MREGC5001 Plant Purchase: Capital Investment Analysis & Replacement

VerifiedAdded on 2023/06/12

|16

|3540

|204

Homework Assignment

AI Summary

This assignment provides a comprehensive analysis of plant purchase, installation, and replacement decisions, utilizing methods such as annual worth, present worth, and internal rate of return (IRR). It includes a detailed evaluation of different automation degrees for a manufacturing process, considering factors like first cost, labor, power, maintenance, and tax implications. The assignment also explores the conventional and modified benefit-cost ratio methods, leasing alternatives, and equivalent annual cost analysis for equipment replacement options. Furthermore, it identifies gaps in the implementation of life cycle costing within ID Engineering Works Limited, offering recommendations for improving the decision-making process by incorporating relevant cost considerations. This document is a student contribution and is available on Desklib, a platform offering a wide array of study resources and AI-powered tools for students.

Running head: PLANT PURCHASE, INSTALLATION AND REPLACEMENT

Plant purchase, Installation and replacement

Name of the Student:

Name of the University:

Authors Note:

Plant purchase, Installation and replacement

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1PLANT PURCHASE, INSTALLATION AND REPLACEMENT

Table of Contents

Answer to Question 1......................................................................................................................2

a)..................................................................................................................................................3

b)..................................................................................................................................................4

c)..................................................................................................................................................4

Answer to Question 2......................................................................................................................5

Answer to Question 3......................................................................................................................7

1...................................................................................................................................................7

2...................................................................................................................................................7

Answer to Question 4......................................................................................................................7

Answer to Question 5......................................................................................................................8

Reference.......................................................................................................................................13

Table of Contents

Answer to Question 1......................................................................................................................2

a)..................................................................................................................................................3

b)..................................................................................................................................................4

c)..................................................................................................................................................4

Answer to Question 2......................................................................................................................5

Answer to Question 3......................................................................................................................7

1...................................................................................................................................................7

2...................................................................................................................................................7

Answer to Question 4......................................................................................................................7

Answer to Question 5......................................................................................................................8

Reference.......................................................................................................................................13

2PLANT PURCHASE, INSTALLATION AND REPLACEMENT

Answer to Question 1

The reason for the relevance of the annual worth, present worth and internal rate of return is

in respect of capital budgeting decisions are as follows:

a) Present Worth-

It is necessary to find the present worth of the company depending on the present value of the

revenues to be generated by the company. It is because while calculating the present value of a

future inflow several factors determine the rate of discounting to be used like the rate of interest,

the rate of inflation present in the economy etc. The present value of the inflows gives an

estimate regarding the real value that is going to flow into the entity (Demis et al., 2015).

b) Internal rate of return-

The internal rate of return represents that the percentage of return that is generated from the

proposed investment into the project. The internal rate of return is important for comparing with

the cost of capital of the company. It might be possible that the Net Present Value of the project

is positive but the rate of returns provided by it is not enough to beat the cost of capital of the

company (Mizobuchi & Takeuchi, 2016). Hence, the value generated by the project will not be

enough to meet the requirements of the entity in respect of repayment of the debt capital and to

match the expectations of the shareholders of the company, in case IRR of the project is less than

the Cost of Capital of the project.

c) Annual worth-

The annual worth of the project or the inflows generated by the proposed project is very crucial

for the management in case of the capital budgeting decisions. The reason behind this is that with

the help of it the management of the company is able to objectively decipher the number of years

Answer to Question 1

The reason for the relevance of the annual worth, present worth and internal rate of return is

in respect of capital budgeting decisions are as follows:

a) Present Worth-

It is necessary to find the present worth of the company depending on the present value of the

revenues to be generated by the company. It is because while calculating the present value of a

future inflow several factors determine the rate of discounting to be used like the rate of interest,

the rate of inflation present in the economy etc. The present value of the inflows gives an

estimate regarding the real value that is going to flow into the entity (Demis et al., 2015).

b) Internal rate of return-

The internal rate of return represents that the percentage of return that is generated from the

proposed investment into the project. The internal rate of return is important for comparing with

the cost of capital of the company. It might be possible that the Net Present Value of the project

is positive but the rate of returns provided by it is not enough to beat the cost of capital of the

company (Mizobuchi & Takeuchi, 2016). Hence, the value generated by the project will not be

enough to meet the requirements of the entity in respect of repayment of the debt capital and to

match the expectations of the shareholders of the company, in case IRR of the project is less than

the Cost of Capital of the project.

c) Annual worth-

The annual worth of the project or the inflows generated by the proposed project is very crucial

for the management in case of the capital budgeting decisions. The reason behind this is that with

the help of it the management of the company is able to objectively decipher the number of years

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3PLANT PURCHASE, INSTALLATION AND REPLACEMENT

after which it will be possible for the company to recover its invested amount. It is also called the

discounting period of the project.

a)

Calculation of the Annual Worth of different Alternatives

Particular A B C D

Supply units 5000 5000 5000 5000

Sales price per unit $3.00 $3.00 $3.00 $3.00

Sales (1) $15,000.00 $15,000.00 $15,000.00 $15,000.00

Fixed Cost $10,000.00 $14,000.00 $20,000.00 $30,000.00

Capital Recovery Factor

0.2296073

8

0.2296073

8

0.2296073

8

0.2296073

8

(A/P,I,N) (2) $2,296.07 $3,214.50 $4,592.15 $6,888.22

Salvage value $500.00 $700.00 $1,000.00 $1,500.00

Sinking Fund factor

0.1296073

8

0.1296073

8

0.1296073

8

0.1296073

8

(A/F, i, N) (3) $64.80 $90.73 $129.61 $194.41

Annual Labor cost (4) $9,000.00 $7,500.00 $5,000.00 $3,000.00

Annual Power and maintenance cost

(5) $500.00 $800.00 $1,000.00 $1,500.00

Annual Worth (1-2+3-4-5) $3,268.73 $3,576.22 $4,537.46 $3,806.19

The table above shows that the Annual worth of alternative C is the highest and

Alternative A is the lowest.

b)

