Financial Portfolio Analysis: Assessing Risk, Return, and Cost

VerifiedAdded on 2023/06/15

|11

|2993

|329

Report

AI Summary

This report conducts a portfolio analysis of Accenture (ACN) and Ameriprise Financial (AMP), representing the IT and Financial sectors, respectively. Using six years of stock price data (2016-2021), the analysis forms an equally weighted portfolio to determine risk and return dynamics, calculating monthly returns, average returns, and standard deviation. The report then explores optimal portfolio construction through various stock combinations, evaluating risk-return trade-offs. Furthermore, it estimates the equity cost of capital for both companies, considering beta, risk-free rate, and average stock return, and discusses the impact of economic conditions on the weighted average cost of capital (WACC). The report concludes by highlighting the benefits of portfolio diversification and the importance of managing risk to achieve optimal returns. Desklib provides access to past papers and solved assignments for students seeking further assistance.

PORTFOLIO ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

COMPANY BACKGROUND........................................................................................................3

SECTION A – Two Asset Portfolio................................................................................................3

Forming an equally weighted portfolio to determine risk and return dynamics..........................3

SECTION B – Optimal Portfolio....................................................................................................5

Average annual returns and standard deviation of various portfolios (Combination of two

stocks)..........................................................................................................................................5

SECTION C – Cost of Capital.........................................................................................................7

Estimation of equity cost of capital.............................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

COMPANY BACKGROUND........................................................................................................3

SECTION A – Two Asset Portfolio................................................................................................3

Forming an equally weighted portfolio to determine risk and return dynamics..........................3

SECTION B – Optimal Portfolio....................................................................................................5

Average annual returns and standard deviation of various portfolios (Combination of two

stocks)..........................................................................................................................................5

SECTION C – Cost of Capital.........................................................................................................7

Estimation of equity cost of capital.............................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

COMPANY BACKGROUND

The present report will be based on Accenture and Ameriprise Financial Plc which are belonging

from two distinct sectors of the economy that is, IT and Financial sector. Accenture is a

specialized MNC basically into providing consultation and IT services based in Ireland. In

addition to this, Ameriprise Financial is a bank holding and diversified financial services

company based in Minneapolis, Minnesota (Narayan and Rehman, 2020).

Accenture and Ameriprise Financial, both are the companies forming part of S&P 500

index for which stock price data has been obtained for the last six years beginning from 1st

September 2016 to 31st August 2021. These companies are belonging from two distinct sectors as

per the industrial classification done by GICS (Global Industry Classification Standards).

Accenture belongs from Information Technology sector whose industry group, industry and sub

– industry is software and services, IT services and IT consulting and other services respectively

(Li and et.al., 2019). On the other hand, Ameriprise Financial belongs from financial sector

whose industry group, industry and sub – industry is diversified financial, capital markets and

Asset management & custody banks respectively.

SECTION A – Two Asset Portfolio

Forming an equally weighted portfolio to determine risk and return dynamics

Therefore, if equally weighted portfolio will be formed for these two stocks, then 50:50

proportion will be given to both of these portfolios. To determine the monthly returns of these

stocks individually, their current month closing price has been subtracted from the closing price

of the previous months and the result so derived has been divided by the previous month’s

closing price. In this way, monthly returns have been obtained for each of these two stocks

(Balcilar, Ozdemir and Ozdemir, 2021). Accordingly, average of these monthly returns has been

calculated for both of these stocks to determine the individual average return of each stock. Also,

to determine the risk of these stocks, standard deviation has been calculated on the basis of

monthly returns of the stock through excel formula. Further, to determine the risk and return

associated with the portfolio comprising of these two stock in equal proportion, the following

calculations has been done:

The present report will be based on Accenture and Ameriprise Financial Plc which are belonging

from two distinct sectors of the economy that is, IT and Financial sector. Accenture is a

specialized MNC basically into providing consultation and IT services based in Ireland. In

addition to this, Ameriprise Financial is a bank holding and diversified financial services

company based in Minneapolis, Minnesota (Narayan and Rehman, 2020).

Accenture and Ameriprise Financial, both are the companies forming part of S&P 500

index for which stock price data has been obtained for the last six years beginning from 1st

September 2016 to 31st August 2021. These companies are belonging from two distinct sectors as

per the industrial classification done by GICS (Global Industry Classification Standards).

Accenture belongs from Information Technology sector whose industry group, industry and sub

– industry is software and services, IT services and IT consulting and other services respectively

(Li and et.al., 2019). On the other hand, Ameriprise Financial belongs from financial sector

whose industry group, industry and sub – industry is diversified financial, capital markets and

Asset management & custody banks respectively.

