Portfolio Management: Options Strategies, Premium & Value Analysis

VerifiedAdded on 2023/05/28

|8

|2134

|293

Homework Assignment

AI Summary

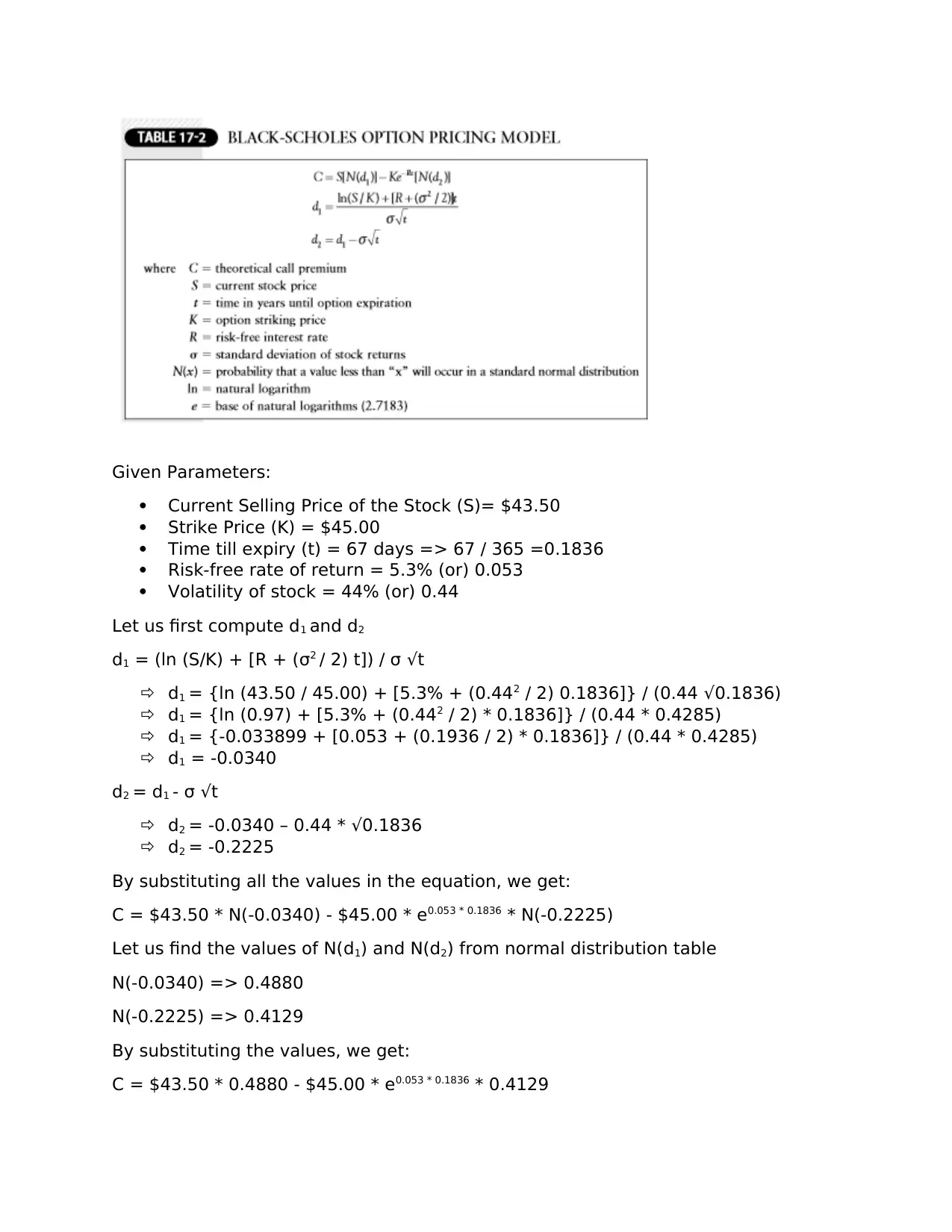

This assignment delves into the intricacies of options trading, contrasting bullish and bearish strategies and examining the components of option premiums. It clarifies the differences between buying a call and writing a put, analyzing the advantages and disadvantages of each approach when one is bullish on a stock. The assignment further dissects option premiums into intrinsic and time value, explaining how these values are determined and their implications for in-the-money and out-of-the-money options. It also presents a comprehensive analysis of options as bets on stock price direction and explores the impact of interest rate changes on option premiums, using the Black-Scholes model for option pricing. Practical problems are solved to illustrate the concepts of time value, intrinsic value, and profit/loss calculations, providing a thorough understanding of options trading dynamics. Desklib offers a variety of resources, including past papers and solved assignments, to aid students in mastering these concepts.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.