Application of Portfolio Theory and Empirical Estimation Analysis

VerifiedAdded on 2020/06/06

|16

|1701

|94

Project

AI Summary

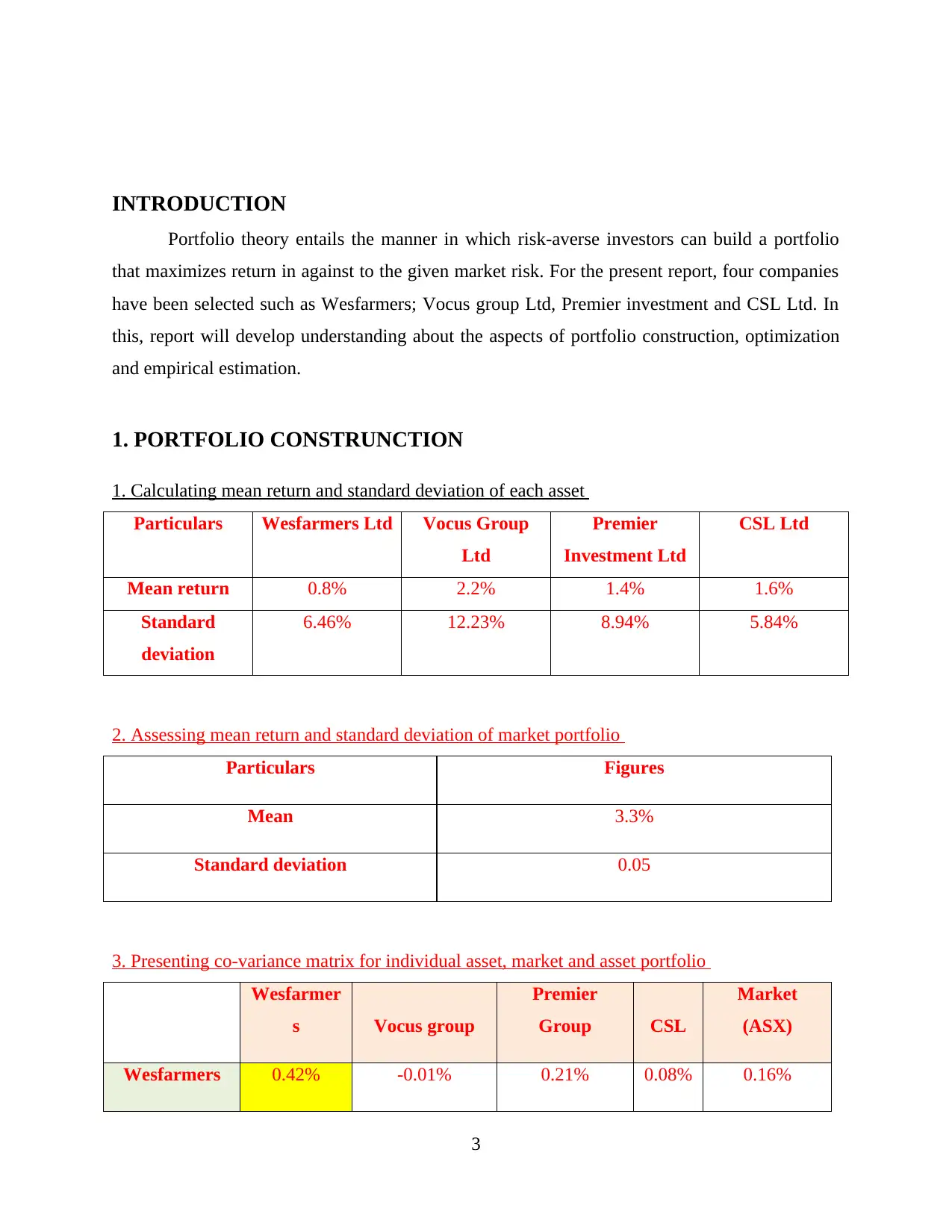

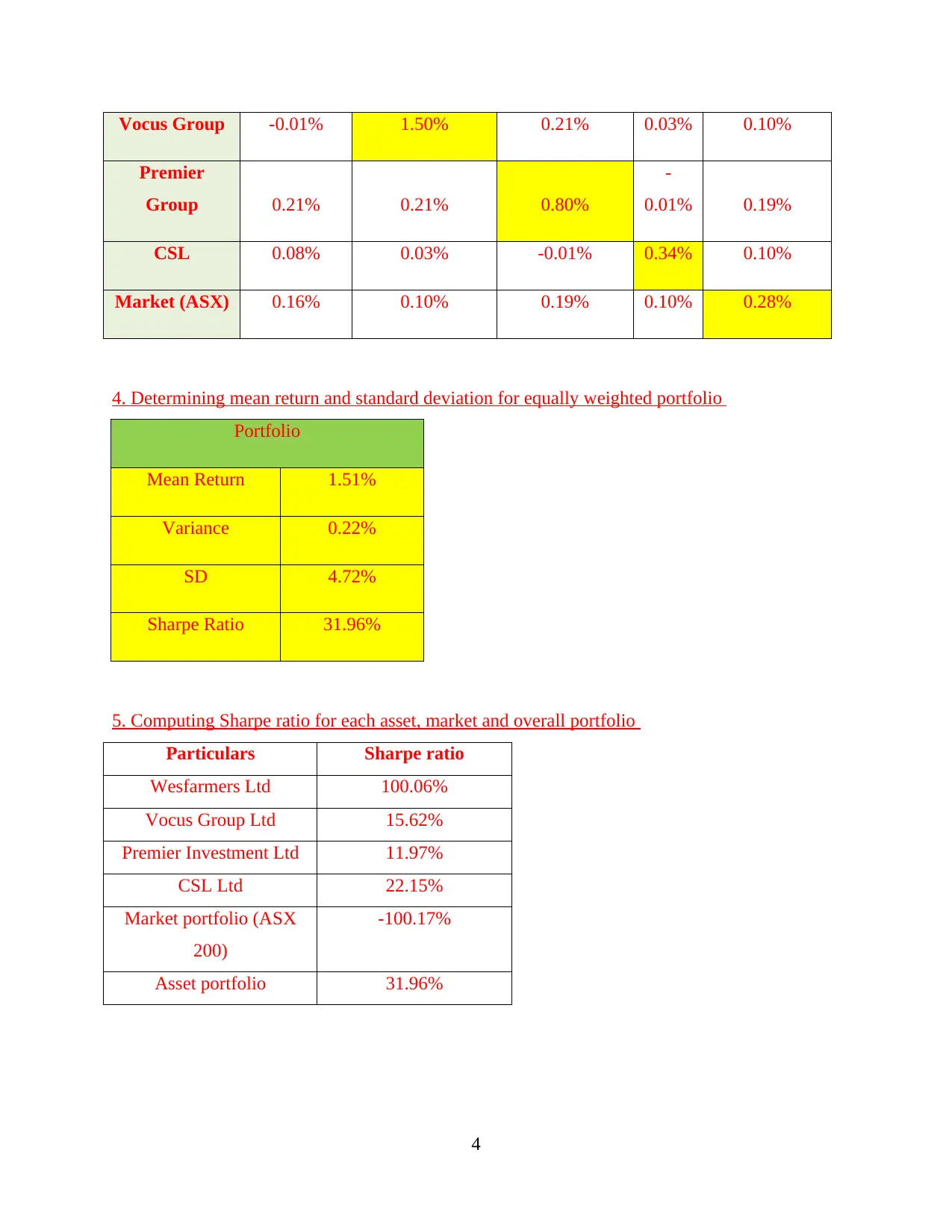

