Plant Purchase, Installation and Replacement Analysis Report - Finance

VerifiedAdded on 2021/06/17

|14

|3179

|474

Project

AI Summary

This project analyzes plant purchase, installation, and replacement decisions, focusing on financial metrics such as present worth, internal rate of return (IRR), and annual worth. The analysis includes calculations for different alternatives, comparing annual and present worth, and determining IRR. It also explores cost-benefit ratios, both conventional and modified, and evaluates leasing alternatives by calculating after-tax cash flows and equivalent annual costs. Furthermore, the project examines the equivalent annual cost of different replacement options and discusses the application of life cycle costing within Vodafone Hutchison Australia, identifying gaps in its implementation and suggesting improvements. The project provides detailed financial calculations and recommendations for optimal decision-making in plant-related investments.

Running head: PLANT PURCHASE, INSTALLATION AND REPLACEMENT

Plant purchase, Installation and replacement

Name of the Student:

Name of the University:

Authors Note:

Plant purchase, Installation and replacement

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1PLANT PURCHASE, INSTALLATION AND REPLACEMENT

Table of Contents

Answer to Question 1......................................................................................................................2

a)..................................................................................................................................................3

b)..................................................................................................................................................4

c)..................................................................................................................................................4

Answer to Question 2......................................................................................................................5

Answer to Question 3......................................................................................................................7

1...................................................................................................................................................7

2...................................................................................................................................................7

Answer to Question 4......................................................................................................................8

Answer to Question 5......................................................................................................................8

Reference.......................................................................................................................................13

Table of Contents

Answer to Question 1......................................................................................................................2

a)..................................................................................................................................................3

b)..................................................................................................................................................4

c)..................................................................................................................................................4

Answer to Question 2......................................................................................................................5

Answer to Question 3......................................................................................................................7

1...................................................................................................................................................7

2...................................................................................................................................................7

Answer to Question 4......................................................................................................................8

Answer to Question 5......................................................................................................................8

Reference.......................................................................................................................................13

2PLANT PURCHASE, INSTALLATION AND REPLACEMENT

Answer to Question 1

In the process, of capital budgeting decisions to be conducted by the company, the concepts

of present worth, internal rate of return and the annual worth hold special significance:

a) Present Worth-

It is of utmost importance that the revenue or the cash flow that is going to be accruing in

respect of the company from the project should be discounted using a suitable

discounting rate. The reason behind this is that the cash flows that are expected to arise

from the project are needed to be adjusted for the fluctuating inflation rate of the

economy, the return that is expected by the stakeholders in return of the risk undertaken

by them and several other factors. Calculation of the present worth of the inflows gives

out the real value that is going to accrue in favour of the company at the end of the

project.

b) Internal rate of return-

The percentage of the real return that is generated by the project in respect of the

company is demonstrated by the internal rate of return. The internal rate of return

generated by the project must always be above the cost of capital of the project. The cost

of capital is termed as the amount that the company will have to pay the investors in

terms of the interest and the repayment of the amount invested by the third parties (Baum

et al., 2017). It might be possible that the net present value of a project is positive but the

internal rate of return for the same is less than the cost of capital of the firm. In such a

situation, the company will fail to repay the interest and the principle amount to the third

parties from whom the company has taken the loan.

Answer to Question 1

In the process, of capital budgeting decisions to be conducted by the company, the concepts

of present worth, internal rate of return and the annual worth hold special significance:

a) Present Worth-

It is of utmost importance that the revenue or the cash flow that is going to be accruing in

respect of the company from the project should be discounted using a suitable

discounting rate. The reason behind this is that the cash flows that are expected to arise

from the project are needed to be adjusted for the fluctuating inflation rate of the

economy, the return that is expected by the stakeholders in return of the risk undertaken

by them and several other factors. Calculation of the present worth of the inflows gives

out the real value that is going to accrue in favour of the company at the end of the

project.

b) Internal rate of return-

The percentage of the real return that is generated by the project in respect of the

company is demonstrated by the internal rate of return. The internal rate of return

generated by the project must always be above the cost of capital of the project. The cost

of capital is termed as the amount that the company will have to pay the investors in

terms of the interest and the repayment of the amount invested by the third parties (Baum

et al., 2017). It might be possible that the net present value of a project is positive but the

internal rate of return for the same is less than the cost of capital of the firm. In such a

situation, the company will fail to repay the interest and the principle amount to the third

parties from whom the company has taken the loan.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3PLANT PURCHASE, INSTALLATION AND REPLACEMENT

