Accounting Information System Weaknesses: Platinum Case Analysis

VerifiedAdded on 2023/06/12

|10

|2332

|246

Case Study

AI Summary

This case study solution provides an in-depth analysis of the Platinum Group's special ordering and procurement processes, utilizing a level 0 data flow diagram to pinpoint weaknesses and propose viable solutions. The evaluation reveals reliance on manual processes, a lack of standardized procurement procedures, and inadequate internal controls, making the system vulnerable to manipulation and internal fraud, particularly in supplier selection and automated check signing. These weaknesses expose the company to procurement risks, including substandard products, uncompetitive pricing, and potential fraudulent activities. The proposed solutions involve implementing a computerized system for order management and establishing a competitive procurement process where potential suppliers submit offers that are collectively evaluated by a buyer team to ensure unbiased supplier selection. The recommendations also emphasize documented order placements, competitive supplier selection, and the elimination of automated check signing, with further modifications suggesting the integration of ICT and SCM software to streamline procurement processes and enhance control policies.

Running Head: ACCOUNTING INFORMATION SYSTEM- PLATINUM CASE 1

Accounting Information System- Platinum Case

Name

Date

Accounting Information System- Platinum Case

Name

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING INFORMATION SYSTEM- PLATINUM CASE 2

Table of Contents

Executive Summary.....................................................................................................................................3

Brief Description of Special ordering System...............................................................................................4

Level 0 Data Flow Diagram..........................................................................................................................4

Internal Control Weaknesses.......................................................................................................................5

Impacts of the Weaknesses on the Organization.........................................................................................6

Measures to mitigate internal weaknesses in special orders at Platinum...................................................7

Modifications to the recommendations.................................................................................................7

References...................................................................................................................................................9

Table of Contents

Executive Summary.....................................................................................................................................3

Brief Description of Special ordering System...............................................................................................4

Level 0 Data Flow Diagram..........................................................................................................................4

Internal Control Weaknesses.......................................................................................................................5

Impacts of the Weaknesses on the Organization.........................................................................................6

Measures to mitigate internal weaknesses in special orders at Platinum...................................................7

Modifications to the recommendations.................................................................................................7

References...................................................................................................................................................9

ACCOUNTING INFORMATION SYSTEM- PLATINUM CASE 3

Executive Summary

This paper evaluated the existing process of procurement for Platinum Group for special

ordering and procurement using a level 0 data flow diagram, with a view to identifying

weaknesses and proposing suitable solutions. Evaluating the system identified manual

approaches, lack of an established procurement process and weak internal controls. The special

ordering and procurement is prone to manipulation and abuse, especially in identifying suppliers

while automated check signing can be prone to abuse. Further, the manual system is time and

resource wasting and unwieldy. The impacts of these weaknesses is exposing the company to

procurement risks, such as substandard products, non competitive pricing, and potential for

internal fraud. A proposed solution is the use of a computerized system to manage orders,

establish a competitive procurement process where all potential suppliers give offers and the

buyers’ sit as a team, evaluate the offers, and select suppliers after a unanimous agreement

Executive Summary

This paper evaluated the existing process of procurement for Platinum Group for special

ordering and procurement using a level 0 data flow diagram, with a view to identifying

weaknesses and proposing suitable solutions. Evaluating the system identified manual

approaches, lack of an established procurement process and weak internal controls. The special

ordering and procurement is prone to manipulation and abuse, especially in identifying suppliers

while automated check signing can be prone to abuse. Further, the manual system is time and

resource wasting and unwieldy. The impacts of these weaknesses is exposing the company to

procurement risks, such as substandard products, non competitive pricing, and potential for

internal fraud. A proposed solution is the use of a computerized system to manage orders,

establish a competitive procurement process where all potential suppliers give offers and the

buyers’ sit as a team, evaluate the offers, and select suppliers after a unanimous agreement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING INFORMATION SYSTEM- PLATINUM CASE 4

