Report on Internal Control Weaknesses in Platinum's Purchase Process

VerifiedAdded on 2021/06/15

|11

|2307

|100

Report

AI Summary

This report analyzes the internal control weaknesses within Platinum's special orders purchase process. The report identifies three primary weaknesses: communication issues due to reliance on verbal exchanges, inequitable distribution of duties, particularly in the treasurer department, and excessive effort expended by various departments due to repetitive verification steps. These weaknesses are associated with potential fraud, auditing challenges, and legal risks. The report recommends adopting an accounting information system to automate processes and mitigate communication problems through electronic documentation, restructuring duties for better distribution, and streamlining verification procedures. A level 0 data flow diagram illustrates the purchase process. The report also assesses the compatibility of these recommendations with the reengineering of Platinum’s IT structure, suggesting that electronic solutions are easily integrated while traditional methods require data conversion.

Running head: INTERNAL CONTROL WEAKNESS OF PLATINUM PURCHASE

PROCESS

INTERNAL CONTROL WEAKNESS OF PLATINUM PURCHASE PROCESS

Name of the Student

Name of the University

Author note

PROCESS

INTERNAL CONTROL WEAKNESS OF PLATINUM PURCHASE PROCESS

Name of the Student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1INTERNAL CONTROL WEAKNESS OF PLATINUM PURCHASE PROCESS

EXECUTIVE SUMMARY

The report had discussed the internal control weakness of Platinum and identified that the

weaknesses are associated with its communication process, inequivalent distribution of duties

and extra effort by the organisation. To avoid the weaknesses, the accounting information

system had been recommended or they can do it by traditional means. In traditional means

adopting of electronic form or enforcing written communication are recommended to

mitigate communicational weakness while restructuring of duties and department for the

other two identified weaknesses. A level 0 data flow diagram has also been attached for better

understanding of the organisations’ purchase process. The impact of the weaknesses has also

been discussed in the report and even measured the compatibility between the recommended

measures and the reengineering of Platinum’s IT structure if they decide to adopt disruptive

technology.

EXECUTIVE SUMMARY

The report had discussed the internal control weakness of Platinum and identified that the

weaknesses are associated with its communication process, inequivalent distribution of duties

and extra effort by the organisation. To avoid the weaknesses, the accounting information

system had been recommended or they can do it by traditional means. In traditional means

adopting of electronic form or enforcing written communication are recommended to

mitigate communicational weakness while restructuring of duties and department for the

other two identified weaknesses. A level 0 data flow diagram has also been attached for better

understanding of the organisations’ purchase process. The impact of the weaknesses has also

been discussed in the report and even measured the compatibility between the recommended

measures and the reengineering of Platinum’s IT structure if they decide to adopt disruptive

technology.

2INTERNAL CONTROL WEAKNESS OF PLATINUM PURCHASE PROCESS

Contents

Purchase Process of Special Orders in Platinum........................................................................3

Level 0 Data Flow Diagram.......................................................................................................4

Table of Identification and Assessment.....................................................................................4

Identification of Internal Control Weakness in Platinum.....................................................5

Impact of Internal Control Weakness....................................................................................5

Recommendation to mitigate the Internal Control Weaknesses............................................5

Measuring the compatibility of recommended measures with reengineering of Platinum’s

IT structure.............................................................................................................................5

Bibliography:..............................................................................................................................9

Contents

Purchase Process of Special Orders in Platinum........................................................................3

Level 0 Data Flow Diagram.......................................................................................................4

Table of Identification and Assessment.....................................................................................4

Identification of Internal Control Weakness in Platinum.....................................................5

Impact of Internal Control Weakness....................................................................................5

Recommendation to mitigate the Internal Control Weaknesses............................................5

Measuring the compatibility of recommended measures with reengineering of Platinum’s

IT structure.............................................................................................................................5

Bibliography:..............................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3INTERNAL CONTROL WEAKNESS OF PLATINUM PURCHASE PROCESS