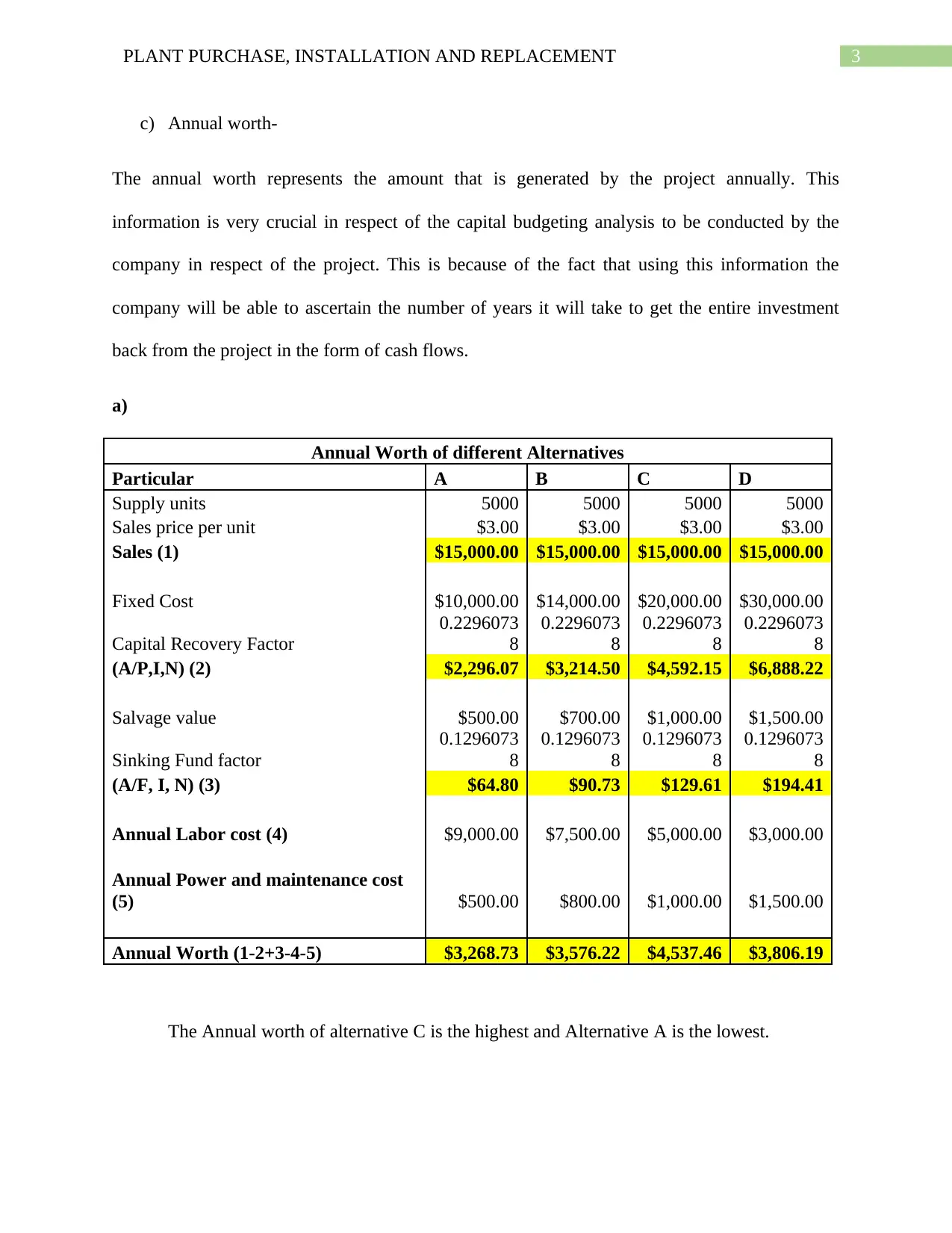

c) Annual worth-

The annual worth represents the amount that is generated by the project annually. This

information is very crucial in respect of the capital budgeting analysis to be conducted by the

company in respect of the project. This is because of the fact that using this information the

company will be able to ascertain the number of years it will take to get the entire investment

back from the project in the form of cash flows.

a)

Annual Worth of different Alternatives

Particular A B C D

Supply units 5000 5000 5000 5000

Sales price per unit $3.00 $3.00 $3.00 $3.00

Sales (1) $15,000.00 $15,000.00 $15,000.00 $15,000.00

Fixed Cost $10,000.00 $14,000.00 $20,000.00 $30,000.00

Capital Recovery Factor

0.2296073

8

0.2296073

8

0.2296073

8

0.2296073

8

(A/P,I,N) (2) $2,296.07 $3,214.50 $4,592.15 $6,888.22

Salvage value $500.00 $700.00 $1,000.00 $1,500.00

Sinking Fund factor

0.1296073

8

0.1296073

8

0.1296073

8

0.1296073

8

(A/F, I, N) (3) $64.80 $90.73 $129.61 $194.41

Annual Labor cost (4) $9,000.00 $7,500.00 $5,000.00 $3,000.00

Annual Power and maintenance cost

(5) $500.00 $800.00 $1,000.00 $1,500.00

Annual Worth (1-2+3-4-5) $3,268.73 $3,576.22 $4,537.46 $3,806.19

The Annual worth of alternative C is the highest and Alternative A is the lowest.

c) Annual worth-

The annual worth represents the amount that is generated by the project annually. This

information is very crucial in respect of the capital budgeting analysis to be conducted by the

company in respect of the project. This is because of the fact that using this information the

company will be able to ascertain the number of years it will take to get the entire investment

back from the project in the form of cash flows.

a)

Annual Worth of different Alternatives

Particular A B C D

Supply units 5000 5000 5000 5000

Sales price per unit $3.00 $3.00 $3.00 $3.00

Sales (1) $15,000.00 $15,000.00 $15,000.00 $15,000.00

Fixed Cost $10,000.00 $14,000.00 $20,000.00 $30,000.00

Capital Recovery Factor

0.2296073

8

0.2296073

8

0.2296073

8

0.2296073

8

(A/P,I,N) (2) $2,296.07 $3,214.50 $4,592.15 $6,888.22

Salvage value $500.00 $700.00 $1,000.00 $1,500.00

Sinking Fund factor

0.1296073

8

0.1296073

8

0.1296073

8

0.1296073

8

(A/F, I, N) (3) $64.80 $90.73 $129.61 $194.41

Annual Labor cost (4) $9,000.00 $7,500.00 $5,000.00 $3,000.00

Annual Power and maintenance cost

(5) $500.00 $800.00 $1,000.00 $1,500.00

Annual Worth (1-2+3-4-5) $3,268.73 $3,576.22 $4,537.46 $3,806.19

The Annual worth of alternative C is the highest and Alternative A is the lowest.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4PLANT PURCHASE, INSTALLATION AND REPLACEMENT

b)

Present Worth of different Alternatives

Particular A B C D

Sales $15,000.00 $15,000.00 $15,000.00 $15,000.00

Less:

Annual Labor cost $9,000.00 $7,500.00 $5,000.00 $3,000.00

Annual Power and maintenance cost $500.00 $800.00 $1,000.00 $1,500.00

Depreciation $1,583.33 $2,216.67 $3,166.67 $4,750.00

Taxable Income $3,916.67 $4,483.33 $5,833.33 $5,750.00

Less:

Tax Payment $1,175.00 $1,345.00 $1,750.00 $1,725.00

Net Income after tax $2,741.67 $3,138.33 $4,083.33 $4,025.00

Add:

Depreciation $1,583.33 $2,216.67 $3,166.67 $4,750.00

Annual Cash inflow after tax $4,325.00 $5,355.00 $7,250.00 $8,775.00

Present value factor of Annuity 4.3553 4.3553 4.3553 4.3553

Present Value of cash inflow after tax $18,836.50 $23,322.42 $31,575.64 $38,217.41

Salvage Value $500.00 $700.00 $1,000.00 $1,500.00

Present value factor

0.5644739

3

0.5644739

3

0.5644739

3

0.5644739

3

Present value of salvage $282.24 $395.13 $564.47 $846.71

Fixed Cost (initial Investment) $10,000.00 $14,000.00 $20,000.00 $30,000.00

Present Worth $9,118.74 $9,717.55 $12,140.11 $9,064.12

The present value of alternative C is the highest and the present value of alternative D is

the lowest.

c)

Calculation of IRR of different Alternatives

Particular A B C D

Year 0 -$10,000.00 -$14,000.00 -$20,000.00 -$30,000.00

Year 1 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 2 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 3 $18,836.50 $23,322.42 $31,575.64 $38,217.41

b)

Present Worth of different Alternatives

Particular A B C D

Sales $15,000.00 $15,000.00 $15,000.00 $15,000.00

Less:

Annual Labor cost $9,000.00 $7,500.00 $5,000.00 $3,000.00

Annual Power and maintenance cost $500.00 $800.00 $1,000.00 $1,500.00

Depreciation $1,583.33 $2,216.67 $3,166.67 $4,750.00

Taxable Income $3,916.67 $4,483.33 $5,833.33 $5,750.00

Less:

Tax Payment $1,175.00 $1,345.00 $1,750.00 $1,725.00

Net Income after tax $2,741.67 $3,138.33 $4,083.33 $4,025.00

Add:

Depreciation $1,583.33 $2,216.67 $3,166.67 $4,750.00

Annual Cash inflow after tax $4,325.00 $5,355.00 $7,250.00 $8,775.00

Present value factor of Annuity 4.3553 4.3553 4.3553 4.3553

Present Value of cash inflow after tax $18,836.50 $23,322.42 $31,575.64 $38,217.41

Salvage Value $500.00 $700.00 $1,000.00 $1,500.00

Present value factor

0.5644739

3

0.5644739

3

0.5644739

3

0.5644739

3

Present value of salvage $282.24 $395.13 $564.47 $846.71

Fixed Cost (initial Investment) $10,000.00 $14,000.00 $20,000.00 $30,000.00

Present Worth $9,118.74 $9,717.55 $12,140.11 $9,064.12

The present value of alternative C is the highest and the present value of alternative D is

the lowest.

c)

Calculation of IRR of different Alternatives

Particular A B C D

Year 0 -$10,000.00 -$14,000.00 -$20,000.00 -$30,000.00

Year 1 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 2 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 3 $18,836.50 $23,322.42 $31,575.64 $38,217.41