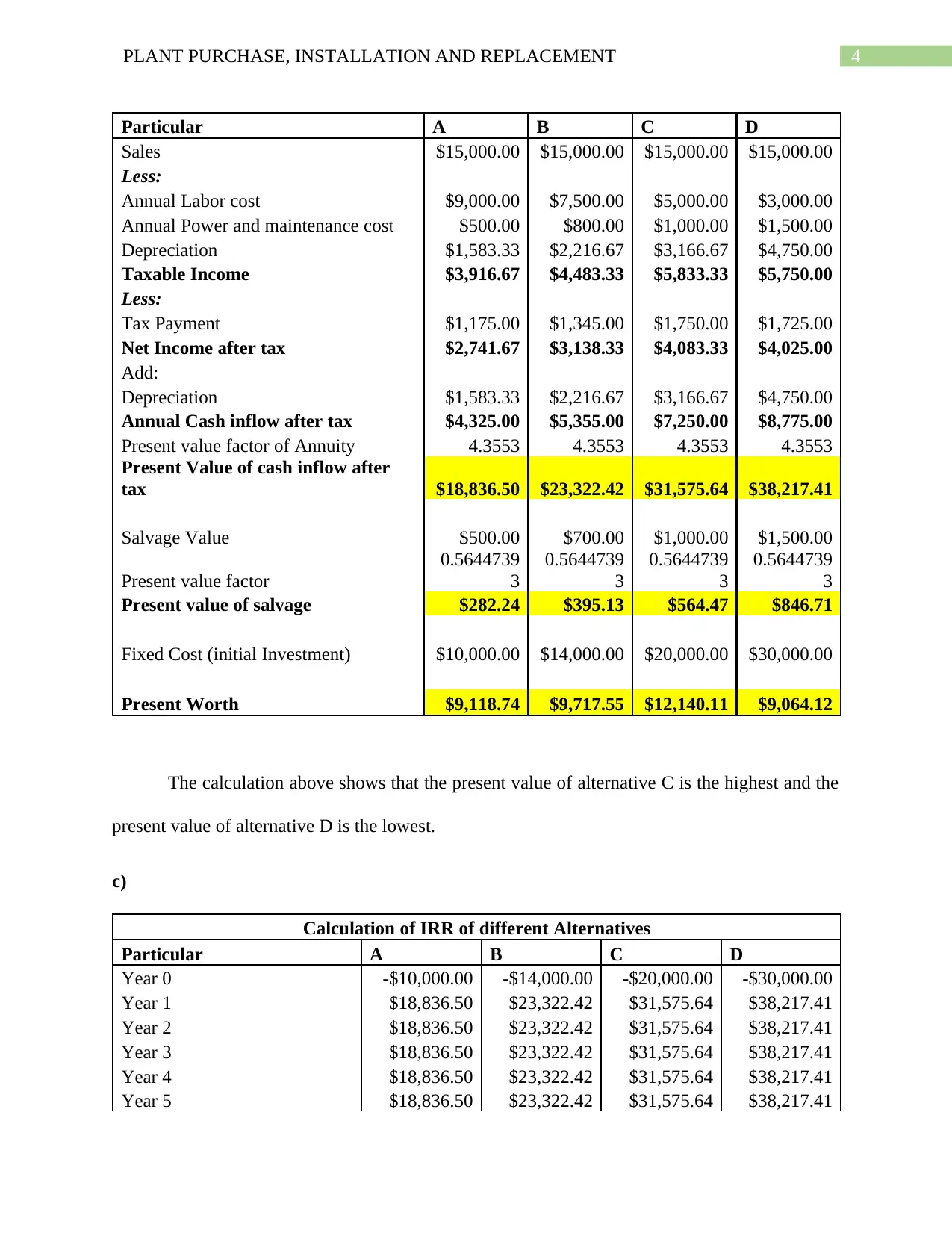

Calculation of the Present Worth of different Alternatives

after which it will be possible for the company to recover its invested amount. It is also called the

discounting period of the project.

a)

Calculation of the Annual Worth of different Alternatives

Particular A B C D

Supply units 5000 5000 5000 5000

Sales price per unit $3.00 $3.00 $3.00 $3.00

Sales (1) $15,000.00 $15,000.00 $15,000.00 $15,000.00

Fixed Cost $10,000.00 $14,000.00 $20,000.00 $30,000.00

Capital Recovery Factor

0.2296073

8

0.2296073

8

0.2296073

8

0.2296073

8

(A/P,I,N) (2) $2,296.07 $3,214.50 $4,592.15 $6,888.22

Salvage value $500.00 $700.00 $1,000.00 $1,500.00

Sinking Fund factor

0.1296073

8

0.1296073

8

0.1296073

8

0.1296073

8

(A/F, i, N) (3) $64.80 $90.73 $129.61 $194.41

Annual Labor cost (4) $9,000.00 $7,500.00 $5,000.00 $3,000.00

Annual Power and maintenance cost

(5) $500.00 $800.00 $1,000.00 $1,500.00

Annual Worth (1-2+3-4-5) $3,268.73 $3,576.22 $4,537.46 $3,806.19

The table above shows that the Annual worth of alternative C is the highest and

Alternative A is the lowest.

b)

Calculation of the Present Worth of different Alternatives

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4PLANT PURCHASE, INSTALLATION AND REPLACEMENT

Particular A B C D

Sales $15,000.00 $15,000.00 $15,000.00 $15,000.00

Less:

Annual Labor cost $9,000.00 $7,500.00 $5,000.00 $3,000.00

Annual Power and maintenance cost $500.00 $800.00 $1,000.00 $1,500.00

Depreciation $1,583.33 $2,216.67 $3,166.67 $4,750.00

Taxable Income $3,916.67 $4,483.33 $5,833.33 $5,750.00

Less:

Tax Payment $1,175.00 $1,345.00 $1,750.00 $1,725.00

Net Income after tax $2,741.67 $3,138.33 $4,083.33 $4,025.00

Add:

Depreciation $1,583.33 $2,216.67 $3,166.67 $4,750.00

Annual Cash inflow after tax $4,325.00 $5,355.00 $7,250.00 $8,775.00

Present value factor of Annuity 4.3553 4.3553 4.3553 4.3553

Present Value of cash inflow after

tax $18,836.50 $23,322.42 $31,575.64 $38,217.41

Salvage Value $500.00 $700.00 $1,000.00 $1,500.00

Present value factor

0.5644739

3

0.5644739

3

0.5644739

3

0.5644739

3

Present value of salvage $282.24 $395.13 $564.47 $846.71

Fixed Cost (initial Investment) $10,000.00 $14,000.00 $20,000.00 $30,000.00

Present Worth $9,118.74 $9,717.55 $12,140.11 $9,064.12

The calculation above shows that the present value of alternative C is the highest and the

present value of alternative D is the lowest.

c)

Calculation of IRR of different Alternatives

Particular A B C D

Year 0 -$10,000.00 -$14,000.00 -$20,000.00 -$30,000.00

Year 1 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 2 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 3 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 4 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 5 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Particular A B C D

Sales $15,000.00 $15,000.00 $15,000.00 $15,000.00

Less:

Annual Labor cost $9,000.00 $7,500.00 $5,000.00 $3,000.00

Annual Power and maintenance cost $500.00 $800.00 $1,000.00 $1,500.00

Depreciation $1,583.33 $2,216.67 $3,166.67 $4,750.00

Taxable Income $3,916.67 $4,483.33 $5,833.33 $5,750.00

Less:

Tax Payment $1,175.00 $1,345.00 $1,750.00 $1,725.00

Net Income after tax $2,741.67 $3,138.33 $4,083.33 $4,025.00

Add:

Depreciation $1,583.33 $2,216.67 $3,166.67 $4,750.00

Annual Cash inflow after tax $4,325.00 $5,355.00 $7,250.00 $8,775.00

Present value factor of Annuity 4.3553 4.3553 4.3553 4.3553

Present Value of cash inflow after

tax $18,836.50 $23,322.42 $31,575.64 $38,217.41

Salvage Value $500.00 $700.00 $1,000.00 $1,500.00

Present value factor

0.5644739

3

0.5644739

3

0.5644739

3

0.5644739

3

Present value of salvage $282.24 $395.13 $564.47 $846.71

Fixed Cost (initial Investment) $10,000.00 $14,000.00 $20,000.00 $30,000.00

Present Worth $9,118.74 $9,717.55 $12,140.11 $9,064.12

The calculation above shows that the present value of alternative C is the highest and the

present value of alternative D is the lowest.

c)

Calculation of IRR of different Alternatives

Particular A B C D

Year 0 -$10,000.00 -$14,000.00 -$20,000.00 -$30,000.00

Year 1 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 2 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 3 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 4 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 5 $18,836.50 $23,322.42 $31,575.64 $38,217.41

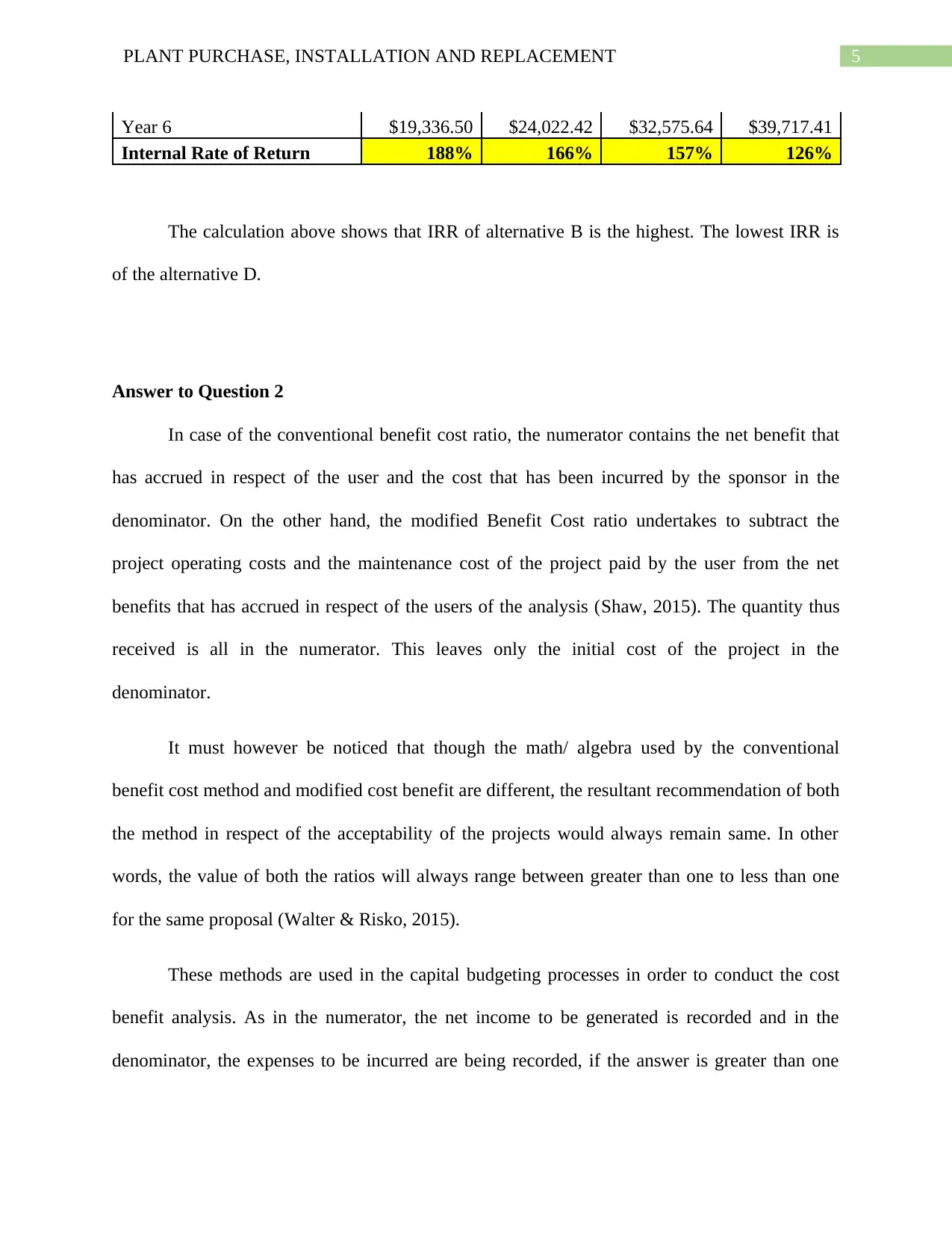

5PLANT PURCHASE, INSTALLATION AND REPLACEMENT

Year 6 $19,336.50 $24,022.42 $32,575.64 $39,717.41

Internal Rate of Return 188% 166% 157% 126%

The calculation above shows that IRR of alternative B is the highest. The lowest IRR is

of the alternative D.

