Financial Analysis and Decision Making Report: Playdough Company

VerifiedAdded on 2020/03/01

|10

|2745

|80

Report

AI Summary

This report provides a comprehensive financial analysis of Playdough Company, focusing on critical decision-making processes. It evaluates the costs and benefits associated with the make-or-buy decision for canisters, comparing traditional and activity-based costing approaches to determine the optimal production strategy. The report also examines the implications of a special offer to sell the company's product at a lower price, utilizing break-even and incremental cost analyses to assess profitability. Furthermore, it explores the potential of adding a new product line, specifically coffee cups, by calculating profit margins and considering the allocation of fixed overhead costs. The analysis incorporates relevant costs, including direct materials, labor, and overhead, to provide a detailed assessment of each decision's financial impact, ultimately guiding the company toward the most financially sound choices.

Playdoug Company 1

Playdough Company Report

Student’s Name

Name of Course

Professor’s Name

Name of the University

City and State

Date

Playdough Company Report

Student’s Name

Name of Course

Professor’s Name

Name of the University

City and State

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Playdoug Company 2

Executive Summary

This report focuses on the decision making process at Playdough Company. Playdough

manufactures and sells playdough canisters. This report analyses the decisions to make or buy

(outsource) canisters, accept or reject a special offer to sell the company’s product at a lower

price and the implications of adding a new product line. The evaluation is based on the

associated costs and benefits arising from a given course of action.

Executive Summary

This report focuses on the decision making process at Playdough Company. Playdough

manufactures and sells playdough canisters. This report analyses the decisions to make or buy

(outsource) canisters, accept or reject a special offer to sell the company’s product at a lower

price and the implications of adding a new product line. The evaluation is based on the

associated costs and benefits arising from a given course of action.

Playdoug Company 3

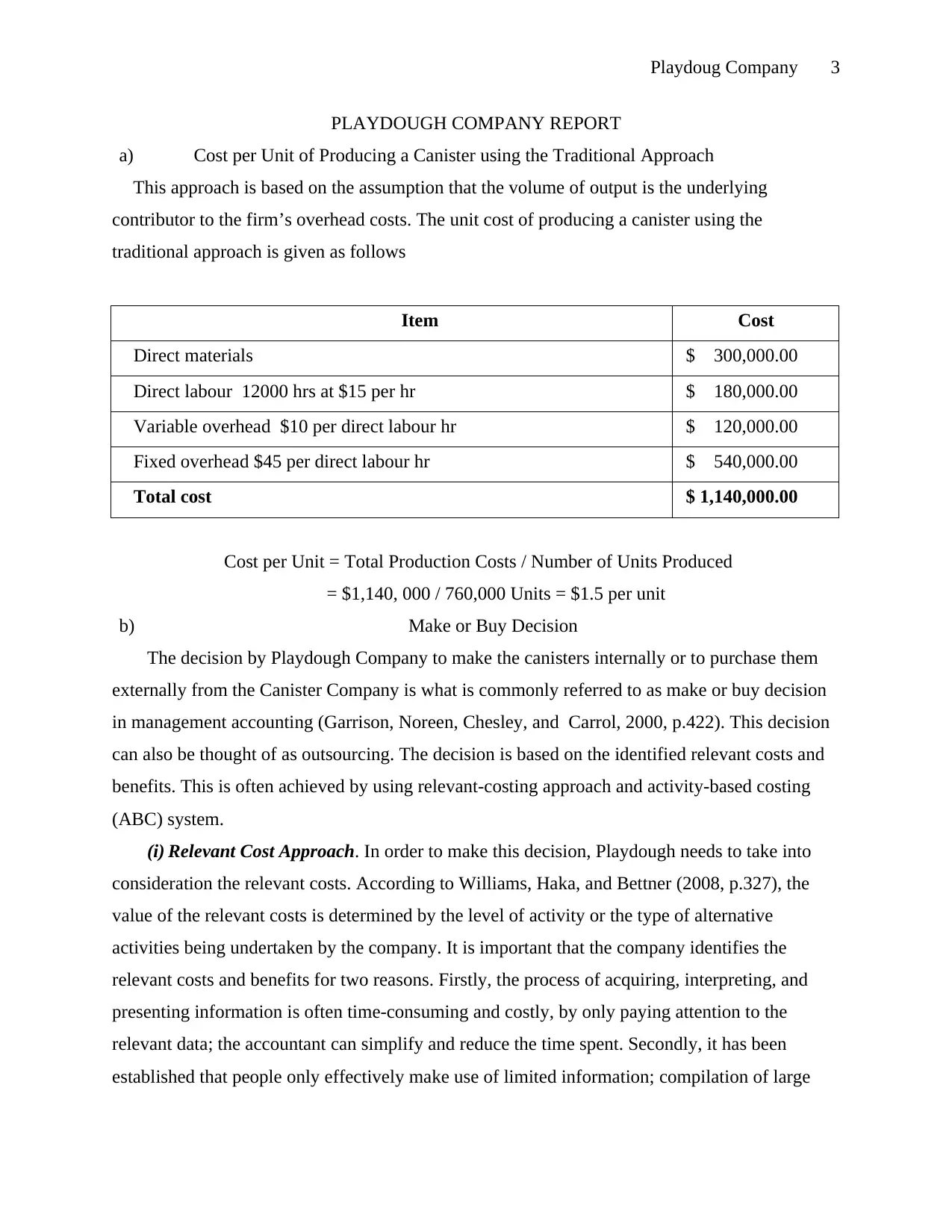

PLAYDOUGH COMPANY REPORT

a) Cost per Unit of Producing a Canister using the Traditional Approach

This approach is based on the assumption that the volume of output is the underlying

contributor to the firm’s overhead costs. The unit cost of producing a canister using the

traditional approach is given as follows

Item Cost

Direct materials $ 300,000.00

Direct labour 12000 hrs at $15 per hr $ 180,000.00

Variable overhead $10 per direct labour hr $ 120,000.00

Fixed overhead $45 per direct labour hr $ 540,000.00

Total cost $ 1,140,000.00

Cost per Unit = Total Production Costs / Number of Units Produced

= $1,140, 000 / 760,000 Units = $1.5 per unit

b) Make or Buy Decision

The decision by Playdough Company to make the canisters internally or to purchase them

externally from the Canister Company is what is commonly referred to as make or buy decision

in management accounting (Garrison, Noreen, Chesley, and Carrol, 2000, p.422). This decision

can also be thought of as outsourcing. The decision is based on the identified relevant costs and

benefits. This is often achieved by using relevant-costing approach and activity-based costing

(ABC) system.