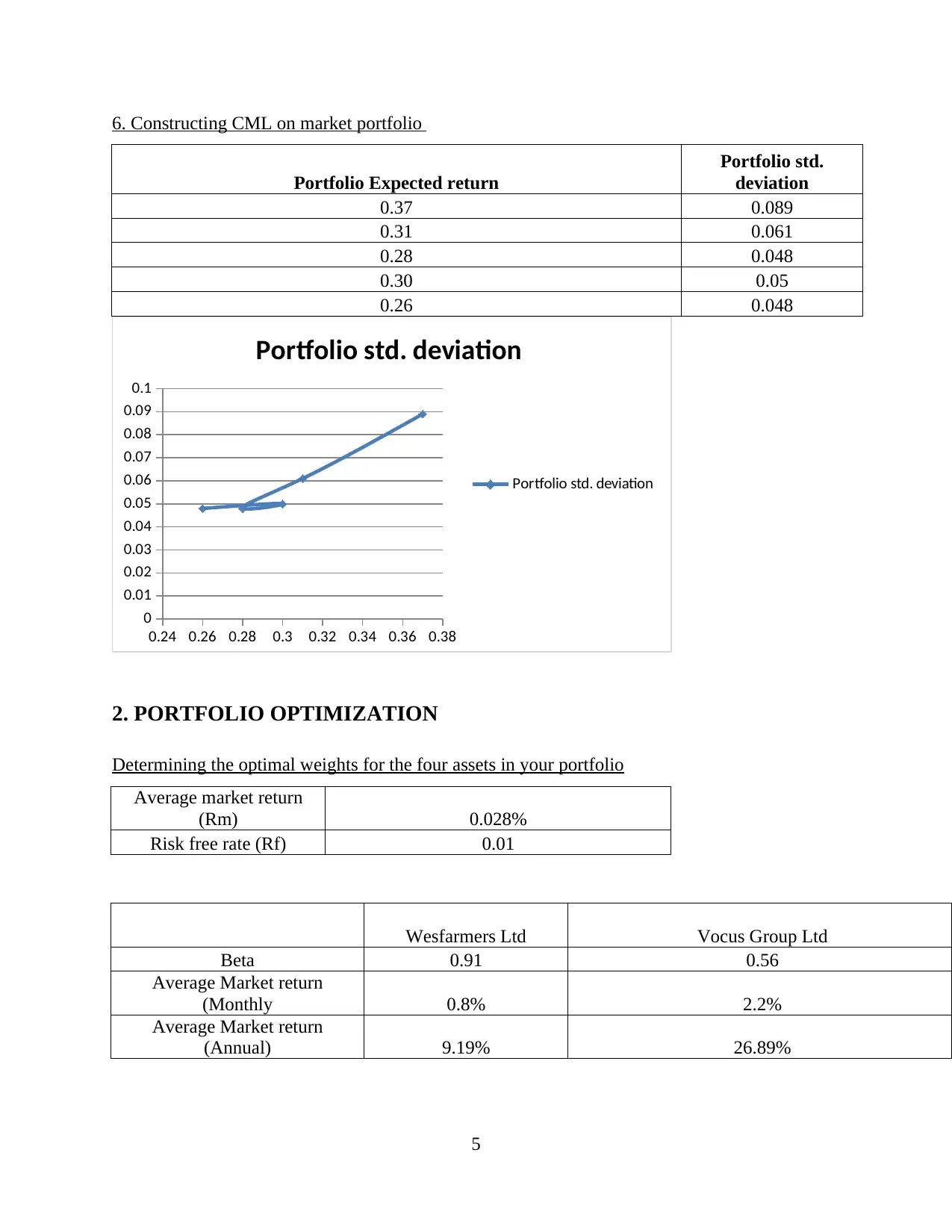

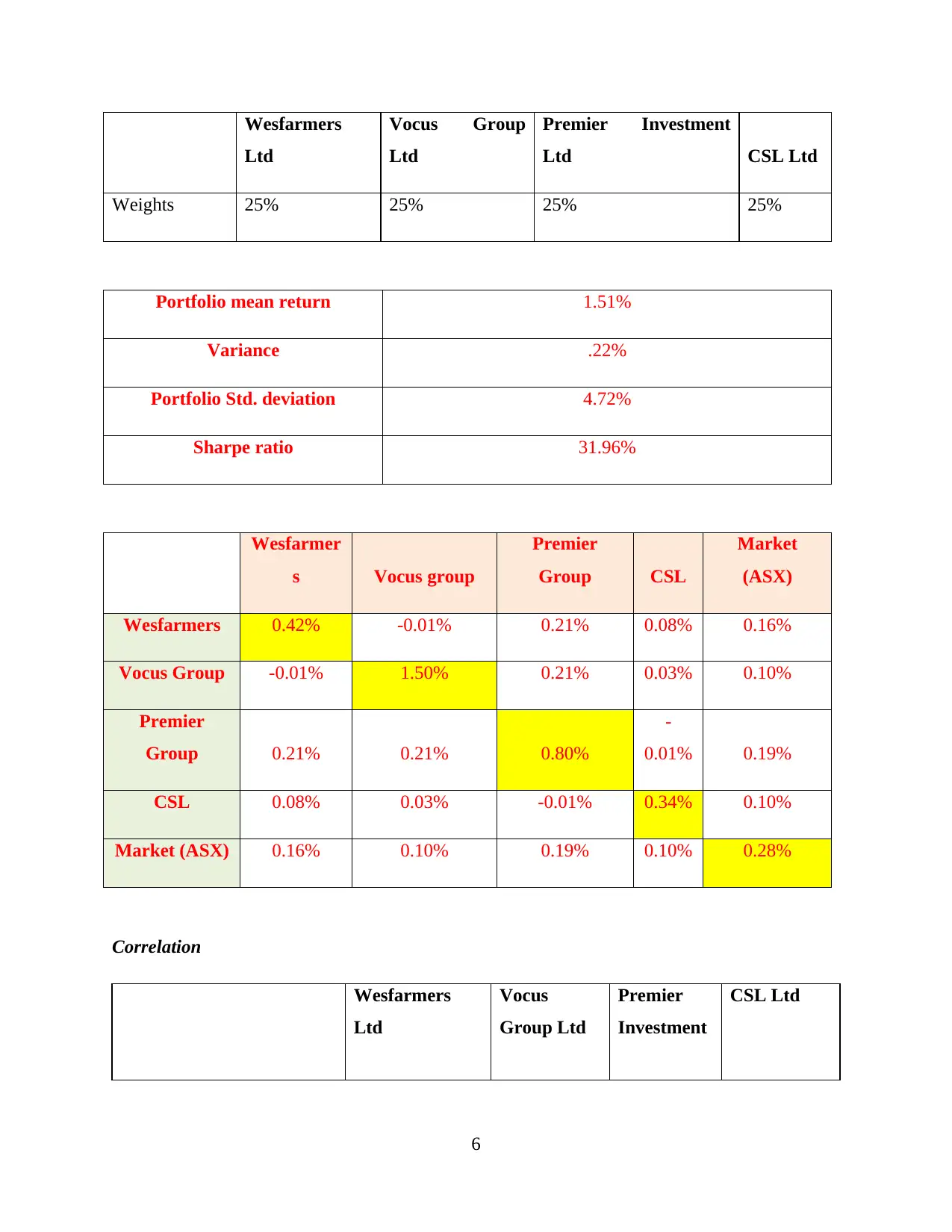

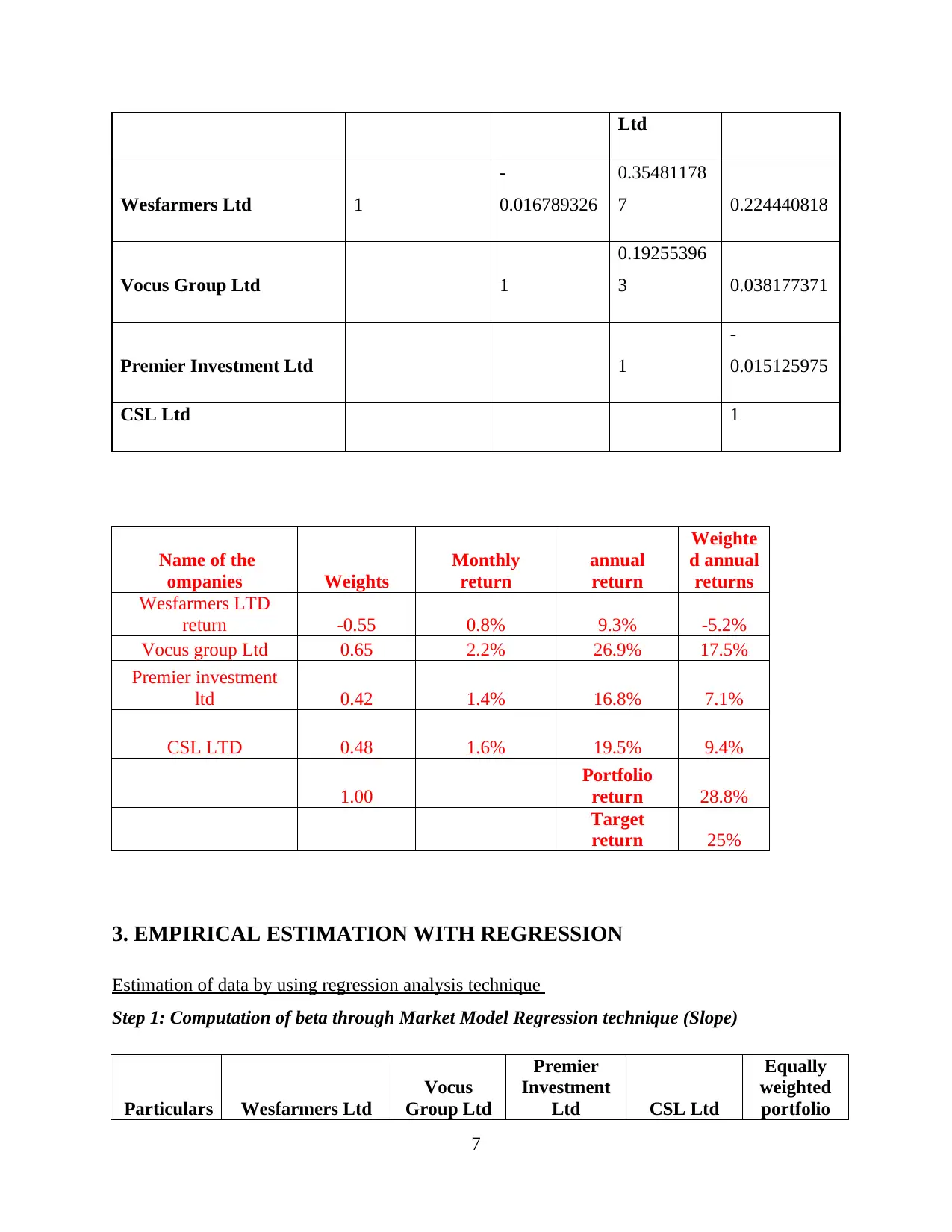

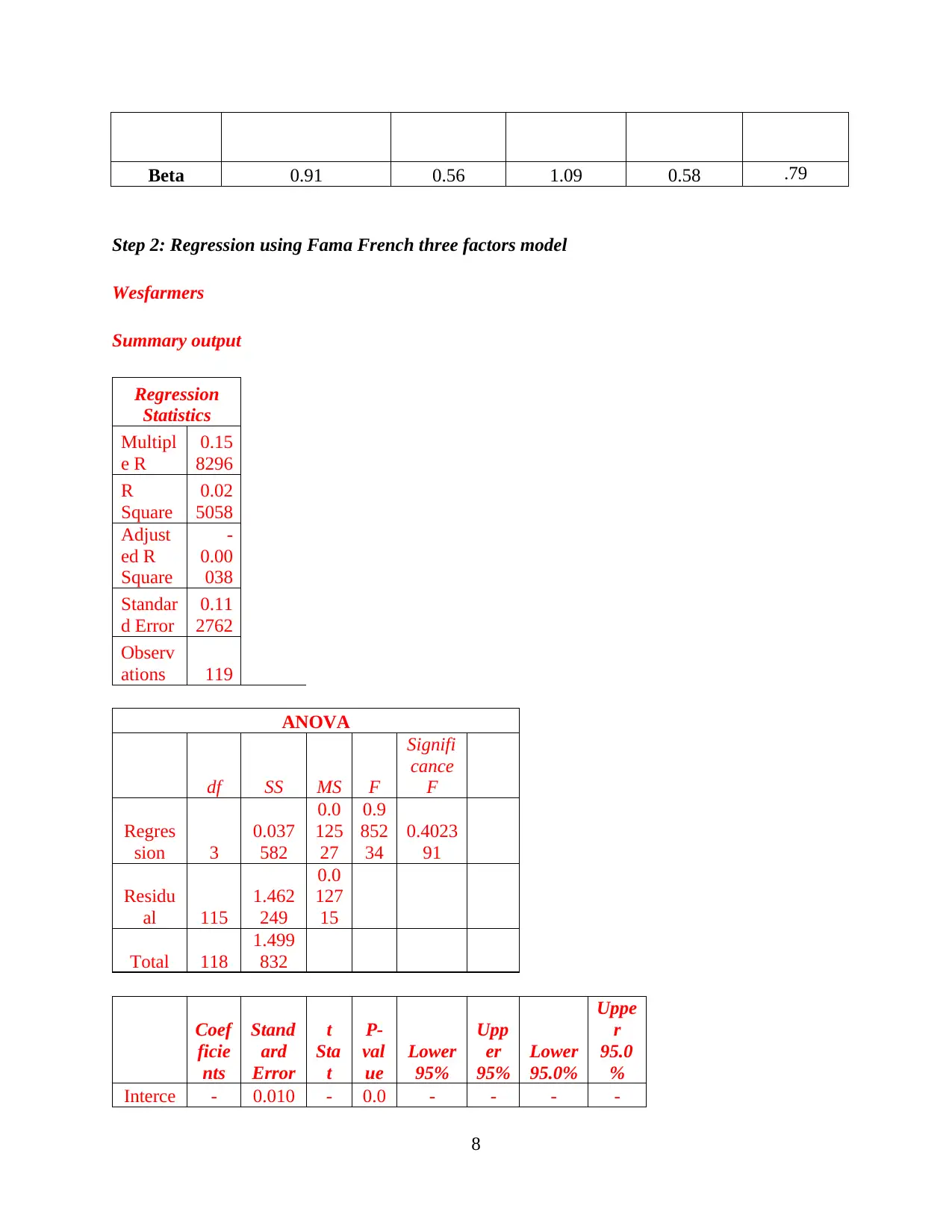

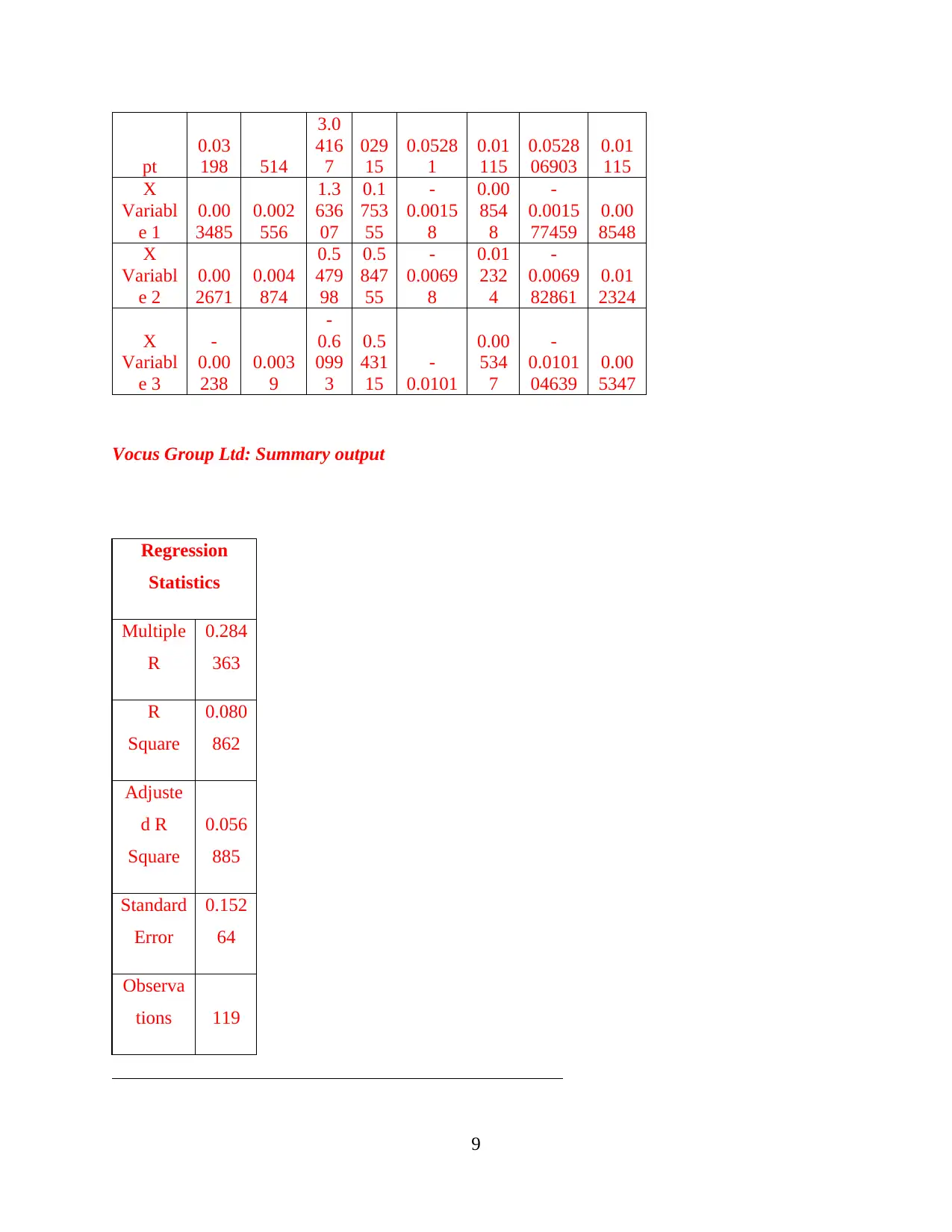