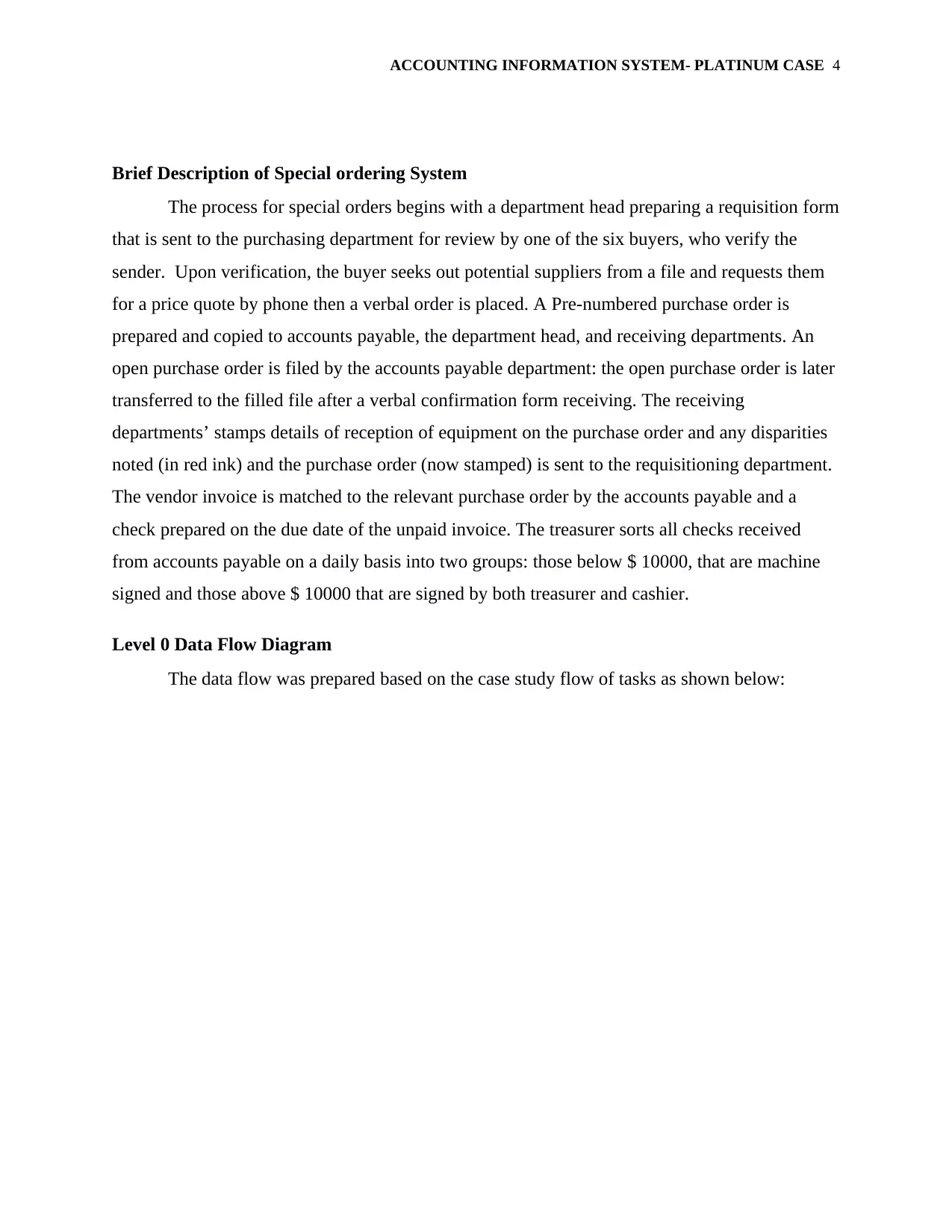

Brief Description of Special ordering System

The process for special orders begins with a department head preparing a requisition form

that is sent to the purchasing department for review by one of the six buyers, who verify the

sender. Upon verification, the buyer seeks out potential suppliers from a file and requests them

for a price quote by phone then a verbal order is placed. A Pre-numbered purchase order is

prepared and copied to accounts payable, the department head, and receiving departments. An

open purchase order is filed by the accounts payable department: the open purchase order is later

transferred to the filled file after a verbal confirmation form receiving. The receiving

departments’ stamps details of reception of equipment on the purchase order and any disparities

noted (in red ink) and the purchase order (now stamped) is sent to the requisitioning department.