Answer to Question 2

In case of the conventional benefit cost ratio, the numerator contains the net benefit that

has accrued in respect of the user and the cost that has been incurred by the sponsor in the

denominator. On the other hand, the modified Benefit Cost ratio undertakes to subtract the

project operating costs and the maintenance cost of the project paid by the user from the net

benefits that has accrued in respect of the users of the analysis (Shaw, 2015). The quantity thus

received is all in the numerator. This leaves only the initial cost of the project in the

denominator.

It must however be noticed that though the math/ algebra used by the conventional

benefit cost method and modified cost benefit are different, the resultant recommendation of both

the method in respect of the acceptability of the projects would always remain same. In other

words, the value of both the ratios will always range between greater than one to less than one

for the same proposal (Walter & Risko, 2015).

These methods are used in the capital budgeting processes in order to conduct the cost

benefit analysis. As in the numerator, the net income to be generated is recorded and in the

denominator, the expenses to be incurred are being recorded, if the answer is greater than one

Year 6 $19,336.50 $24,022.42 $32,575.64 $39,717.41

Internal Rate of Return 188% 166% 157% 126%

The calculation above shows that IRR of alternative B is the highest. The lowest IRR is

of the alternative D.

Answer to Question 2

In case of the conventional benefit cost ratio, the numerator contains the net benefit that

has accrued in respect of the user and the cost that has been incurred by the sponsor in the

denominator. On the other hand, the modified Benefit Cost ratio undertakes to subtract the

project operating costs and the maintenance cost of the project paid by the user from the net

benefits that has accrued in respect of the users of the analysis (Shaw, 2015). The quantity thus

received is all in the numerator. This leaves only the initial cost of the project in the

denominator.

It must however be noticed that though the math/ algebra used by the conventional

benefit cost method and modified cost benefit are different, the resultant recommendation of both

the method in respect of the acceptability of the projects would always remain same. In other

words, the value of both the ratios will always range between greater than one to less than one

for the same proposal (Walter & Risko, 2015).

These methods are used in the capital budgeting processes in order to conduct the cost

benefit analysis. As in the numerator, the net income to be generated is recorded and in the

denominator, the expenses to be incurred are being recorded, if the answer is greater than one

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6PLANT PURCHASE, INSTALLATION AND REPLACEMENT

then the benefits of the project are greater than the expenses and vice versa. Hence, depending on

the value of the result obtained the project is accepted or rejected.

