginal methods of calculation and the

income statements prepared using management accounting techniques and the financial

reporting documents are as follows (M2, D2):

8

an income statement using marginal and absorption costing

Cost analysis is the process which relates to calculation of total costs of business operations

and bifurcation of the cost to the cost elements so as to make the decisions with regards to

cost control and cost reduction. There are two methods which can be used by the multi-

national manufacturing organisations like Zylla Company for management accounting

reporting in relation to costs and profits of the business viz. absorption costing and marginal

costing. These costing techniques help in the cost allocation and cost calculation on the basis

of which the net profits of the business can be calculated.

Absorption costing is the method in which the total cost of production is calculated on the

basis of overall absorption rate which is calculated by dividing the total cost of all the

material labour and overheads used in production process by the number of units produced.

The same rate of absorption is used for calculating the value of the inventory of business

(Raiborn & Kinney, 2013). It is also known as the traditional method of management

reporting.

The method of calculating and reporting costs by the management accountants in which the

total variable costs of the business are added to arrive at the total cost for calculating the

contribution made by each product to the business is known as marginal costing method. In

this method the variable overheads including production, administration and sales are added

and the total is deducted from the revenue. The fixed expenses are deducted from

contribution to calculate net profit.

The calculation of costs using absorption and marginal methods of calculation and the

income statements prepared using management accounting techniques and the financial

reporting documents are as follows (M2, D2):

