MREGC5001 Plant Purchase, Installation, Replacement Solution

VerifiedAdded on 2023/06/12

|9

|2462

|478

Homework Assignment

AI Summary

This assignment provides a detailed solution to a finance homework problem involving plant purchase, installation, and replacement decisions. It explains and applies the concepts of Annual Worth (AW), Present Worth (PW), and Internal Rate of Return (IRR) to evaluate different degrees of automation for a manufacturing process. The assignment also covers benefit-cost ratio analysis for machine selection and lease versus purchase decisions. Furthermore, it analyzes the viability of replacing an existing asset with newer alternatives using present worth analysis. The solution also identifies gaps in life cycle costing and suggests ways to improve cost-benefit balance. Desklib offers a wealth of similar solved assignments and past papers to aid students in their studies.

Assignment 2: Plant Purchase, Installation and replacement

Name of the Student

Name of the University

Name of the Student

Name of the University

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Answer to question 1:................................................................................................................3

Answer to question 2:................................................................................................................4

Answer to question 3:................................................................................................................5

Answer to question 4:................................................................................................................6

Answer to question 5:................................................................................................................6

Introduction to costing...........................................................................................................6

Gaps Identified in life cycle costing........................................................................................6

Improving cost benefit balance..............................................................................................7

Reference List.........................................................................................................................9

Answer to question 1:................................................................................................................3

Answer to question 2:................................................................................................................4

Answer to question 3:................................................................................................................5

Answer to question 4:................................................................................................................6

Answer to question 5:................................................................................................................6

Introduction to costing...........................................................................................................6

Gaps Identified in life cycle costing........................................................................................6

Improving cost benefit balance..............................................................................................7

Reference List.........................................................................................................................9