SECTION A – Two Asset Portfolio

Forming an equally weighted portfolio to determine risk and return dynamics

Therefore, if equally weighted portfolio will be formed for these two stocks, then 50:50

proportion will be given to both of these portfolios. To determine the monthly returns of these

stocks individually, their current month closing price has been subtracted from the closing price

of the previous months and the result so derived has been divided by the previous month’s

closing price. In this way, monthly returns have been obtained for each of these two stocks

(Balcilar, Ozdemir and Ozdemir, 2021). Accordingly, average of these monthly returns has been

calculated for both of these stocks to determine the individual average return of each stock. Also,

to determine the risk of these stocks, standard deviation has been calculated on the basis of

monthly returns of the stock through excel formula. Further, to determine the risk and return

associated with the portfolio comprising of these two stock in equal proportion, the following

calculations has been done:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Portfolio returns

Return on stock of Accenture (ACN) = 1.90%

Return on stock of Ameriprise Financial (AMP) = 2.19%

Weights assignment will be 50% to each stock, as it is an equally weighted portfolio. Therefore,

portfolio return will be calculated as follows:

Rp = RACN * 0.5 + RAMP * 0.5 = 0.019 * 0.5 + 0.0219 * 0.5 = 0.0095 + 0.01095

= 0.02045 or 2.045%.

Portfolio risk

To determine the risk of portfolio comprising of equally weighted two assets or stocks, the

following formula could be used:

σP = √ σ12 * w12 + σ22 * w22 + 2 * w1 * w2 * ρ 1 2 * σ1 * σ2

σ1 = 5.8% (Standard deviation of monthly returns on ACN)

w1 = 50% (Weight assigned to ACN stock in the portfolio)

σ2 = 9.7% (Standard deviation of monthly returns on AMP)

w2 = 50% (Weight assigned to AMP stock in the portfolio)

ρ 1 2 = 0.63 (Correlation between monthly returns of ACN and AMP)

σP = √ (0.058)2 * (0.5)2 + (0.097)2 * (0.5)2 + 2 * 0.5 * 0.5 * 0.63 * 0.058 * 0.097

σP = √ 0.0034 * 0.25 + 0.0094 * 0.25 + 0.0018

σP = √ 0.00085 + 0.00235 + 0.0018

σP = √0.005 = 0.07 or 7%.

Interpretation of risk and return from equally weighted portfolio

From the risk and return obtained by giving equal weightage to both stocks in the portfolio, it has

been identified that if investment is done individually into these stocks then there will be less risk

and less return in case of ACN stock whereas there would be higher risk and higher return for

Return on stock of Accenture (ACN) = 1.90%

Return on stock of Ameriprise Financial (AMP) = 2.19%

Weights assignment will be 50% to each stock, as it is an equally weighted portfolio. Therefore,

portfolio return will be calculated as follows:

Rp = RACN * 0.5 + RAMP * 0.5 = 0.019 * 0.5 + 0.0219 * 0.5 = 0.0095 + 0.01095

= 0.02045 or 2.045%.

Portfolio risk

To determine the risk of portfolio comprising of equally weighted two assets or stocks, the

following formula could be used:

σP = √ σ12 * w12 + σ22 * w22 + 2 * w1 * w2 * ρ 1 2 * σ1 * σ2

σ1 = 5.8% (Standard deviation of monthly returns on ACN)

w1 = 50% (Weight assigned to ACN stock in the portfolio)

σ2 = 9.7% (Standard deviation of monthly returns on AMP)

w2 = 50% (Weight assigned to AMP stock in the portfolio)

ρ 1 2 = 0.63 (Correlation between monthly returns of ACN and AMP)

σP = √ (0.058)2 * (0.5)2 + (0.097)2 * (0.5)2 + 2 * 0.5 * 0.5 * 0.63 * 0.058 * 0.097

σP = √ 0.0034 * 0.25 + 0.0094 * 0.25 + 0.0018

σP = √ 0.00085 + 0.00235 + 0.0018

σP = √0.005 = 0.07 or 7%.

Interpretation of risk and return from equally weighted portfolio

From the risk and return obtained by giving equal weightage to both stocks in the portfolio, it has

been identified that if investment is done individually into these stocks then there will be less risk

and less return in case of ACN stock whereas there would be higher risk and higher return for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AMP stock (Fang, Tan and Wirjanto, 2019). However, by forming a portfolio of stocks, risks can

be diversified and at a lower risk of 7%, there would be approximately 2% returns that could be

generated by investing equally into each of the two stocks (Vamvakaris, Pantelous and Zuev,

2018). It can be seen that, if a risk averse investor who want to earn higher returns by taking

lower risks he can be go for investing forming portfolio of two stocks as higher risk attached

with AMP’s stock can be easily diversified through including different sector’s stock in the

portfolio.

Critical discussion of value of portfolio diversification

Portfolio diversification refers to the minimization of overall risk involved in the portfolio of

assets or stocks by making investment in different securities and asset classes. The most basic

purpose for which portfolio diversification is done is to reduce the risk associated with a specific

market segment or company (Narayan and Rehman, 2018). There are various benefits that could

be enjoyed by a risk averse investor by diversifying his portfolio such as impact of market

volatility and time spent on portfolio monitoring can be reduced along with taking advantage of

various investible instruments.