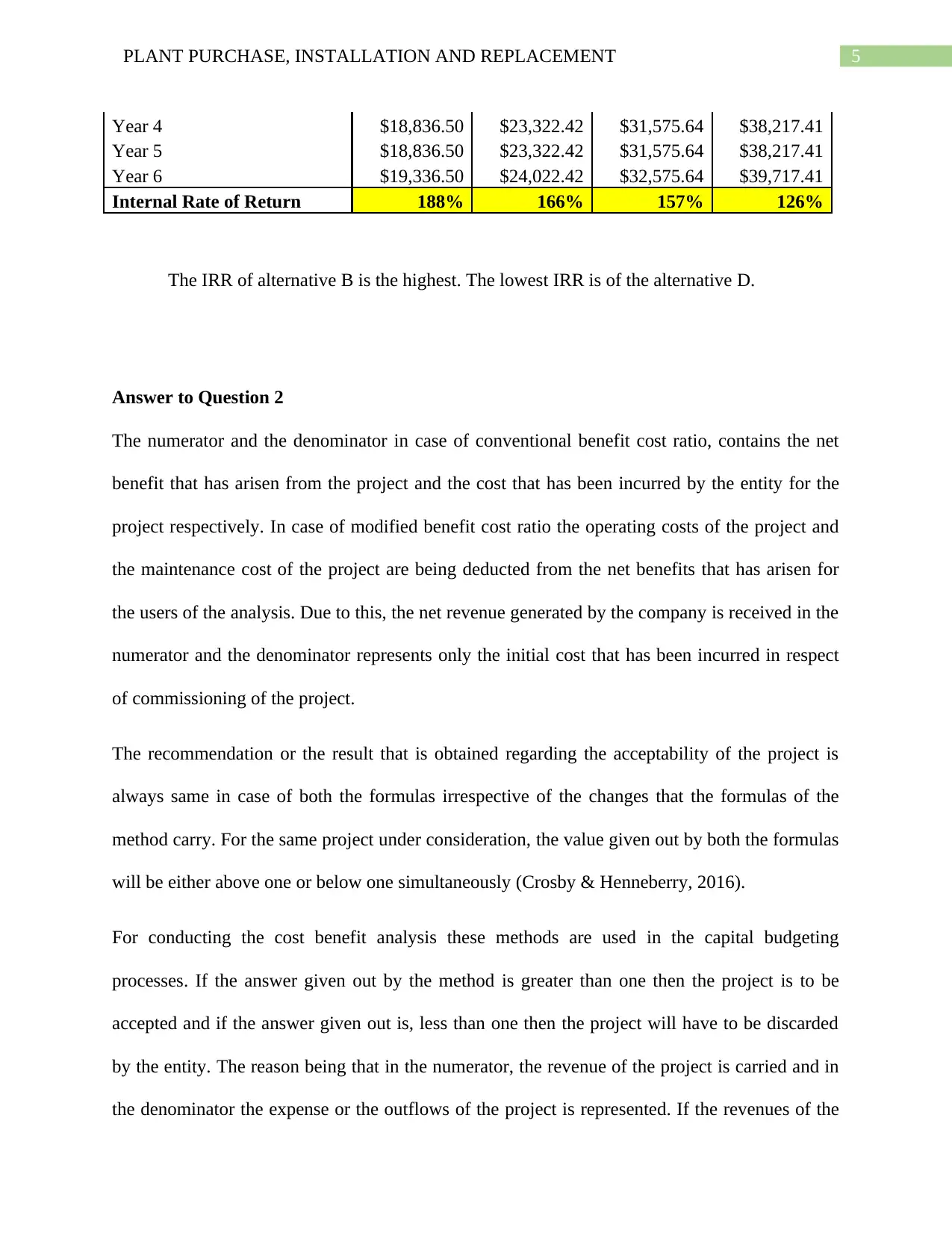

5PLANT PURCHASE, INSTALLATION AND REPLACEMENT

Year 4 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 5 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 6 $19,336.50 $24,022.42 $32,575.64 $39,717.41

Internal Rate of Return 188% 166% 157% 126%

The IRR of alternative B is the highest. The lowest IRR is of the alternative D.

Answer to Question 2

The numerator and the denominator in case of conventional benefit cost ratio, contains the net

benefit that has arisen from the project and the cost that has been incurred by the entity for the

project respectively. In case of modified benefit cost ratio the operating costs of the project and

the maintenance cost of the project are being deducted from the net benefits that has arisen for

the users of the analysis. Due to this, the net revenue generated by the company is received in the

numerator and the denominator represents only the initial cost that has been incurred in respect

of commissioning of the project.

The recommendation or the result that is obtained regarding the acceptability of the project is

always same in case of both the formulas irrespective of the changes that the formulas of the

method carry. For the same project under consideration, the value given out by both the formulas

will be either above one or below one simultaneously (Crosby & Henneberry, 2016).

For conducting the cost benefit analysis these methods are used in the capital budgeting

processes. If the answer given out by the method is greater than one then the project is to be

accepted and if the answer given out is, less than one then the project will have to be discarded

by the entity. The reason being that in the numerator, the revenue of the project is carried and in

the denominator the expense or the outflows of the project is represented. If the revenues of the

Year 4 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 5 $18,836.50 $23,322.42 $31,575.64 $38,217.41

Year 6 $19,336.50 $24,022.42 $32,575.64 $39,717.41

Internal Rate of Return 188% 166% 157% 126%

The IRR of alternative B is the highest. The lowest IRR is of the alternative D.

Answer to Question 2

The numerator and the denominator in case of conventional benefit cost ratio, contains the net

benefit that has arisen from the project and the cost that has been incurred by the entity for the

project respectively. In case of modified benefit cost ratio the operating costs of the project and

the maintenance cost of the project are being deducted from the net benefits that has arisen for

the users of the analysis. Due to this, the net revenue generated by the company is received in the

numerator and the denominator represents only the initial cost that has been incurred in respect

of commissioning of the project.

The recommendation or the result that is obtained regarding the acceptability of the project is

always same in case of both the formulas irrespective of the changes that the formulas of the

method carry. For the same project under consideration, the value given out by both the formulas

will be either above one or below one simultaneously (Crosby & Henneberry, 2016).

For conducting the cost benefit analysis these methods are used in the capital budgeting

processes. If the answer given out by the method is greater than one then the project is to be

accepted and if the answer given out is, less than one then the project will have to be discarded

by the entity. The reason being that in the numerator, the revenue of the project is carried and in

the denominator the expense or the outflows of the project is represented. If the revenues of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6PLANT PURCHASE, INSTALLATION AND REPLACEMENT

project is more than the expense of the project the result will be more than one and if the expense

are more than the revenue generated by the project then the result will be less than one.

