FIN301: Portfolio Optimization and Efficient Frontier Analysis

VerifiedAdded on 2023/01/20

|4

|815

|42

Homework Assignment

AI Summary

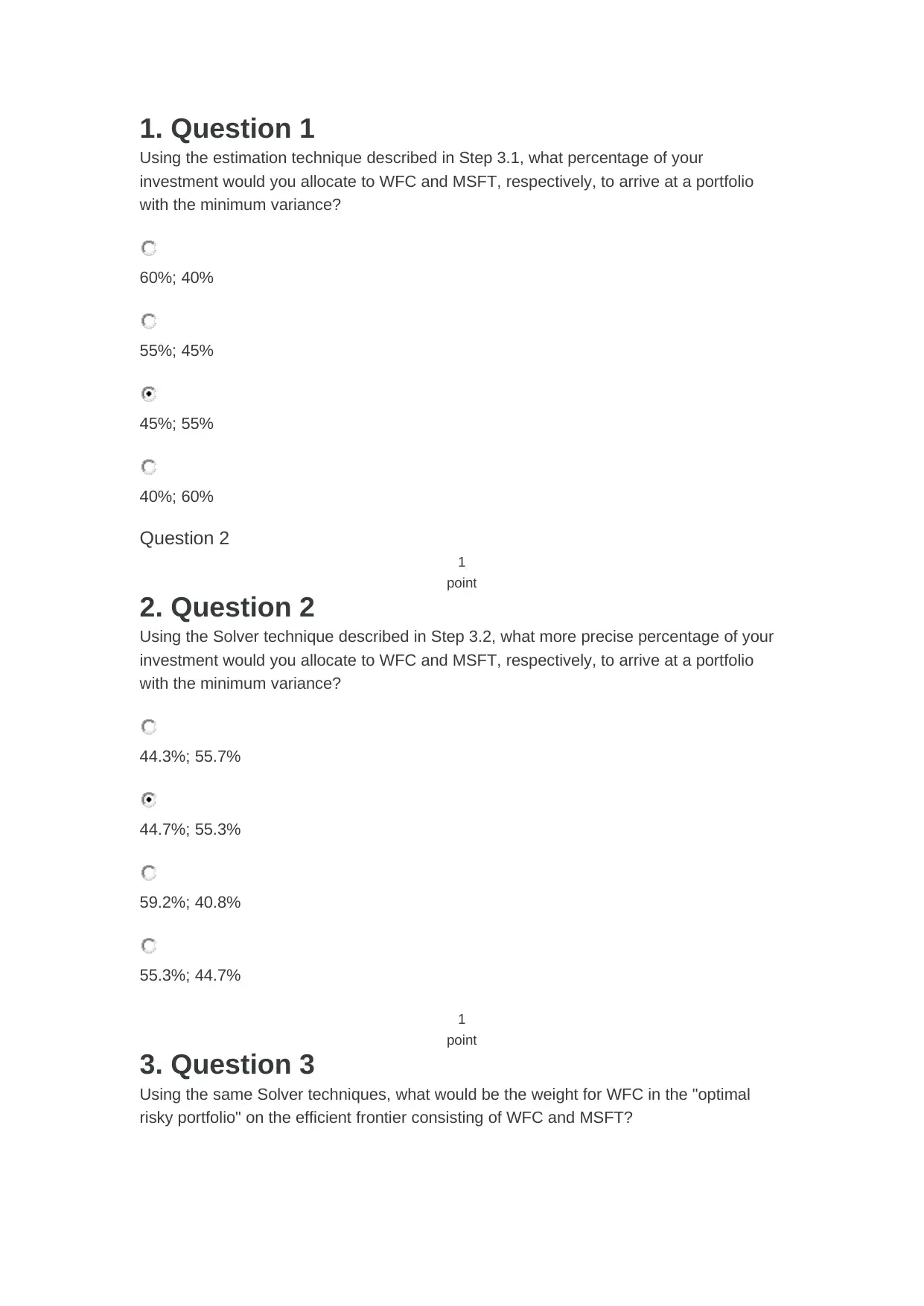

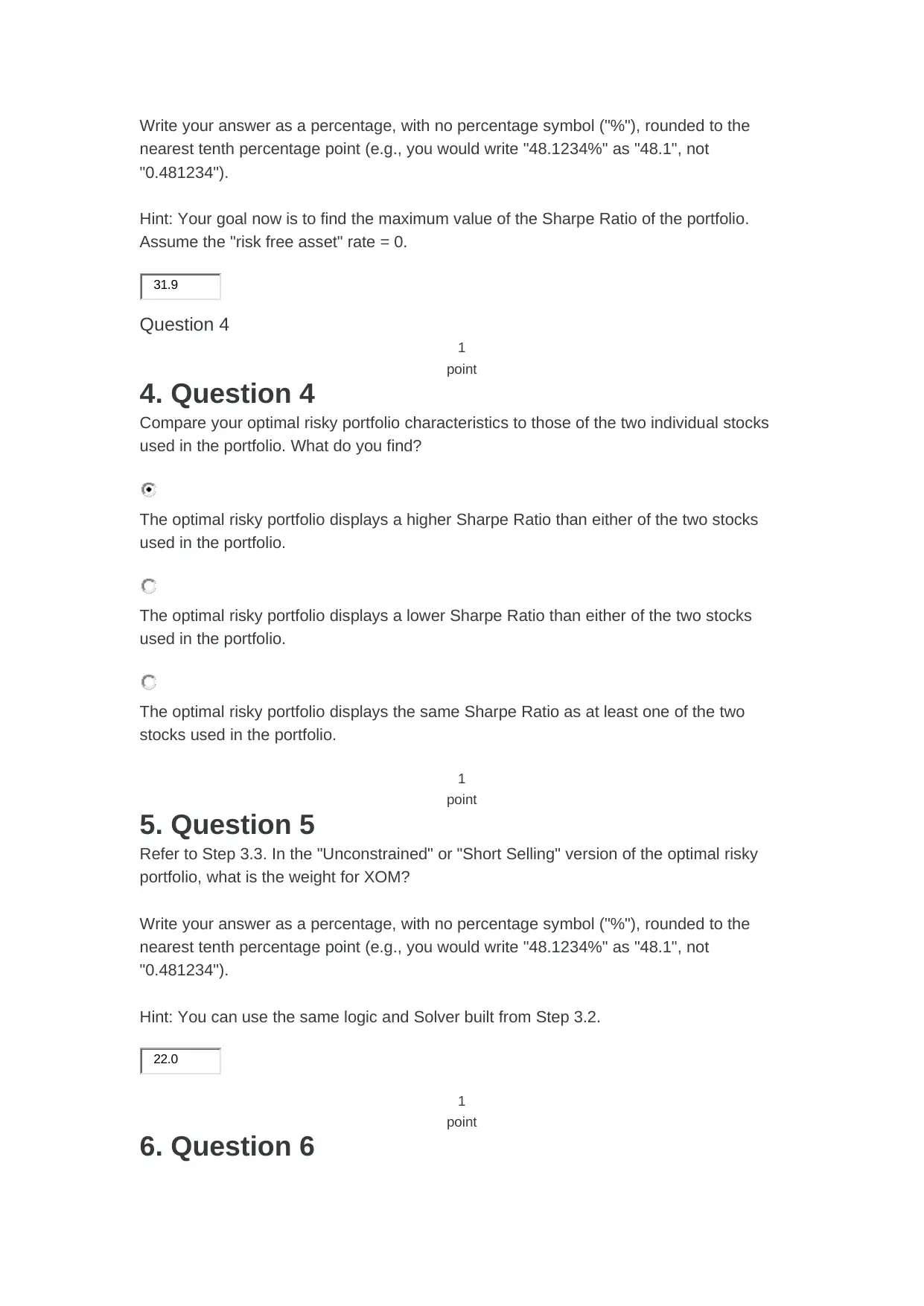

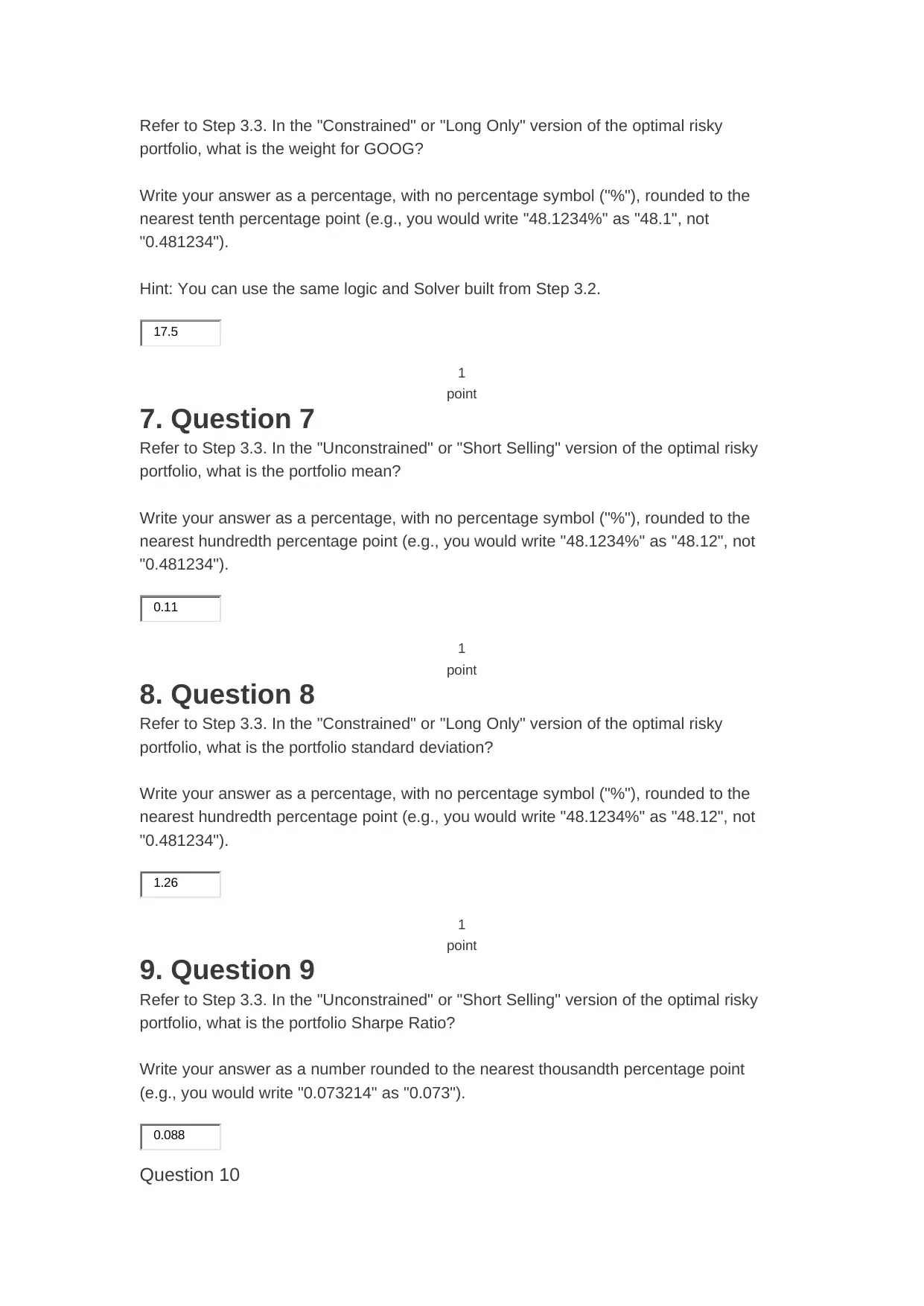

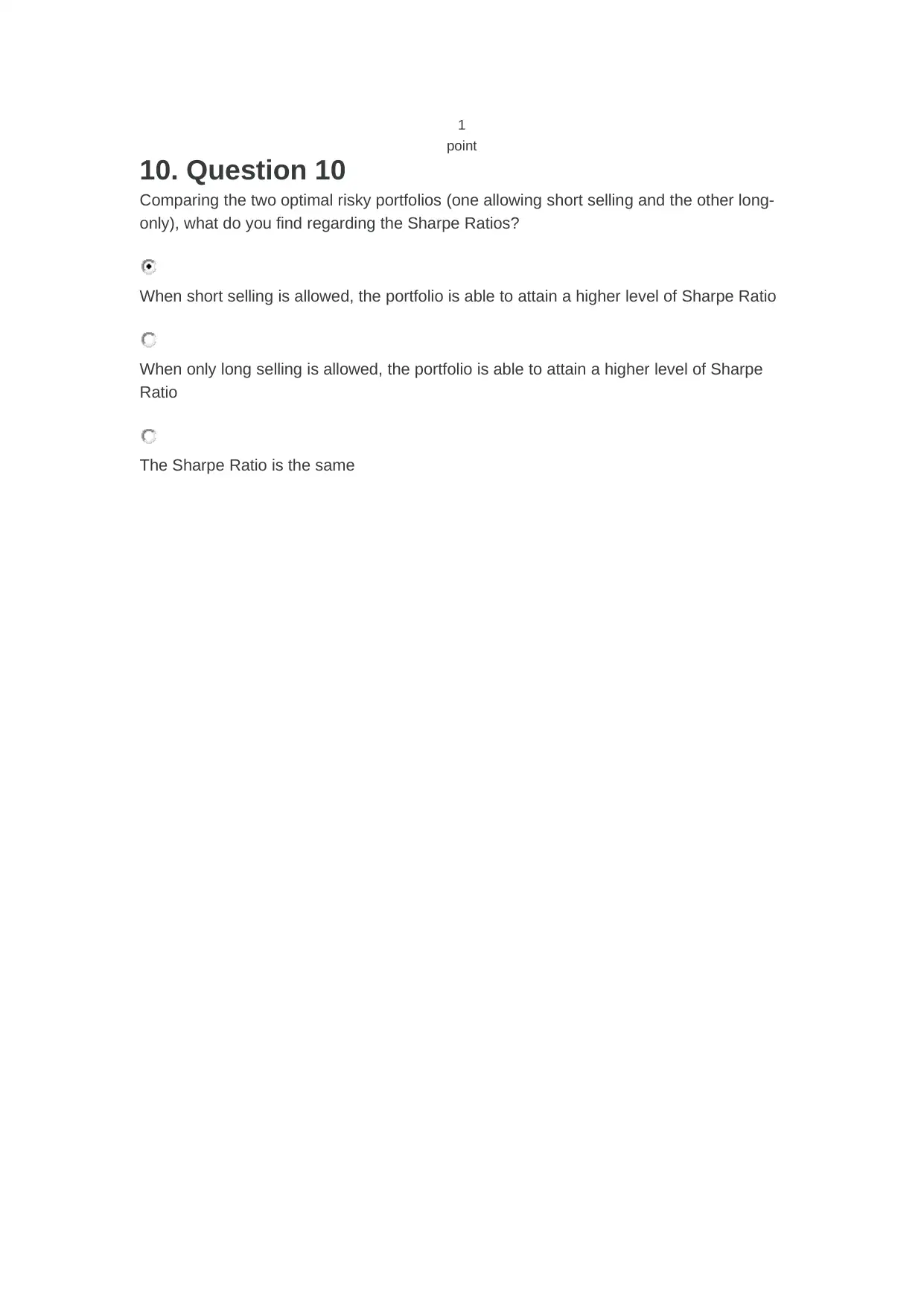

This assignment focuses on portfolio optimization and investment strategies. Students are tasked with applying concepts like minimum variance portfolios, the efficient frontier, and the Sharpe Ratio to construct optimal portfolios using Excel Solver. The assignment explores both two-asset and multi-asset portfolios, considering constraints like long-only investments and short selling. Students analyze the characteristics of different portfolios, comparing their risk and return profiles. The assignment also involves calculating the weights of various assets to achieve the highest Sharpe Ratio and evaluating the impact of short selling on portfolio performance. The student is required to calculate the weight for WFC and MSFT for the minimum variance portfolio, the weight for WFC in the optimal risky portfolio, and the weights of VBTLX and VFIAX to achieve an optimal risky portfolio. The assignment also touches upon the comparison of optimal risky portfolios and the impact of short selling versus long-only strategies.

1 out of 4

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.