Purchase Process of Special Orders in Platinum

Platinum manufacturing group has a department based purchase process where

different department plays the prominent role to complete a process. The first role is of the

purchase department which have five buyers who on receiving purchase requisition from the

head justifies the requisition validity within the department. Then, one of the five buyers

takes the initiative and proceeds with the buying process where he/she selects a suitable

vendor for the purchase and demands a price quotation from them while placing a verbal

order. Then the selected buyer forms a pre-numbered purchase order and forward it to

different department along with the head to proceed with the task in hand. The receiving

department on receiving the pre-numbered purchase order and the ordered item from the

vendor starts their role in which they compare the received item and the ordered item. If the

received item is suitable as per the ordered item, then they stamp the purchase order and

forward it to the accounts payable while in the other scenario they mark the purchase order

with red ink. After receiving the stamped purchase order from the receiving department, the

accounts department comes to pay their role where they justify the similarity of the vendor’s

invoice and the purchase order. On verification of the similarity between the purchase order

and the vendor’s invoice, the accounts department formulates a check and sends it to the

treasurer completing its role in the purchase procedure. The next part is played by the

treasures department where the cashier on receiving the checks the amount to be paid which;

if under $10,000 then the machine signs the check and over $10,000 is signed by the machine

as well as the cashier completing the purchase procedure.

Purchase Process of Special Orders in Platinum

Platinum manufacturing group has a department based purchase process where

different department plays the prominent role to complete a process. The first role is of the

purchase department which have five buyers who on receiving purchase requisition from the

head justifies the requisition validity within the department. Then, one of the five buyers

takes the initiative and proceeds with the buying process where he/she selects a suitable

vendor for the purchase and demands a price quotation from them while placing a verbal

order. Then the selected buyer forms a pre-numbered purchase order and forward it to

different department along with the head to proceed with the task in hand. The receiving

department on receiving the pre-numbered purchase order and the ordered item from the

vendor starts their role in which they compare the received item and the ordered item. If the

received item is suitable as per the ordered item, then they stamp the purchase order and

forward it to the accounts payable while in the other scenario they mark the purchase order

with red ink. After receiving the stamped purchase order from the receiving department, the

accounts department comes to pay their role where they justify the similarity of the vendor’s

invoice and the purchase order. On verification of the similarity between the purchase order

and the vendor’s invoice, the accounts department formulates a check and sends it to the

treasurer completing its role in the purchase procedure. The next part is played by the

treasures department where the cashier on receiving the checks the amount to be paid which;

if under $10,000 then the machine signs the check and over $10,000 is signed by the machine

as well as the cashier completing the purchase procedure.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4INTERNAL CONTROL WEAKNESS OF PLATINUM PURCHASE PROCESS