However, portfolio diversification has been criticized on various grounds such as it limits

higher returns associated with single security by including lower return security in the portfolio

as can be seen in the above case where ACN having comparatively lower returns than AMP has

been included in the portfolio (Li and et.al., 2019).

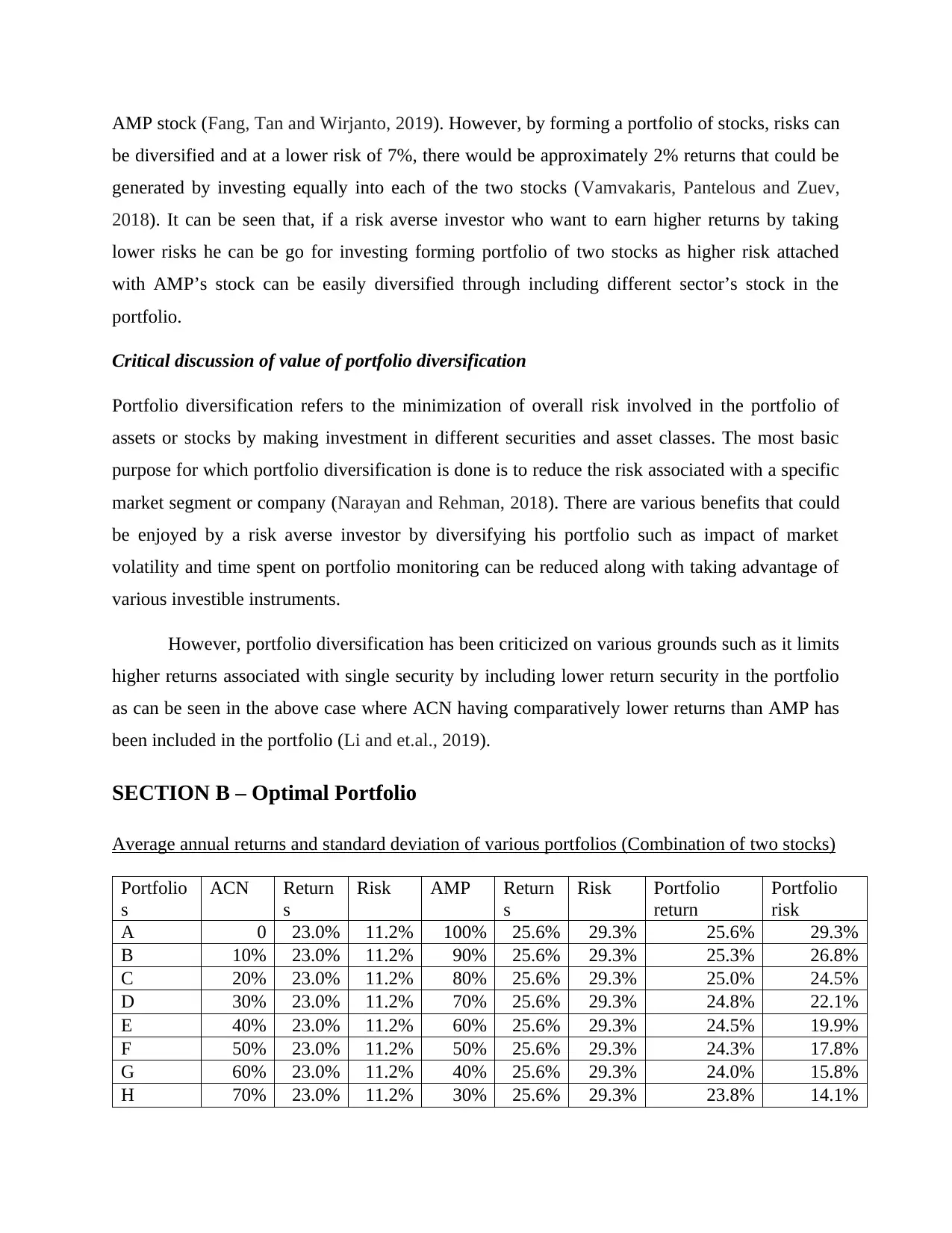

SECTION B – Optimal Portfolio

Average annual returns and standard deviation of various portfolios (Combination of two stocks)