The vendor invoice is matched to the relevant purchase order by the accounts payable and a

check prepared on the due date of the unpaid invoice. The treasurer sorts all checks received

from accounts payable on a daily basis into two groups: those below $ 10000, that are machine

signed and those above $ 10000 that are signed by both treasurer and cashier.

Level 0 Data Flow Diagram

The data flow was prepared based on the case study flow of tasks as shown below:

Brief Description of Special ordering System

The process for special orders begins with a department head preparing a requisition form

that is sent to the purchasing department for review by one of the six buyers, who verify the

sender. Upon verification, the buyer seeks out potential suppliers from a file and requests them

for a price quote by phone then a verbal order is placed. A Pre-numbered purchase order is

prepared and copied to accounts payable, the department head, and receiving departments. An

open purchase order is filed by the accounts payable department: the open purchase order is later

transferred to the filled file after a verbal confirmation form receiving. The receiving

departments’ stamps details of reception of equipment on the purchase order and any disparities

noted (in red ink) and the purchase order (now stamped) is sent to the requisitioning department.

The vendor invoice is matched to the relevant purchase order by the accounts payable and a

check prepared on the due date of the unpaid invoice. The treasurer sorts all checks received

from accounts payable on a daily basis into two groups: those below $ 10000, that are machine

signed and those above $ 10000 that are signed by both treasurer and cashier.

Level 0 Data Flow Diagram

The data flow was prepared based on the case study flow of tasks as shown below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING INFORMATION SYSTEM- PLATINUM CASE 5

Internal Control Weaknesses

One of the biggest weaknesses with the Platinum process for special orders purchase is

verbal (and telephone) methods of placing orders and making confirmations. The oral/ verbal

confirmations and order placement has an inherent weakness in that one of the parties may forget

the exact details of the product, resulting in either the wrong product/ equipment being purchased

or time and resources being wasted as a result. Further, apart from just forgetting the important

details about the order, the parties involved may disagree in the end if there are discrepancies on

order filling and the delivered product: the parties are likely to disagree on the exact details of

the orders and verbal confirmations. The other internal weakness is the buyer selecting

appropriate suppliers from a file, rather than selecting a few Pre-qualified suppliers and asking

them to send their quotations and then select the most competitive bid. This implies they may not

be getting value for money and there may be bias in selecting supplier, or even chicanery

between the buyer and some suppliers. Further, it is questionable that these requisitions are

Internal Control Weaknesses

One of the biggest weaknesses with the Platinum process for special orders purchase is

verbal (and telephone) methods of placing orders and making confirmations. The oral/ verbal

confirmations and order placement has an inherent weakness in that one of the parties may forget

the exact details of the product, resulting in either the wrong product/ equipment being purchased

or time and resources being wasted as a result. Further, apart from just forgetting the important

details about the order, the parties involved may disagree in the end if there are discrepancies on

order filling and the delivered product: the parties are likely to disagree on the exact details of

the orders and verbal confirmations. The other internal weakness is the buyer selecting

appropriate suppliers from a file, rather than selecting a few Pre-qualified suppliers and asking

them to send their quotations and then select the most competitive bid. This implies they may not

be getting value for money and there may be bias in selecting supplier, or even chicanery

between the buyer and some suppliers. Further, it is questionable that these requisitions are