8

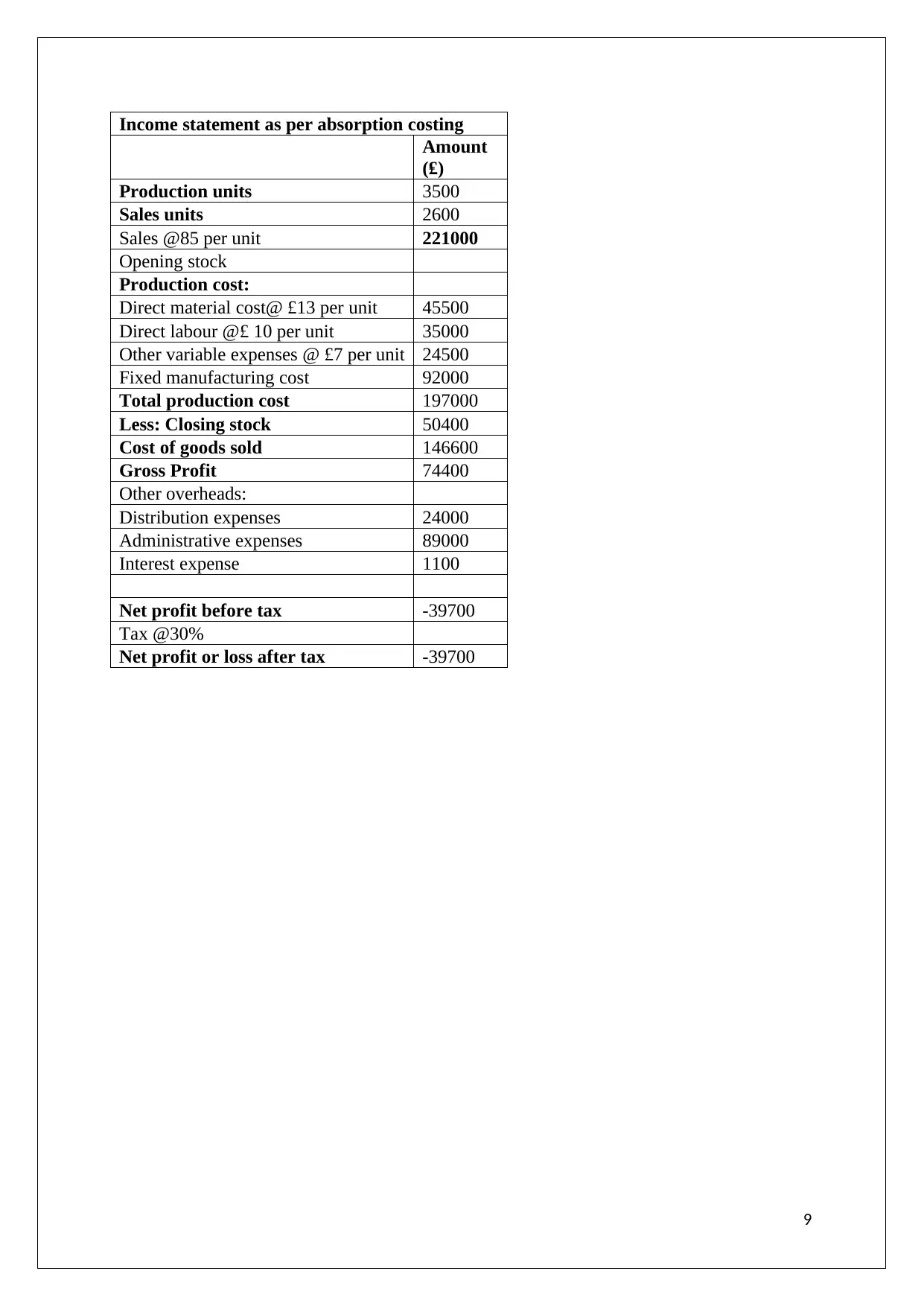

Income statement as per absorption costing

Amount

(₤)

Production units 3500

Sales units 2600

Sales @85 per unit 221000

Opening stock

Production cost:

Direct material cost@ £13 per unit 45500

Direct labour @£ 10 per unit 35000

Other variable expenses @ £7 per unit 24500

Fixed manufacturing cost 92000

Total production cost 197000

Less: Closing stock 50400

Cost of goods sold 146600

Gross Profit 74400

Other overheads:

Distribution expenses 24000

Administrative expenses 89000

Interest expense 1100

Net profit before tax -39700

Tax @30%

Net profit or loss after tax -39700

9

Amount

(₤)

Production units 3500

Sales units 2600

Sales @85 per unit 221000

Opening stock

Production cost:

Direct material cost@ £13 per unit 45500

Direct labour @£ 10 per unit 35000

Other variable expenses @ £7 per unit 24500

Fixed manufacturing cost 92000

Total production cost 197000

Less: Closing stock 50400

Cost of goods sold 146600

Gross Profit 74400

Other overheads:

Distribution expenses 24000

Administrative expenses 89000

Interest expense 1100

Net profit before tax -39700

Tax @30%

Net profit or loss after tax -39700

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Income statement as per marginal costing

Amount

(₤)

Production units 3500

Sales units 2600

Sales @85 per unit 221000

Opening stock

Production cost: Variable

Direct material cost@ £13 per unit 45500

Direct labour @£ 10 per unit 35000

Other variable expenses @ £7 per

unit 24500

Total Variable production cost 105000

Less: Closing stock 27000

Cost of goods sold 78000

Interest expenses 1100

Contribution 141900

Distribution expenses 24000

Administrative expenses 89000

Manufacturing expenses fixed 92000

Net profit before tax -63100

Tax @30%

Net profit or loss after tax -63100

10

Amount

(₤)