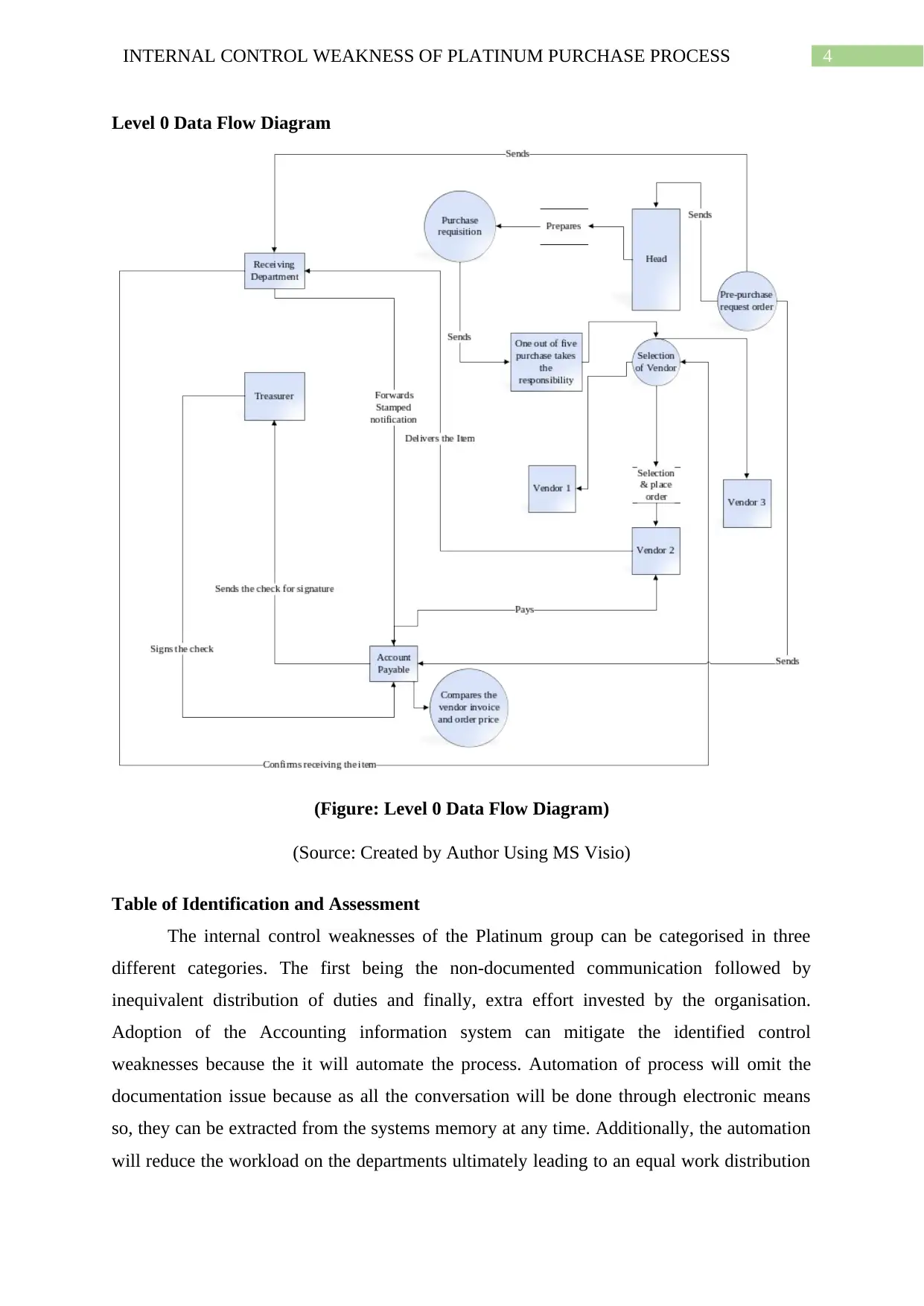

Level 0 Data Flow Diagram

(Figure: Level 0 Data Flow Diagram)

(Source: Created by Author Using MS Visio)

Table of Identification and Assessment

The internal control weaknesses of the Platinum group can be categorised in three

different categories. The first being the non-documented communication followed by

inequivalent distribution of duties and finally, extra effort invested by the organisation.

Adoption of the Accounting information system can mitigate the identified control

weaknesses because the it will automate the process. Automation of process will omit the

documentation issue because as all the conversation will be done through electronic means

so, they can be extracted from the systems memory at any time. Additionally, the automation

will reduce the workload on the departments ultimately leading to an equal work distribution

Level 0 Data Flow Diagram

(Figure: Level 0 Data Flow Diagram)

(Source: Created by Author Using MS Visio)

Table of Identification and Assessment

The internal control weaknesses of the Platinum group can be categorised in three

different categories. The first being the non-documented communication followed by

inequivalent distribution of duties and finally, extra effort invested by the organisation.

Adoption of the Accounting information system can mitigate the identified control

weaknesses because the it will automate the process. Automation of process will omit the

documentation issue because as all the conversation will be done through electronic means

so, they can be extracted from the systems memory at any time. Additionally, the automation

will reduce the workload on the departments ultimately leading to an equal work distribution