(i) Relevant Cost Approach. In order to make this decision, Playdough needs to take into

consideration the relevant costs. According to Williams, Haka, and Bettner (2008, p.327), the

value of the relevant costs is determined by the level of activity or the type of alternative

activities being undertaken by the company. It is important that the company identifies the

relevant costs and benefits for two reasons. Firstly, the process of acquiring, interpreting, and

presenting information is often time-consuming and costly, by only paying attention to the

relevant data; the accountant can simplify and reduce the time spent. Secondly, it has been

established that people only effectively make use of limited information; compilation of large

PLAYDOUGH COMPANY REPORT

a) Cost per Unit of Producing a Canister using the Traditional Approach

This approach is based on the assumption that the volume of output is the underlying

contributor to the firm’s overhead costs. The unit cost of producing a canister using the

traditional approach is given as follows

Item Cost

Direct materials $ 300,000.00

Direct labour 12000 hrs at $15 per hr $ 180,000.00

Variable overhead $10 per direct labour hr $ 120,000.00

Fixed overhead $45 per direct labour hr $ 540,000.00

Total cost $ 1,140,000.00

Cost per Unit = Total Production Costs / Number of Units Produced

= $1,140, 000 / 760,000 Units = $1.5 per unit

b) Make or Buy Decision

The decision by Playdough Company to make the canisters internally or to purchase them

externally from the Canister Company is what is commonly referred to as make or buy decision

in management accounting (Garrison, Noreen, Chesley, and Carrol, 2000, p.422). This decision

can also be thought of as outsourcing. The decision is based on the identified relevant costs and

benefits. This is often achieved by using relevant-costing approach and activity-based costing

(ABC) system.

(i) Relevant Cost Approach. In order to make this decision, Playdough needs to take into

consideration the relevant costs. According to Williams, Haka, and Bettner (2008, p.327), the

value of the relevant costs is determined by the level of activity or the type of alternative

activities being undertaken by the company. It is important that the company identifies the

relevant costs and benefits for two reasons. Firstly, the process of acquiring, interpreting, and

presenting information is often time-consuming and costly, by only paying attention to the

relevant data; the accountant can simplify and reduce the time spent. Secondly, it has been

established that people only effectively make use of limited information; compilation of large

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Playdoug Company 4

amounts of data reduces the level and quality of decision-making (Hilton and Platt, 2014, p.592).

The most common relevant costs are sunk costs and differential cost.

Sunk costs are those that have already been incurred by the company and cannot be

changed by any current and/ or future actions of the company (Garrison et al., 2000, p. 443). In

this analysis sunk costs are not relevant given that the company has started operations. The

second categories of costs are differential costs which can also be thought of as avoidable,

relevant, and/or incremental costs (Garrison et al., 2000, p. 444). Differential costs are variation

in costs arising from two alternative decisions (Accounting for Management Organisation n.d.).

In the case of Playdough, the differential costs are the only relevant costs. In the

differential cost analysis approach a summary of the benefits of one alternative relative to

another alternative is given. Playdough Company has the choice to make or purchase the

canisters. When making this decision, the company will take into consideration the costs that

would be saved by outsourcing the production relative to the cost of purchasing the canisters.

The company would be able to save variable costs and some overhead costs by outsourcing the

production. The computations are given as follows

Item Cost

Direct materials $ 300,000.00

Direct labour $ 180,000.00

Variable overhead $ 120,000.00

Fixed overhead:

Supervisor Salaries $80,000

Machinery Depreciation $28,000 $ 108,000.00

Total Cost Saved By Outsourcing $ 708,000.00

Cost of Purchasing the Canister = $1 per canister x 760,000 canister = $ 760, 000

The cost spent to purchase the canisters is $ 760,000 while the costs saved is $ 708,000. This

indicates that the amount spent on purchasing the canister rather than producing them in-house

would be $ 42,000 more. It can thus be concluded that it is more beneficial to make the canister

than to buy. Thus the offer is rejected.

(ii) Activity Based Cost Analysis Approach. This approach was developed by Johnson and

Kaplan in 1987 as a solution to the process of determining the costs and factors that bring about

amounts of data reduces the level and quality of decision-making (Hilton and Platt, 2014, p.592).

The most common relevant costs are sunk costs and differential cost.

Sunk costs are those that have already been incurred by the company and cannot be

changed by any current and/ or future actions of the company (Garrison et al., 2000, p. 443). In

this analysis sunk costs are not relevant given that the company has started operations. The

second categories of costs are differential costs which can also be thought of as avoidable,

relevant, and/or incremental costs (Garrison et al., 2000, p. 444). Differential costs are variation

in costs arising from two alternative decisions (Accounting for Management Organisation n.d.).

In the case of Playdough, the differential costs are the only relevant costs. In the

differential cost analysis approach a summary of the benefits of one alternative relative to

another alternative is given. Playdough Company has the choice to make or purchase the

canisters. When making this decision, the company will take into consideration the costs that

would be saved by outsourcing the production relative to the cost of purchasing the canisters.

The company would be able to save variable costs and some overhead costs by outsourcing the

production. The computations are given as follows

Item Cost

Direct materials $ 300,000.00

Direct labour $ 180,000.00

Variable overhead $ 120,000.00

Fixed overhead:

Supervisor Salaries $80,000

Machinery Depreciation $28,000 $ 108,000.00

Total Cost Saved By Outsourcing $ 708,000.00

Cost of Purchasing the Canister = $1 per canister x 760,000 canister = $ 760, 000

The cost spent to purchase the canisters is $ 760,000 while the costs saved is $ 708,000. This

indicates that the amount spent on purchasing the canister rather than producing them in-house

would be $ 42,000 more. It can thus be concluded that it is more beneficial to make the canister

than to buy. Thus the offer is rejected.