ACCOUNTING INFORMATION SYSTEM- PLATINUM CASE 6

approved by the board beforehand, rather than on a case by case basis because this could be open

to abuse. The idea of automatic signing of checks is also a weakness that can be open to

exploitation or misuse, and would only be necessary where there are numerous purchase orders

Impacts of the Weaknesses on the Organization

The impacts include procurement risks: the weaknesses will expose the organization to

supply risks such as the wrong product being supplied. Further, the system does not provide a

watertight method for monitoring the activities of the purchasing department: the loopholes can

be exploited by malicious employees (Balm, Van Amstel, Habers, Aditjandra, & Zunder, 2016,

p. 254). The system creates inconsistency in how purchases and equipment’s are procured; this

is because there is no guiding quality principle, such as the requirement to get competitive

quotations from suppliers before making a purchasing decision (Rao, Radhakrishna, Mishra, &

Kata, 2016, p. 33). The system has serious inefficiencies, with much use of paper and manual

handling, as well as verbal order confirmation and document confirmation. The result will be

poor procurement experiences for all stakeholders (both internal and external) (Kuuse, 2016).

The current system creates knowledge gaps and eventually, some members will find their own

ways of accomplishing tasks; for instance, there is not clear policy on how suppliers are selected,

how orders and requisitions can be verified through detailed descriptions, or internal

verifications of documents and task completion. The weaknesses in Platinum special orders

procurement approach will create a misalignment between the organization and the equipment

suppliers (Ronson, 2013).

There will be no uniform experience for internal customers such as the different

department heads because the buyers do not collaborate and choose suppliers competitively or

based on a written policy. The result is the internal customers at the organization will not know

what to expect because of a lack of standardization in selecting suppliers. The reputation of

Platinum with suppliers can be damaged as a result of this misalignment (Koppelmann, 2011, p.

37). Proper and effective communication within the organization and with suppliers is crucial in

aligning procurement goals and creating positive relationships with suppliers and internal

customers. The present system does not enable effective measurement of procurement

performance, yet this is crucial in gauging the existing procurement policies. The present system

and its weaknesses and loopholes do not provide suitable metrics to use in measuring

approved by the board beforehand, rather than on a case by case basis because this could be open

to abuse. The idea of automatic signing of checks is also a weakness that can be open to

exploitation or misuse, and would only be necessary where there are numerous purchase orders

Impacts of the Weaknesses on the Organization

The impacts include procurement risks: the weaknesses will expose the organization to

supply risks such as the wrong product being supplied. Further, the system does not provide a

watertight method for monitoring the activities of the purchasing department: the loopholes can

be exploited by malicious employees (Balm, Van Amstel, Habers, Aditjandra, & Zunder, 2016,

p. 254). The system creates inconsistency in how purchases and equipment’s are procured; this

is because there is no guiding quality principle, such as the requirement to get competitive

quotations from suppliers before making a purchasing decision (Rao, Radhakrishna, Mishra, &

Kata, 2016, p. 33). The system has serious inefficiencies, with much use of paper and manual

handling, as well as verbal order confirmation and document confirmation. The result will be

poor procurement experiences for all stakeholders (both internal and external) (Kuuse, 2016).

The current system creates knowledge gaps and eventually, some members will find their own

ways of accomplishing tasks; for instance, there is not clear policy on how suppliers are selected,

how orders and requisitions can be verified through detailed descriptions, or internal

verifications of documents and task completion. The weaknesses in Platinum special orders

procurement approach will create a misalignment between the organization and the equipment

suppliers (Ronson, 2013).

There will be no uniform experience for internal customers such as the different

department heads because the buyers do not collaborate and choose suppliers competitively or

based on a written policy. The result is the internal customers at the organization will not know

what to expect because of a lack of standardization in selecting suppliers. The reputation of

Platinum with suppliers can be damaged as a result of this misalignment (Koppelmann, 2011, p.