Portfolio

s

ACN Return

s

Risk AMP Return

s

Risk Portfolio

return

Portfolio

risk

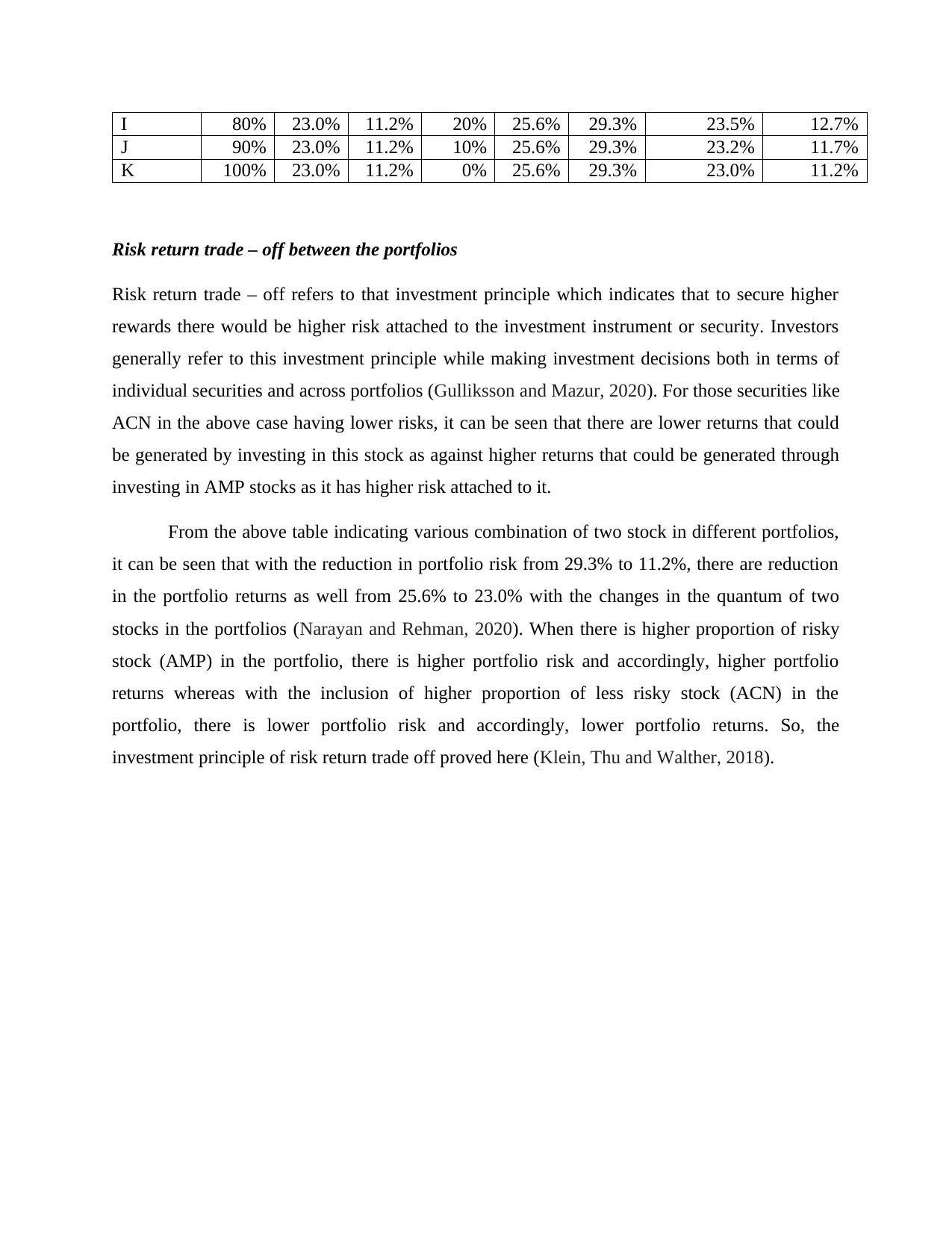

A 0 23.0% 11.2% 100% 25.6% 29.3% 25.6% 29.3%

B 10% 23.0% 11.2% 90% 25.6% 29.3% 25.3% 26.8%

C 20% 23.0% 11.2% 80% 25.6% 29.3% 25.0% 24.5%

D 30% 23.0% 11.2% 70% 25.6% 29.3% 24.8% 22.1%

E 40% 23.0% 11.2% 60% 25.6% 29.3% 24.5% 19.9%

F 50% 23.0% 11.2% 50% 25.6% 29.3% 24.3% 17.8%

G 60% 23.0% 11.2% 40% 25.6% 29.3% 24.0% 15.8%

H 70% 23.0% 11.2% 30% 25.6% 29.3% 23.8% 14.1%

be diversified and at a lower risk of 7%, there would be approximately 2% returns that could be

generated by investing equally into each of the two stocks (Vamvakaris, Pantelous and Zuev,

2018). It can be seen that, if a risk averse investor who want to earn higher returns by taking

lower risks he can be go for investing forming portfolio of two stocks as higher risk attached

with AMP’s stock can be easily diversified through including different sector’s stock in the

portfolio.

Critical discussion of value of portfolio diversification

Portfolio diversification refers to the minimization of overall risk involved in the portfolio of

assets or stocks by making investment in different securities and asset classes. The most basic

purpose for which portfolio diversification is done is to reduce the risk associated with a specific

market segment or company (Narayan and Rehman, 2018). There are various benefits that could

be enjoyed by a risk averse investor by diversifying his portfolio such as impact of market

volatility and time spent on portfolio monitoring can be reduced along with taking advantage of

various investible instruments.

However, portfolio diversification has been criticized on various grounds such as it limits

higher returns associated with single security by including lower return security in the portfolio

as can be seen in the above case where ACN having comparatively lower returns than AMP has

been included in the portfolio (Li and et.al., 2019).

