Finance Assignment: Risk and Return Analysis and Portfolio Management

VerifiedAdded on 2020/05/08

|9

|1343

|131

Homework Assignment

AI Summary

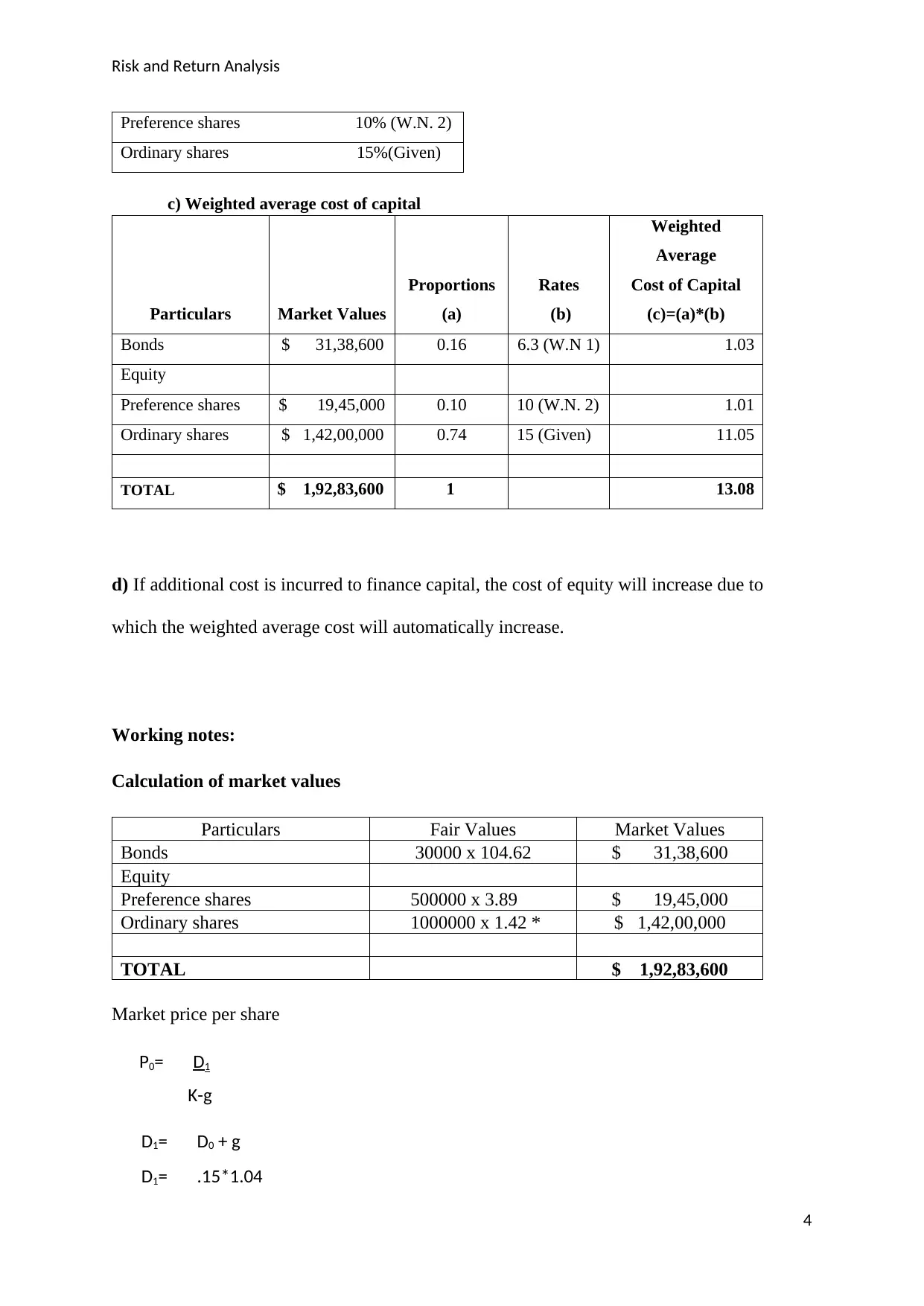

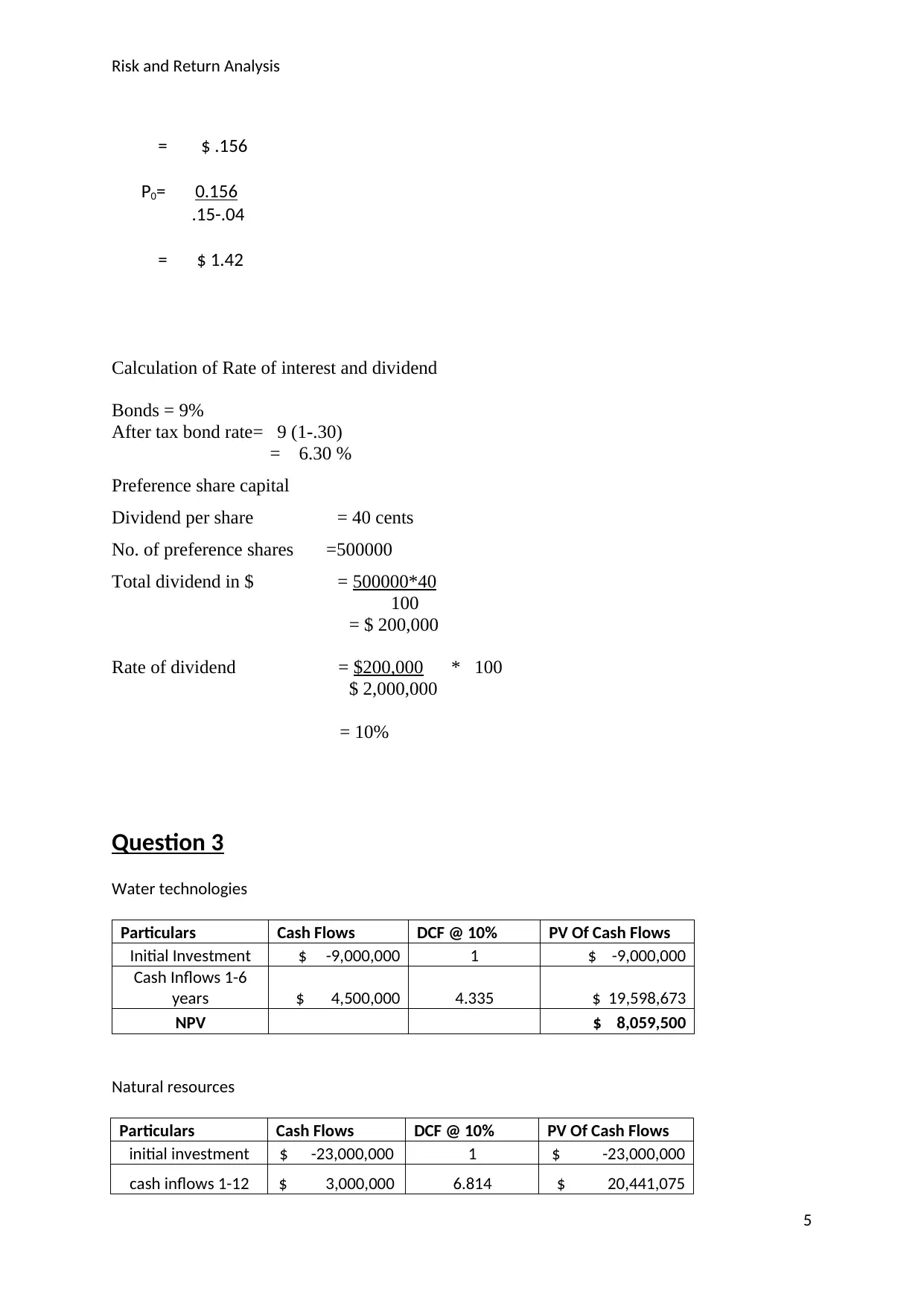

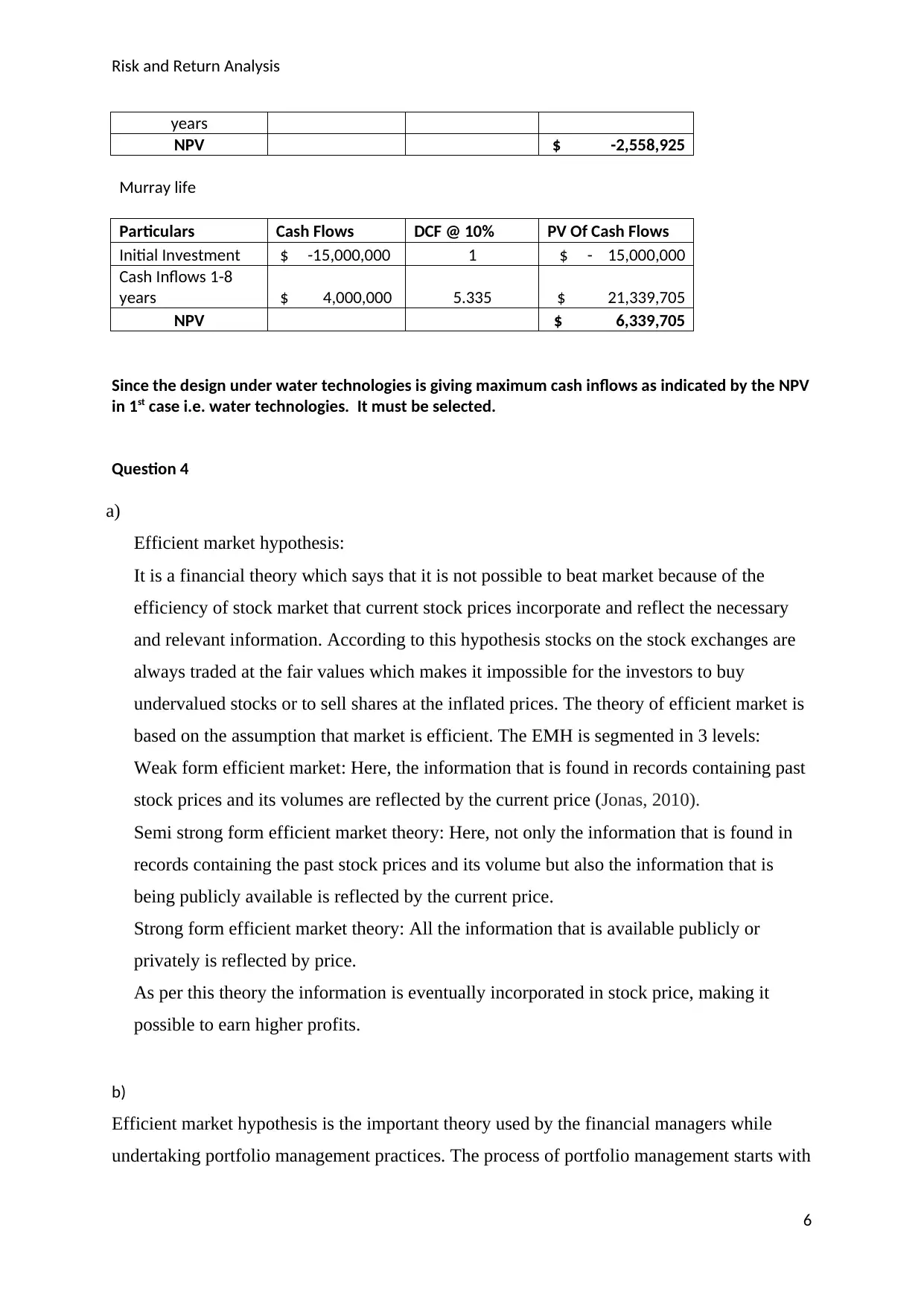

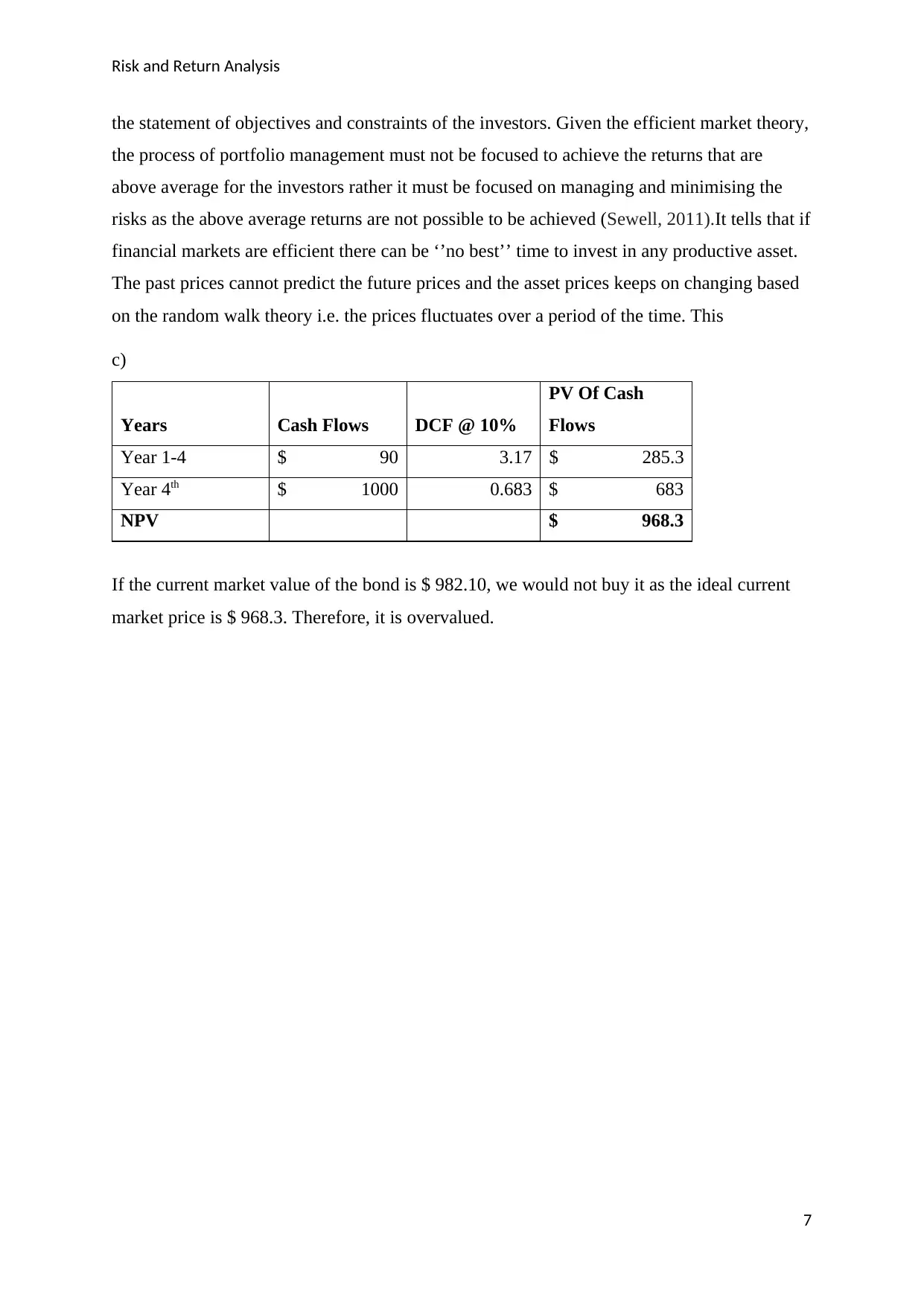

This finance assignment presents a comprehensive analysis of risk and return, covering various aspects of portfolio management and investment strategies. The assignment begins with a calculation of historical returns, standard deviation, and average return over several years, followed by an analysis of expected return and standard deviation under different probability scenarios. The Capital Asset Pricing Model (CAPM) is then employed to evaluate the required rate of return for a project, determining whether the project is a worthwhile investment. The assignment proceeds to calculate the market value proportions and after-tax costs of capital for different sources of finance, including bonds, preference shares, and ordinary shares. The weighted average cost of capital (WACC) is also computed. Furthermore, the assignment involves a Net Present Value (NPV) analysis to evaluate the profitability of different investment projects, such as water technologies, natural resources, and Murray life, to determine which project offers the highest potential returns. Finally, the assignment explores the efficient market hypothesis (EMH), discussing its different forms and implications for portfolio management, and concludes with an analysis of bond valuation.

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.