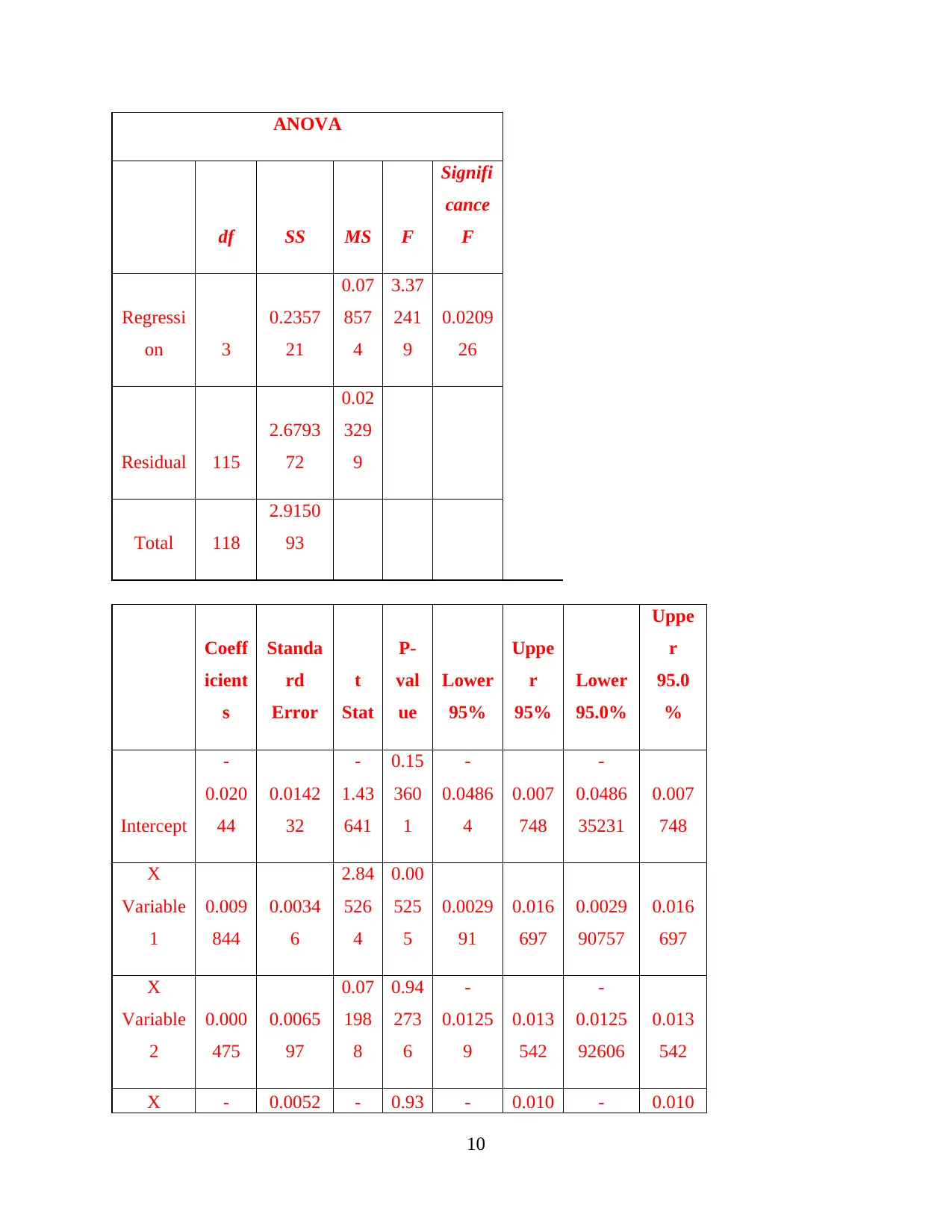

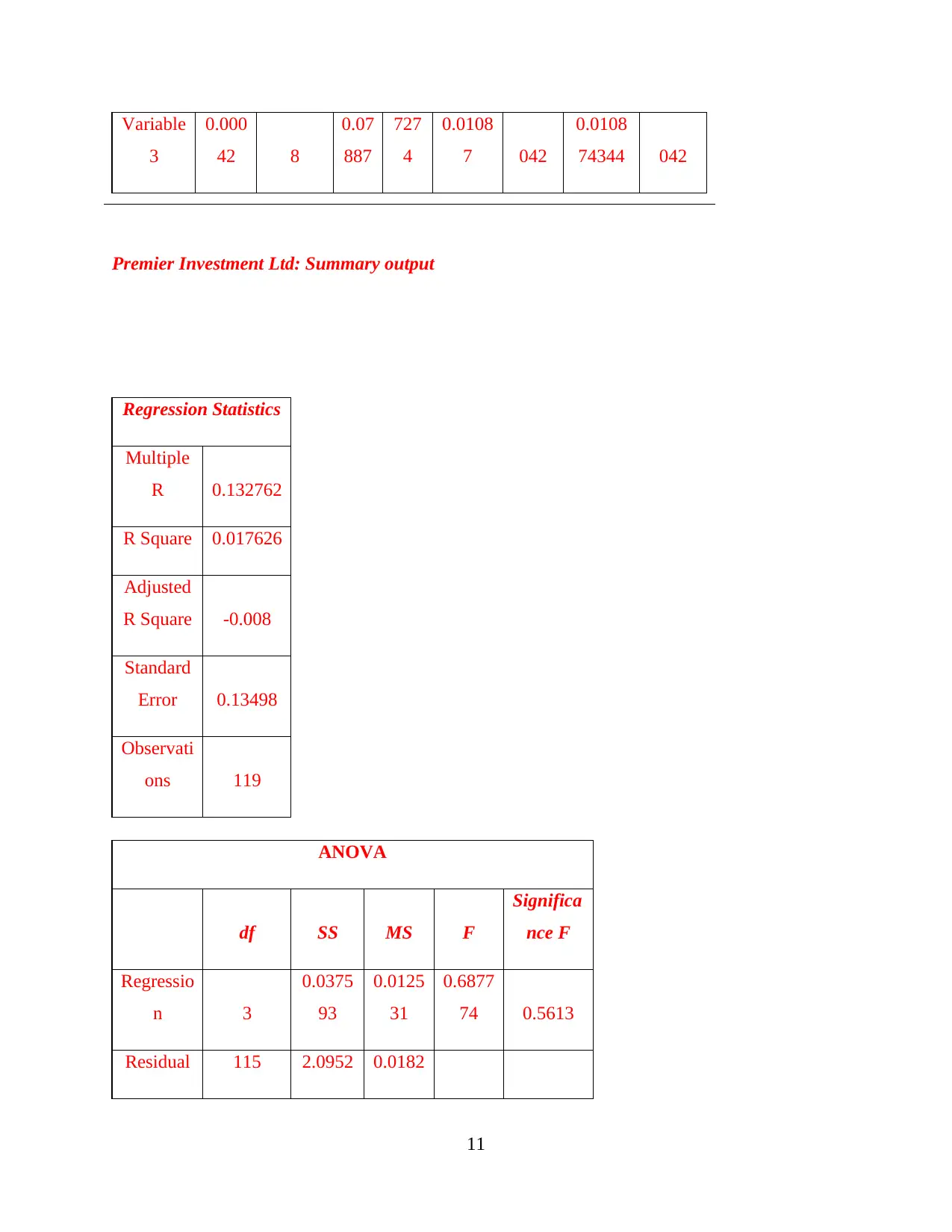

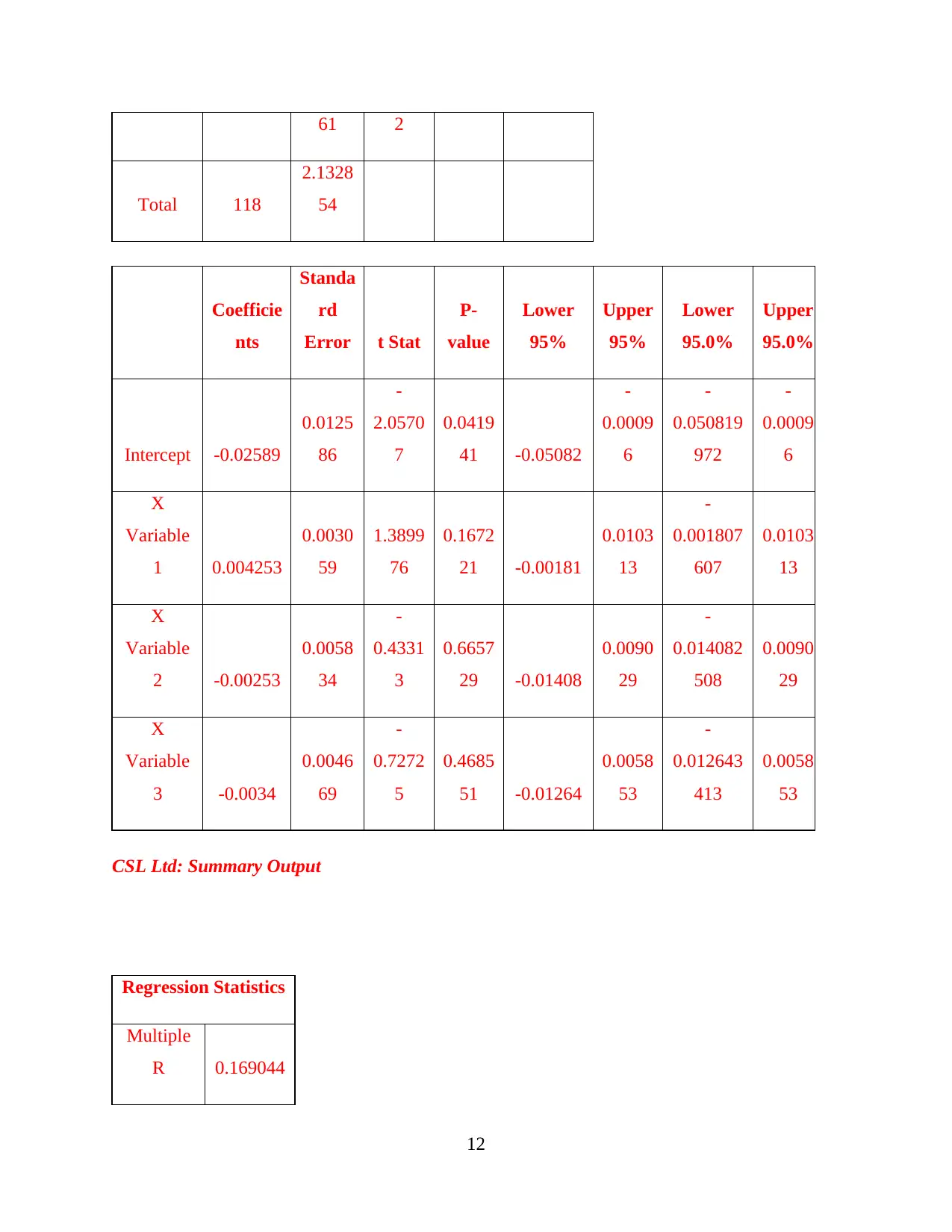

This project delves into the application of portfolio theory, encompassing portfolio construction, optimization, and empirical estimation techniques. The project begins with constructing a portfolio, calculating mean returns, standard deviations, and Sharpe ratios for individual assets, a market portfolio, and an equally weighted portfolio. It then presents a covariance matrix for the assets. The project proceeds to portfolio optimization, determining optimal weights for four selected assets using beta and market return data. Finally, it utilizes regression analysis to empirically estimate data using the market model and Fama-French three-factor model to compute beta values and assess risk. The evaluation section interprets the findings, highlighting the performance of different assets and the implications of portfolio optimization and regression results. The conclusion summarizes the key findings, emphasizing the importance of Vocus Group Ltd in maximizing returns and the significance of the capital market line.

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.