37). Proper and effective communication within the organization and with suppliers is crucial in

aligning procurement goals and creating positive relationships with suppliers and internal

customers. The present system does not enable effective measurement of procurement

performance, yet this is crucial in gauging the existing procurement policies. The present system

and its weaknesses and loopholes do not provide suitable metrics to use in measuring

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING INFORMATION SYSTEM- PLATINUM CASE 7

procurement performance. When there are standard approaches, such as in selecting suppliers,

metrics can be generated easily and performance of procurement effectively measured (Thai,

2017, p. 7)

Measures to mitigate internal weaknesses in special orders at Platinum

The following measures should mitigate the risks posed by the internal procurement

weaknesses at the organization in the next few weeks and do not require significant investments

For starters, the orders should be placed in a documented manner, such as using PDF or

even word documents to generate purchase orders. Further, confirmation of orders and receipt of

goods delivery should be documented; for instance, all received goods and equipment should be

accompanied by a delivery note that Platinum duly signs and a copy attached to the purchase

order and filed, after inspection of the equipment (Smith, 2013, p. 55)

To get value for money, the process of selecting suppliers should be made competitive

and standardized, so that a number of suppliers are requested to submit quotations and only the

most competitive bids and terms given selected to supply equipment (Muckle, 2015)

A machine should not be used to sign checks; the equipment requisitions under special

orders cannot be so many that the cashier and treasurer cannot sign, otherwise, it points to a poor

and flawed procurement strategy where there are many special orders for equipment (Booth,

2010, p.16).

The buyers should work as a team and jointly evaluate requisitions, vet suppliers, and

jointly choose the preferred supplier.

Modifications to the recommendations

The recommendations can be modified an enhanced even further if ICT is brought into

the equation. For starters, the organization can re-engineer its procurement processes so that

department heads raise orders through a unified application portal; for instance the company can

make use of free or low cost SCM (supply chain management) software that have online/ cloud

functionality to streamline procurement processes (Day, 2014). When a department head wants

equipment, they log into the system using provided credentials and place the order. The buyers

automatically get the requisition and can confirm if the sender is a department head quickly

procurement performance. When there are standard approaches, such as in selecting suppliers,

metrics can be generated easily and performance of procurement effectively measured (Thai,

2017, p. 7)

Measures to mitigate internal weaknesses in special orders at Platinum

The following measures should mitigate the risks posed by the internal procurement

weaknesses at the organization in the next few weeks and do not require significant investments

For starters, the orders should be placed in a documented manner, such as using PDF or

even word documents to generate purchase orders. Further, confirmation of orders and receipt of

goods delivery should be documented; for instance, all received goods and equipment should be

accompanied by a delivery note that Platinum duly signs and a copy attached to the purchase

order and filed, after inspection of the equipment (Smith, 2013, p. 55)

To get value for money, the process of selecting suppliers should be made competitive

and standardized, so that a number of suppliers are requested to submit quotations and only the

most competitive bids and terms given selected to supply equipment (Muckle, 2015)

A machine should not be used to sign checks; the equipment requisitions under special

orders cannot be so many that the cashier and treasurer cannot sign, otherwise, it points to a poor

and flawed procurement strategy where there are many special orders for equipment (Booth,

2010, p.16).

The buyers should work as a team and jointly evaluate requisitions, vet suppliers, and

jointly choose the preferred supplier.

Modifications to the recommendations

The recommendations can be modified an enhanced even further if ICT is brought into

the equation. For starters, the organization can re-engineer its procurement processes so that

department heads raise orders through a unified application portal; for instance the company can

make use of free or low cost SCM (supply chain management) software that have online/ cloud

functionality to streamline procurement processes (Day, 2014). When a department head wants

equipment, they log into the system using provided credentials and place the order. The buyers

automatically get the requisition and can confirm if the sender is a department head quickly

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING INFORMATION SYSTEM- PLATINUM CASE 8

(through the verified password). Next, the buyers check their database for shortlisted suppliers or

alternatively, send out a supply tender or an e-mail to possible suppliers to submit quotations.