(ii) Activity Based Cost Analysis Approach. This approach was developed by Johnson and

Kaplan in 1987 as a solution to the process of determining the costs and factors that bring about

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Playdoug Company 5

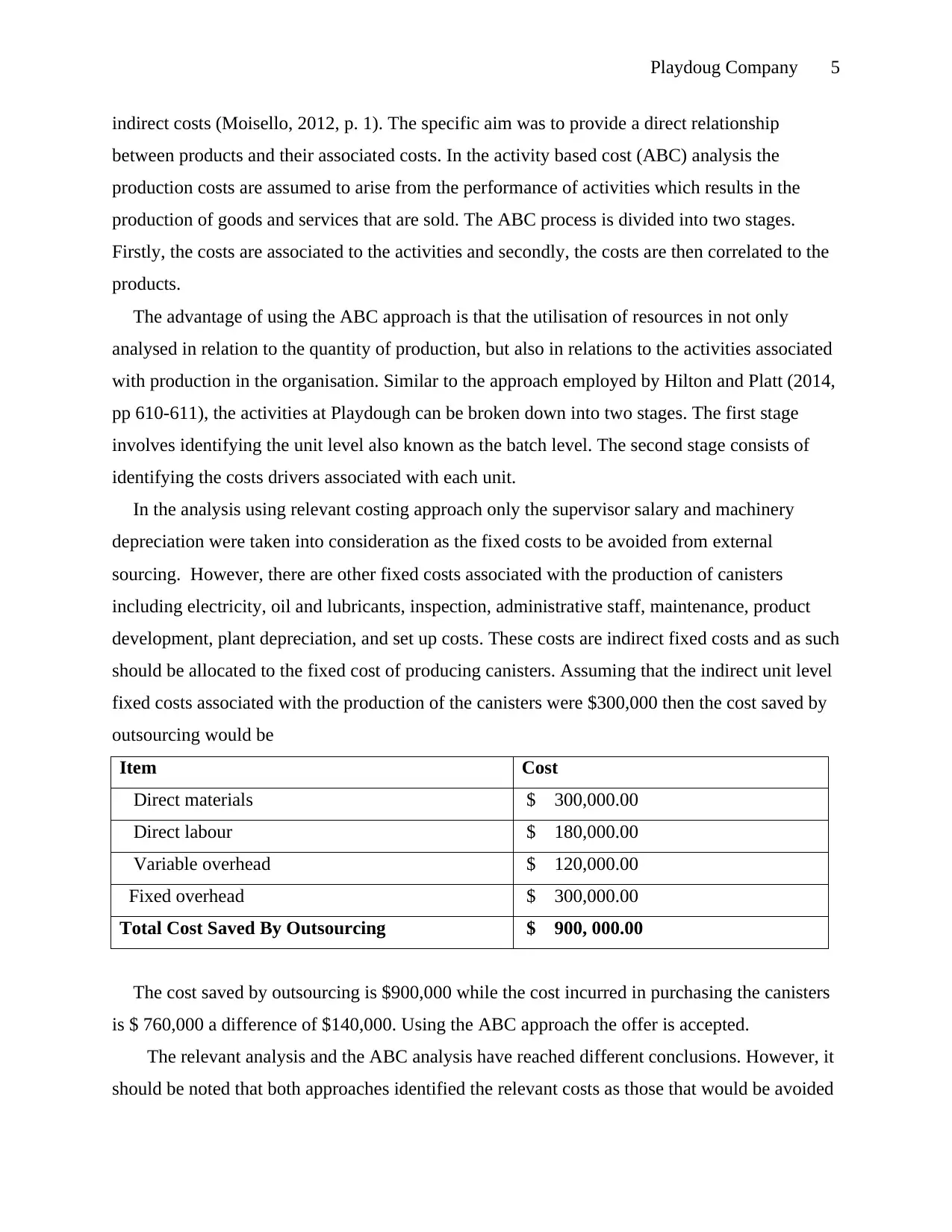

indirect costs (Moisello, 2012, p. 1). The specific aim was to provide a direct relationship

between products and their associated costs. In the activity based cost (ABC) analysis the

production costs are assumed to arise from the performance of activities which results in the

production of goods and services that are sold. The ABC process is divided into two stages.

Firstly, the costs are associated to the activities and secondly, the costs are then correlated to the

products.

The advantage of using the ABC approach is that the utilisation of resources in not only

analysed in relation to the quantity of production, but also in relations to the activities associated

with production in the organisation. Similar to the approach employed by Hilton and Platt (2014,

pp 610-611), the activities at Playdough can be broken down into two stages. The first stage

involves identifying the unit level also known as the batch level. The second stage consists of

identifying the costs drivers associated with each unit.

In the analysis using relevant costing approach only the supervisor salary and machinery

depreciation were taken into consideration as the fixed costs to be avoided from external

sourcing. However, there are other fixed costs associated with the production of canisters

including electricity, oil and lubricants, inspection, administrative staff, maintenance, product

development, plant depreciation, and set up costs. These costs are indirect fixed costs and as such

should be allocated to the fixed cost of producing canisters. Assuming that the indirect unit level

fixed costs associated with the production of the canisters were $300,000 then the cost saved by

outsourcing would be

Item Cost

Direct materials $ 300,000.00

Direct labour $ 180,000.00

Variable overhead $ 120,000.00

Fixed overhead $ 300,000.00

Total Cost Saved By Outsourcing $ 900, 000.00

The cost saved by outsourcing is $900,000 while the cost incurred in purchasing the canisters

is $ 760,000 a difference of $140,000. Using the ABC approach the offer is accepted.

The relevant analysis and the ABC analysis have reached different conclusions. However, it

should be noted that both approaches identified the relevant costs as those that would be avoided

indirect costs (Moisello, 2012, p. 1). The specific aim was to provide a direct relationship

between products and their associated costs. In the activity based cost (ABC) analysis the

production costs are assumed to arise from the performance of activities which results in the

production of goods and services that are sold. The ABC process is divided into two stages.

Firstly, the costs are associated to the activities and secondly, the costs are then correlated to the

products.

The advantage of using the ABC approach is that the utilisation of resources in not only

analysed in relation to the quantity of production, but also in relations to the activities associated

with production in the organisation. Similar to the approach employed by Hilton and Platt (2014,

pp 610-611), the activities at Playdough can be broken down into two stages. The first stage

involves identifying the unit level also known as the batch level. The second stage consists of

identifying the costs drivers associated with each unit.