5INTERNAL CONTROL WEAKNESS OF PLATINUM PURCHASE PROCESS

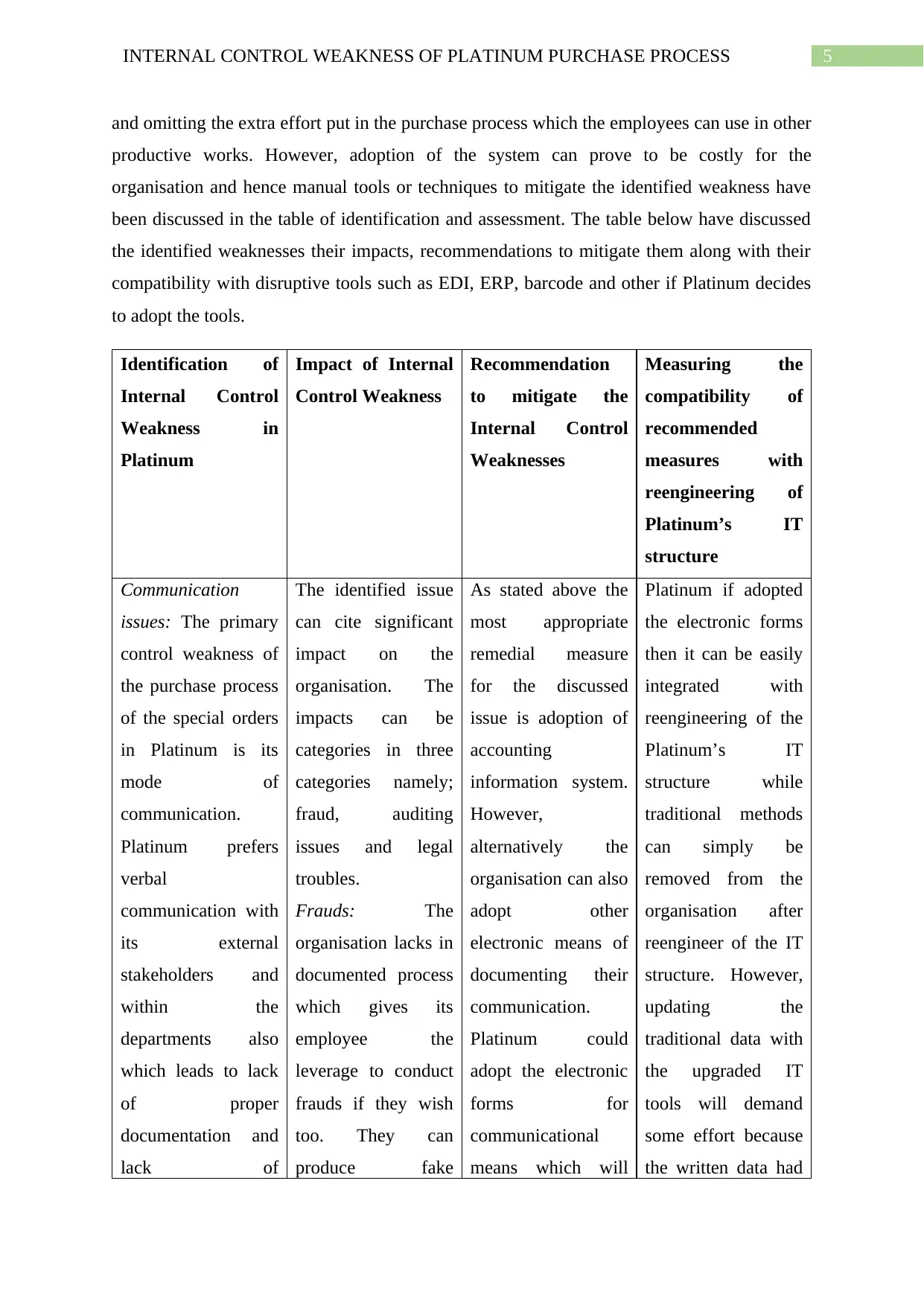

and omitting the extra effort put in the purchase process which the employees can use in other

productive works. However, adoption of the system can prove to be costly for the

organisation and hence manual tools or techniques to mitigate the identified weakness have

been discussed in the table of identification and assessment. The table below have discussed

the identified weaknesses their impacts, recommendations to mitigate them along with their

compatibility with disruptive tools such as EDI, ERP, barcode and other if Platinum decides

to adopt the tools.

Identification of

Internal Control

Weakness in

Platinum

Impact of Internal

Control Weakness

Recommendation

to mitigate the

Internal Control

Weaknesses

Measuring the

compatibility of

recommended

measures with

reengineering of

Platinum’s IT

structure

Communication

issues: The primary

control weakness of

the purchase process

of the special orders

in Platinum is its

mode of

communication.

Platinum prefers

verbal

communication with

its external

stakeholders and

within the

departments also

which leads to lack

of proper

documentation and

lack of

The identified issue

can cite significant

impact on the

organisation. The

impacts can be

categories in three

categories namely;

fraud, auditing

issues and legal

troubles.

Frauds: The

organisation lacks in

documented process

which gives its

employee the

leverage to conduct

frauds if they wish

too. They can

produce fake

As stated above the

most appropriate

remedial measure

for the discussed

issue is adoption of

accounting

information system.

However,

alternatively the

organisation can also

adopt other

electronic means of

documenting their

communication.

Platinum could

adopt the electronic

forms for

communicational

means which will

Platinum if adopted

the electronic forms

then it can be easily

integrated with

reengineering of the

Platinum’s IT

structure while

traditional methods

can simply be

removed from the

organisation after

reengineer of the IT

structure. However,

updating the

traditional data with

the upgraded IT

tools will demand

some effort because

the written data had

and omitting the extra effort put in the purchase process which the employees can use in other

productive works. However, adoption of the system can prove to be costly for the

organisation and hence manual tools or techniques to mitigate the identified weakness have

been discussed in the table of identification and assessment. The table below have discussed

the identified weaknesses their impacts, recommendations to mitigate them along with their

compatibility with disruptive tools such as EDI, ERP, barcode and other if Platinum decides

to adopt the tools.

