University Finance Assignment: Portfolio Management Analysis

VerifiedAdded on 2022/08/23

|8

|881

|25

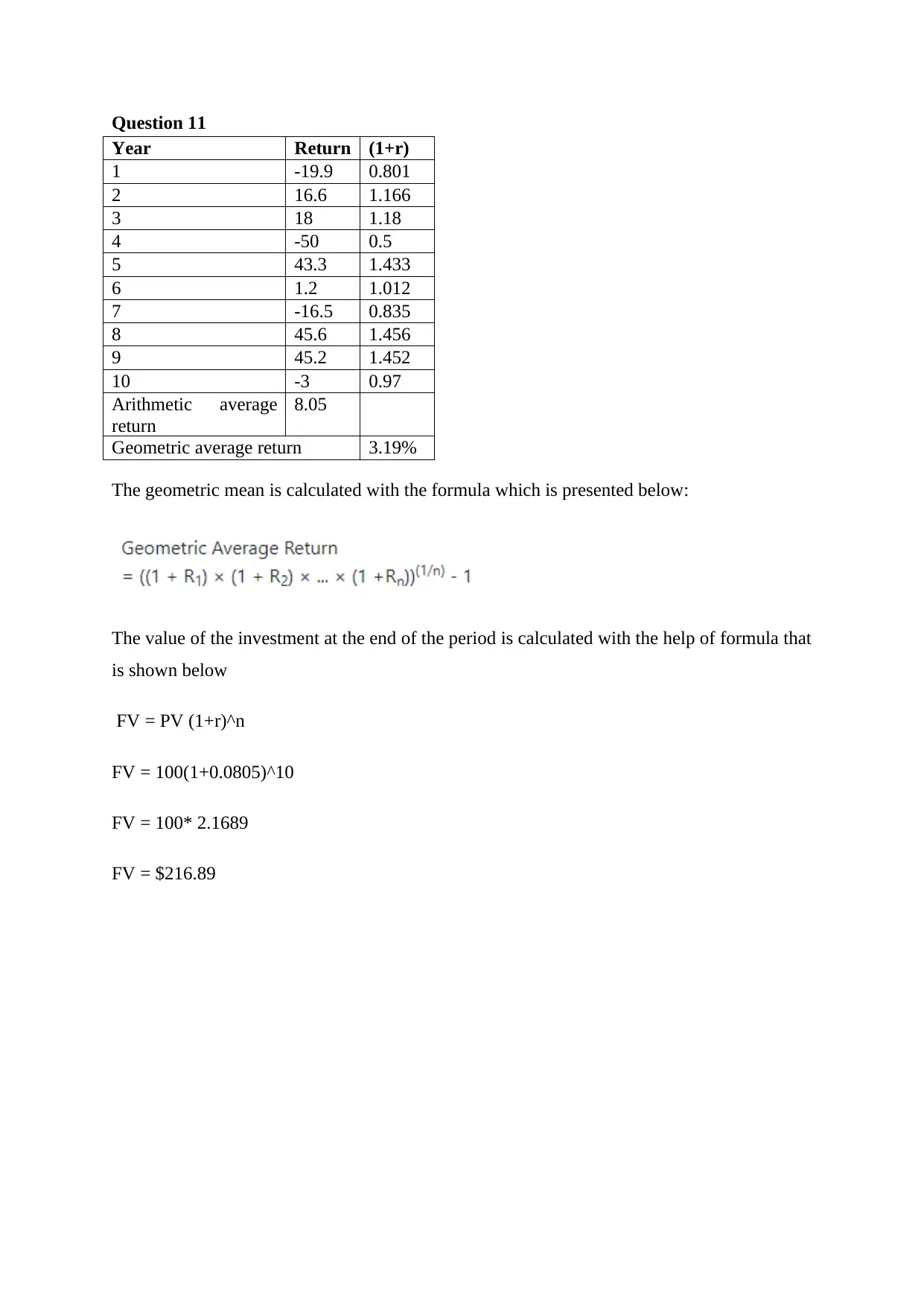

Homework Assignment

AI Summary

This finance assignment solution provides a detailed analysis of portfolio management, covering various aspects such as calculating the expected return on a portfolio, determining the weights of stocks within a portfolio, and analyzing historical risk and return data. It includes calculations of realized returns, dividend yields, and capital gains, along with an assessment of portfolio volatility using standard deviation and correlation. The assignment also explores the concepts of common versus independent risk, diversification strategies, and the impact of economic conditions on investment decisions. The solution uses formulas and provides step-by-step calculations to illustrate the concepts. It also includes references to academic research on portfolio diversification and stock return analysis. The document provides a comprehensive overview of portfolio construction, risk management, and investment strategies.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.