SECTION B – Optimal Portfolio

Average annual returns and standard deviation of various portfolios (Combination of two stocks)

Portfolio

s

ACN Return

s

Risk AMP Return

s

Risk Portfolio

return

Portfolio

risk

A 0 23.0% 11.2% 100% 25.6% 29.3% 25.6% 29.3%

B 10% 23.0% 11.2% 90% 25.6% 29.3% 25.3% 26.8%

C 20% 23.0% 11.2% 80% 25.6% 29.3% 25.0% 24.5%

D 30% 23.0% 11.2% 70% 25.6% 29.3% 24.8% 22.1%

E 40% 23.0% 11.2% 60% 25.6% 29.3% 24.5% 19.9%

F 50% 23.0% 11.2% 50% 25.6% 29.3% 24.3% 17.8%

G 60% 23.0% 11.2% 40% 25.6% 29.3% 24.0% 15.8%

H 70% 23.0% 11.2% 30% 25.6% 29.3% 23.8% 14.1%

I 80% 23.0% 11.2% 20% 25.6% 29.3% 23.5% 12.7%

J 90% 23.0% 11.2% 10% 25.6% 29.3% 23.2% 11.7%

K 100% 23.0% 11.2% 0% 25.6% 29.3% 23.0% 11.2%

Risk return trade – off between the portfolios

Risk return trade – off refers to that investment principle which indicates that to secure higher

rewards there would be higher risk attached to the investment instrument or security. Investors

generally refer to this investment principle while making investment decisions both in terms of

individual securities and across portfolios (Gulliksson and Mazur, 2020). For those securities like

ACN in the above case having lower risks, it can be seen that there are lower returns that could

be generated by investing in this stock as against higher returns that could be generated through

investing in AMP stocks as it has higher risk attached to it.

From the above table indicating various combination of two stock in different portfolios,

it can be seen that with the reduction in portfolio risk from 29.3% to 11.2%, there are reduction

in the portfolio returns as well from 25.6% to 23.0% with the changes in the quantum of two

stocks in the portfolios (Narayan and Rehman, 2020). When there is higher proportion of risky

stock (AMP) in the portfolio, there is higher portfolio risk and accordingly, higher portfolio

returns whereas with the inclusion of higher proportion of less risky stock (ACN) in the

portfolio, there is lower portfolio risk and accordingly, lower portfolio returns. So, the

investment principle of risk return trade off proved here (Klein, Thu and Walther, 2018).

J 90% 23.0% 11.2% 10% 25.6% 29.3% 23.2% 11.7%

K 100% 23.0% 11.2% 0% 25.6% 29.3% 23.0% 11.2%

Risk return trade – off between the portfolios

Risk return trade – off refers to that investment principle which indicates that to secure higher

rewards there would be higher risk attached to the investment instrument or security. Investors

generally refer to this investment principle while making investment decisions both in terms of

individual securities and across portfolios (Gulliksson and Mazur, 2020). For those securities like

ACN in the above case having lower risks, it can be seen that there are lower returns that could

be generated by investing in this stock as against higher returns that could be generated through

investing in AMP stocks as it has higher risk attached to it.

From the above table indicating various combination of two stock in different portfolios,

it can be seen that with the reduction in portfolio risk from 29.3% to 11.2%, there are reduction

in the portfolio returns as well from 25.6% to 23.0% with the changes in the quantum of two

stocks in the portfolios (Narayan and Rehman, 2020). When there is higher proportion of risky

stock (AMP) in the portfolio, there is higher portfolio risk and accordingly, higher portfolio

returns whereas with the inclusion of higher proportion of less risky stock (ACN) in the

portfolio, there is lower portfolio risk and accordingly, lower portfolio returns. So, the

investment principle of risk return trade off proved here (Klein, Thu and Walther, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