Identification of

Internal Control

Weakness in

Platinum

Impact of Internal

Control Weakness

Recommendation

to mitigate the

Internal Control

Weaknesses

Measuring the

compatibility of

recommended

measures with

reengineering of

Platinum’s IT

structure

Communication

issues: The primary

control weakness of

the purchase process

of the special orders

in Platinum is its

mode of

communication.

Platinum prefers

verbal

communication with

its external

stakeholders and

within the

departments also

which leads to lack

of proper

documentation and

lack of

The identified issue

can cite significant

impact on the

organisation. The

impacts can be

categories in three

categories namely;

fraud, auditing

issues and legal

troubles.

Frauds: The

organisation lacks in

documented process

which gives its

employee the

leverage to conduct

frauds if they wish

too. They can

produce fake

As stated above the

most appropriate

remedial measure

for the discussed

issue is adoption of

accounting

information system.

However,

alternatively the

organisation can also

adopt other

electronic means of

documenting their

communication.

Platinum could

adopt the electronic

forms for

communicational

means which will

Platinum if adopted

the electronic forms

then it can be easily

integrated with

reengineering of the

Platinum’s IT

structure while

traditional methods

can simply be

removed from the

organisation after

reengineer of the IT

structure. However,

updating the

traditional data with

the upgraded IT

tools will demand

some effort because

the written data had

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6INTERNAL CONTROL WEAKNESS OF PLATINUM PURCHASE PROCESS

documentation is

one of the most

prominent challenge

for any organisation

because information

are the most vital

factor for an

organisations

sustainability.

quotations or can

even back down

from their words as

the organisation

lacks any solid

documented

evidence of the

communication.

Auditing issues: Due

to lack of

documentation the

organisation may

face trouble in the

auditing process

which in turn will

develop challenges

for the strategy

development of

Platinum’s financial

resources.

Legal trouble:

Platinum’s lack of

proper

documentation may

lay them in legal

trouble because they

cannot prove

evidence of their

purchase and the

claims of tax

avoidance, illegal

import & export or

other similar

charges.

ensure that the

communication is

documented

additionally, e-mails,

and official chatting

tools can also offer

their services to the

organisational

communication.

Another method that

the organisation

could adopt to omit

the organisational

communication issue

is adoption of

traditional means

where all the

conversations both

internally and

externally are done

through paperwork

in form of notice,

memos, quotations

and other. However,

this method will

consume a lot of

organisational

resources and also

can be ignored by

the employees and

hence, more focus

should be given to

enforcement of the

paper

to be converted to

the digital data to

integrate them with

the system.

documentation is

one of the most

prominent challenge

for any organisation

because information

are the most vital

factor for an

organisations

sustainability.

quotations or can

even back down

from their words as

the organisation

lacks any solid

documented

evidence of the

communication.

Auditing issues: Due

to lack of

documentation the

organisation may

face trouble in the

auditing process

which in turn will

develop challenges

for the strategy

development of

Platinum’s financial

resources.

Legal trouble:

Platinum’s lack of

proper

documentation may

lay them in legal

trouble because they

cannot prove

evidence of their

purchase and the

claims of tax

avoidance, illegal

import & export or

other similar

charges.

ensure that the

communication is

documented

additionally, e-mails,

and official chatting

tools can also offer

their services to the

organisational

communication.

Another method that

the organisation

could adopt to omit

the organisational

communication issue

is adoption of

traditional means

where all the

conversations both

internally and

externally are done

through paperwork

in form of notice,

memos, quotations

and other. However,

this method will

consume a lot of

organisational

resources and also

can be ignored by

the employees and

hence, more focus

should be given to

enforcement of the

paper

to be converted to

the digital data to

integrate them with

the system.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INTERNAL CONTROL WEAKNESS OF PLATINUM PURCHASE PROCESS

communication

rather than its

implementation .