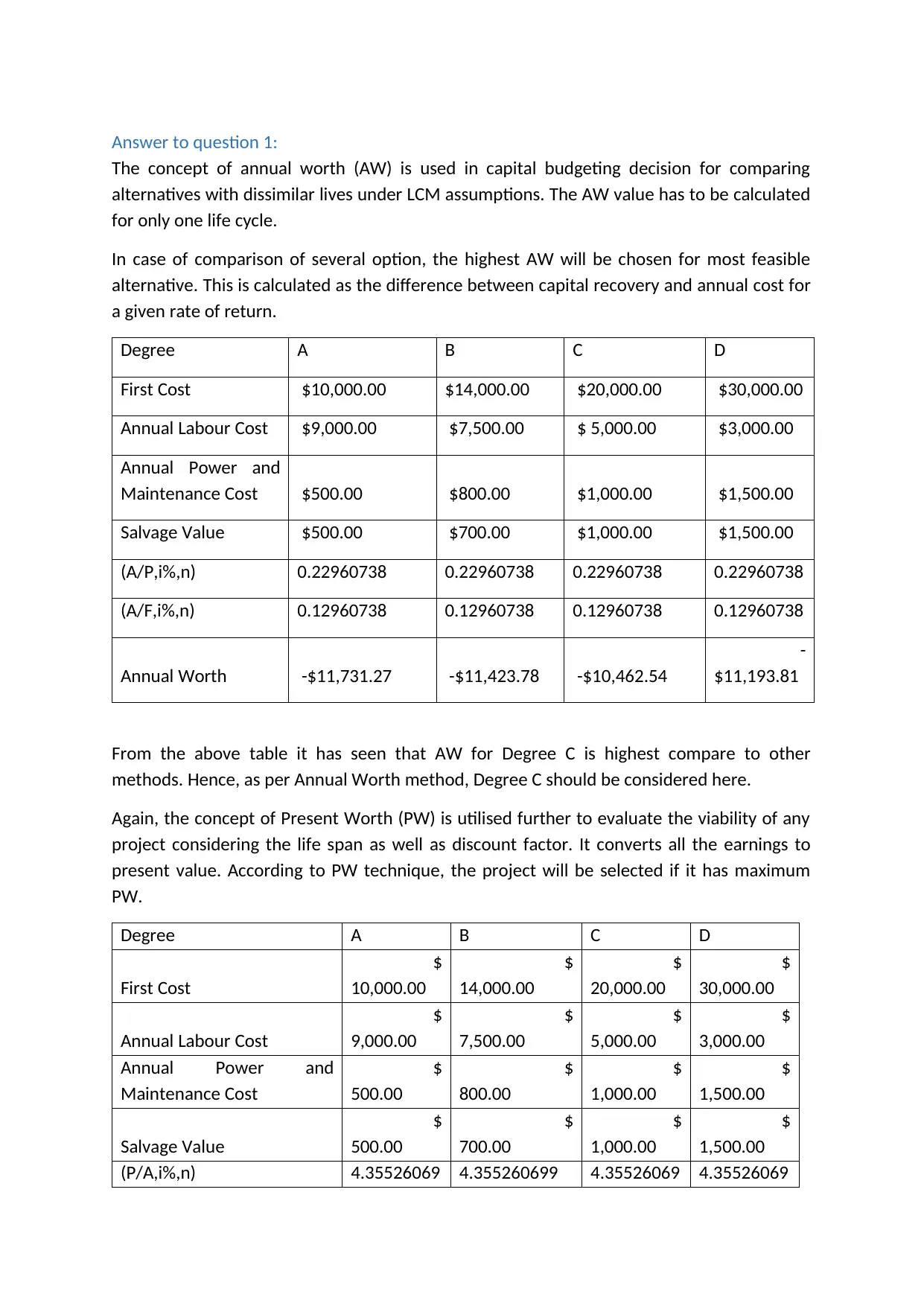

Answer to question 1:

The concept of annual worth (AW) is used in capital budgeting decision for comparing

alternatives with dissimilar lives under LCM assumptions. The AW value has to be calculated

for only one life cycle.

In case of comparison of several option, the highest AW will be chosen for most feasible

alternative. This is calculated as the difference between capital recovery and annual cost for

a given rate of return.

Degree A B C D

First Cost $10,000.00 $14,000.00 $20,000.00 $30,000.00

Annual Labour Cost $9,000.00 $7,500.00 $ 5,000.00 $3,000.00

Annual Power and

Maintenance Cost $500.00 $800.00 $1,000.00 $1,500.00

Salvage Value $500.00 $700.00 $1,000.00 $1,500.00

(A/P,i%,n) 0.22960738 0.22960738 0.22960738 0.22960738

(A/F,i%,n) 0.12960738 0.12960738 0.12960738 0.12960738

Annual Worth -$11,731.27 -$11,423.78 -$10,462.54

-

$11,193.81

From the above table it has seen that AW for Degree C is highest compare to other

methods. Hence, as per Annual Worth method, Degree C should be considered here.

Again, the concept of Present Worth (PW) is utilised further to evaluate the viability of any

project considering the life span as well as discount factor. It converts all the earnings to

present value. According to PW technique, the project will be selected if it has maximum

PW.

Degree A B C D

First Cost

$

10,000.00

$

14,000.00

$

20,000.00

$

30,000.00

Annual Labour Cost

$

9,000.00

$

7,500.00

$

5,000.00

$

3,000.00

Annual Power and

Maintenance Cost

$

500.00

$

800.00

$

1,000.00

$

1,500.00

Salvage Value

$

500.00

$

700.00

$

1,000.00

$

1,500.00

(P/A,i%,n) 4.35526069 4.355260699 4.35526069 4.35526069

The concept of annual worth (AW) is used in capital budgeting decision for comparing

alternatives with dissimilar lives under LCM assumptions. The AW value has to be calculated

for only one life cycle.

In case of comparison of several option, the highest AW will be chosen for most feasible

alternative. This is calculated as the difference between capital recovery and annual cost for

a given rate of return.

Degree A B C D

First Cost $10,000.00 $14,000.00 $20,000.00 $30,000.00

Annual Labour Cost $9,000.00 $7,500.00 $ 5,000.00 $3,000.00

Annual Power and

Maintenance Cost $500.00 $800.00 $1,000.00 $1,500.00

Salvage Value $500.00 $700.00 $1,000.00 $1,500.00

(A/P,i%,n) 0.22960738 0.22960738 0.22960738 0.22960738

(A/F,i%,n) 0.12960738 0.12960738 0.12960738 0.12960738

Annual Worth -$11,731.27 -$11,423.78 -$10,462.54

-

$11,193.81

From the above table it has seen that AW for Degree C is highest compare to other

methods. Hence, as per Annual Worth method, Degree C should be considered here.

Again, the concept of Present Worth (PW) is utilised further to evaluate the viability of any

project considering the life span as well as discount factor. It converts all the earnings to

present value. According to PW technique, the project will be selected if it has maximum

PW.

Degree A B C D

First Cost

$

10,000.00

$

14,000.00

$

20,000.00

$

30,000.00

Annual Labour Cost

$

9,000.00

$

7,500.00

$

5,000.00

$

3,000.00

Annual Power and

Maintenance Cost

$

500.00

$

800.00

$

1,000.00

$

1,500.00

Salvage Value

$

500.00

$

700.00

$

1,000.00

$

1,500.00

(P/A,i%,n) 4.35526069 4.355260699 4.35526069 4.35526069

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9 9 9

(P/F,i%,n) 0.56447393 0.56447393 0.56447393 0.56447393

Present Worth

$ -

51,092.74

$ -

49,753.53

$ -

45,567.09

$ -

48,751.96

The above table has shown that Degree C has the highest PW and thus it will be selected.