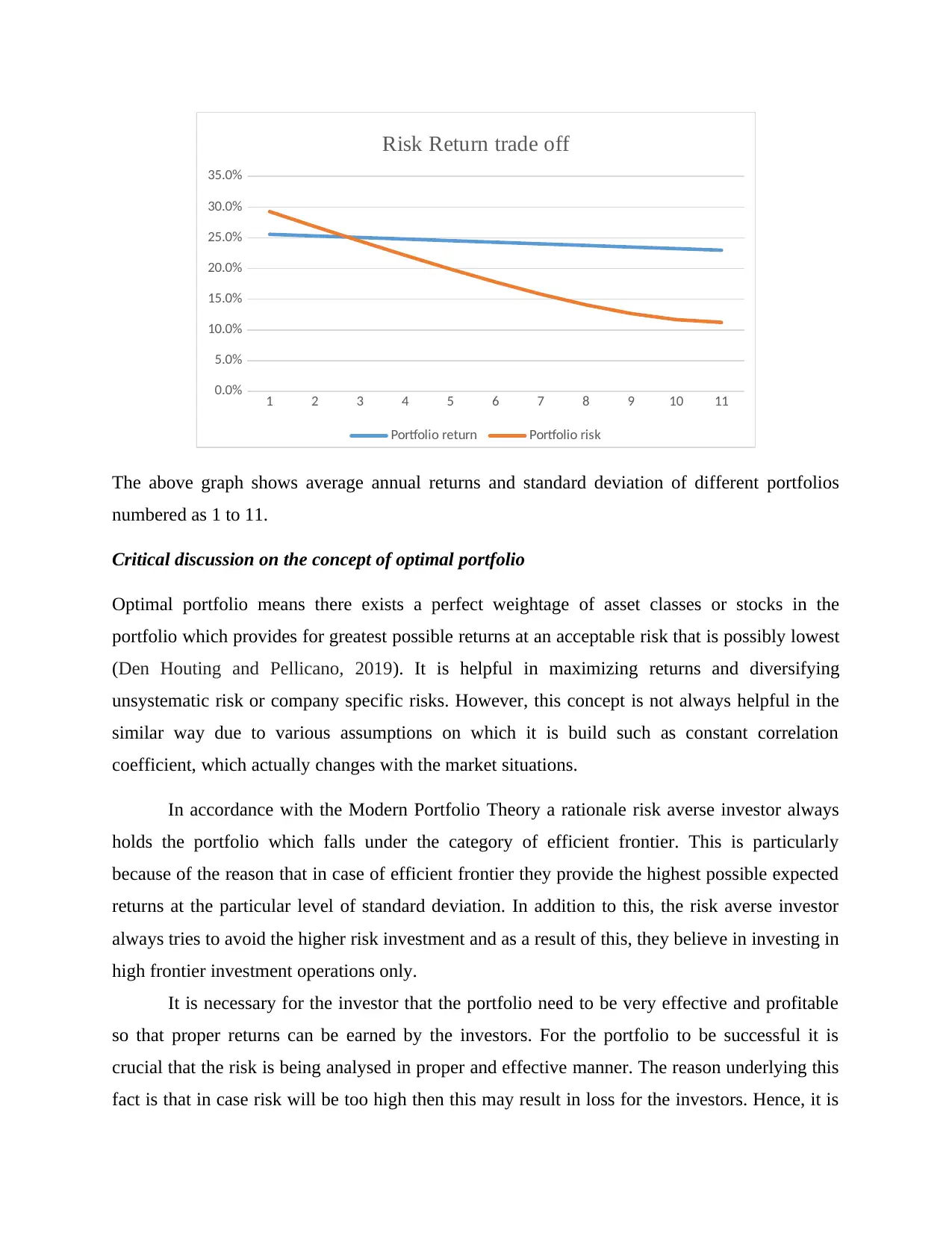

1 2 3 4 5 6 7 8 9 10 11

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

Risk Return trade off

Portfolio return Portfolio risk

The above graph shows average annual returns and standard deviation of different portfolios

numbered as 1 to 11.

Critical discussion on the concept of optimal portfolio

Optimal portfolio means there exists a perfect weightage of asset classes or stocks in the

portfolio which provides for greatest possible returns at an acceptable risk that is possibly lowest

(Den Houting and Pellicano, 2019). It is helpful in maximizing returns and diversifying

unsystematic risk or company specific risks. However, this concept is not always helpful in the

similar way due to various assumptions on which it is build such as constant correlation

coefficient, which actually changes with the market situations.

In accordance with the Modern Portfolio Theory a rationale risk averse investor always

holds the portfolio which falls under the category of efficient frontier. This is particularly

because of the reason that in case of efficient frontier they provide the highest possible expected

returns at the particular level of standard deviation. In addition to this, the risk averse investor

always tries to avoid the higher risk investment and as a result of this, they believe in investing in

high frontier investment operations only.

It is necessary for the investor that the portfolio need to be very effective and profitable

so that proper returns can be earned by the investors. For the portfolio to be successful it is

crucial that the risk is being analysed in proper and effective manner. The reason underlying this

fact is that in case risk will be too high then this may result in loss for the investors. Hence, it is

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

Risk Return trade off

Portfolio return Portfolio risk

The above graph shows average annual returns and standard deviation of different portfolios

numbered as 1 to 11.

Critical discussion on the concept of optimal portfolio

Optimal portfolio means there exists a perfect weightage of asset classes or stocks in the

portfolio which provides for greatest possible returns at an acceptable risk that is possibly lowest

(Den Houting and Pellicano, 2019). It is helpful in maximizing returns and diversifying

unsystematic risk or company specific risks. However, this concept is not always helpful in the

similar way due to various assumptions on which it is build such as constant correlation

coefficient, which actually changes with the market situations.

In accordance with the Modern Portfolio Theory a rationale risk averse investor always

holds the portfolio which falls under the category of efficient frontier. This is particularly

because of the reason that in case of efficient frontier they provide the highest possible expected

returns at the particular level of standard deviation. In addition to this, the risk averse investor

always tries to avoid the higher risk investment and as a result of this, they believe in investing in

high frontier investment operations only.