Production units 3500

Sales units 2600

Sales @85 per unit 221000

Opening stock

Production cost: Variable

Direct material cost@ £13 per unit 45500

Direct labour @£ 10 per unit 35000

Other variable expenses @ £7 per

unit 24500

Total Variable production cost 105000

Less: Closing stock 27000

Cost of goods sold 78000

Interest expenses 1100

Contribution 141900

Distribution expenses 24000

Administrative expenses 89000

Manufacturing expenses fixed 92000

Net profit before tax -63100

Tax @30%

Net profit or loss after tax -63100

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

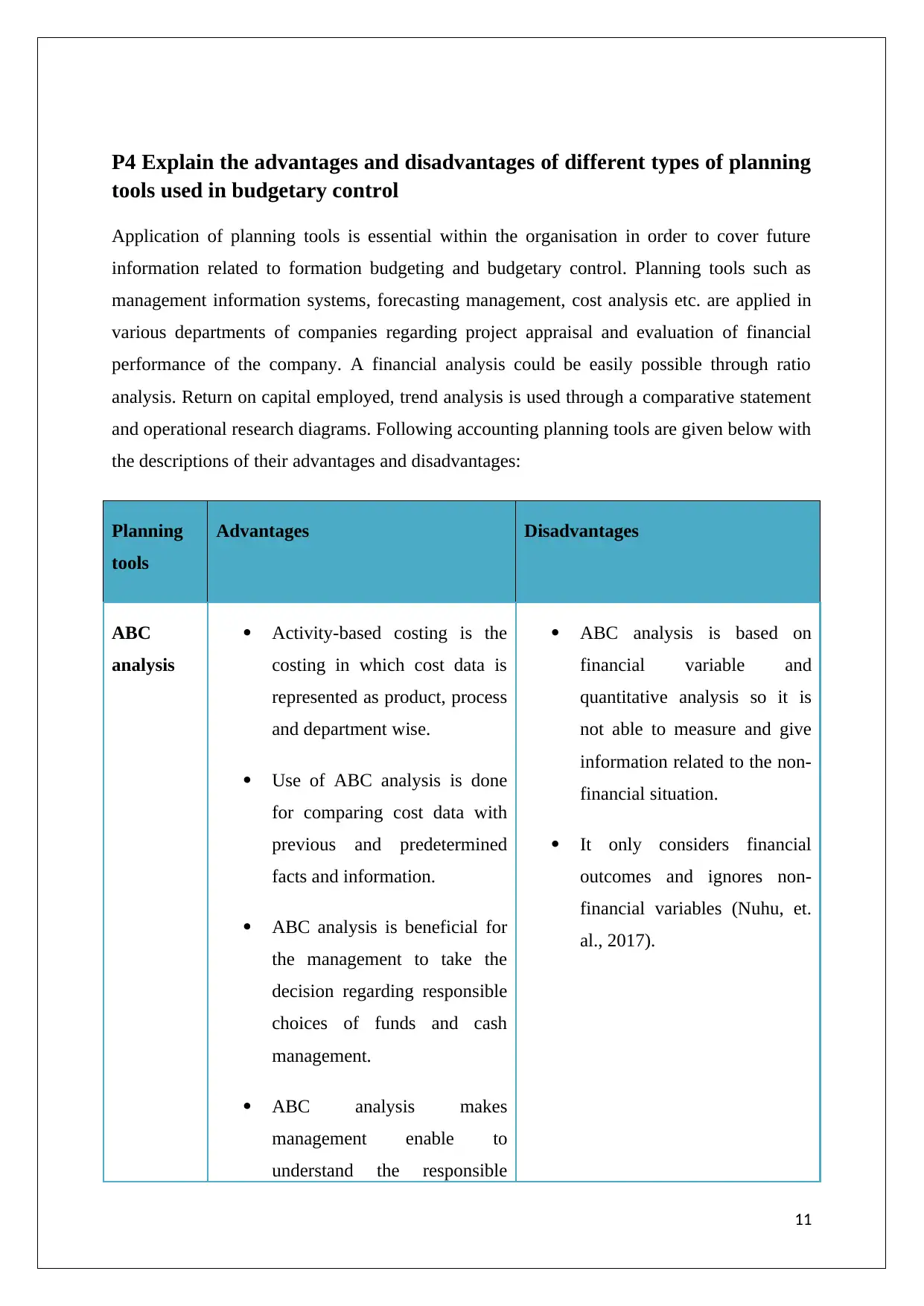

P4 Explain the advantages and disadvantages of different types of planning

tools used in budgetary control

Application of planning tools is essential within the organisation in order to cover future

information related to formation budgeting and budgetary control. Planning tools such as

management information systems, forecasting management, cost analysis etc. are applied in

various departments of companies regarding project appraisal and evaluation of financial

performance of the company. A financial analysis could be easily possible through ratio

analysis. Return on capital employed, trend analysis is used through a comparative statement

and operational research diagrams. Following accounting planning tools are given below with

the descriptions of their advantages and disadvantages:

Planning

tools

Advantages Disadvantages

ABC

analysis

Activity-based costing is the

costing in which cost data is

represented as product, process

and department wise.

Use of ABC analysis is done

for comparing cost data with

previous and predetermined

facts and information.

ABC analysis is beneficial for

the management to take the

decision regarding responsible

choices of funds and cash

management.

ABC analysis makes

management enable to

understand the responsible

ABC analysis is based on

financial variable and

quantitative analysis so it is

not able to measure and give

information related to the non-

financial situation.

It only considers financial

outcomes and ignores non-

financial variables (Nuhu, et.

al., 2017).

11

tools used in budgetary control

Application of planning tools is essential within the organisation in order to cover future

information related to formation budgeting and budgetary control. Planning tools such as

management information systems, forecasting management, cost analysis etc. are applied in

various departments of companies regarding project appraisal and evaluation of financial

performance of the company. A financial analysis could be easily possible through ratio

analysis. Return on capital employed, trend analysis is used through a comparative statement

and operational research diagrams. Following accounting planning tools are given below with

the descriptions of their advantages and disadvantages:

Planning

tools

Advantages Disadvantages

ABC

analysis

Activity-based costing is the

costing in which cost data is

represented as product, process

and department wise.

Use of ABC analysis is done

for comparing cost data with

previous and predetermined

facts and information.

ABC analysis is beneficial for

the management to take the

decision regarding responsible

choices of funds and cash

management.

ABC analysis makes

management enable to

understand the responsible

ABC analysis is based on

financial variable and

quantitative analysis so it is

not able to measure and give

information related to the non-

financial situation.

It only considers financial

outcomes and ignores non-

financial variables (Nuhu, et.

al., 2017).