In the analysis using relevant costing approach only the supervisor salary and machinery

depreciation were taken into consideration as the fixed costs to be avoided from external

sourcing. However, there are other fixed costs associated with the production of canisters

including electricity, oil and lubricants, inspection, administrative staff, maintenance, product

development, plant depreciation, and set up costs. These costs are indirect fixed costs and as such

should be allocated to the fixed cost of producing canisters. Assuming that the indirect unit level

fixed costs associated with the production of the canisters were $300,000 then the cost saved by

outsourcing would be

Item Cost

Direct materials $ 300,000.00

Direct labour $ 180,000.00

Variable overhead $ 120,000.00

Fixed overhead $ 300,000.00

Total Cost Saved By Outsourcing $ 900, 000.00

The cost saved by outsourcing is $900,000 while the cost incurred in purchasing the canisters

is $ 760,000 a difference of $140,000. Using the ABC approach the offer is accepted.

The relevant analysis and the ABC analysis have reached different conclusions. However, it

should be noted that both approaches identified the relevant costs as those that would be avoided

Playdoug Company 6

by purchasing the canisters. According to Holt and Platt (2014, p.611), the consideration of the

avoidable costs is valid with the only difference between both approaches being the better

capability of the ABC approach to specifically recognise the avoidable costs associated with the

process of production. In conclusion, both approaches are valid, however, ABC is more superior

at identifying avoidable costs. Therefore, the company should purchase the canisters.

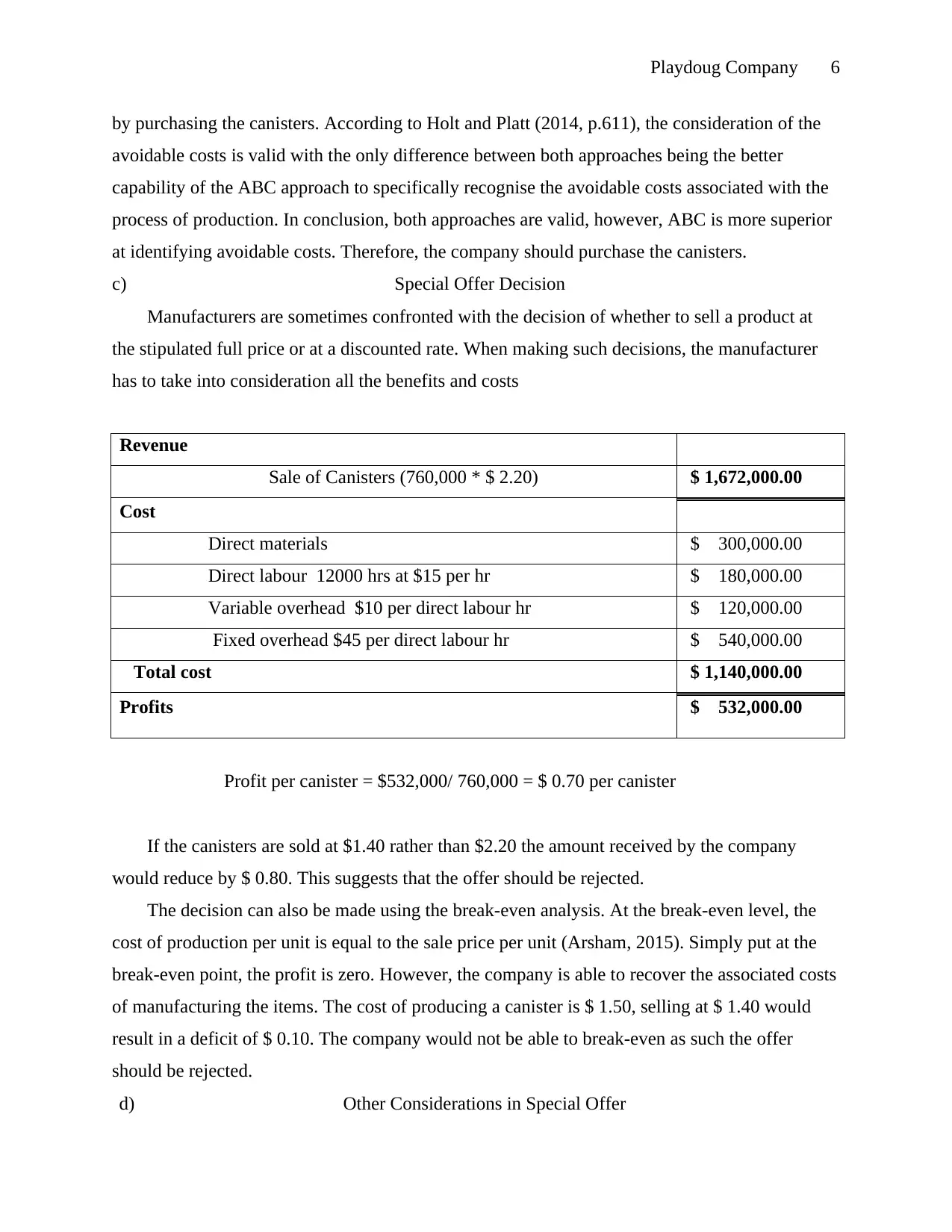

c) Special Offer Decision

Manufacturers are sometimes confronted with the decision of whether to sell a product at

the stipulated full price or at a discounted rate. When making such decisions, the manufacturer

has to take into consideration all the benefits and costs

Revenue

Sale of Canisters (760,000 * $ 2.20) $ 1,672,000.00

Cost

Direct materials $ 300,000.00

Direct labour 12000 hrs at $15 per hr $ 180,000.00

Variable overhead $10 per direct labour hr $ 120,000.00

Fixed overhead $45 per direct labour hr $ 540,000.00

Total cost $ 1,140,000.00

Profits $ 532,000.00

Profit per canister = $532,000/ 760,000 = $ 0.70 per canister

If the canisters are sold at $1.40 rather than $2.20 the amount received by the company

would reduce by $ 0.80. This suggests that the offer should be rejected.