The system is configured to undertake preliminary review of price quotes and then buyer team

can then evaluate the shortlisted quotations and make a structured decision on who give the

supply order. The supplier, once shortlisted, then sends a Pro-forma invoice against which a

purchase order is raised, through the system. When the equipment is delivered, a bar scanner is

used to assign it a unique code and accept the equipment into the organization. The equipment is

accompanied by a delivery note that must be signed and then entered into the system to confirm

receipt; the bar scanner automatically enters the received item into the organization assets

management system. A check is then issued against the invoice attached to the delivery note and

updated on the system.

The system needs to be a complete ERP with links to financial systems in the

organization. The system should use electronic forms to replace paper forms as much as possible

(Reaume, 2010). The system will have automation and inbuilt control policies that ensure that

only authorized people can make some changes or requisitions. The system should also have a

strong access and credential management system to ensure only authorized persons can access

the system and make changes. The automated system should then have a cloud application, such

that all transactions are stored in a hybrid cloud to ensure redundancy and business process

continuity in the event that there is downtime with the private cloud/ physical servers where the

firm runs its operations. With a cloud instance, the system will remain fully updated and ensure

there is no downtime or interruptions. The system also has the benefit that actions and processes

can be tracked so that if there is a problem, it is easy to track it to the source. Such a system will

also offset some of the impacts of the internal weaknesses in the current system (Walker, 2008,

p. 246)

(through the verified password). Next, the buyers check their database for shortlisted suppliers or

alternatively, send out a supply tender or an e-mail to possible suppliers to submit quotations.

The system is configured to undertake preliminary review of price quotes and then buyer team

can then evaluate the shortlisted quotations and make a structured decision on who give the

supply order. The supplier, once shortlisted, then sends a Pro-forma invoice against which a

purchase order is raised, through the system. When the equipment is delivered, a bar scanner is

used to assign it a unique code and accept the equipment into the organization. The equipment is

accompanied by a delivery note that must be signed and then entered into the system to confirm

receipt; the bar scanner automatically enters the received item into the organization assets

management system. A check is then issued against the invoice attached to the delivery note and

updated on the system.

The system needs to be a complete ERP with links to financial systems in the

organization. The system should use electronic forms to replace paper forms as much as possible

(Reaume, 2010). The system will have automation and inbuilt control policies that ensure that

only authorized people can make some changes or requisitions. The system should also have a

strong access and credential management system to ensure only authorized persons can access

the system and make changes. The automated system should then have a cloud application, such

that all transactions are stored in a hybrid cloud to ensure redundancy and business process

continuity in the event that there is downtime with the private cloud/ physical servers where the

firm runs its operations. With a cloud instance, the system will remain fully updated and ensure

there is no downtime or interruptions. The system also has the benefit that actions and processes

can be tracked so that if there is a problem, it is easy to track it to the source. Such a system will

also offset some of the impacts of the internal weaknesses in the current system (Walker, 2008,

p. 246)

ACCOUNTING INFORMATION SYSTEM- PLATINUM CASE 9

References

Balm, S., Van Amstel, W., Habers, J., Aditjandra, P., & Zunder, T. H. (2016). The

purchasing behavior of public organizations and its impact on city logistics. In The

9th International Conference on City Logistics (p. 254). Retrieved from

https://www.sciencedirect.com/science/article/pii/S2352146516000648/pdf?

md5=0840882efba6a226dceeabcb31aad17a&pid=1-s2.0-S2352146516000648-

main.pdf&_valck=1

Booth, C. (2010). Strategic procurement: Organizing suppliers and supply chains for

competitive advantage (1st ed.). London: Kogan Page.

Day, A. (2014, May 29). 10 ways the procurement profession can improve. Retrieved from

https://www.cips.org/supply-management/opinion/2014/may/10-ways-the-

procurement-profession-can-improve/

Koppelmann, U. (2011). Procurement marketing: A strategic concept. Berlin: Springer.