Finally, the initial rate of return (IRR) is the most useful technique in capital budgeting

decision, as it considered all time value of money constraints. This is a specific rate, where

the NPV of any proposed project/investment will be zero. According to IRR, if the rate is

higher than rate of return, then the project will be financially feasible. In case of multiple

alternatives, project/option with highest will be chosen. According to the IRR calculations,

Degree A will be chosen as it has the highest IRR compare to rest three alternatives.

IRR

Degree A 37%

Degree B 31%

Degree C 28%

Degree D 19%

Answer to question 2:

The benefit and cost ratio (BCR) explains the association between costs as well as benefits of

any project. This method is used to assess the project cost and benefits considering both

qualitative and quantitative aspects. However, in case of qualitative factors, these are

converted to financial terms to perform this calculation. It is the proportion of discounted

benefits and discounted costs for given discounting factor. In case of modified benefit cost

ratio, the operating and maintenance cost is subtracted from the benefits and then the

proportion is calculated.

For the given two options, the Benefit cost ratios are as follows:

BCR

Machine A 106.28%

Machine B 102.93%

Since, Machine A has the highest BCR, it should be selected to produce greater revenue.

(P/F,i%,n) 0.56447393 0.56447393 0.56447393 0.56447393

Present Worth

$ -

51,092.74

$ -

49,753.53

$ -

45,567.09

$ -

48,751.96

The above table has shown that Degree C has the highest PW and thus it will be selected.

Finally, the initial rate of return (IRR) is the most useful technique in capital budgeting

decision, as it considered all time value of money constraints. This is a specific rate, where

the NPV of any proposed project/investment will be zero. According to IRR, if the rate is

higher than rate of return, then the project will be financially feasible. In case of multiple

alternatives, project/option with highest will be chosen. According to the IRR calculations,

Degree A will be chosen as it has the highest IRR compare to rest three alternatives.

IRR

Degree A 37%

Degree B 31%

Degree C 28%

Degree D 19%

Answer to question 2:

The benefit and cost ratio (BCR) explains the association between costs as well as benefits of

any project. This method is used to assess the project cost and benefits considering both

qualitative and quantitative aspects. However, in case of qualitative factors, these are

converted to financial terms to perform this calculation. It is the proportion of discounted

benefits and discounted costs for given discounting factor. In case of modified benefit cost

ratio, the operating and maintenance cost is subtracted from the benefits and then the

proportion is calculated.

For the given two options, the Benefit cost ratios are as follows:

BCR

Machine A 106.28%

Machine B 102.93%

Since, Machine A has the highest BCR, it should be selected to produce greater revenue.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