The decision can also be made using the break-even analysis. At the break-even level, the

cost of production per unit is equal to the sale price per unit (Arsham, 2015). Simply put at the

break-even point, the profit is zero. However, the company is able to recover the associated costs

of manufacturing the items. The cost of producing a canister is $ 1.50, selling at $ 1.40 would

result in a deficit of $ 0.10. The company would not be able to break-even as such the offer

should be rejected.

d) Other Considerations in Special Offer

by purchasing the canisters. According to Holt and Platt (2014, p.611), the consideration of the

avoidable costs is valid with the only difference between both approaches being the better

capability of the ABC approach to specifically recognise the avoidable costs associated with the

process of production. In conclusion, both approaches are valid, however, ABC is more superior

at identifying avoidable costs. Therefore, the company should purchase the canisters.

c) Special Offer Decision

Manufacturers are sometimes confronted with the decision of whether to sell a product at

the stipulated full price or at a discounted rate. When making such decisions, the manufacturer

has to take into consideration all the benefits and costs

Revenue

Sale of Canisters (760,000 * $ 2.20) $ 1,672,000.00

Cost

Direct materials $ 300,000.00

Direct labour 12000 hrs at $15 per hr $ 180,000.00

Variable overhead $10 per direct labour hr $ 120,000.00

Fixed overhead $45 per direct labour hr $ 540,000.00

Total cost $ 1,140,000.00

Profits $ 532,000.00

Profit per canister = $532,000/ 760,000 = $ 0.70 per canister

If the canisters are sold at $1.40 rather than $2.20 the amount received by the company

would reduce by $ 0.80. This suggests that the offer should be rejected.

The decision can also be made using the break-even analysis. At the break-even level, the

cost of production per unit is equal to the sale price per unit (Arsham, 2015). Simply put at the

break-even point, the profit is zero. However, the company is able to recover the associated costs

of manufacturing the items. The cost of producing a canister is $ 1.50, selling at $ 1.40 would

result in a deficit of $ 0.10. The company would not be able to break-even as such the offer

should be rejected.

d) Other Considerations in Special Offer

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Playdoug Company 7

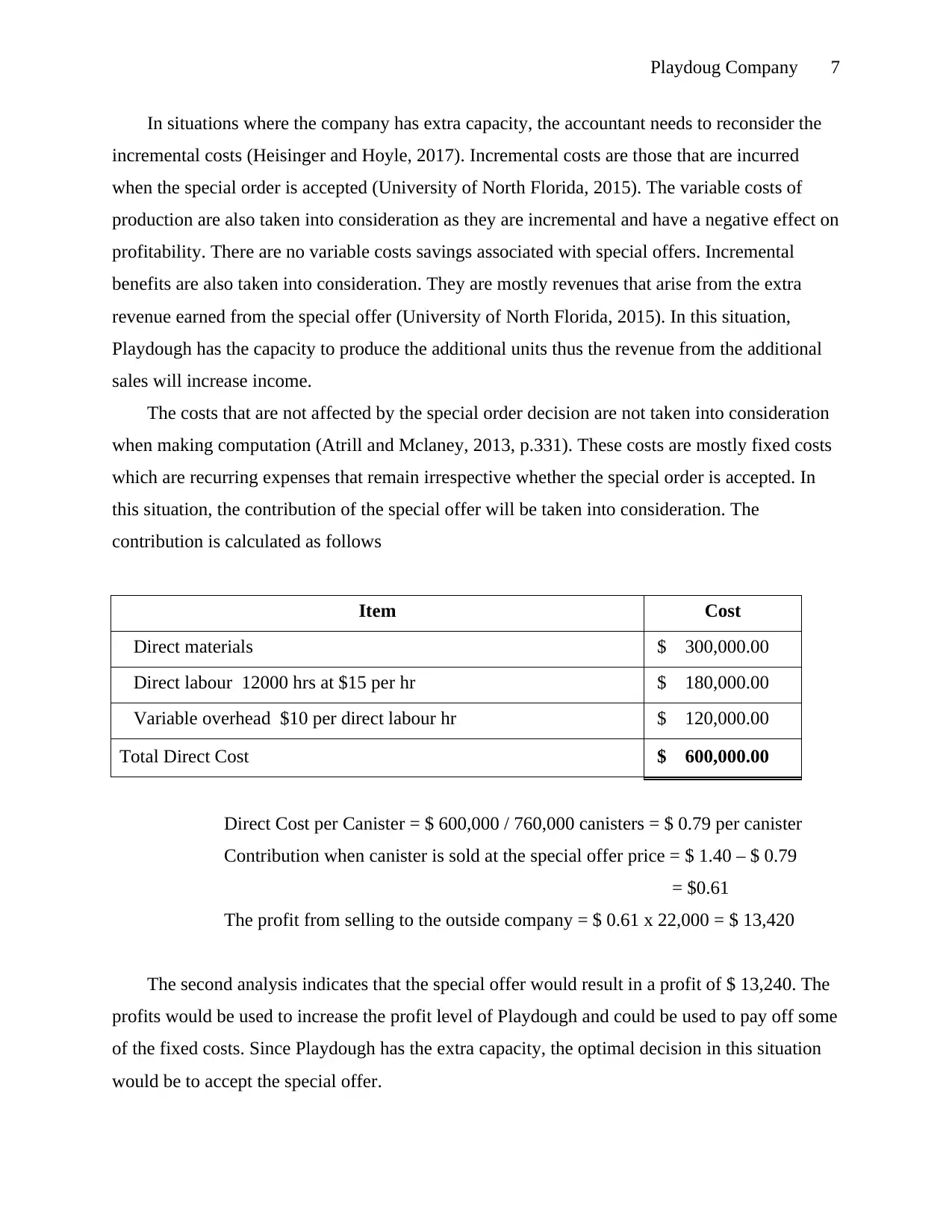

In situations where the company has extra capacity, the accountant needs to reconsider the

incremental costs (Heisinger and Hoyle, 2017). Incremental costs are those that are incurred

when the special order is accepted (University of North Florida, 2015). The variable costs of

production are also taken into consideration as they are incremental and have a negative effect on

profitability. There are no variable costs savings associated with special offers. Incremental

benefits are also taken into consideration. They are mostly revenues that arise from the extra

revenue earned from the special offer (University of North Florida, 2015). In this situation,

Playdough has the capacity to produce the additional units thus the revenue from the additional

sales will increase income.