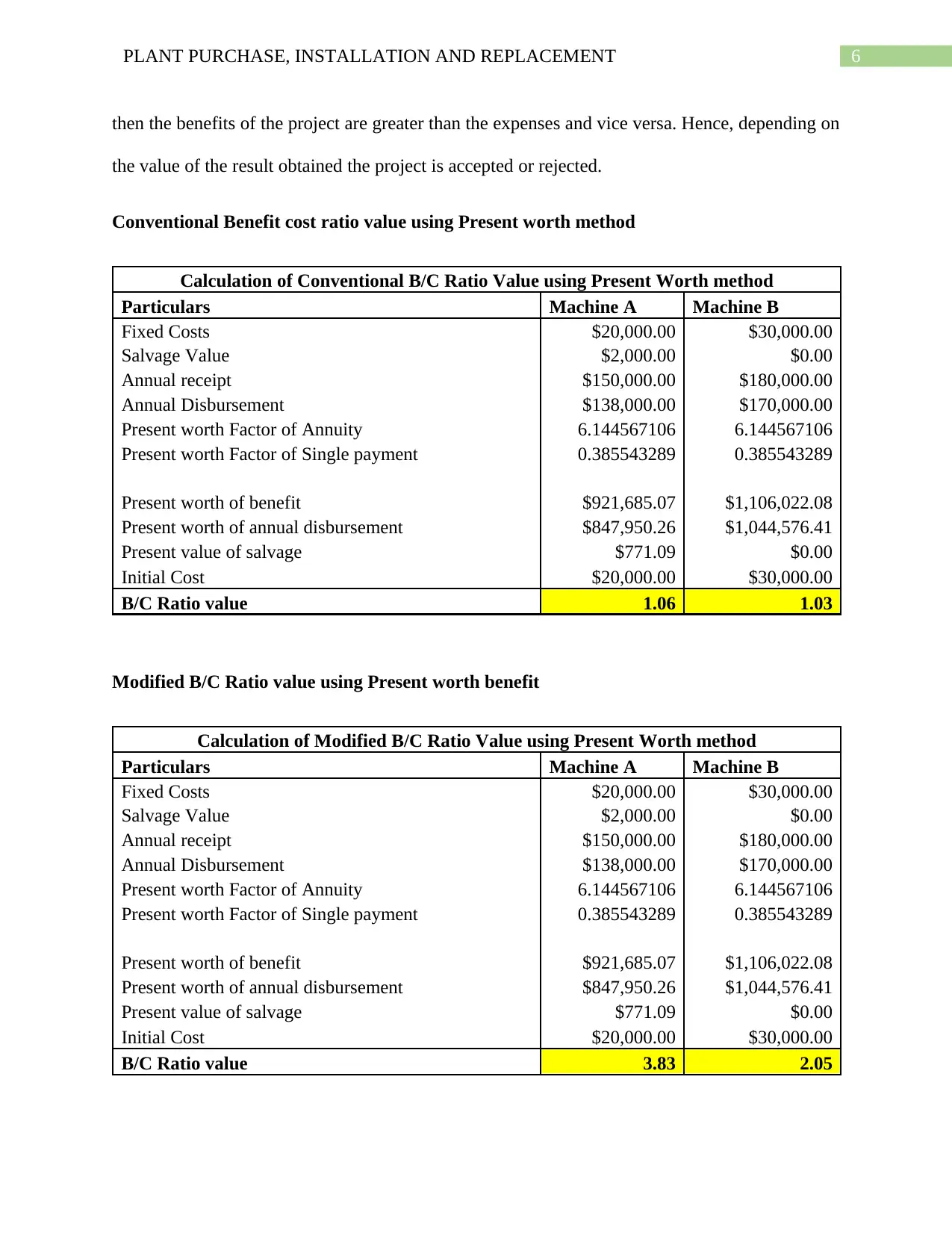

Conventional Benefit cost ratio value using Present worth method

Calculation of Conventional B/C Ratio Value using Present Worth method

Particulars Machine A Machine B

Fixed Costs $20,000.00 $30,000.00

Salvage Value $2,000.00 $0.00

Annual receipt $150,000.00 $180,000.00

Annual Disbursement $138,000.00 $170,000.00

Present worth Factor of Annuity 6.144567106 6.144567106

Present worth Factor of Single payment 0.385543289 0.385543289

Present worth of benefit $921,685.07 $1,106,022.08

Present worth of annual disbursement $847,950.26 $1,044,576.41

Present value of salvage $771.09 $0.00

Initial Cost $20,000.00 $30,000.00

B/C Ratio value 1.06 1.03

Modified B/C Ratio value using Present worth benefit

Calculation of Modified B/C Ratio Value using Present Worth method

Particulars Machine A Machine B

Fixed Costs $20,000.00 $30,000.00

Salvage Value $2,000.00 $0.00

Annual receipt $150,000.00 $180,000.00

Annual Disbursement $138,000.00 $170,000.00

Present worth Factor of Annuity 6.144567106 6.144567106

Present worth Factor of Single payment 0.385543289 0.385543289

Present worth of benefit $921,685.07 $1,106,022.08

Present worth of annual disbursement $847,950.26 $1,044,576.41

Present value of salvage $771.09 $0.00

Initial Cost $20,000.00 $30,000.00

B/C Ratio value 3.83 2.05

then the benefits of the project are greater than the expenses and vice versa. Hence, depending on

the value of the result obtained the project is accepted or rejected.

Conventional Benefit cost ratio value using Present worth method

Calculation of Conventional B/C Ratio Value using Present Worth method

Particulars Machine A Machine B

Fixed Costs $20,000.00 $30,000.00

Salvage Value $2,000.00 $0.00

Annual receipt $150,000.00 $180,000.00

Annual Disbursement $138,000.00 $170,000.00

Present worth Factor of Annuity 6.144567106 6.144567106

Present worth Factor of Single payment 0.385543289 0.385543289

Present worth of benefit $921,685.07 $1,106,022.08

Present worth of annual disbursement $847,950.26 $1,044,576.41

Present value of salvage $771.09 $0.00

Initial Cost $20,000.00 $30,000.00

B/C Ratio value 1.06 1.03

Modified B/C Ratio value using Present worth benefit

Calculation of Modified B/C Ratio Value using Present Worth method

Particulars Machine A Machine B

Fixed Costs $20,000.00 $30,000.00

Salvage Value $2,000.00 $0.00

Annual receipt $150,000.00 $180,000.00

Annual Disbursement $138,000.00 $170,000.00

Present worth Factor of Annuity 6.144567106 6.144567106

Present worth Factor of Single payment 0.385543289 0.385543289

Present worth of benefit $921,685.07 $1,106,022.08

Present worth of annual disbursement $847,950.26 $1,044,576.41

Present value of salvage $771.09 $0.00

Initial Cost $20,000.00 $30,000.00

B/C Ratio value 3.83 2.05

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7PLANT PURCHASE, INSTALLATION AND REPLACEMENT

Answer to Question 3

1.

