Comprehensive Analysis of Portfolio Risk and Return Strategies

VerifiedAdded on 2020/05/08

|8

|1270

|59

Homework Assignment

AI Summary

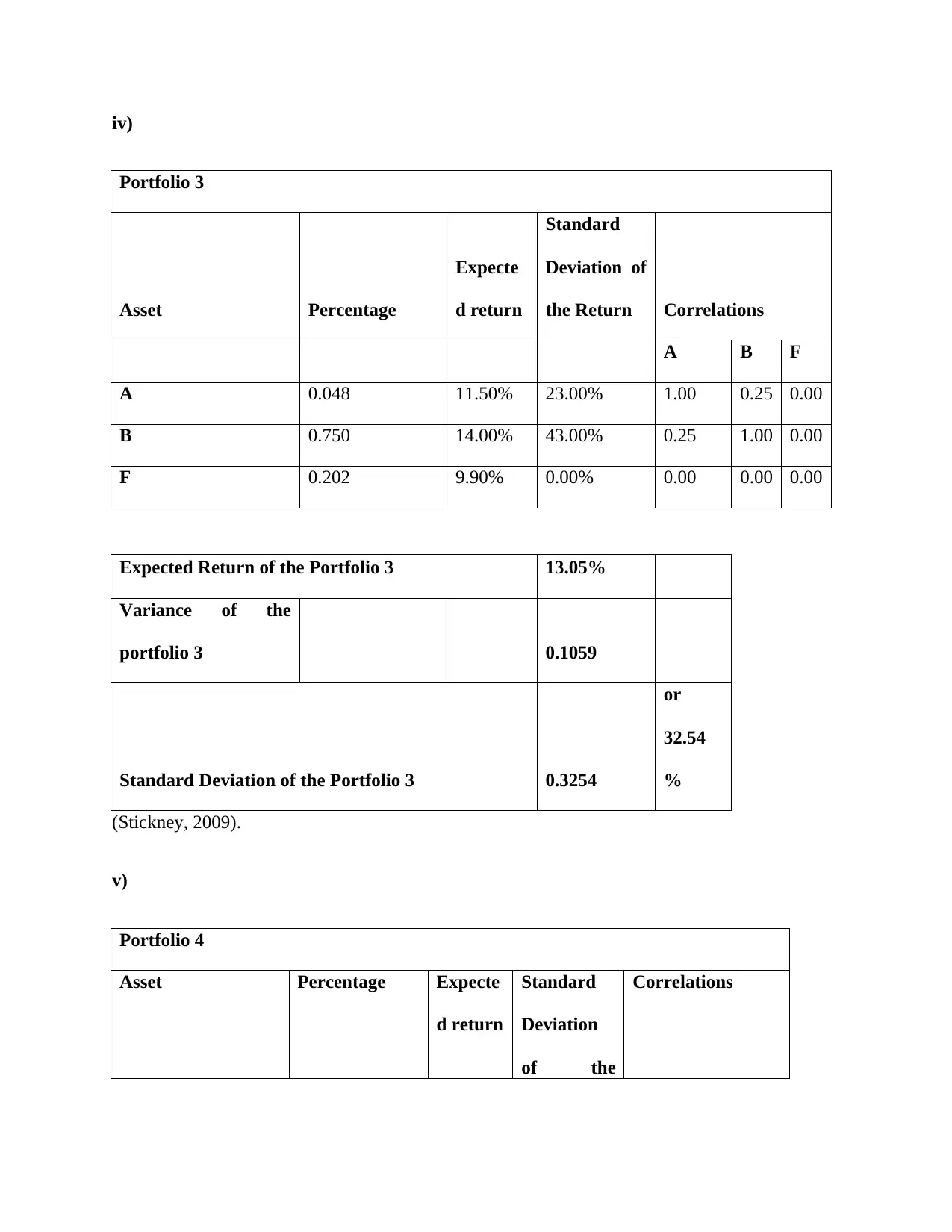

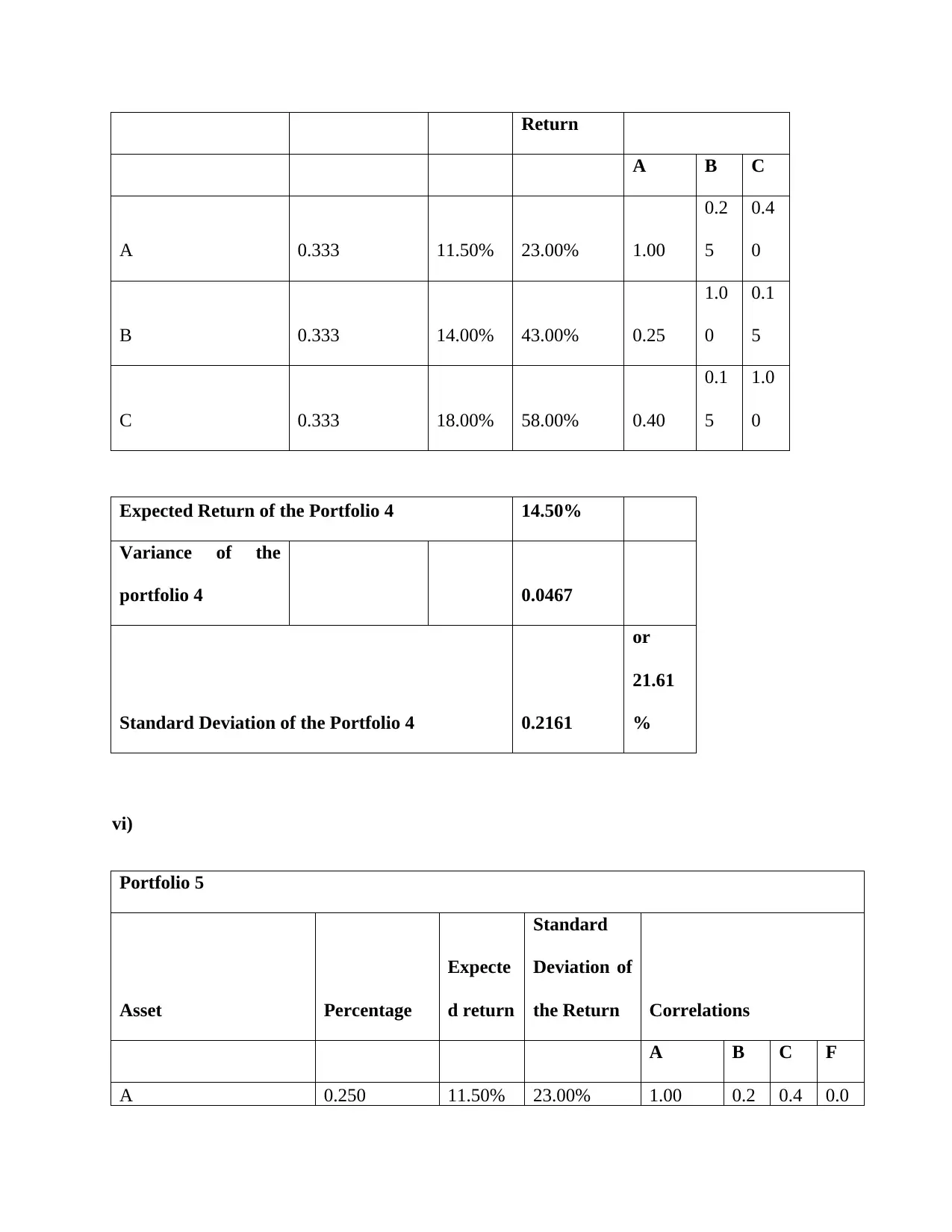

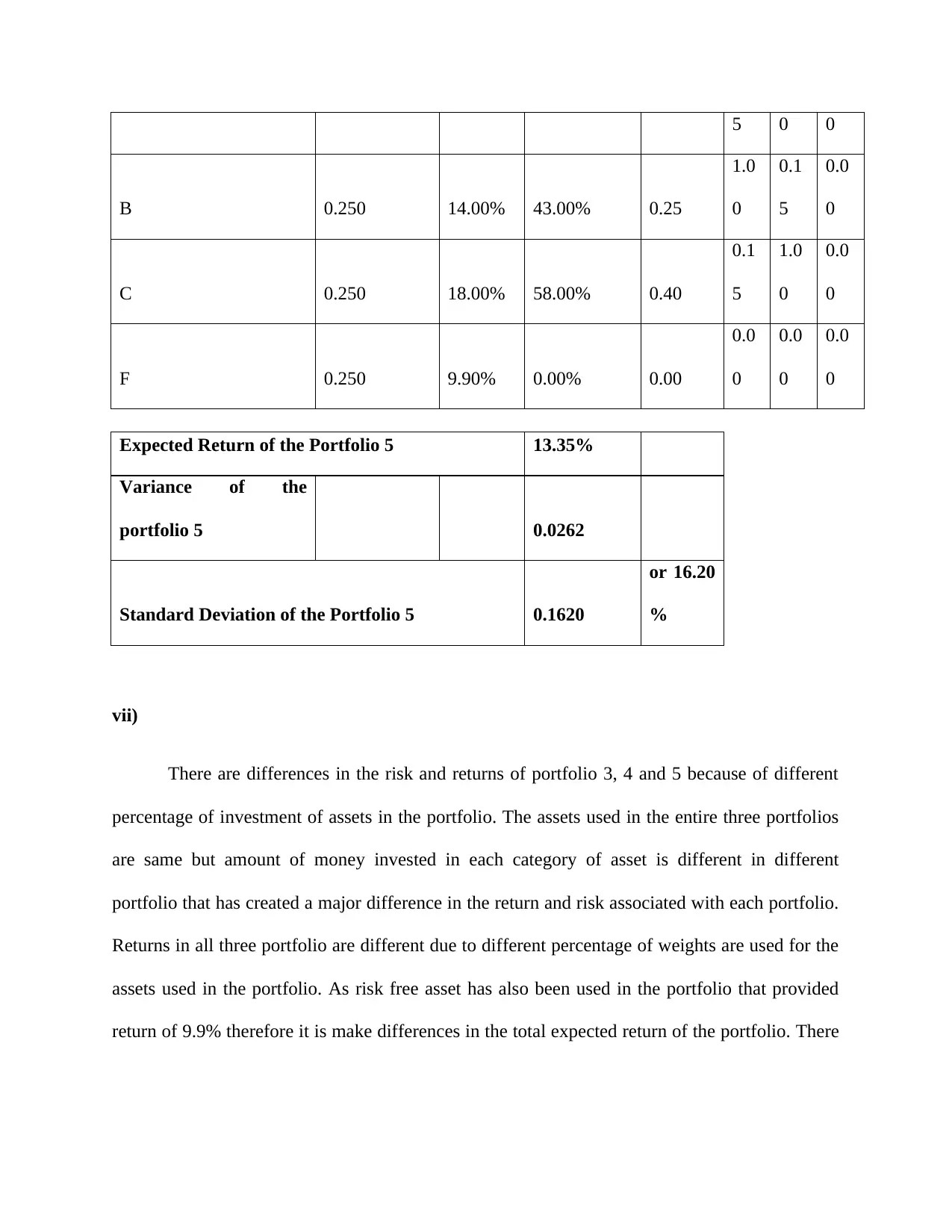

This assignment provides a comprehensive analysis of portfolio risk and return, covering key concepts such as standard deviation, correlation, and diversification. Part 1 explains the measurement of market volatility through standard deviation, the impact of beta on returns, and the role of correlation in portfolio risk. It also differentiates between systematic and unsystematic risk, and discusses the risk-free asset. Part 2 involves the calculation of expected returns, variance, and standard deviation for five different portfolios with varying asset allocations, including the use of a risk-free asset. The analysis highlights how different portfolio compositions affect overall risk and return profiles, emphasizing the importance of diversification and asset weighting in financial decision-making. The assignment references key financial accounting texts to support its analysis.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.