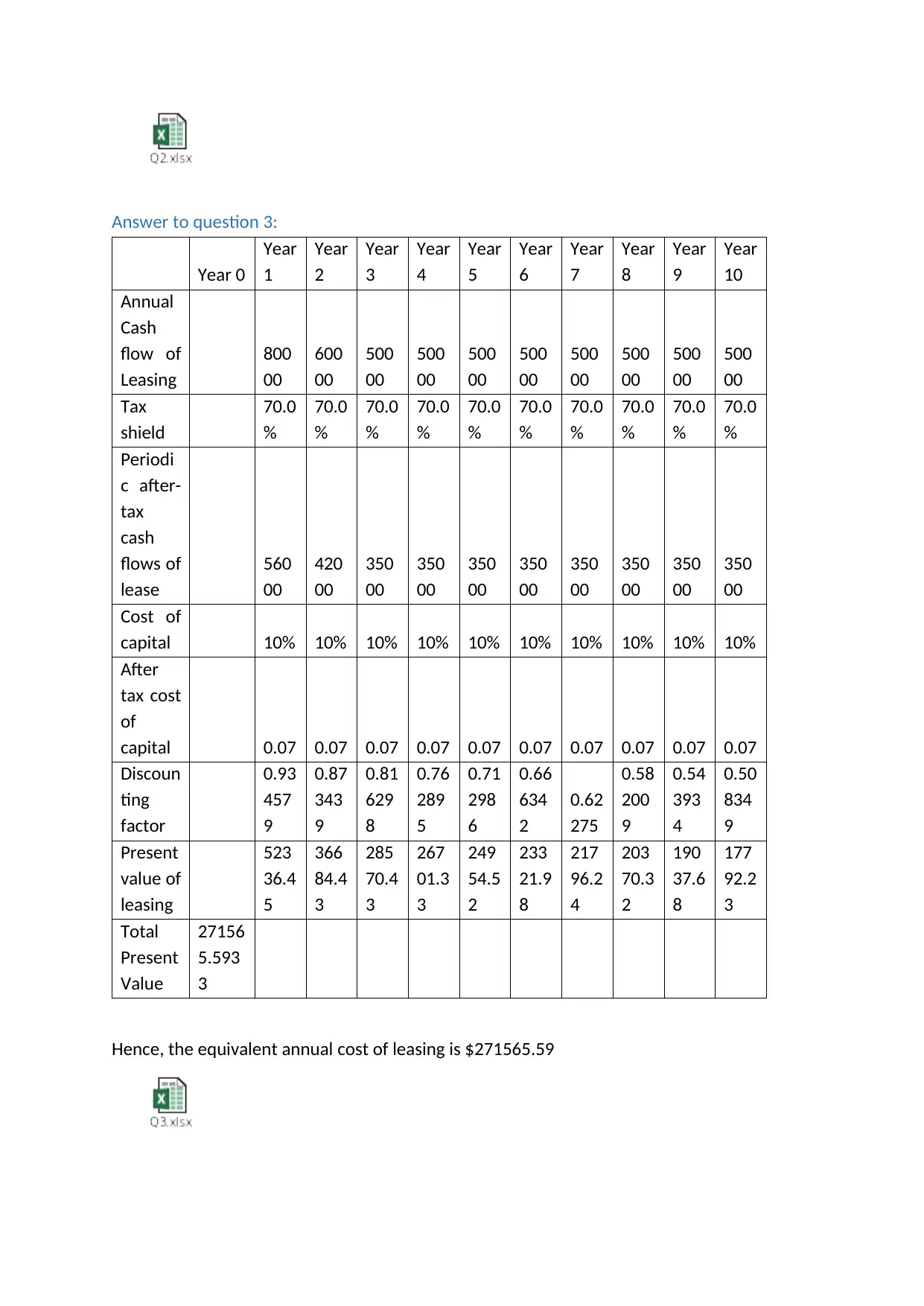

Answer to question 3:

Year 0

Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

Annual

Cash

flow of

Leasing

800

00

600

00

500

00

500

00

500

00

500

00

500

00

500

00

500

00

500

00

Tax

shield

70.0

%

70.0

%

70.0

%

70.0

%

70.0

%

70.0

%

70.0

%

70.0

%

70.0

%

70.0

%

Periodi

c after-

tax

cash

flows of

lease

560

00

420

00

350

00

350

00

350

00

350

00

350

00

350

00

350

00

350

00

Cost of

capital 10% 10% 10% 10% 10% 10% 10% 10% 10% 10%

After

tax cost

of

capital 0.07 0.07 0.07 0.07 0.07 0.07 0.07 0.07 0.07 0.07

Discoun

ting

factor

0.93

457

9

0.87

343

9

0.81

629

8

0.76

289

5

0.71

298

6

0.66

634

2

0.62

275

0.58

200

9

0.54

393

4

0.50

834

9

Present

value of

leasing

523

36.4

5

366

84.4

3

285

70.4

3

267

01.3

3

249

54.5

2

233

21.9

8

217

96.2

4

203

70.3

2

190

37.6

8

177

92.2

3

Total

Present

Value

27156

5.593

3

Hence, the equivalent annual cost of leasing is $271565.59

Year 0

Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

Annual

Cash

flow of

Leasing

800

00

600

00

500

00

500

00

500

00

500

00

500

00

500

00

500

00

500

00

Tax

shield

70.0

%

70.0

%

70.0

%

70.0

%

70.0

%

70.0

%

70.0

%

70.0

%

70.0

%

70.0

%

Periodi

c after-

tax

cash

flows of

lease

560

00

420

00

350

00

350

00

350

00

350

00

350

00

350

00

350

00

350

00

Cost of

capital 10% 10% 10% 10% 10% 10% 10% 10% 10% 10%

After

tax cost

of

capital 0.07 0.07 0.07 0.07 0.07 0.07 0.07 0.07 0.07 0.07

Discoun

ting

factor

0.93

457

9

0.87

343

9

0.81

629

8

0.76

289

5

0.71

298

6

0.66

634

2

0.62

275

0.58

200

9

0.54

393

4

0.50

834

9

Present

value of

leasing

523

36.4

5

366

84.4

3

285

70.4

3

267

01.3

3

249

54.5

2

233

21.9

8

217

96.2

4

203

70.3

2

190

37.6

8

177

92.2

3

Total

Present

Value

27156

5.593

3

Hence, the equivalent annual cost of leasing is $271565.59

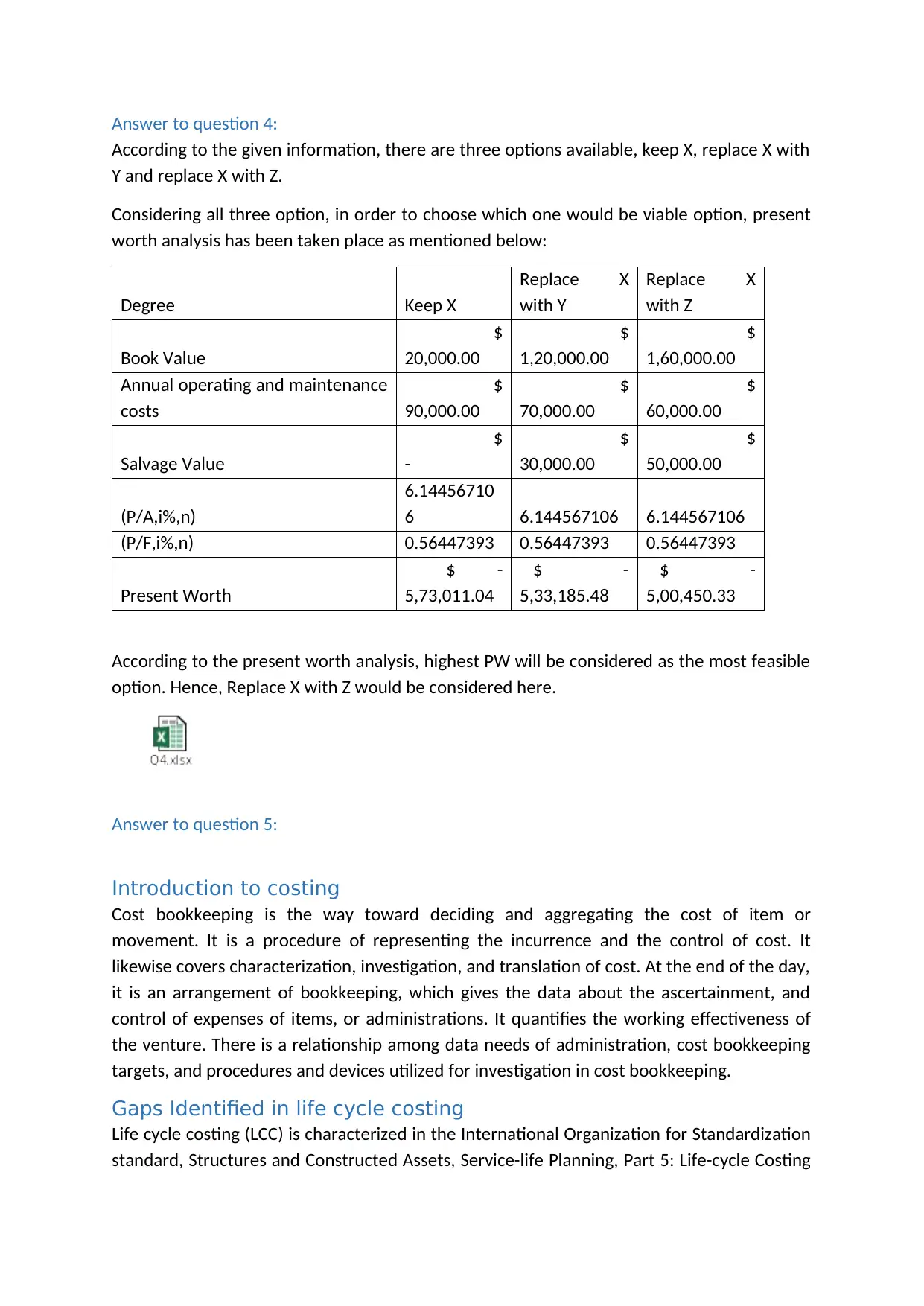

Answer to question 4:

According to the given information, there are three options available, keep X, replace X with

Y and replace X with Z.

Considering all three option, in order to choose which one would be viable option, present

worth analysis has been taken place as mentioned below:

Degree Keep X

Replace X

with Y

Replace X

with Z

Book Value

$

20,000.00

$

1,20,000.00

$

1,60,000.00

Annual operating and maintenance

costs

$

90,000.00

$

70,000.00

$

60,000.00

Salvage Value

$

-

$

30,000.00

$

50,000.00

(P/A,i%,n)

6.14456710

6 6.144567106 6.144567106

(P/F,i%,n) 0.56447393 0.56447393 0.56447393

Present Worth

$ -

5,73,011.04

$ -

5,33,185.48

$ -

5,00,450.33

According to the present worth analysis, highest PW will be considered as the most feasible

option. Hence, Replace X with Z would be considered here.