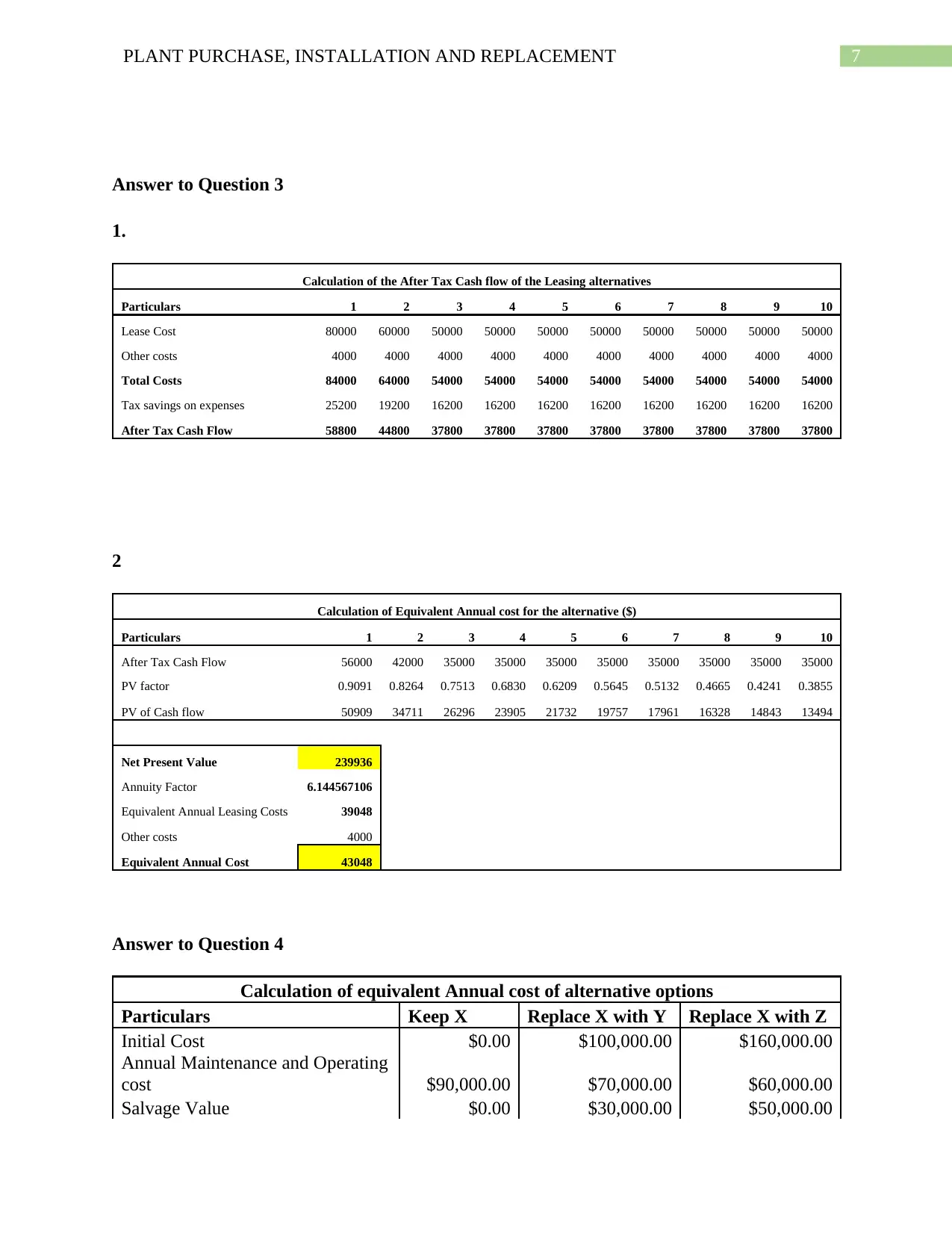

Calculation of the After Tax Cash flow of the Leasing alternatives

Particulars 1 2 3 4 5 6 7 8 9 10

Lease Cost 80000 60000 50000 50000 50000 50000 50000 50000 50000 50000

Other costs 4000 4000 4000 4000 4000 4000 4000 4000 4000 4000

Total Costs 84000 64000 54000 54000 54000 54000 54000 54000 54000 54000

Tax savings on expenses 25200 19200 16200 16200 16200 16200 16200 16200 16200 16200

After Tax Cash Flow 58800 44800 37800 37800 37800 37800 37800 37800 37800 37800

2

Calculation of Equivalent Annual cost for the alternative ($)

Particulars 1 2 3 4 5 6 7 8 9 10

After Tax Cash Flow 56000 42000 35000 35000 35000 35000 35000 35000 35000 35000

PV factor 0.9091 0.8264 0.7513 0.6830 0.6209 0.5645 0.5132 0.4665 0.4241 0.3855

PV of Cash flow 50909 34711 26296 23905 21732 19757 17961 16328 14843 13494

Net Present Value 239936

Annuity Factor 6.144567106

Equivalent Annual Leasing Costs 39048

Other costs 4000

Equivalent Annual Cost 43048

Answer to Question 4

Calculation of equivalent Annual cost of alternative options

Particulars Keep X Replace X with Y Replace X with Z

Initial Cost $0.00 $100,000.00 $160,000.00

Annual Maintenance and Operating

cost $90,000.00 $70,000.00 $60,000.00

Salvage Value $0.00 $30,000.00 $50,000.00

Answer to Question 3

1.

Calculation of the After Tax Cash flow of the Leasing alternatives

Particulars 1 2 3 4 5 6 7 8 9 10

Lease Cost 80000 60000 50000 50000 50000 50000 50000 50000 50000 50000

Other costs 4000 4000 4000 4000 4000 4000 4000 4000 4000 4000

Total Costs 84000 64000 54000 54000 54000 54000 54000 54000 54000 54000

Tax savings on expenses 25200 19200 16200 16200 16200 16200 16200 16200 16200 16200

After Tax Cash Flow 58800 44800 37800 37800 37800 37800 37800 37800 37800 37800

2

Calculation of Equivalent Annual cost for the alternative ($)