It is necessary for the investor that the portfolio need to be very effective and profitable

so that proper returns can be earned by the investors. For the portfolio to be successful it is

crucial that the risk is being analysed in proper and effective manner. The reason underlying this

fact is that in case risk will be too high then this may result in loss for the investors. Hence, it is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

very crucial for them to ensure that the risk involved within the portfolio falls under the category

of tolerance so that profitability is not affected to a great extent.

SECTION C – Cost of Capital

Estimation of equity cost of capital

Equity cost of capital of capital of ACN

Beta of the stock = 1.13

Risk free rate of return = 1.46%

Average monthly return of stock = 1.9%

Formula = Risk free return + [Beta * (Average stock return – risk free return)]

Equity cost of capital = 1.46% + [1.13 * (1.9% – 1.46%)] = 1.46% + 0.4972 = 1.9572%

Equity cost of capital of capital of AMP

Beta of the stock = 1.61

Risk free rate of return = 1.46%

Average monthly return of stock = 2.19%

Equity cost of capital = 1.46% + [1.61 * (2.19% – 1.46%)] = 1.46% + 1.1753 = 2.6353%

The weighted average cost of capital is defined as the average of all the cost relating to

external funding which company uses in order to operate. This is very important for the company

because in case the capital will not be taken in proper manner then this will be affecting the

working efficiency of the company. Thus, according to Steffen (2020) the primary driver of

WACC that is weighted average cost of capital is cost of equity and the cost of debt. In addition

to this, there are many different types of factors which can affect the WACC to a great extent.

This is particularly because of the reason that cost is being defined by the market rate and it is

not necessary that the cost of capital is static because there are many changes within the external

environment.

In addition to this cost, another key driver of WACC is that economic condition. This is

also a driver of WACC because in case the economic condition is not good and there is increase

of tolerance so that profitability is not affected to a great extent.

SECTION C – Cost of Capital

Estimation of equity cost of capital

Equity cost of capital of capital of ACN

Beta of the stock = 1.13

Risk free rate of return = 1.46%

Average monthly return of stock = 1.9%

Formula = Risk free return + [Beta * (Average stock return – risk free return)]

Equity cost of capital = 1.46% + [1.13 * (1.9% – 1.46%)] = 1.46% + 0.4972 = 1.9572%

Equity cost of capital of capital of AMP

Beta of the stock = 1.61

Risk free rate of return = 1.46%

Average monthly return of stock = 2.19%

Equity cost of capital = 1.46% + [1.61 * (2.19% – 1.46%)] = 1.46% + 1.1753 = 2.6353%

The weighted average cost of capital is defined as the average of all the cost relating to

external funding which company uses in order to operate. This is very important for the company

because in case the capital will not be taken in proper manner then this will be affecting the

working efficiency of the company. Thus, according to Steffen (2020) the primary driver of

WACC that is weighted average cost of capital is cost of equity and the cost of debt. In addition

to this, there are many different types of factors which can affect the WACC to a great extent.

This is particularly because of the reason that cost is being defined by the market rate and it is

not necessary that the cost of capital is static because there are many changes within the external

environment.

In addition to this cost, another key driver of WACC is that economic condition. This is

also a driver of WACC because in case the economic condition is not good and there is increase

in interest rate. As per the views of Vartiainen and et.al., (2020) then this will result in increase

in cost of debt which in turn will increase overall cost of capital for the company. Hence, it is

necessary for the both the companies that is Accenture and Ameriprise Financial to take of the

economic condition before finalising the balance of both equity and debt. In case the interest rate

will be low then companies can take more debt at lower rate and this will result in increase in

balance of debt within the company.

Along with this another driver of cost of capital is the market condition that is inflation of

recession. In case there is inflation then all the working of the company will be affected as

everything will be having high cost. Thus, for getting successful both the companies need to

analyse all the drivers in better way so that proper decision can be taken.

CONCLUSION

From the above report it has been concluded that by forming a portfolio of stock

belonging from different sectors, a risk averse investor can be benefitted from maximum returns

and minimum risks. In this report, it has been evaluated that how by equally weighing stocks

from different sectors higher returns could be generated at a lower acceptable risk as against

investing individually in single stocks which results in comparatively higher risks and lower

returns as a whole. Also, it has been evaluated that how by optimally weighing different stocks in

the portfolio higher returns could be ensured at a minimum possible risks through following risk

return trade off principle of investment. At last, equity cost of capital has been estimated for the

stocks of two different sector that is ACN from IT sector and AMP from financial sector which

are listed companies on S&P 500 index along with discussing various drivers of firm’s WACC.

in cost of debt which in turn will increase overall cost of capital for the company. Hence, it is

necessary for the both the companies that is Accenture and Ameriprise Financial to take of the

economic condition before finalising the balance of both equity and debt. In case the interest rate

will be low then companies can take more debt at lower rate and this will result in increase in

balance of debt within the company.

Along with this another driver of cost of capital is the market condition that is inflation of

recession. In case there is inflation then all the working of the company will be affected as

everything will be having high cost. Thus, for getting successful both the companies need to

analyse all the drivers in better way so that proper decision can be taken.