Answer to question 5:

Introduction to costing

Cost bookkeeping is the way toward deciding and aggregating the cost of item or

movement. It is a procedure of representing the incurrence and the control of cost. It

likewise covers characterization, investigation, and translation of cost. At the end of the day,

it is an arrangement of bookkeeping, which gives the data about the ascertainment, and

control of expenses of items, or administrations. It quantifies the working effectiveness of

the venture. There is a relationship among data needs of administration, cost bookkeeping

targets, and procedures and devices utilized for investigation in cost bookkeeping.

Gaps Identified in life cycle costing

Life cycle costing (LCC) is characterized in the International Organization for Standardization

standard, Structures and Constructed Assets, Service-life Planning, Part 5: Life-cycle Costing

According to the given information, there are three options available, keep X, replace X with

Y and replace X with Z.

Considering all three option, in order to choose which one would be viable option, present

worth analysis has been taken place as mentioned below:

Degree Keep X

Replace X

with Y

Replace X

with Z

Book Value

$

20,000.00

$

1,20,000.00

$

1,60,000.00

Annual operating and maintenance

costs

$

90,000.00

$

70,000.00

$

60,000.00

Salvage Value

$

-

$

30,000.00

$

50,000.00

(P/A,i%,n)

6.14456710

6 6.144567106 6.144567106

(P/F,i%,n) 0.56447393 0.56447393 0.56447393

Present Worth

$ -

5,73,011.04

$ -

5,33,185.48

$ -

5,00,450.33

According to the present worth analysis, highest PW will be considered as the most feasible

option. Hence, Replace X with Z would be considered here.

Answer to question 5:

Introduction to costing

Cost bookkeeping is the way toward deciding and aggregating the cost of item or

movement. It is a procedure of representing the incurrence and the control of cost. It

likewise covers characterization, investigation, and translation of cost. At the end of the day,

it is an arrangement of bookkeeping, which gives the data about the ascertainment, and

control of expenses of items, or administrations. It quantifies the working effectiveness of

the venture. There is a relationship among data needs of administration, cost bookkeeping

targets, and procedures and devices utilized for investigation in cost bookkeeping.

Gaps Identified in life cycle costing

Life cycle costing (LCC) is characterized in the International Organization for Standardization

standard, Structures and Constructed Assets, Service-life Planning, Part 5: Life-cycle Costing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(ISO 15686-5) as a "monetary appraisal considering all concurred anticipated critical and

pertinent cost streams over a period of examination communicated in money related

esteem. The anticipated expenses are those expected to accomplish characterized levels of

execution, including unwavering quality, wellbeing and accessibility."

The utilization of LCC is basic to show that acquisition procedures and choices need to move

past considering the price tag of a decent or on the other hand benefit, at the buy cost does

not mirror the budgetary and non-monetary profits that are advertised by earth and socially

best resources as they gather amid the activities and utilize stages of the benefit life cycle

(Lanen, 2016).

However, there are several research works that identified that LCC has several issue or gap

while applying to current scenario. The first and foremost gap in LCC is that any decision

taken considering this LCC will lead paying more upfront (Ellul et al. 2015). In a few nations,

the generation of maintainable and LCC-proficient products and ventures is still embryonic,

which implies that the best way to source maintainable options will be through costly

imports or paying a high cost premium to fortify baby neighbourhood businesses. In bring

down pay economies, this distinction can be higher, as much as 10 to 50 for each penny. In

time, in any case, the substantial volumes requested by open obtainment contracts can

make economies of scale more attainable, and the costs of these items can be relied upon

to diminish as more makers enter the market. Moreover, open procurers can start to utilize

their solid market situating to arrange mass rebates as the advertise starts to develop (Taleb

et al. 2015).

Another important gap in LCC is that the capital as well as revenue budgets are conflicting in

terms of organisation’s nature as well as time frame. There is additionally the issue of

spending proprietorship, in other words, split duties regarding capital and working costs.

While obtainment contracting may be the obligation of one organization, spending plans are

controlled by another and the utilization and upkeep of the item/benefit/advancement has

a place with yet another (Christ and Burritt, 2015). As the advantages of SPP collect amid the

undertaking life and at its end transfer, those bearing the capital expenses may not be the

first to understand the advantages of reasonable options. Further, there are issue related

application of LCC due to insufficient amount of research.