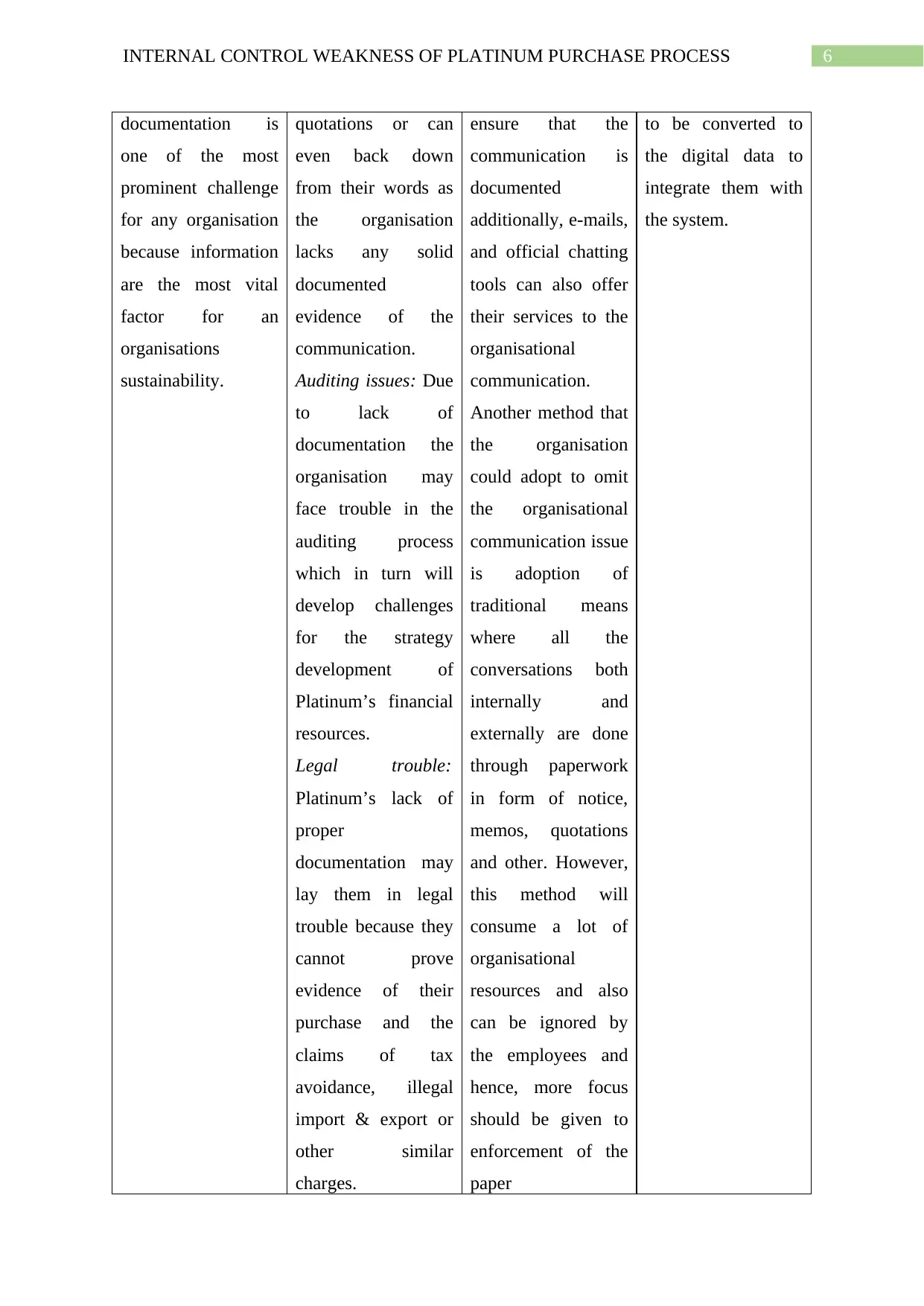

Distribution of

duties: The

distribution of duties

in the Platinum are

inequivalent as is

evident from the

treasurer department

where all the checks

are signed by the

cashier who suffers

from extra work

load and also gives

him/her the

opportunity to fraud.

The inequivalent of

duties can cite some

significant impact on

the organisation,

especially, its

employee. The

cashier is shouldered

with the

responsibility to sign

over all the checks

which over

shoulders him/her

with responsibility

which may lead to

exhaustion of the

cashier and

ultimately lead to

decrease in their

productivity.

Additionally, it is

concerning for

Platinum because

over reliability on

the cashier may

provide them with

the leverage to fraud

in the organisation

which will sure

affect the

organisation

The

recommendation for

the discussed

weakness is to

ensure equal

distribution of

duties. To attain the

desired result

organisation should

create three domains

where the lowest

budget domain that

is below $10,000

should be machine

signed, thee second

domain should be

signed by the

machine & cashier

and the highest

domain by machine

& treasurer. It will

reduce the work load

and also restrict the

powers of cashier

that will mitigate the

risk of frauds.

The duties

distribution will also

be compatible with

the reengineering of

the IT structure

because the

proposed

recommendation

considers human

involvement which

can easily be trained

in IT.

communication

rather than its

implementation .