CONCLUSION

From the above report it has been concluded that by forming a portfolio of stock

belonging from different sectors, a risk averse investor can be benefitted from maximum returns

and minimum risks. In this report, it has been evaluated that how by equally weighing stocks

from different sectors higher returns could be generated at a lower acceptable risk as against

investing individually in single stocks which results in comparatively higher risks and lower

returns as a whole. Also, it has been evaluated that how by optimally weighing different stocks in

the portfolio higher returns could be ensured at a minimum possible risks through following risk

return trade off principle of investment. At last, equity cost of capital has been estimated for the

stocks of two different sector that is ACN from IT sector and AMP from financial sector which

are listed companies on S&P 500 index along with discussing various drivers of firm’s WACC.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Balcilar, M., Ozdemir, Z. A. and Ozdemir, H., 2021. Dynamic return and volatility spillovers

among S&P 500, crude oil, and gold. International Journal of Finance & Economics, 26(1),

pp.153-170.

Den Houting, J. and Pellicano, E., 2019. A portfolio analysis of autism research funding in

Australia, 2008–2017. Journal of autism and developmental disorders, 49(11),

pp.4400-4408.

Fang, M., Tan, K. S. and Wirjanto, T. S., 2019. Sustainable portfolio management under climate

change. Journal of Sustainable Finance & Investment, 9(1), pp.45-67.

Gulliksson, M. and Mazur, S., 2020. An iterative approach to ill-conditioned optimal portfolio

selection. Computational Economics, 56(4), pp.773-794.

Klein, T., Thu, H. P. and Walther, T., 2018. Bitcoin is not the New Gold–A comparison of

volatility, correlation, and portfolio performance. International Review of Financial

Analysis, 59, pp.105-116.

Li, Y., and et.al., 2019. Portfolio optimization based on network topology. Physica A: Statistical

Mechanics and its Applications, 515, pp.671-681.

Narayan, S. and Rehman, M. U., 2020. International portfolio strategies and opportunities: the

case of the US, Japan and Asia. Finance Research Letters, 37, p.101358.

Narayan, S. W. and Rehman, M. U., 2018. Portfolio diversification opportunities within

emerging and frontier stock markets: evidence from ten Asian countries. Buletin

Ekonomi Moneter dan Perbankan, 21(1), pp.1-22.

Steffen, B., 2020. Estimating the cost of capital for renewable energy projects. Energy

Economics. 88. p.104783.

Vamvakaris, M. D., Pantelous, A. A. and Zuev, K. M., 2018. Time series analysis of S&P 500

index: A horizontal visibility graph approach. Physica A: Statistical Mechanics and its

Applications, 497, pp.41-51.

Balcilar, M., Ozdemir, Z. A. and Ozdemir, H., 2021. Dynamic return and volatility spillovers

among S&P 500, crude oil, and gold. International Journal of Finance & Economics, 26(1),

pp.153-170.

Den Houting, J. and Pellicano, E., 2019. A portfolio analysis of autism research funding in

Australia, 2008–2017. Journal of autism and developmental disorders, 49(11),

pp.4400-4408.

Fang, M., Tan, K. S. and Wirjanto, T. S., 2019. Sustainable portfolio management under climate

change. Journal of Sustainable Finance & Investment, 9(1), pp.45-67.

Gulliksson, M. and Mazur, S., 2020. An iterative approach to ill-conditioned optimal portfolio

selection. Computational Economics, 56(4), pp.773-794.

Klein, T., Thu, H. P. and Walther, T., 2018. Bitcoin is not the New Gold–A comparison of

volatility, correlation, and portfolio performance. International Review of Financial

Analysis, 59, pp.105-116.

Li, Y., and et.al., 2019. Portfolio optimization based on network topology. Physica A: Statistical

Mechanics and its Applications, 515, pp.671-681.

Narayan, S. and Rehman, M. U., 2020. International portfolio strategies and opportunities: the

case of the US, Japan and Asia. Finance Research Letters, 37, p.101358.

Narayan, S. W. and Rehman, M. U., 2018. Portfolio diversification opportunities within

emerging and frontier stock markets: evidence from ten Asian countries. Buletin

Ekonomi Moneter dan Perbankan, 21(1), pp.1-22.

Steffen, B., 2020. Estimating the cost of capital for renewable energy projects. Energy

Economics. 88. p.104783.

Vamvakaris, M. D., Pantelous, A. A. and Zuev, K. M., 2018. Time series analysis of S&P 500

index: A horizontal visibility graph approach. Physica A: Statistical Mechanics and its

Applications, 497, pp.41-51.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Vartiainen, E., and et.al., 2020. Impact of weighted average cost of capital, capital expenditure,

and other parameters on future utility‐scale PV levelised cost of electricity. Progress in

photovoltaics: research and applications. 28(6). pp.439-453.

and other parameters on future utility‐scale PV levelised cost of electricity. Progress in

photovoltaics: research and applications. 28(6). pp.439-453.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.