Epeus Portfolio Management: AFCP8001 Assignment Report

VerifiedAdded on 2022/08/14

|16

|2019

|11

Report

AI Summary

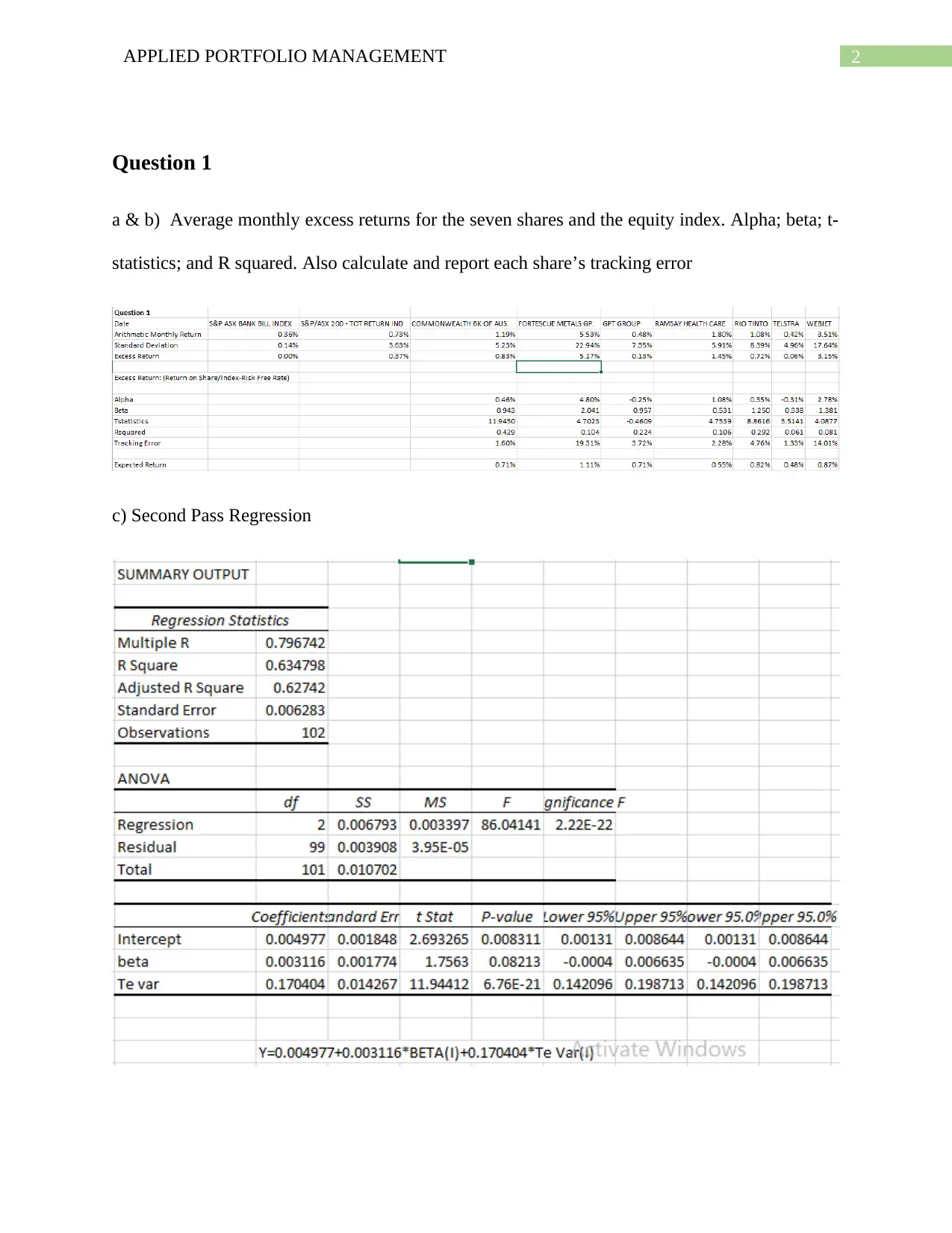

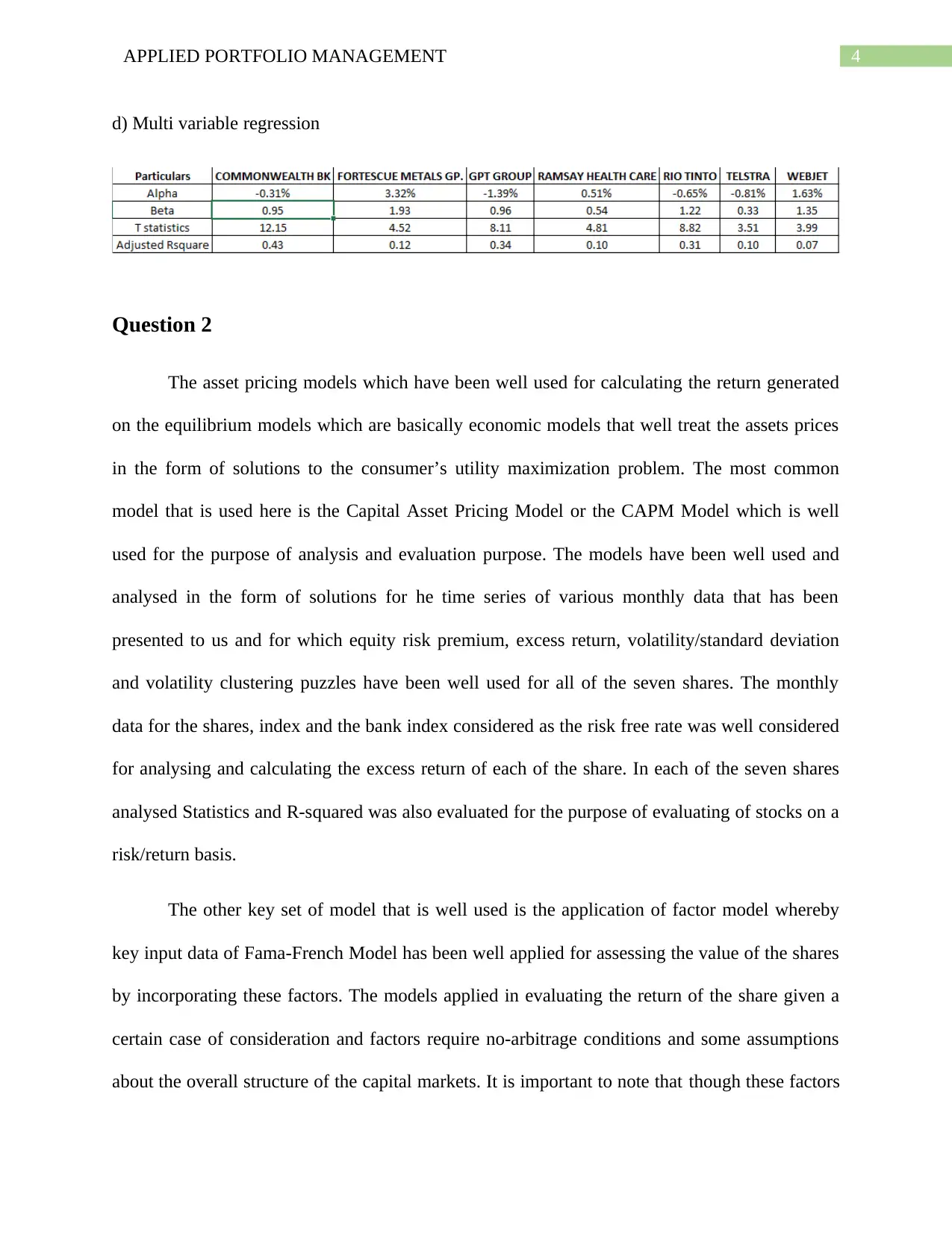

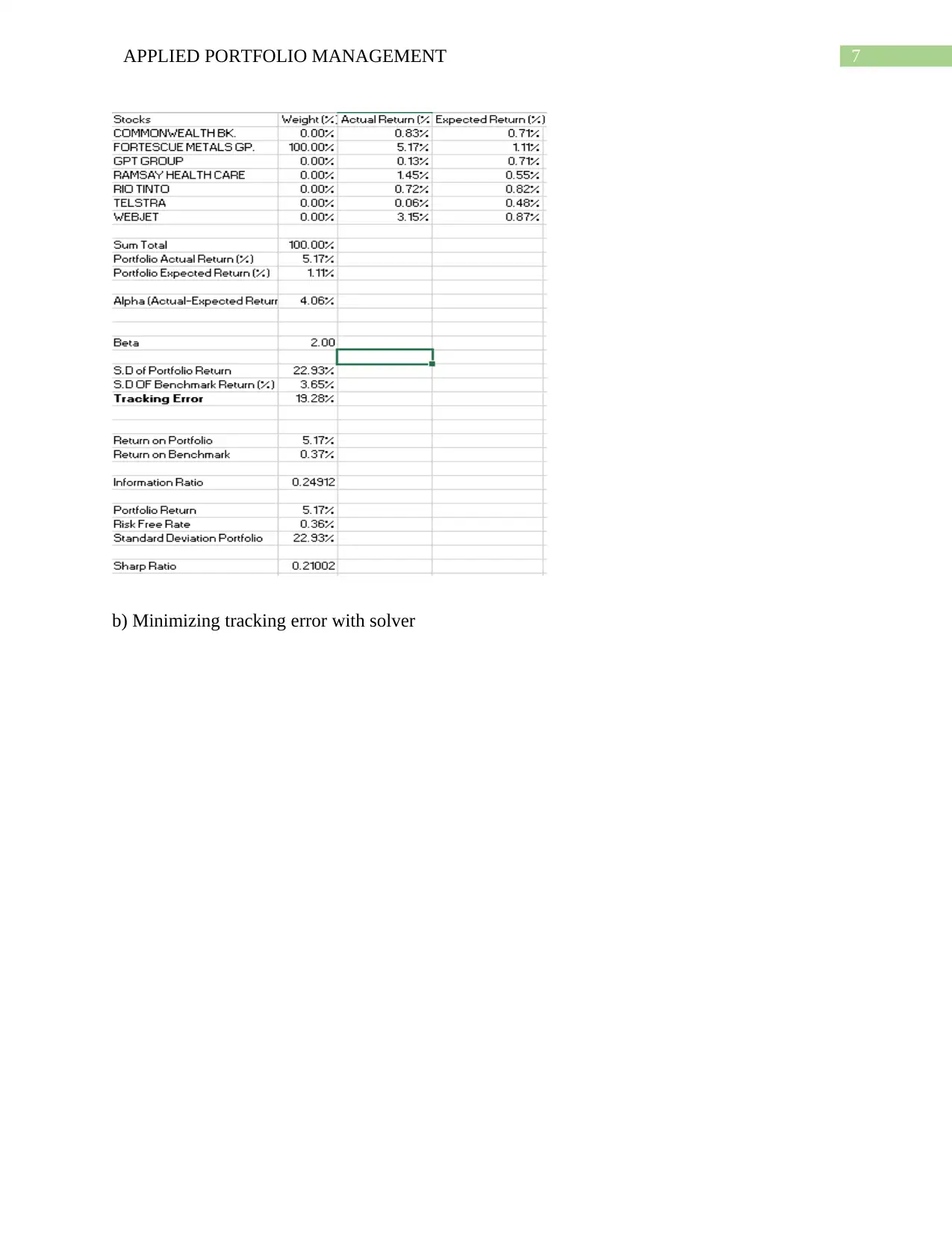

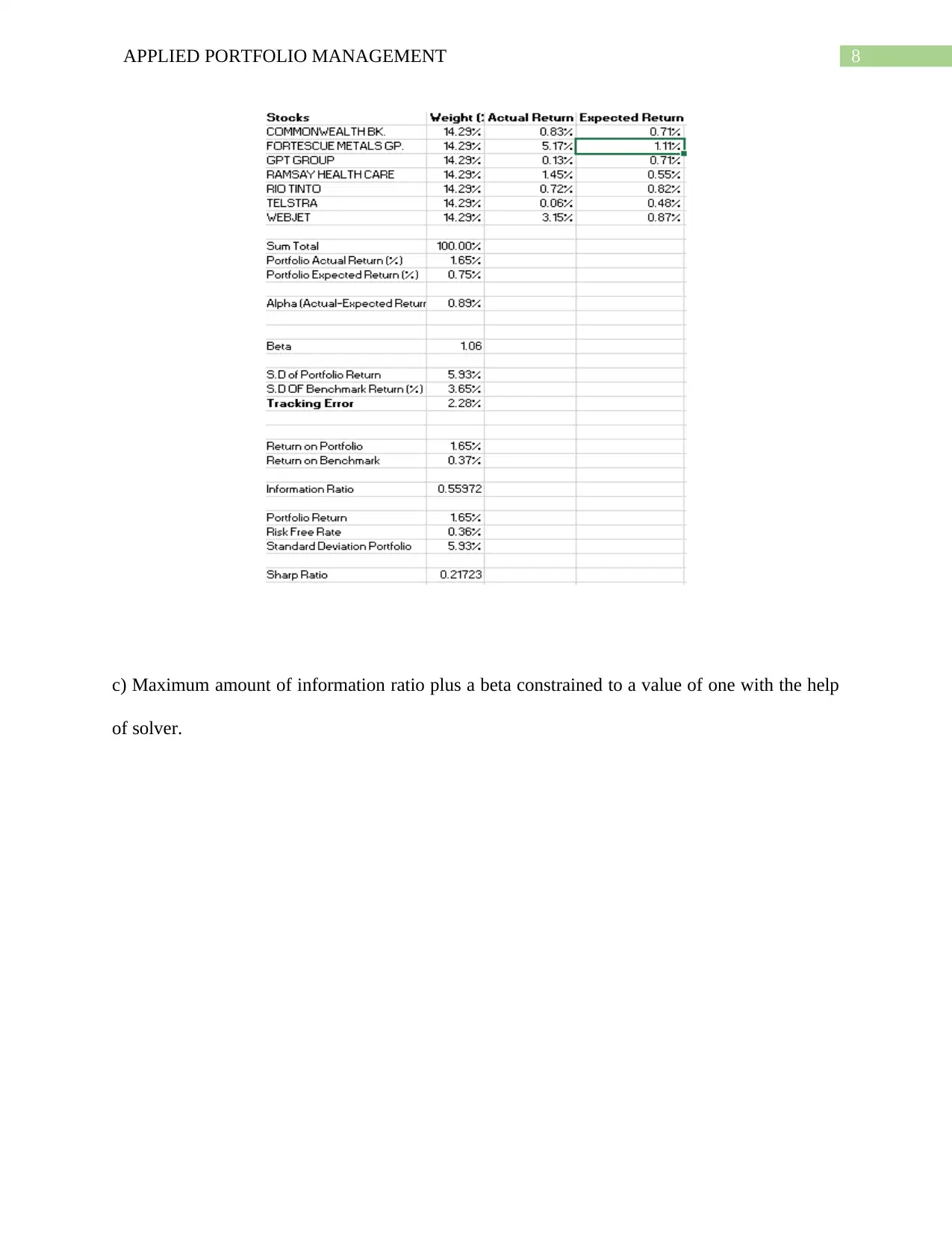

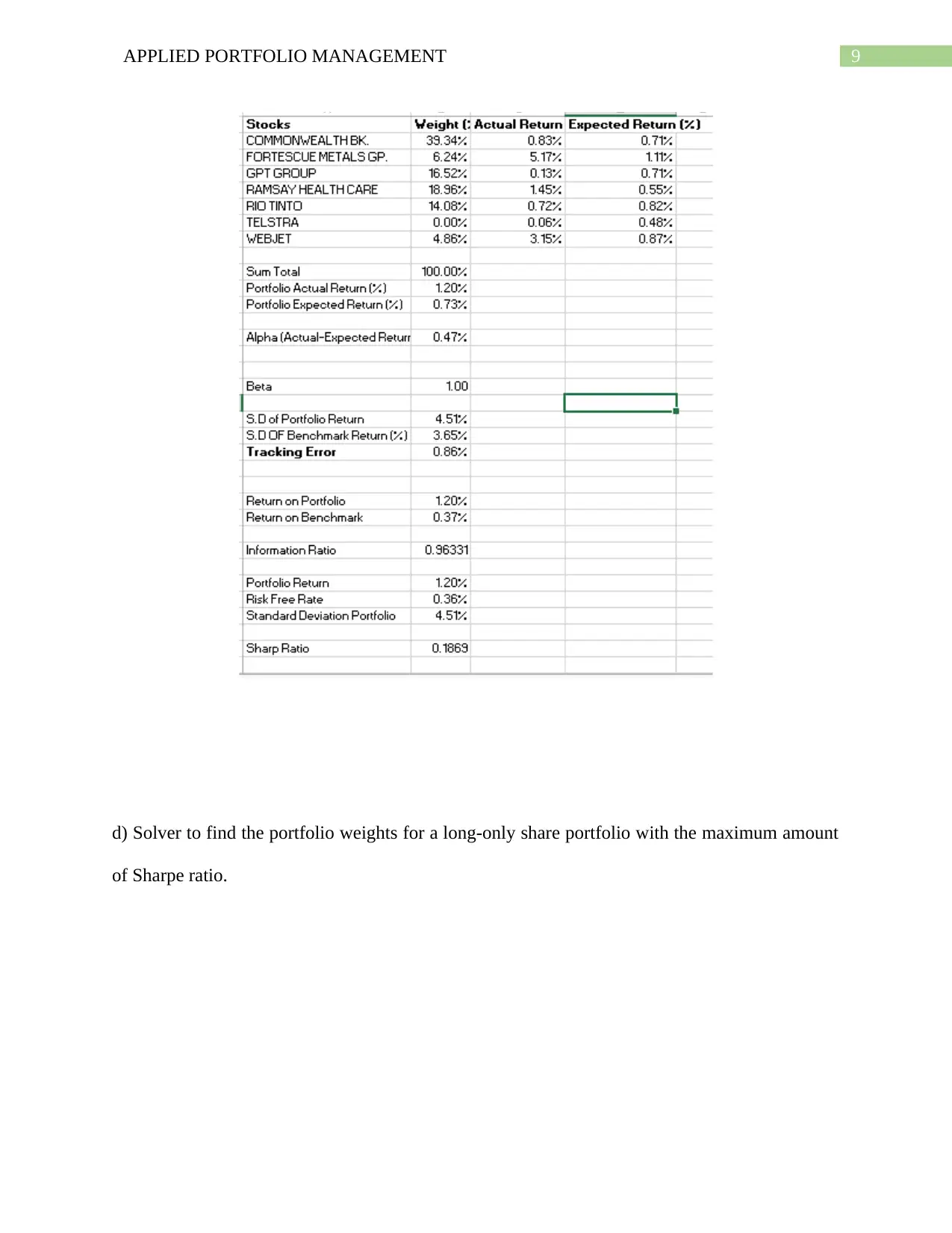

This report provides a comprehensive analysis of portfolio management principles, focusing on asset pricing models, multifactor models, and the application of robo-advisors. The report begins with an examination of average monthly excess returns, alpha, beta, and tracking error calculations for seven shares and an equity index, followed by a discussion of asset pricing models, including the Capital Asset Pricing Model (CAPM) and factor models. The report then delves into the application of multifactor models, outlining their use by investment managers and the different categories of these models, including macroeconomic, fundamental, and statistical models. The report further explores the use of Solver to optimize portfolios by maximizing alpha, minimizing tracking error, maximizing the information ratio with beta constraints, and maximizing the Sharpe ratio. Additionally, the report assesses the performance of different portfolios, recommending the best-performing portfolio based on information ratio and diversification benefits. The report also includes an analysis of market data, calculating Sharpe ratios and discussing the Capital Allocation Line and optimal risky portfolio. Finally, the report examines the role of robo-advisors in investment management, their benefits, and their suitability for firms like Epeus Portfolio Management. The report concludes by providing references to support the analysis and findings.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.