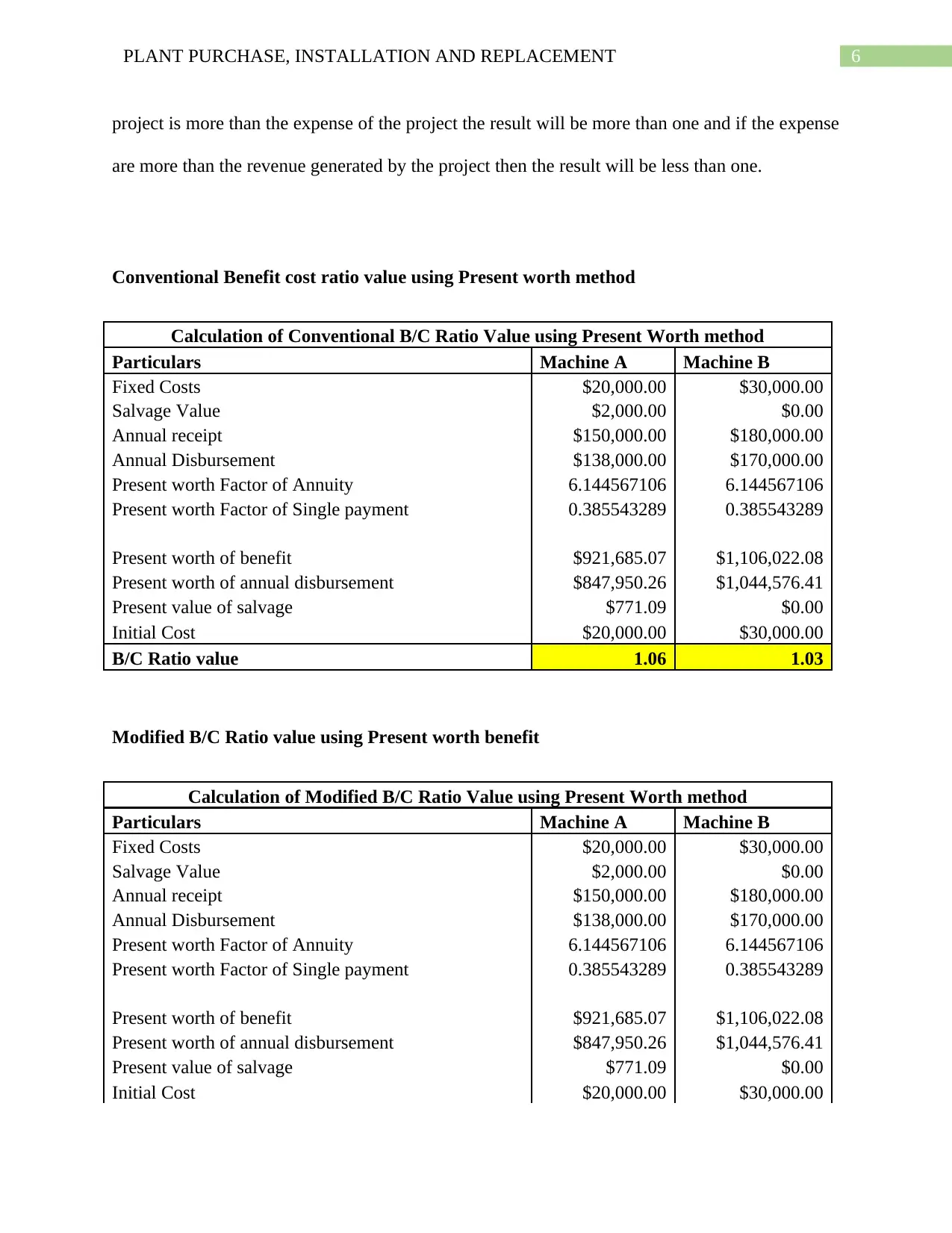

Conventional Benefit cost ratio value using Present worth method

Calculation of Conventional B/C Ratio Value using Present Worth method

Particulars Machine A Machine B

Fixed Costs $20,000.00 $30,000.00

Salvage Value $2,000.00 $0.00

Annual receipt $150,000.00 $180,000.00

Annual Disbursement $138,000.00 $170,000.00

Present worth Factor of Annuity 6.144567106 6.144567106

Present worth Factor of Single payment 0.385543289 0.385543289

Present worth of benefit $921,685.07 $1,106,022.08

Present worth of annual disbursement $847,950.26 $1,044,576.41

Present value of salvage $771.09 $0.00

Initial Cost $20,000.00 $30,000.00

B/C Ratio value 1.06 1.03

Modified B/C Ratio value using Present worth benefit

Calculation of Modified B/C Ratio Value using Present Worth method

Particulars Machine A Machine B

Fixed Costs $20,000.00 $30,000.00

Salvage Value $2,000.00 $0.00

Annual receipt $150,000.00 $180,000.00

Annual Disbursement $138,000.00 $170,000.00

Present worth Factor of Annuity 6.144567106 6.144567106

Present worth Factor of Single payment 0.385543289 0.385543289

Present worth of benefit $921,685.07 $1,106,022.08

Present worth of annual disbursement $847,950.26 $1,044,576.41

Present value of salvage $771.09 $0.00

Initial Cost $20,000.00 $30,000.00

project is more than the expense of the project the result will be more than one and if the expense

are more than the revenue generated by the project then the result will be less than one.

Conventional Benefit cost ratio value using Present worth method

Calculation of Conventional B/C Ratio Value using Present Worth method

Particulars Machine A Machine B

Fixed Costs $20,000.00 $30,000.00

Salvage Value $2,000.00 $0.00

Annual receipt $150,000.00 $180,000.00

Annual Disbursement $138,000.00 $170,000.00

Present worth Factor of Annuity 6.144567106 6.144567106

Present worth Factor of Single payment 0.385543289 0.385543289

Present worth of benefit $921,685.07 $1,106,022.08

Present worth of annual disbursement $847,950.26 $1,044,576.41

Present value of salvage $771.09 $0.00

Initial Cost $20,000.00 $30,000.00

B/C Ratio value 1.06 1.03

Modified B/C Ratio value using Present worth benefit

Calculation of Modified B/C Ratio Value using Present Worth method

Particulars Machine A Machine B

Fixed Costs $20,000.00 $30,000.00

Salvage Value $2,000.00 $0.00

Annual receipt $150,000.00 $180,000.00

Annual Disbursement $138,000.00 $170,000.00

Present worth Factor of Annuity 6.144567106 6.144567106

Present worth Factor of Single payment 0.385543289 0.385543289

Present worth of benefit $921,685.07 $1,106,022.08

Present worth of annual disbursement $847,950.26 $1,044,576.41

Present value of salvage $771.09 $0.00

Initial Cost $20,000.00 $30,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7PLANT PURCHASE, INSTALLATION AND REPLACEMENT

B/C Ratio value 3.83 2.05

Answer to Question 3

1.