The costs that are not affected by the special order decision are not taken into consideration

when making computation (Atrill and Mclaney, 2013, p.331). These costs are mostly fixed costs

which are recurring expenses that remain irrespective whether the special order is accepted. In

this situation, the contribution of the special offer will be taken into consideration. The

contribution is calculated as follows

Item Cost

Direct materials $ 300,000.00

Direct labour 12000 hrs at $15 per hr $ 180,000.00

Variable overhead $10 per direct labour hr $ 120,000.00

Total Direct Cost $ 600,000.00

Direct Cost per Canister = $ 600,000 / 760,000 canisters = $ 0.79 per canister

Contribution when canister is sold at the special offer price = $ 1.40 – $ 0.79

= $0.61

The profit from selling to the outside company = $ 0.61 x 22,000 = $ 13,420

The second analysis indicates that the special offer would result in a profit of $ 13,240. The

profits would be used to increase the profit level of Playdough and could be used to pay off some

of the fixed costs. Since Playdough has the extra capacity, the optimal decision in this situation

would be to accept the special offer.

In situations where the company has extra capacity, the accountant needs to reconsider the

incremental costs (Heisinger and Hoyle, 2017). Incremental costs are those that are incurred

when the special order is accepted (University of North Florida, 2015). The variable costs of

production are also taken into consideration as they are incremental and have a negative effect on

profitability. There are no variable costs savings associated with special offers. Incremental

benefits are also taken into consideration. They are mostly revenues that arise from the extra

revenue earned from the special offer (University of North Florida, 2015). In this situation,

Playdough has the capacity to produce the additional units thus the revenue from the additional

sales will increase income.

The costs that are not affected by the special order decision are not taken into consideration

when making computation (Atrill and Mclaney, 2013, p.331). These costs are mostly fixed costs

which are recurring expenses that remain irrespective whether the special order is accepted. In

this situation, the contribution of the special offer will be taken into consideration. The

contribution is calculated as follows

Item Cost

Direct materials $ 300,000.00

Direct labour 12000 hrs at $15 per hr $ 180,000.00

Variable overhead $10 per direct labour hr $ 120,000.00

Total Direct Cost $ 600,000.00

Direct Cost per Canister = $ 600,000 / 760,000 canisters = $ 0.79 per canister

Contribution when canister is sold at the special offer price = $ 1.40 – $ 0.79

= $0.61

The profit from selling to the outside company = $ 0.61 x 22,000 = $ 13,420

The second analysis indicates that the special offer would result in a profit of $ 13,240. The

profits would be used to increase the profit level of Playdough and could be used to pay off some

of the fixed costs. Since Playdough has the extra capacity, the optimal decision in this situation

would be to accept the special offer.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Playdoug Company 8

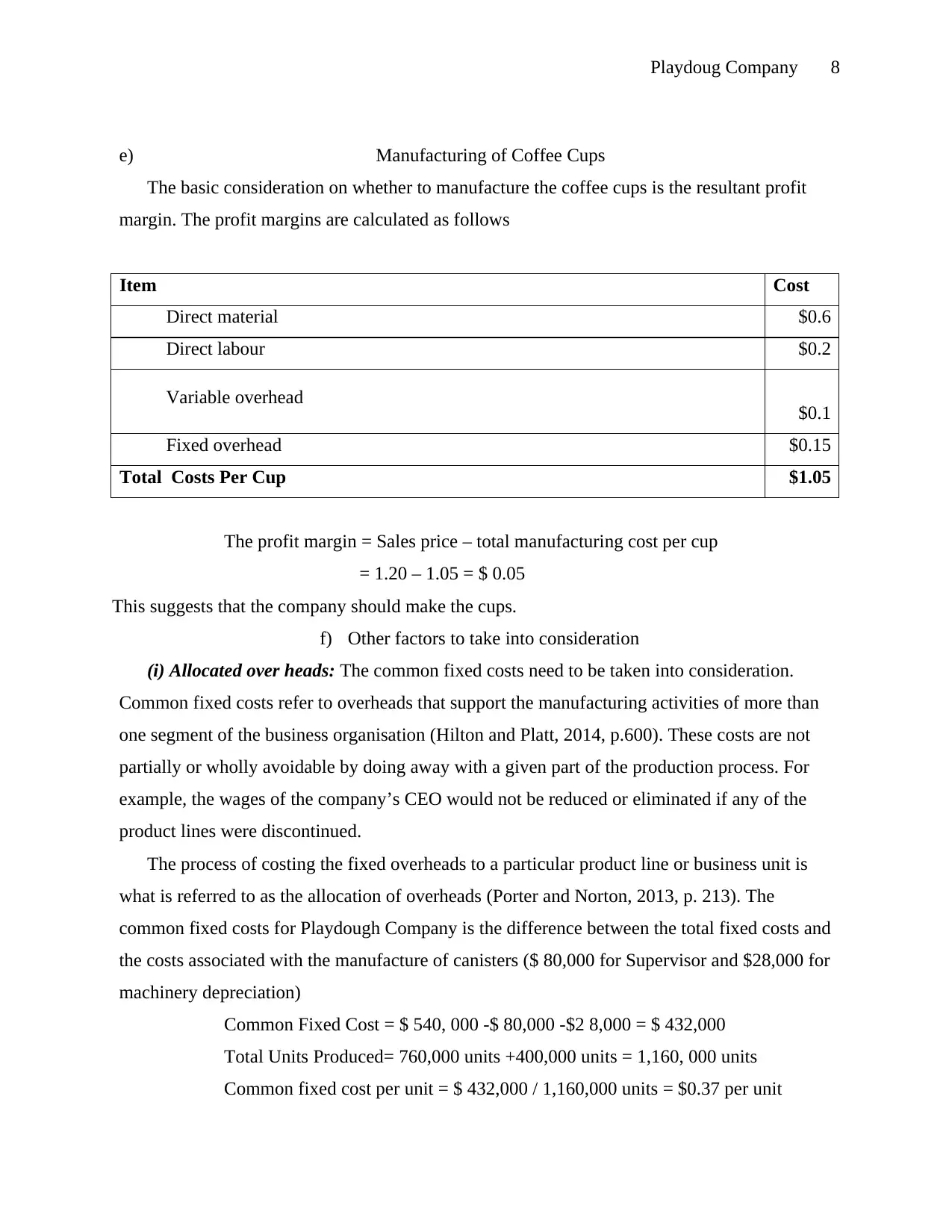

e) Manufacturing of Coffee Cups

The basic consideration on whether to manufacture the coffee cups is the resultant profit

margin. The profit margins are calculated as follows

Item Cost

Direct material $0.6

Direct labour $0.2

Variable overhead $0.1

Fixed overhead $0.15

Total Costs Per Cup $1.05

The profit margin = Sales price – total manufacturing cost per cup

= 1.20 – 1.05 = $ 0.05

This suggests that the company should make the cups.

f) Other factors to take into consideration

(i) Allocated over heads: The common fixed costs need to be taken into consideration.