Particulars 1 2 3 4 5 6 7 8 9 10

After Tax Cash Flow 56000 42000 35000 35000 35000 35000 35000 35000 35000 35000

PV factor 0.9091 0.8264 0.7513 0.6830 0.6209 0.5645 0.5132 0.4665 0.4241 0.3855

PV of Cash flow 50909 34711 26296 23905 21732 19757 17961 16328 14843 13494

Net Present Value 239936

Annuity Factor 6.144567106

Equivalent Annual Leasing Costs 39048

Other costs 4000

Equivalent Annual Cost 43048

Answer to Question 4

Calculation of equivalent Annual cost of alternative options

Particulars Keep X Replace X with Y Replace X with Z

Initial Cost $0.00 $100,000.00 $160,000.00

Annual Maintenance and Operating

cost $90,000.00 $70,000.00 $60,000.00

Salvage Value $0.00 $30,000.00 $50,000.00

8PLANT PURCHASE, INSTALLATION AND REPLACEMENT

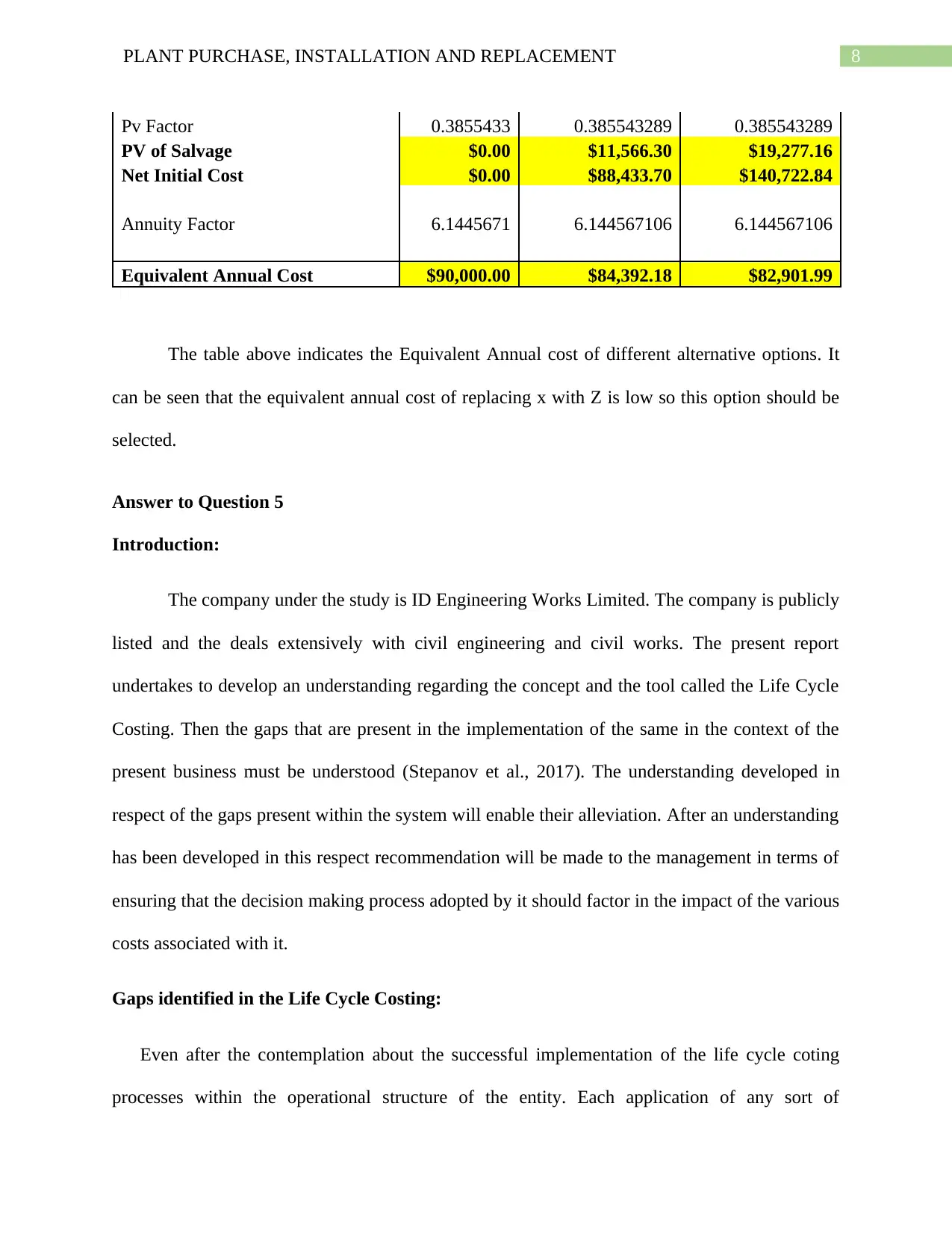

Pv Factor 0.3855433 0.385543289 0.385543289

PV of Salvage $0.00 $11,566.30 $19,277.16

Net Initial Cost $0.00 $88,433.70 $140,722.84

Annuity Factor 6.1445671 6.144567106 6.144567106

Equivalent Annual Cost $90,000.00 $84,392.18 $82,901.99

The table above indicates the Equivalent Annual cost of different alternative options. It

can be seen that the equivalent annual cost of replacing x with Z is low so this option should be

selected.

Answer to Question 5

Introduction:

The company under the study is ID Engineering Works Limited. The company is publicly

listed and the deals extensively with civil engineering and civil works. The present report

undertakes to develop an understanding regarding the concept and the tool called the Life Cycle

Costing. Then the gaps that are present in the implementation of the same in the context of the

present business must be understood (Stepanov et al., 2017). The understanding developed in

respect of the gaps present within the system will enable their alleviation. After an understanding

has been developed in this respect recommendation will be made to the management in terms of

ensuring that the decision making process adopted by it should factor in the impact of the various

costs associated with it.

Gaps identified in the Life Cycle Costing:

Even after the contemplation about the successful implementation of the life cycle coting

processes within the operational structure of the entity. Each application of any sort of

Pv Factor 0.3855433 0.385543289 0.385543289

PV of Salvage $0.00 $11,566.30 $19,277.16

Net Initial Cost $0.00 $88,433.70 $140,722.84

Annuity Factor 6.1445671 6.144567106 6.144567106

Equivalent Annual Cost $90,000.00 $84,392.18 $82,901.99

The table above indicates the Equivalent Annual cost of different alternative options. It

can be seen that the equivalent annual cost of replacing x with Z is low so this option should be

selected.

Answer to Question 5

Introduction:

The company under the study is ID Engineering Works Limited. The company is publicly

listed and the deals extensively with civil engineering and civil works. The present report

undertakes to develop an understanding regarding the concept and the tool called the Life Cycle

Costing. Then the gaps that are present in the implementation of the same in the context of the

present business must be understood (Stepanov et al., 2017). The understanding developed in

respect of the gaps present within the system will enable their alleviation. After an understanding

has been developed in this respect recommendation will be made to the management in terms of

ensuring that the decision making process adopted by it should factor in the impact of the various

costs associated with it.

Gaps identified in the Life Cycle Costing:

Even after the contemplation about the successful implementation of the life cycle coting

processes within the operational structure of the entity. Each application of any sort of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9PLANT PURCHASE, INSTALLATION AND REPLACEMENT

accounting or management tool is accompanied by certain gaps. The gaps in the implementation

of these tools and procedures arise due to several factors that are unique and sometimes

redundant in case of related entity. In the present situation, too certain gaps have been identified

in respect of the life cycle costing process implemented by the management of the company in

respect of the actualisation of the life cycle costing framework (Mohammadirad & Nagasaka,

2015). It must be noted that the application of such system must not be eliminated by the

management due to the reason that there are certain gaps present within the framework of the

tool. Rather, the management should look forward towards filling up hot gaps effectively for the

purpose of utilisation of the tool effectively and efficiently and create valuable source of

information for itself thorough its application instead. The main purpose of identification of the

gaps is thus, necessary for better implementation of the tool rather than providing the parameters

to decide the validity of the same for the company. The gaps that have been discovered in the life

cycle costing are as follows:

a) For referring to the nominal cash flows arising in respect of the entity, the management

must make use of the nominal annual yield rates. In case the management decides to use

the actual rates it must be ensured that, the cash flows are adjusted to the variations

occurring in the price level index. In addition to that, the management must also factor in

the effects of the expected annual inflation rate (Deo, 2016).

b) The costs must also be adjusted to the systematic risk that the fund provider is incurring.