Improving cost benefit balance

The crucial legitimization for the use of money saving advantage examination (all the more

effectively social cost advantage investigation, however we overlook that capability for

effortlessness) is that it permits arrangement producers to evaluate whether an undertaking

conveys picks up in monetary productivity (Bierer et al. 2015). The thought of effectiveness

being evoked here is that depicted by the Hicks-Kaldor paradigm: in particular that a

venture is an change over the present state of affairs on the off chance that it is feasible for

those that advantage from the venture to repay those that lose, and still be in an ideal

pertinent cost streams over a period of examination communicated in money related

esteem. The anticipated expenses are those expected to accomplish characterized levels of

execution, including unwavering quality, wellbeing and accessibility."

The utilization of LCC is basic to show that acquisition procedures and choices need to move

past considering the price tag of a decent or on the other hand benefit, at the buy cost does

not mirror the budgetary and non-monetary profits that are advertised by earth and socially

best resources as they gather amid the activities and utilize stages of the benefit life cycle

(Lanen, 2016).

However, there are several research works that identified that LCC has several issue or gap

while applying to current scenario. The first and foremost gap in LCC is that any decision

taken considering this LCC will lead paying more upfront (Ellul et al. 2015). In a few nations,

the generation of maintainable and LCC-proficient products and ventures is still embryonic,

which implies that the best way to source maintainable options will be through costly

imports or paying a high cost premium to fortify baby neighbourhood businesses. In bring

down pay economies, this distinction can be higher, as much as 10 to 50 for each penny. In

time, in any case, the substantial volumes requested by open obtainment contracts can

make economies of scale more attainable, and the costs of these items can be relied upon

to diminish as more makers enter the market. Moreover, open procurers can start to utilize

their solid market situating to arrange mass rebates as the advertise starts to develop (Taleb

et al. 2015).

Another important gap in LCC is that the capital as well as revenue budgets are conflicting in

terms of organisation’s nature as well as time frame. There is additionally the issue of

spending proprietorship, in other words, split duties regarding capital and working costs.

While obtainment contracting may be the obligation of one organization, spending plans are

controlled by another and the utilization and upkeep of the item/benefit/advancement has

a place with yet another (Christ and Burritt, 2015). As the advantages of SPP collect amid the

undertaking life and at its end transfer, those bearing the capital expenses may not be the

first to understand the advantages of reasonable options. Further, there are issue related

application of LCC due to insufficient amount of research.

Improving cost benefit balance

The crucial legitimization for the use of money saving advantage examination (all the more

effectively social cost advantage investigation, however we overlook that capability for

effortlessness) is that it permits arrangement producers to evaluate whether an undertaking

conveys picks up in monetary productivity (Bierer et al. 2015). The thought of effectiveness

being evoked here is that depicted by the Hicks-Kaldor paradigm: in particular that a

venture is an change over the present state of affairs on the off chance that it is feasible for

those that advantage from the venture to repay those that lose, and still be in an ideal

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

situation themselves. The Hicks-Kaldor measure is on the other hand known as the potential

Pareto change model or basically the pay guideline (Just et al., 2005).

A fruitful advantage cost investigation produces believable outcomes at a level of detail that

is proper for its expected utilize and the task's level of examination (Rieckhof et al. 2015).

The underlying arranging exercises ought to characterize a typical structure for contrasting

the impacts of an Alternative against the Base Case. Vital components to characterize right

on time in the examination procedure incorporate the interstate situations to be dissected,

the begin and end a very long time for the investigation, the geological zone considered, and

the approach that will be utilized to break down movement conduct. It is fundamental that

all choices be produced and investigated to a similar level of detail; this ought to be

represented in the arranging stage (Ladabaum et al. 2017). A typical system can be set up by

finishing the accompanying below process:

An initial phase in setting up a structure for the examination is to characterize the

motivation behind the advantage cost investigation. Recognizing the motivation behind the

investigation characterizes the level of detail suitable for the examination. Two different

factors additionally help characterize the fitting level of detail: accessible information and

investigation spending plan. Accessible information fluctuates by task and impacts the level

of detail proper for the advantage cost investigation. Information sources go from

customary building techniques to modern provincial travel request models. The accessibility

of this information differs with each undertaking. Advantage cost examination arranging

ought to set up what information is accessible, and after that check that the accessible

information suits the investigation reason and gives the proper level of detail for the

advantage cost investigation. The investigation spending impacts the suitable level of detail

too. The level of detail ought to be reliable all through the investigation (the same for the

Base Case and Alternatives) and comparable with the accessible spending plan.

Pareto change model or basically the pay guideline (Just et al., 2005).

A fruitful advantage cost investigation produces believable outcomes at a level of detail that

is proper for its expected utilize and the task's level of examination (Rieckhof et al. 2015).