Distribution of

duties: The

distribution of duties

in the Platinum are

inequivalent as is

evident from the

treasurer department

where all the checks

are signed by the

cashier who suffers

from extra work

load and also gives

him/her the

opportunity to fraud.

The inequivalent of

duties can cite some

significant impact on

the organisation,

especially, its

employee. The

cashier is shouldered

with the

responsibility to sign

over all the checks

which over

shoulders him/her

with responsibility

which may lead to

exhaustion of the

cashier and

ultimately lead to

decrease in their

productivity.

Additionally, it is

concerning for

Platinum because

over reliability on

the cashier may

provide them with

the leverage to fraud

in the organisation

which will sure

affect the

organisation

The

recommendation for

the discussed

weakness is to

ensure equal

distribution of

duties. To attain the

desired result

organisation should

create three domains

where the lowest

budget domain that

is below $10,000

should be machine

signed, thee second

domain should be

signed by the

machine & cashier

and the highest

domain by machine

& treasurer. It will

reduce the work load

and also restrict the

powers of cashier

that will mitigate the

risk of frauds.

The duties

distribution will also

be compatible with

the reengineering of

the IT structure

because the

proposed

recommendation

considers human

involvement which

can easily be trained

in IT.

8INTERNAL CONTROL WEAKNESS OF PLATINUM PURCHASE PROCESS

adversely.

Extra effort by

departments: The

purchase process

within the depart

undergoes repetitive

process where the

repetition of the

verification is done

over and over which

consumes the

organisational

resources which

could be used to

increase the

productivity of the

organisation.

Another notable

internal control

weakness of the

organisation is extra

effort of the

organisation which

is evident from the

re-verification

process of the

purchase order and

its associates. Its

impact is

challenging for the

organisation because

it increases the

resources of the

organisation. The

time, effort, human

and other stationery

resources could be

better utilised to

increase the

productivity of the

organisation.

The organisation

must restructure its

purchase process to

by formulating a

team that will verify

each aspects from

purchase order to

vendor’s invoice and

the received item to

reduce the effort

invested by different

departments in the

discussed process

which will save the

time, effort and

organisational

resources.

The formulated team

can also be

integrated with the

barcode system,

EDI, ERP and others

because they will

have to collect the

data directly from

the adopted tools

and which will

simplify their

problems and hence

can be considered as

a suitable measure.

TABLE: TABLE OF Identification and Assessment

(Source: Created by Author)

adversely.

Extra effort by

departments: The

purchase process

within the depart

undergoes repetitive

process where the

repetition of the

verification is done

over and over which

consumes the

organisational

resources which

could be used to

increase the

productivity of the

organisation.

Another notable

internal control

weakness of the

organisation is extra

effort of the

organisation which

is evident from the

re-verification

process of the

purchase order and

its associates. Its

impact is

challenging for the

organisation because

it increases the

resources of the

organisation. The

time, effort, human

and other stationery

resources could be

better utilised to

increase the

productivity of the

organisation.

The organisation

must restructure its

purchase process to

by formulating a

team that will verify

each aspects from

purchase order to

vendor’s invoice and

the received item to

reduce the effort

invested by different

departments in the

discussed process

which will save the

time, effort and

organisational

resources.

The formulated team

can also be

integrated with the

barcode system,

EDI, ERP and others

because they will

have to collect the

data directly from

the adopted tools

and which will

simplify their

problems and hence

can be considered as

a suitable measure.

TABLE: TABLE OF Identification and Assessment

(Source: Created by Author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9INTERNAL CONTROL WEAKNESS OF PLATINUM PURCHASE PROCESS

Bibliography:

Anandarajan, M., Simmers, C. A., & Teo, T. S. (2014). The Internet and workplace

transformation: An introduction. In The internet and workplace transformation (pp.

13-22). Routledge.

Brewster, C., Hegewisch, A., Mayne, L., & Tregaskis, O. (2017). Employee communication

and participation. Policy and Practice in European Human Resource Management:

The Price Waterhouse Cranfield Survey, 154.

Chang, S. I., Yen, D. C., Chang, I. C., & Jan, D. (2014). Internal control framework for a

compliant ERP system. Information & Management, 51(2), 187-205.

Chaturvedi, S., & Chakrabarti, D. (2015). Internal purchase process: a study for setting

improvement target. International Journal of Procurement Management, 8(6), 753-

768.

DeFond, M. L., & Lennox, C. S. (2017). Do PCAOB inspections improve the quality of

internal control audits?. Journal of Accounting Research, 55(3), 591-627.