Common fixed costs refer to overheads that support the manufacturing activities of more than

one segment of the business organisation (Hilton and Platt, 2014, p.600). These costs are not

partially or wholly avoidable by doing away with a given part of the production process. For

example, the wages of the company’s CEO would not be reduced or eliminated if any of the

product lines were discontinued.

The process of costing the fixed overheads to a particular product line or business unit is

what is referred to as the allocation of overheads (Porter and Norton, 2013, p. 213). The

common fixed costs for Playdough Company is the difference between the total fixed costs and

the costs associated with the manufacture of canisters ($ 80,000 for Supervisor and $28,000 for

machinery depreciation)

Common Fixed Cost = $ 540, 000 -$ 80,000 -$2 8,000 = $ 432,000

Total Units Produced= 760,000 units +400,000 units = 1,160, 000 units

Common fixed cost per unit = $ 432,000 / 1,160,000 units = $0.37 per unit

e) Manufacturing of Coffee Cups

The basic consideration on whether to manufacture the coffee cups is the resultant profit

margin. The profit margins are calculated as follows

Item Cost

Direct material $0.6

Direct labour $0.2

Variable overhead $0.1

Fixed overhead $0.15

Total Costs Per Cup $1.05

The profit margin = Sales price – total manufacturing cost per cup

= 1.20 – 1.05 = $ 0.05

This suggests that the company should make the cups.

f) Other factors to take into consideration

(i) Allocated over heads: The common fixed costs need to be taken into consideration.

Common fixed costs refer to overheads that support the manufacturing activities of more than

one segment of the business organisation (Hilton and Platt, 2014, p.600). These costs are not

partially or wholly avoidable by doing away with a given part of the production process. For

example, the wages of the company’s CEO would not be reduced or eliminated if any of the

product lines were discontinued.

The process of costing the fixed overheads to a particular product line or business unit is

what is referred to as the allocation of overheads (Porter and Norton, 2013, p. 213). The

common fixed costs for Playdough Company is the difference between the total fixed costs and

the costs associated with the manufacture of canisters ($ 80,000 for Supervisor and $28,000 for

machinery depreciation)

Common Fixed Cost = $ 540, 000 -$ 80,000 -$2 8,000 = $ 432,000

Total Units Produced= 760,000 units +400,000 units = 1,160, 000 units

Common fixed cost per unit = $ 432,000 / 1,160,000 units = $0.37 per unit

Playdoug Company 9

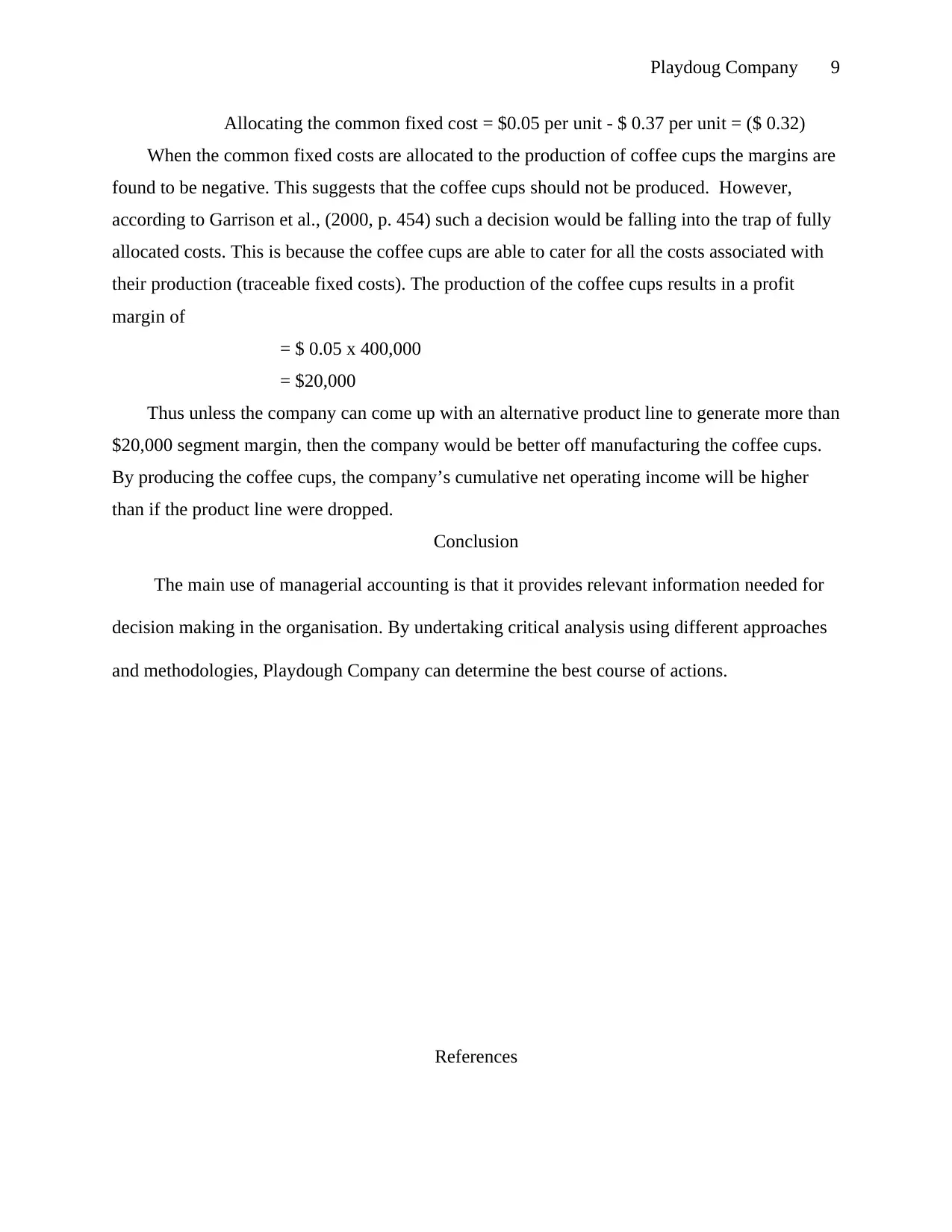

Allocating the common fixed cost = $0.05 per unit - $ 0.37 per unit = ($ 0.32)