Calculation of the After Tax Cash flow of the Leasing alternatives

Particulars 1 2 3 4 5 6 7 8 9 10

Lease Cost 80000 60000 50000 50000 50000 50000 50000 50000 50000 50000

Other costs 4000 4000 4000 4000 4000 4000 4000 4000 4000 4000

Total Costs 84000 64000 54000 54000 54000 54000 54000 54000 54000 54000

Tax savings on expenses 25200 19200 16200 16200 16200 16200 16200 16200 16200 16200

After Tax Cash Flow 58800 44800 37800 37800 37800 37800 37800 37800 37800 37800

2

Calculation of Equivalent Annual cost for the alternative ($)

Particulars 1 2 3 4 5 6 7 8 9 10

After Tax Cash Flow 56000 42000 35000 35000 35000 35000 35000 35000 35000 35000

PV factor 0.9091

0.826

4

0.751

3

0.683

0

0.620

9

0.564

5

0.513

2

0.466

5

0.424

1

0.385

5

PV of Cash flow 50909 34711 26296 23905 21732 19757 17961 16328 14843 13494

Net Present Value 239936

Annuity Factor

6.14456710

6

Equivalent Annual Leasing Costs 39048

Other costs 4000

Equivalent Annual Cost 43048

Answer to Question 4

Calculation of equivalent Annual cost of alternative options

Particulars Keep X Replace X with Y Replace X with Z

B/C Ratio value 3.83 2.05

Answer to Question 3

1.

Calculation of the After Tax Cash flow of the Leasing alternatives

Particulars 1 2 3 4 5 6 7 8 9 10

Lease Cost 80000 60000 50000 50000 50000 50000 50000 50000 50000 50000

Other costs 4000 4000 4000 4000 4000 4000 4000 4000 4000 4000

Total Costs 84000 64000 54000 54000 54000 54000 54000 54000 54000 54000

Tax savings on expenses 25200 19200 16200 16200 16200 16200 16200 16200 16200 16200

After Tax Cash Flow 58800 44800 37800 37800 37800 37800 37800 37800 37800 37800

2

Calculation of Equivalent Annual cost for the alternative ($)