Kuuse, A. (2016). 5 Consequences of Not Adhering to the Procurement Management Plan.

Retrieved from http://blog.deltabid.com/5-consequences-of-not-adhering-to-the-

procurement-management-plan

Muckle, K. (2015, December 21). Why Tender? The Benefits of Running a Competitive Tender

to Procure Services. Retrieved from https://www.linkedin.com/pulse/why-tender-

benefits-running-competitive-procure-services-muckle

Rao, N. C., Radhakrishna, R., Mishra, R. K., & Kata, V. R. (2016). Organised Retailing and

Agri-Business: Implications of New Supply Chains on the Indian Farm Economy

(2nd ed.). Delhi: Springer.

References

Balm, S., Van Amstel, W., Habers, J., Aditjandra, P., & Zunder, T. H. (2016). The

purchasing behavior of public organizations and its impact on city logistics. In The

9th International Conference on City Logistics (p. 254). Retrieved from

https://www.sciencedirect.com/science/article/pii/S2352146516000648/pdf?

md5=0840882efba6a226dceeabcb31aad17a&pid=1-s2.0-S2352146516000648-

main.pdf&_valck=1

Booth, C. (2010). Strategic procurement: Organizing suppliers and supply chains for

competitive advantage (1st ed.). London: Kogan Page.

Day, A. (2014, May 29). 10 ways the procurement profession can improve. Retrieved from

https://www.cips.org/supply-management/opinion/2014/may/10-ways-the-

procurement-profession-can-improve/

Koppelmann, U. (2011). Procurement marketing: A strategic concept. Berlin: Springer.

Kuuse, A. (2016). 5 Consequences of Not Adhering to the Procurement Management Plan.

Retrieved from http://blog.deltabid.com/5-consequences-of-not-adhering-to-the-

procurement-management-plan

Muckle, K. (2015, December 21). Why Tender? The Benefits of Running a Competitive Tender

to Procure Services. Retrieved from https://www.linkedin.com/pulse/why-tender-

benefits-running-competitive-procure-services-muckle

Rao, N. C., Radhakrishna, R., Mishra, R. K., & Kata, V. R. (2016). Organised Retailing and

Agri-Business: Implications of New Supply Chains on the Indian Farm Economy

(2nd ed.). Delhi: Springer.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING INFORMATION SYSTEM- PLATINUM CASE 10

Reaume, J. (2010, March 1). 6 Procurement Actions that Can Boost Your Business.

Retrieved from

http://www.scmr.com/article/6_procurement_actions_that_can_boost_your_business

Ronson, S. (2013, February). The impact of poor procurement decisions | FM Magazine.

Retrieved from https://www.fmmagazine.com.au/sectors/the-impact-of-poor-

procurement-decisions/

Smith,K.I. (2013). The PMP Notebook: A Study Companion to the PMP exam (2nd ed.).

London: Springer.

Thai, K. V. (2017). International Handbook of Public Procurement (1st ed.). london: CRC

Press.

Walker, D. (2008). Procurement Strategies [electronic resource] : A Relationship-based

Approach (3rd ed.). Oxford: Blackwell Science.

Reaume, J. (2010, March 1). 6 Procurement Actions that Can Boost Your Business.

Retrieved from

http://www.scmr.com/article/6_procurement_actions_that_can_boost_your_business

Ronson, S. (2013, February). The impact of poor procurement decisions | FM Magazine.

Retrieved from https://www.fmmagazine.com.au/sectors/the-impact-of-poor-

procurement-decisions/

Smith,K.I. (2013). The PMP Notebook: A Study Companion to the PMP exam (2nd ed.).

London: Springer.

Thai, K. V. (2017). International Handbook of Public Procurement (1st ed.). london: CRC

Press.

Walker, D. (2008). Procurement Strategies [electronic resource] : A Relationship-based

Approach (3rd ed.). Oxford: Blackwell Science.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.