When the common fixed costs are allocated to the production of coffee cups the margins are

found to be negative. This suggests that the coffee cups should not be produced. However,

according to Garrison et al., (2000, p. 454) such a decision would be falling into the trap of fully

allocated costs. This is because the coffee cups are able to cater for all the costs associated with

their production (traceable fixed costs). The production of the coffee cups results in a profit

margin of

= $ 0.05 x 400,000

= $20,000

Thus unless the company can come up with an alternative product line to generate more than

$20,000 segment margin, then the company would be better off manufacturing the coffee cups.

By producing the coffee cups, the company’s cumulative net operating income will be higher

than if the product line were dropped.

Conclusion

The main use of managerial accounting is that it provides relevant information needed for

decision making in the organisation. By undertaking critical analysis using different approaches

and methodologies, Playdough Company can determine the best course of actions.

References

Allocating the common fixed cost = $0.05 per unit - $ 0.37 per unit = ($ 0.32)

When the common fixed costs are allocated to the production of coffee cups the margins are

found to be negative. This suggests that the coffee cups should not be produced. However,

according to Garrison et al., (2000, p. 454) such a decision would be falling into the trap of fully

allocated costs. This is because the coffee cups are able to cater for all the costs associated with

their production (traceable fixed costs). The production of the coffee cups results in a profit

margin of

= $ 0.05 x 400,000

= $20,000

Thus unless the company can come up with an alternative product line to generate more than

$20,000 segment margin, then the company would be better off manufacturing the coffee cups.

By producing the coffee cups, the company’s cumulative net operating income will be higher

than if the product line were dropped.

Conclusion

The main use of managerial accounting is that it provides relevant information needed for

decision making in the organisation. By undertaking critical analysis using different approaches

and methodologies, Playdough Company can determine the best course of actions.

References

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Playdoug Company 10

Accounting for Management Organisation (n.d.) Differential, opportunity and sunk costs.

Available at < http://www.accountingformanagement.org/differential-opportunity-and-

sunk-costs/> (Accessed: 30 August 2017).

Arsham, P., 2015. Break even analysis and forecasting. Available at

<https://home.ubalt.edu/ntsbarsh/Business-stat/otherapplets/BreakEven.htm> (Accessed:

30 August 201).

Atrill, P., and Mclaney, E., 2013. Financial accounting for decision making (7th ed. ).

New York: Pearson.

Garrison, R., Noreen, E., Chesley, G., and Carrol, R., 2000. Managerial Accounting: Concepts

for planning, control, and decision making (4th ed.). New York: Mc-Graw-Hill Ryerson.

Heisinger, K., and Hoyle, J., 2017. Special order decisions. Flat world. Available at

<https://catalog.flatworldknowledge.com/bookhub/reader/4402?e=heisinger_1.0-

ch07_s02> (Accessed: 31 August 2017).

Hilton, R., and Platt, D., 2014. Managerial Accounting: Creating value in a dynamic business

environment (10th ed.). New York: McGraw-Hill.

Moisello, A., 2012. Costing for decision making: Activity based costing vs. theory of constraints.

The International Journal of Knowledge, Culture, and Change Management, 12, pp. 1-

12.

Porter, G., and Norton, C., 2013. Financial accounting: The impact on decision making (8th ed.).

Ohio: South-western, Cengage Learning.

Williams, J., Haka, S., and Bettner, S., 2005. Financial and managerial accounting: The basis of

business decision. Boston: McGraw-Hill.

University of North Florida, 2015. Special order decision. Available at

http://www.unf.edu/~dtanner/dtch/dt_ch20.htm (Accessed: 31 August 2017).

Accounting for Management Organisation (n.d.) Differential, opportunity and sunk costs.

Available at < http://www.accountingformanagement.org/differential-opportunity-and-

sunk-costs/> (Accessed: 30 August 2017).

Arsham, P., 2015. Break even analysis and forecasting. Available at

<https://home.ubalt.edu/ntsbarsh/Business-stat/otherapplets/BreakEven.htm> (Accessed:

30 August 201).

Atrill, P., and Mclaney, E., 2013. Financial accounting for decision making (7th ed. ).

New York: Pearson.

Garrison, R., Noreen, E., Chesley, G., and Carrol, R., 2000. Managerial Accounting: Concepts

for planning, control, and decision making (4th ed.). New York: Mc-Graw-Hill Ryerson.

Heisinger, K., and Hoyle, J., 2017. Special order decisions. Flat world. Available at

<https://catalog.flatworldknowledge.com/bookhub/reader/4402?e=heisinger_1.0-

ch07_s02> (Accessed: 31 August 2017).

Hilton, R., and Platt, D., 2014. Managerial Accounting: Creating value in a dynamic business

environment (10th ed.). New York: McGraw-Hill.

Moisello, A., 2012. Costing for decision making: Activity based costing vs. theory of constraints.

The International Journal of Knowledge, Culture, and Change Management, 12, pp. 1-

12.

Porter, G., and Norton, C., 2013. Financial accounting: The impact on decision making (8th ed.).

Ohio: South-western, Cengage Learning.

Williams, J., Haka, S., and Bettner, S., 2005. Financial and managerial accounting: The basis of

business decision. Boston: McGraw-Hill.

University of North Florida, 2015. Special order decision. Available at

http://www.unf.edu/~dtanner/dtch/dt_ch20.htm (Accessed: 31 August 2017).

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.