Feng, M., Li, C., McVay, S. E., & Skaife, H. (2014). Does ineffective internal control over

financial reporting affect a firm's operations? Evidence from firms' inventory

management. The Accounting Review, 90(2), 529-557.

Gallemore, J., & Labro, E. (2015). The importance of the internal information environment

for tax avoidance. Journal of Accounting and Economics, 60(1), 149-167.

Ge, W., Koester, A., & McVay, S. (2017). Benefits and costs of Sarbanes-Oxley Section 404

(b) exemption: Evidence from small firms’ internal control disclosures. Journal of

Accounting and Economics, 63(2-3), 358-384.

Gunduz, M., & Önder, O. (2013). Corruption and internal fraud in the Turkish construction

industry. Science and engineering ethics, 19(2), 505-528.

Hassan, H., Nasir, M. H. M., & Khairudin, N. (2017). Accounting Information Systems.

In SHS Web of Conferences (Vol. 34). EDP Sciences.

Ismail, N. A., & King, M. (2014). Factors influencing the alignment of accounting

information systems in small and medium sized Malaysian manufacturing

firms. Journal of Information Systems and Small Business, 1(1-2), 1-20.

Bibliography:

Anandarajan, M., Simmers, C. A., & Teo, T. S. (2014). The Internet and workplace

transformation: An introduction. In The internet and workplace transformation (pp.

13-22). Routledge.

Brewster, C., Hegewisch, A., Mayne, L., & Tregaskis, O. (2017). Employee communication

and participation. Policy and Practice in European Human Resource Management:

The Price Waterhouse Cranfield Survey, 154.

Chang, S. I., Yen, D. C., Chang, I. C., & Jan, D. (2014). Internal control framework for a

compliant ERP system. Information & Management, 51(2), 187-205.

Chaturvedi, S., & Chakrabarti, D. (2015). Internal purchase process: a study for setting

improvement target. International Journal of Procurement Management, 8(6), 753-

768.

DeFond, M. L., & Lennox, C. S. (2017). Do PCAOB inspections improve the quality of

internal control audits?. Journal of Accounting Research, 55(3), 591-627.

Feng, M., Li, C., McVay, S. E., & Skaife, H. (2014). Does ineffective internal control over

financial reporting affect a firm's operations? Evidence from firms' inventory

management. The Accounting Review, 90(2), 529-557.

Gallemore, J., & Labro, E. (2015). The importance of the internal information environment

for tax avoidance. Journal of Accounting and Economics, 60(1), 149-167.

Ge, W., Koester, A., & McVay, S. (2017). Benefits and costs of Sarbanes-Oxley Section 404

(b) exemption: Evidence from small firms’ internal control disclosures. Journal of

Accounting and Economics, 63(2-3), 358-384.

Gunduz, M., & Önder, O. (2013). Corruption and internal fraud in the Turkish construction

industry. Science and engineering ethics, 19(2), 505-528.

Hassan, H., Nasir, M. H. M., & Khairudin, N. (2017). Accounting Information Systems.

In SHS Web of Conferences (Vol. 34). EDP Sciences.

Ismail, N. A., & King, M. (2014). Factors influencing the alignment of accounting

information systems in small and medium sized Malaysian manufacturing

firms. Journal of Information Systems and Small Business, 1(1-2), 1-20.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10INTERNAL CONTROL WEAKNESS OF PLATINUM PURCHASE PROCESS

Ifenthaler, D. (2018). How we learn at the digital workplace. In Digital Workplace

Learning (pp. 3-8). Springer, Cham.

Khairi, M. S., & Baridwan, Z. (2015). An empirical study on organizational acceptance

accounting information systems in Sharia banking. The International Journal of

Accounting and Business Society, 23(1), 97-122.

Walther, J. B., Van Der Heide, B., Ramirez, A., Burgoon, J. K., & Peña, J. (2015).

Interpersonal and Hyperpersonal Dimensions of Computer‐Mediated

Communication. The handbook of the psychology of communication technology, 1-22.

Ifenthaler, D. (2018). How we learn at the digital workplace. In Digital Workplace

Learning (pp. 3-8). Springer, Cham.

Khairi, M. S., & Baridwan, Z. (2015). An empirical study on organizational acceptance

accounting information systems in Sharia banking. The International Journal of

Accounting and Business Society, 23(1), 97-122.

Walther, J. B., Van Der Heide, B., Ramirez, A., Burgoon, J. K., & Peña, J. (2015).

Interpersonal and Hyperpersonal Dimensions of Computer‐Mediated

Communication. The handbook of the psychology of communication technology, 1-22.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.