The underlying arranging exercises ought to characterize a typical structure for contrasting

the impacts of an Alternative against the Base Case. Vital components to characterize right

on time in the examination procedure incorporate the interstate situations to be dissected,

the begin and end a very long time for the investigation, the geological zone considered, and

the approach that will be utilized to break down movement conduct. It is fundamental that

all choices be produced and investigated to a similar level of detail; this ought to be

represented in the arranging stage (Ladabaum et al. 2017). A typical system can be set up by

finishing the accompanying below process:

An initial phase in setting up a structure for the examination is to characterize the

motivation behind the advantage cost investigation. Recognizing the motivation behind the

investigation characterizes the level of detail suitable for the examination. Two different

factors additionally help characterize the fitting level of detail: accessible information and

investigation spending plan. Accessible information fluctuates by task and impacts the level

of detail proper for the advantage cost investigation. Information sources go from

customary building techniques to modern provincial travel request models. The accessibility

of this information differs with each undertaking. Advantage cost examination arranging

ought to set up what information is accessible, and after that check that the accessible

information suits the investigation reason and gives the proper level of detail for the

advantage cost investigation. The investigation spending impacts the suitable level of detail

too. The level of detail ought to be reliable all through the investigation (the same for the

Base Case and Alternatives) and comparable with the accessible spending plan.

Reference List

Bierer, A., Götze, U., Meynerts, L. and Sygulla, R., 2015. Integrating life cycle costing and life

cycle assessment using extended material flow cost accounting. Journal of Cleaner

Production, 108, pp.1289-1301.

Christ, K.L. and Burritt, R.L., 2015. Material flow cost accounting: a review and agenda for

future research. Journal of Cleaner Production, 108, pp.1378-1389.

Ellul, A., Jotikasthira, C., Lundblad, C.T. and Wang, Y., 2015. Is historical cost accounting a

panacea? Market stress, incentive distortions, and gains trading. The Journal of

Finance, 70(6), pp.2489-2538.

Ladabaum, U., Mannalithara, A., Rachocki, C., Laleau, V., Garcia, D., Chen, E., Grimes, B.,

Vittinghoff, E. and Somsouk, M., 2017. Prospective Cost-Accounting of an Outreach Program

to Increase Fecal Immunochemical Test (FIT)-Based Colorectal Cancer (CRC) Screening

Among Underinsured Persons in a Randomized Trial. Gastroenterology, 152(5), p.S75.

Lanen, W., 2016. Fundamentals of cost accounting. McGraw-Hill Higher Education.

Rieckhof, R., Bergmann, A. and Guenther, E., 2015. Interrelating material flow cost

accounting with management control systems to introduce resource efficiency into

strategy. Journal of Cleaner Production, 108, pp.1262-1278.

Taleb, M.A., Gibson, B. and Hovey, M., 2015. Fifty years of Sustainability Accounting: does

accounting for income in business sustainability really exist?. International Journal of

Accounting and Financial Reporting, 5(1), pp.36-47.

Bierer, A., Götze, U., Meynerts, L. and Sygulla, R., 2015. Integrating life cycle costing and life

cycle assessment using extended material flow cost accounting. Journal of Cleaner

Production, 108, pp.1289-1301.

Christ, K.L. and Burritt, R.L., 2015. Material flow cost accounting: a review and agenda for

future research. Journal of Cleaner Production, 108, pp.1378-1389.

Ellul, A., Jotikasthira, C., Lundblad, C.T. and Wang, Y., 2015. Is historical cost accounting a

panacea? Market stress, incentive distortions, and gains trading. The Journal of

Finance, 70(6), pp.2489-2538.

Ladabaum, U., Mannalithara, A., Rachocki, C., Laleau, V., Garcia, D., Chen, E., Grimes, B.,

Vittinghoff, E. and Somsouk, M., 2017. Prospective Cost-Accounting of an Outreach Program

to Increase Fecal Immunochemical Test (FIT)-Based Colorectal Cancer (CRC) Screening

Among Underinsured Persons in a Randomized Trial. Gastroenterology, 152(5), p.S75.

Lanen, W., 2016. Fundamentals of cost accounting. McGraw-Hill Higher Education.

Rieckhof, R., Bergmann, A. and Guenther, E., 2015. Interrelating material flow cost

accounting with management control systems to introduce resource efficiency into

strategy. Journal of Cleaner Production, 108, pp.1262-1278.

Taleb, M.A., Gibson, B. and Hovey, M., 2015. Fifty years of Sustainability Accounting: does

accounting for income in business sustainability really exist?. International Journal of

Accounting and Financial Reporting, 5(1), pp.36-47.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.