Particulars 1 2 3 4 5 6 7 8 9 10

After Tax Cash Flow 56000 42000 35000 35000 35000 35000 35000 35000 35000 35000

PV factor 0.9091

0.826

4

0.751

3

0.683

0

0.620

9

0.564

5

0.513

2

0.466

5

0.424

1

0.385

5

PV of Cash flow 50909 34711 26296 23905 21732 19757 17961 16328 14843 13494

Net Present Value 239936

Annuity Factor

6.14456710

6

Equivalent Annual Leasing Costs 39048

Other costs 4000

Equivalent Annual Cost 43048

Answer to Question 4

Calculation of equivalent Annual cost of alternative options

Particulars Keep X Replace X with Y Replace X with Z

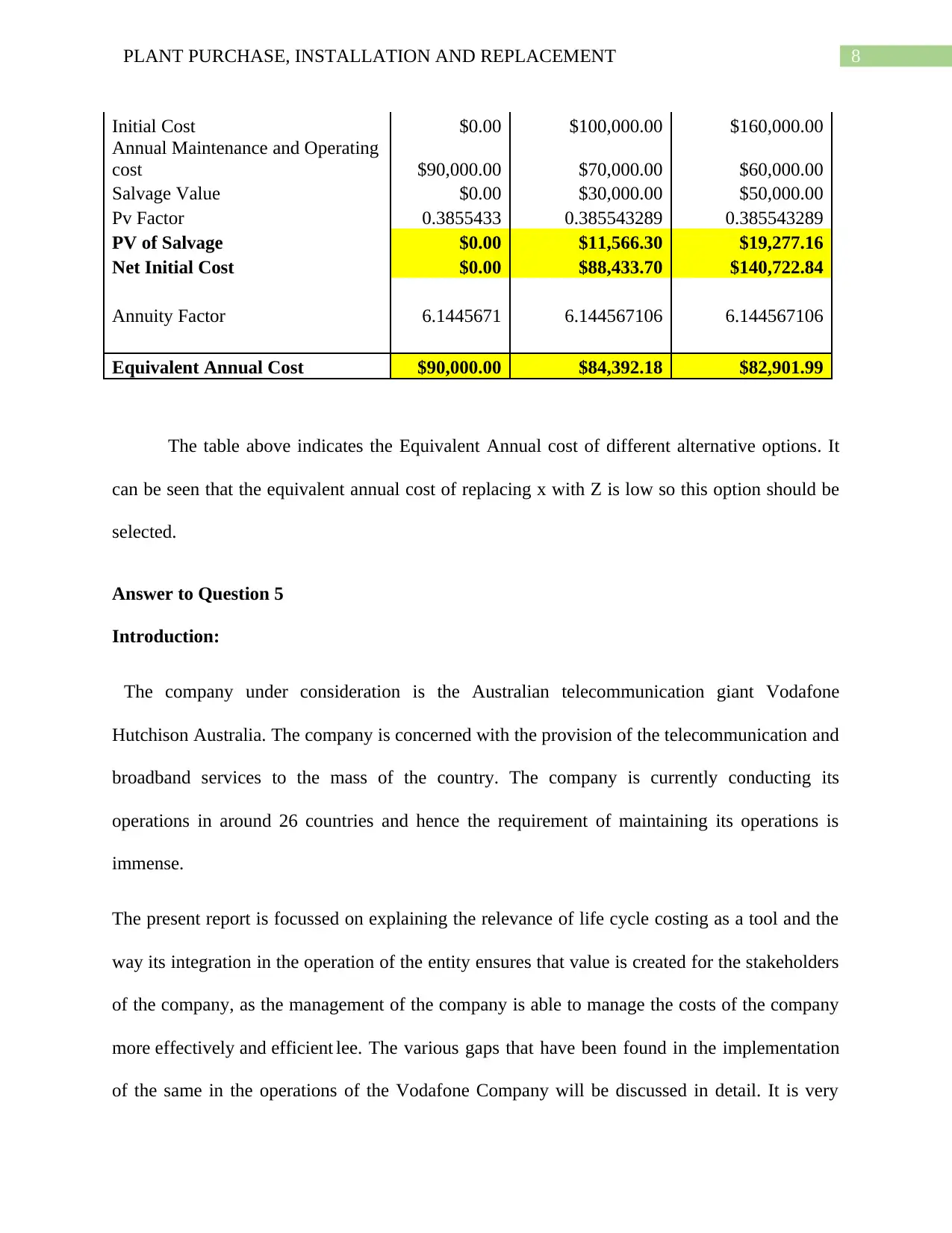

8PLANT PURCHASE, INSTALLATION AND REPLACEMENT

Initial Cost $0.00 $100,000.00 $160,000.00

Annual Maintenance and Operating

cost $90,000.00 $70,000.00 $60,000.00

Salvage Value $0.00 $30,000.00 $50,000.00

Pv Factor 0.3855433 0.385543289 0.385543289

PV of Salvage $0.00 $11,566.30 $19,277.16

Net Initial Cost $0.00 $88,433.70 $140,722.84

Annuity Factor 6.1445671 6.144567106 6.144567106

Equivalent Annual Cost $90,000.00 $84,392.18 $82,901.99

The table above indicates the Equivalent Annual cost of different alternative options. It

can be seen that the equivalent annual cost of replacing x with Z is low so this option should be

selected.

Answer to Question 5

Introduction:

The company under consideration is the Australian telecommunication giant Vodafone

Hutchison Australia. The company is concerned with the provision of the telecommunication and

broadband services to the mass of the country. The company is currently conducting its

operations in around 26 countries and hence the requirement of maintaining its operations is

immense.

The present report is focussed on explaining the relevance of life cycle costing as a tool and the

way its integration in the operation of the entity ensures that value is created for the stakeholders

of the company, as the management of the company is able to manage the costs of the company

more effectively and efficient lee. The various gaps that have been found in the implementation

of the same in the operations of the Vodafone Company will be discussed in detail. It is very

Initial Cost $0.00 $100,000.00 $160,000.00

Annual Maintenance and Operating

cost $90,000.00 $70,000.00 $60,000.00

Salvage Value $0.00 $30,000.00 $50,000.00

Pv Factor 0.3855433 0.385543289 0.385543289

PV of Salvage $0.00 $11,566.30 $19,277.16

Net Initial Cost $0.00 $88,433.70 $140,722.84

Annuity Factor 6.1445671 6.144567106 6.144567106

Equivalent Annual Cost $90,000.00 $84,392.18 $82,901.99

The table above indicates the Equivalent Annual cost of different alternative options. It

can be seen that the equivalent annual cost of replacing x with Z is low so this option should be

selected.

Answer to Question 5

Introduction:

The company under consideration is the Australian telecommunication giant Vodafone

Hutchison Australia. The company is concerned with the provision of the telecommunication and

broadband services to the mass of the country. The company is currently conducting its

operations in around 26 countries and hence the requirement of maintaining its operations is

immense.

The present report is focussed on explaining the relevance of life cycle costing as a tool and the

way its integration in the operation of the entity ensures that value is created for the stakeholders

of the company, as the management of the company is able to manage the costs of the company

more effectively and efficient lee. The various gaps that have been found in the implementation

of the same in the operations of the Vodafone Company will be discussed in detail. It is very

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9PLANT PURCHASE, INSTALLATION AND REPLACEMENT

crucial to understand the gaps that are present in the implementation process of this system. It is

necessary because only after developing an understanding regarding the gaps present in the

system it will be possible to alleviate the same (Idowu et al., 2016). Subsequently, some

recommendation will be made to the management concerning the due consideration that must be

given by it to the cost implications of the decisions taken by it in respect of the operations of the

entity.

Gaps that have been identified in the system:

It is very difficult to completely eradicate the gaps that are presented due to the implementation

or usage if any accounting toll or management tool by the company for monitoring its

procedures. The gaps and the inefficiencies of the systems are the result of the carious feature

and the characteristics that may be and may not be same for the operations of the Vodafone

Company. The gaps present in the implementation procedures of the tools should not at any cost

refrain the company from making use of such a good tool. Instead, the company must endeavour

to look for ways for alleviating the gaps that are present within the system with respect to the

application of the tool. The main purpose of identification of the gaps in the process is not to

determine whether the tool is useful for the management or not. Rather the main purpose is to

find out ways in which the gaps present in the system can be alleviated. Some of the gaps that

have bene discovered in the application of the life cycle costing process of the company are as

follows:

a) Nominal yield rates must be adopted by the company for determining the nominal cash

flows arising in respect of the company. For making use of the actual rates by the

company, it must be ensured that the cash flows generated or accruing in respect of the

crucial to understand the gaps that are present in the implementation process of this system. It is

necessary because only after developing an understanding regarding the gaps present in the

system it will be possible to alleviate the same (Idowu et al., 2016). Subsequently, some

recommendation will be made to the management concerning the due consideration that must be

given by it to the cost implications of the decisions taken by it in respect of the operations of the

entity.