11

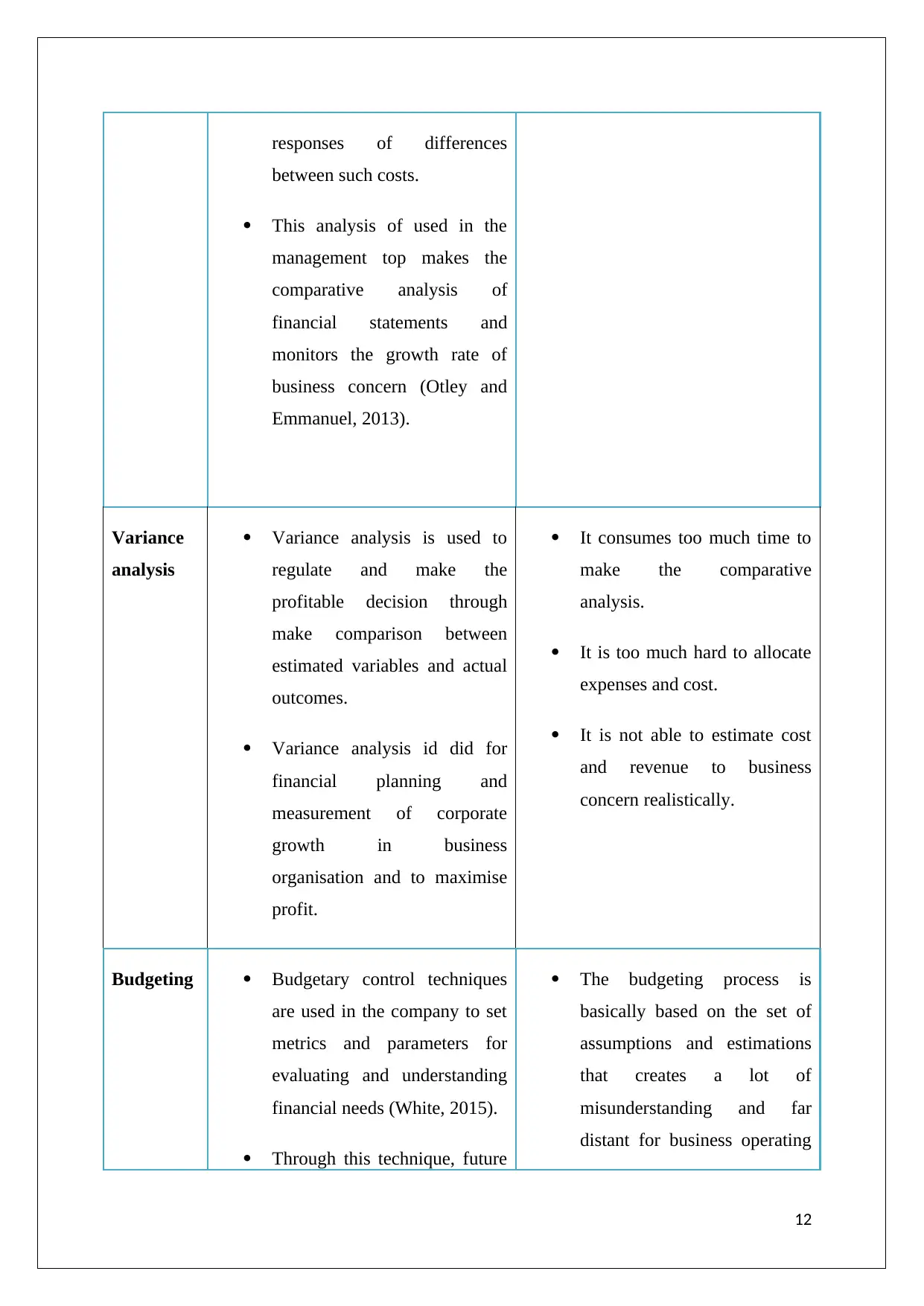

responses of differences

between such costs.

This analysis of used in the

management top makes the

comparative analysis of

financial statements and

monitors the growth rate of

business concern (Otley and

Emmanuel, 2013).

Variance

analysis

Variance analysis is used to

regulate and make the

profitable decision through

make comparison between

estimated variables and actual

outcomes.

Variance analysis id did for

financial planning and

measurement of corporate

growth in business

organisation and to maximise

profit.

It consumes too much time to

make the comparative

analysis.

It is too much hard to allocate

expenses and cost.

It is not able to estimate cost

and revenue to business

concern realistically.

Budgeting Budgetary control techniques

are used in the company to set

metrics and parameters for

evaluating and understanding

financial needs (White, 2015).

Through this technique, future

The budgeting process is

basically based on the set of

assumptions and estimations

that creates a lot of

misunderstanding and far

distant for business operating

12

between such costs.

This analysis of used in the

management top makes the

comparative analysis of

financial statements and

monitors the growth rate of

business concern (Otley and

Emmanuel, 2013).

Variance

analysis

Variance analysis is used to

regulate and make the

profitable decision through

make comparison between

estimated variables and actual

outcomes.

Variance analysis id did for

financial planning and

measurement of corporate

growth in business

organisation and to maximise

profit.

It consumes too much time to

make the comparative

analysis.

It is too much hard to allocate

expenses and cost.

It is not able to estimate cost

and revenue to business

concern realistically.

Budgeting Budgetary control techniques

are used in the company to set

metrics and parameters for

evaluating and understanding

financial needs (White, 2015).

Through this technique, future

The budgeting process is

basically based on the set of

assumptions and estimations

that creates a lot of

misunderstanding and far

distant for business operating

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.