The reason for this is that every person providing funds to the entity expects appropriate

and justifiable returns in respect of the risk that are being incurred by him.

c) The weights used by the management for the process must be based upon the market

values of the wide range of financial resources used up by the management. In case of

accounting or management tool is accompanied by certain gaps. The gaps in the implementation

of these tools and procedures arise due to several factors that are unique and sometimes

redundant in case of related entity. In the present situation, too certain gaps have been identified

in respect of the life cycle costing process implemented by the management of the company in

respect of the actualisation of the life cycle costing framework (Mohammadirad & Nagasaka,

2015). It must be noted that the application of such system must not be eliminated by the

management due to the reason that there are certain gaps present within the framework of the

tool. Rather, the management should look forward towards filling up hot gaps effectively for the

purpose of utilisation of the tool effectively and efficiently and create valuable source of

information for itself thorough its application instead. The main purpose of identification of the

gaps is thus, necessary for better implementation of the tool rather than providing the parameters

to decide the validity of the same for the company. The gaps that have been discovered in the life

cycle costing are as follows:

a) For referring to the nominal cash flows arising in respect of the entity, the management

must make use of the nominal annual yield rates. In case the management decides to use

the actual rates it must be ensured that, the cash flows are adjusted to the variations

occurring in the price level index. In addition to that, the management must also factor in

the effects of the expected annual inflation rate (Deo, 2016).

b) The costs must also be adjusted to the systematic risk that the fund provider is incurring.

The reason for this is that every person providing funds to the entity expects appropriate

and justifiable returns in respect of the risk that are being incurred by him.

c) The weights used by the management for the process must be based upon the market

values of the wide range of financial resources used up by the management. In case of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10PLANT PURCHASE, INSTALLATION AND REPLACEMENT

absence of information in this respect is absent the management must makes sure that it

utilises the present accounting information available with itself (Azar et al., 2014).

d) The discount rate that is being used by the management for this purpose is always subject

to change. The reason for the subjectivity of the changes of the discounting rates is due to

many factors present within the business environment of the entity, which might be

within or outside the control of the management (Di Dio et al., 2015). Some of the factors

that are responsible for this include forecasted period of the cash flows, the alterations

that might occur in the inflation rates, the presence of systematic risk and the present

capital structure of the company.

Recommendation in respect of improvement for cost/ benefit and risk management:

For the sustainability and the reliability of the operations of the assets owned by the company

or the overall l operations conducted by the company it is necessary that the cost incurred by the

entity and the returns generated in respect of them are continuously monitored by the

management. In absence of the monitoring process the processes, tools and the control systems

that are implemented by the management will go haywire in no time and will not be able to

generate revenue and thereby failing to generate value for the stakeholders of the company at

large (Oueslati et al., 2016). Some of the recommendation that is needed to be made for

improving the cost/ benefit and the risk management of the company are as follows:

a) The management should ensure the adoption of the advanced tools, various techniques of

analysis, various technologies for the purpose of optimising the management and

absence of information in this respect is absent the management must makes sure that it

utilises the present accounting information available with itself (Azar et al., 2014).

d) The discount rate that is being used by the management for this purpose is always subject

to change. The reason for the subjectivity of the changes of the discounting rates is due to

many factors present within the business environment of the entity, which might be

within or outside the control of the management (Di Dio et al., 2015). Some of the factors

that are responsible for this include forecasted period of the cash flows, the alterations

that might occur in the inflation rates, the presence of systematic risk and the present

capital structure of the company.

Recommendation in respect of improvement for cost/ benefit and risk management:

For the sustainability and the reliability of the operations of the assets owned by the company

or the overall l operations conducted by the company it is necessary that the cost incurred by the

entity and the returns generated in respect of them are continuously monitored by the

management. In absence of the monitoring process the processes, tools and the control systems

that are implemented by the management will go haywire in no time and will not be able to

generate revenue and thereby failing to generate value for the stakeholders of the company at

large (Oueslati et al., 2016). Some of the recommendation that is needed to be made for

improving the cost/ benefit and the risk management of the company are as follows:

a) The management should ensure the adoption of the advanced tools, various techniques of

analysis, various technologies for the purpose of optimising the management and

11PLANT PURCHASE, INSTALLATION AND REPLACEMENT

conducting the planning, execution and control of the industrial production.

b) The management should ensure that the discounting rate that is being chosen by it factors

in the various elements that are present in the environment of the entity. It must be able to

clearly depict the effect of the various factors on the future cash flows of the company.

c) The weights that are identified by the management must be in accordance with the market

values that the financial sources of the company bear (Bartela et al., 2014).

Conclusion:

From the above analysis, it can be concluded that the cost implications of the decisions

taken up by the management has an immense bearing on the revenue to be generated by it in the

future. And the returns that are going to be generated in respect of the stakeholders of the

company as a result of the decisions that are used or taken up by the management. It is a well-

known fact that the fixed assets owned by the company are the major sources of income that

generate revenue for the entity in the end. Hence, the decisions regarding the acquisition of such

assets form a significant part of the decisions of the management. Hence, the management must

exercise caution and ensure that the right tolls are being used by it for determining the right

decision in respect of acquisition, maintenance and the disposal of the assets of the company. In

these decisions of the management, it is guided by the various managerial tools such as Life

Cycle Costing.

conducting the planning, execution and control of the industrial production.

b) The management should ensure that the discounting rate that is being chosen by it factors

in the various elements that are present in the environment of the entity. It must be able to

clearly depict the effect of the various factors on the future cash flows of the company.

c) The weights that are identified by the management must be in accordance with the market

values that the financial sources of the company bear (Bartela et al., 2014).

Conclusion:

From the above analysis, it can be concluded that the cost implications of the decisions

taken up by the management has an immense bearing on the revenue to be generated by it in the

future. And the returns that are going to be generated in respect of the stakeholders of the

company as a result of the decisions that are used or taken up by the management. It is a well-

known fact that the fixed assets owned by the company are the major sources of income that

generate revenue for the entity in the end. Hence, the decisions regarding the acquisition of such

assets form a significant part of the decisions of the management. Hence, the management must

exercise caution and ensure that the right tolls are being used by it for determining the right

decision in respect of acquisition, maintenance and the disposal of the assets of the company. In

these decisions of the management, it is guided by the various managerial tools such as Life

Cycle Costing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.