Gaps that have been identified in the system:

It is very difficult to completely eradicate the gaps that are presented due to the implementation

or usage if any accounting toll or management tool by the company for monitoring its

procedures. The gaps and the inefficiencies of the systems are the result of the carious feature

and the characteristics that may be and may not be same for the operations of the Vodafone

Company. The gaps present in the implementation procedures of the tools should not at any cost

refrain the company from making use of such a good tool. Instead, the company must endeavour

to look for ways for alleviating the gaps that are present within the system with respect to the

application of the tool. The main purpose of identification of the gaps in the process is not to

determine whether the tool is useful for the management or not. Rather the main purpose is to

find out ways in which the gaps present in the system can be alleviated. Some of the gaps that

have bene discovered in the application of the life cycle costing process of the company are as

follows:

a) Nominal yield rates must be adopted by the company for determining the nominal cash

flows arising in respect of the company. For making use of the actual rates by the

company, it must be ensured that the cash flows generated or accruing in respect of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10PLANT PURCHASE, INSTALLATION AND REPLACEMENT

company must be adjusted for the variations in the price level index. The effects of the

annual fluctuating inflation rates must also be factored in by the management.

b) There are significant amount of systematic risks that are being incurred by the fund

providers the same must be adjusted against the costs. This is done because the investors

investing their money in the project FO the company also demand certain justifiable and

good returns out of the investment that is being made by them.

c) The market value of the wider angel of the financial sources that are being used by the

company must form the basis of the weights that are being chosen by the company for

this purpose. The present accounting information available with the entity must be used if

information pertaining to the market value FO the resources is not available due to some

reasons with the company.

d) It is also observed that the discounting rate that is being used by the Vodafone Company

is always subjected to change. Several factors affect the rates on a continuous basis.

These factors may or may not be in the hands of the management. These factors include

the capital structure of the company, the amount of systematic risk involved in the

project, the changes that might occur in the inflation rate of the economy and the changes

in the forecasted cash flows of the project.

The various recommendations to the management in respect of cost/ benefit and risk

management:

The continuous monitoring of the cost incurred by the company in respect of its operations

and the revenue generated by them is very crucial for ensuring that the company is able to

generate significant amount of revenues on a sustainable basis. If the monitoring of the costs

will not be conducted by the company then the process of revenue generation by the

company must be adjusted for the variations in the price level index. The effects of the

annual fluctuating inflation rates must also be factored in by the management.

b) There are significant amount of systematic risks that are being incurred by the fund

providers the same must be adjusted against the costs. This is done because the investors

investing their money in the project FO the company also demand certain justifiable and

good returns out of the investment that is being made by them.

c) The market value of the wider angel of the financial sources that are being used by the

company must form the basis of the weights that are being chosen by the company for

this purpose. The present accounting information available with the entity must be used if

information pertaining to the market value FO the resources is not available due to some

reasons with the company.

d) It is also observed that the discounting rate that is being used by the Vodafone Company

is always subjected to change. Several factors affect the rates on a continuous basis.

These factors may or may not be in the hands of the management. These factors include

the capital structure of the company, the amount of systematic risk involved in the

project, the changes that might occur in the inflation rate of the economy and the changes

in the forecasted cash flows of the project.

The various recommendations to the management in respect of cost/ benefit and risk

management:

The continuous monitoring of the cost incurred by the company in respect of its operations

and the revenue generated by them is very crucial for ensuring that the company is able to

generate significant amount of revenues on a sustainable basis. If the monitoring of the costs

will not be conducted by the company then the process of revenue generation by the

11PLANT PURCHASE, INSTALLATION AND REPLACEMENT

company will become so inefficient that the stakeholders will never be able to receive the

returns they were expecting to get. Hence, it is of utmost importance that the company

undertakes the maintenance and the upkeep of all the internal control systems and the control

mechanism installed by the company must be monitored on a regular basis. Some of the

recommendations that can be made to the management are as follows:

a) For the purpose of identification of the risks present in the environment of the Vodafone

both externally and internally, the company must undertake the adoption of the policy of

recruitment of the best financial advisors present in the market. The management must go

through the papers that are big published by the firms and the companies providing the

financial services to the entities all across the globe (Mulley et al., 2016).

b) The management must make sure that for the purpose of capital budgeting decision it

must make use of such discounting rates that takes into account the variation in the

inflation rates of the economy, the factors that affects the future cash flows of the

company and elements that are present in the environment of the entity that can affect the

company internally and externally.

c) The market values of the financial sources used by the company should form the basis of

the weights to be used by the company.

Conclusion:

the revenue generated by the company and the future expected cash flows of the entity are

greatly influenced by the cost implications of the decisions that are being taken up by the

management. The management of the company also needs to factor in the returns that are going

to be generated by the decisions that are going to be taken by the management in respect of the

projects that are going to be taken up by the management. The company makes use of the various

company will become so inefficient that the stakeholders will never be able to receive the

returns they were expecting to get. Hence, it is of utmost importance that the company

undertakes the maintenance and the upkeep of all the internal control systems and the control

mechanism installed by the company must be monitored on a regular basis. Some of the

recommendations that can be made to the management are as follows:

a) For the purpose of identification of the risks present in the environment of the Vodafone

both externally and internally, the company must undertake the adoption of the policy of

recruitment of the best financial advisors present in the market. The management must go

through the papers that are big published by the firms and the companies providing the

financial services to the entities all across the globe (Mulley et al., 2016).

b) The management must make sure that for the purpose of capital budgeting decision it

must make use of such discounting rates that takes into account the variation in the

inflation rates of the economy, the factors that affects the future cash flows of the

company and elements that are present in the environment of the entity that can affect the

company internally and externally.

c) The market values of the financial sources used by the company should form the basis of

the weights to be used by the company.

Conclusion:

the revenue generated by the company and the future expected cash flows of the entity are

greatly influenced by the cost implications of the decisions that are being taken up by the

management. The management of the company also needs to factor in the returns that are going

to be generated by the decisions that are going to be taken by the management in respect of the

projects that are going to be taken up by the management. The company makes use of the various

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.