University Finance: Portfolio Optimization, Risk, and Return Analysis

VerifiedAdded on 2022/09/10

|4

|634

|18

Homework Assignment

AI Summary

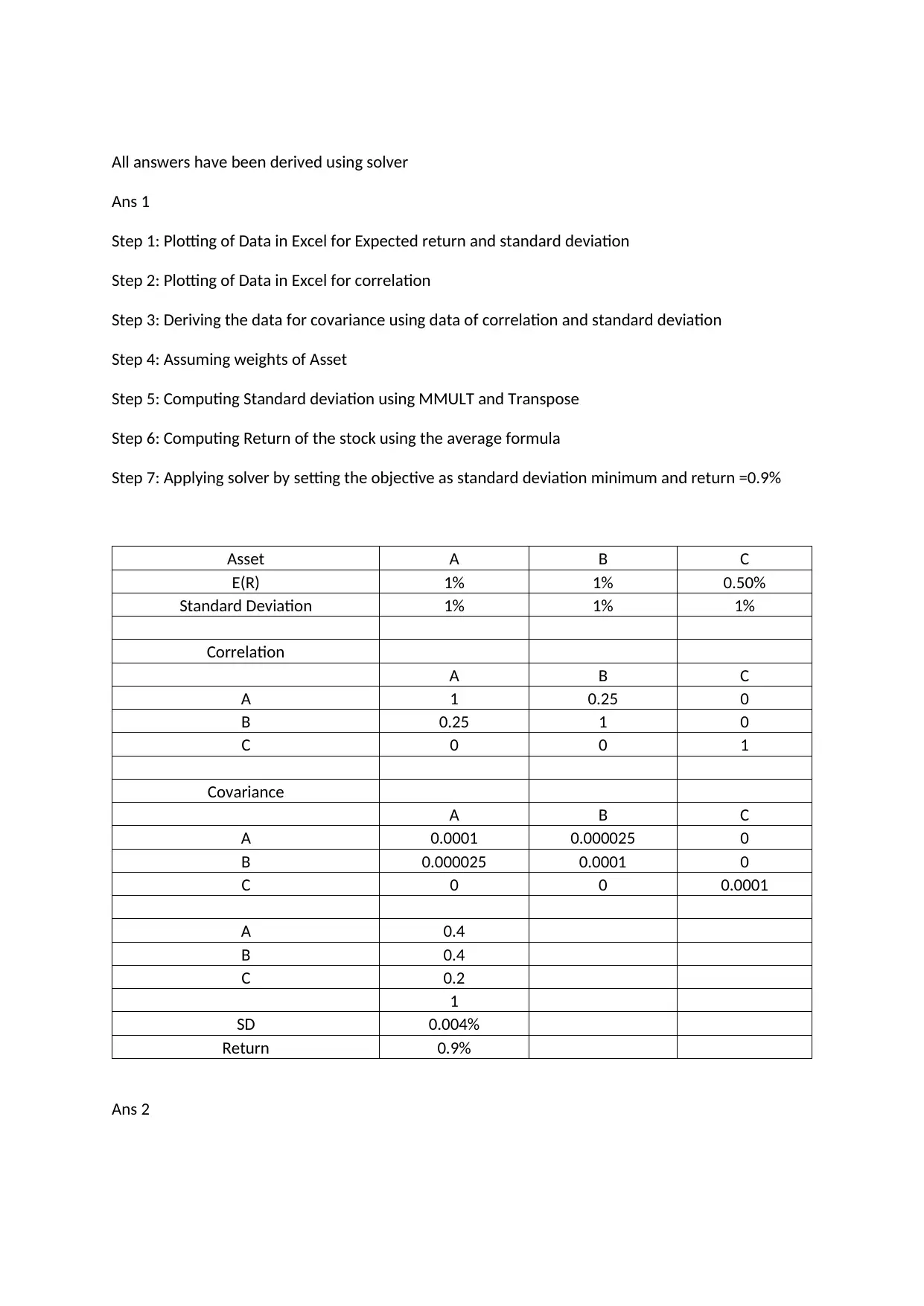

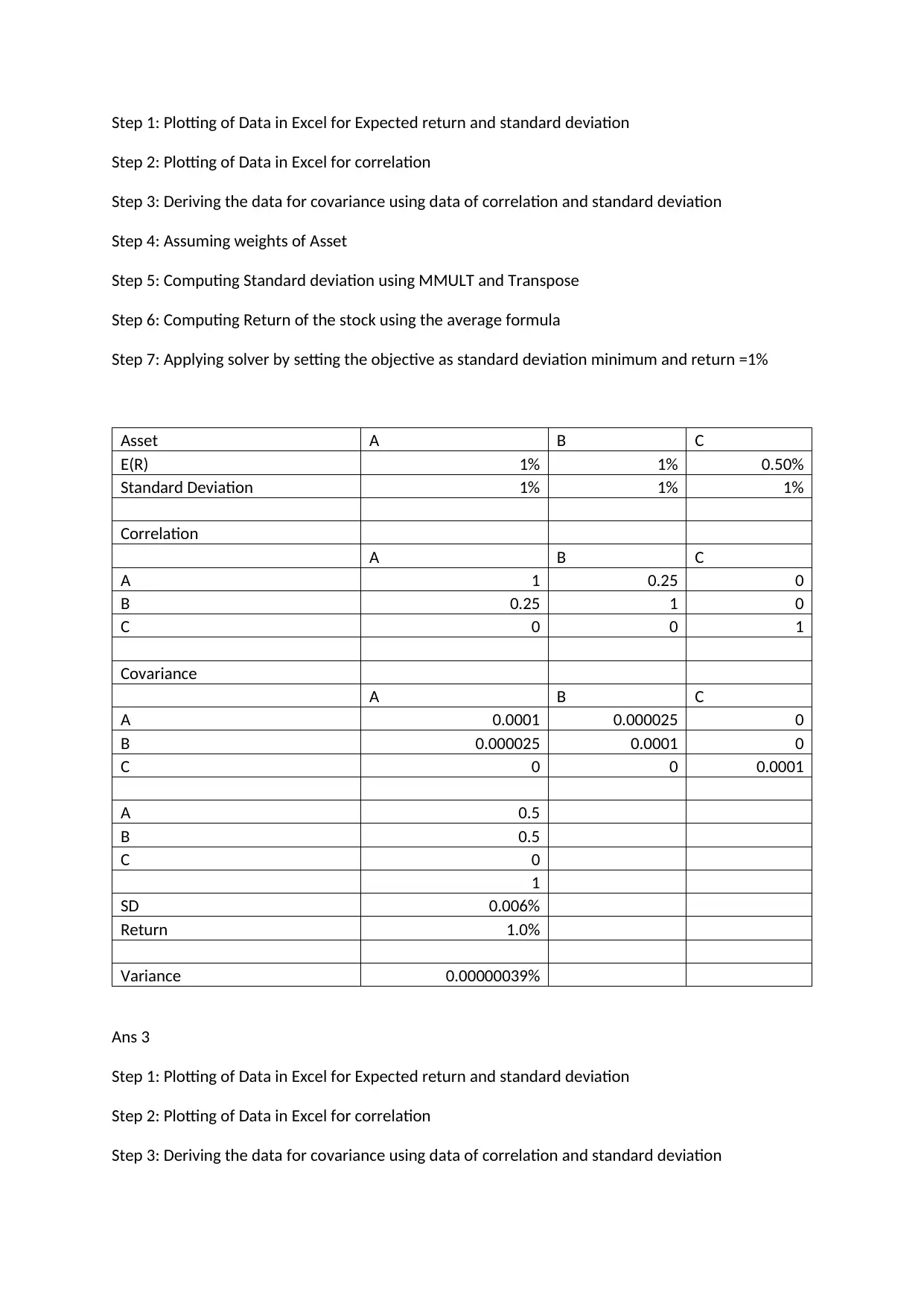

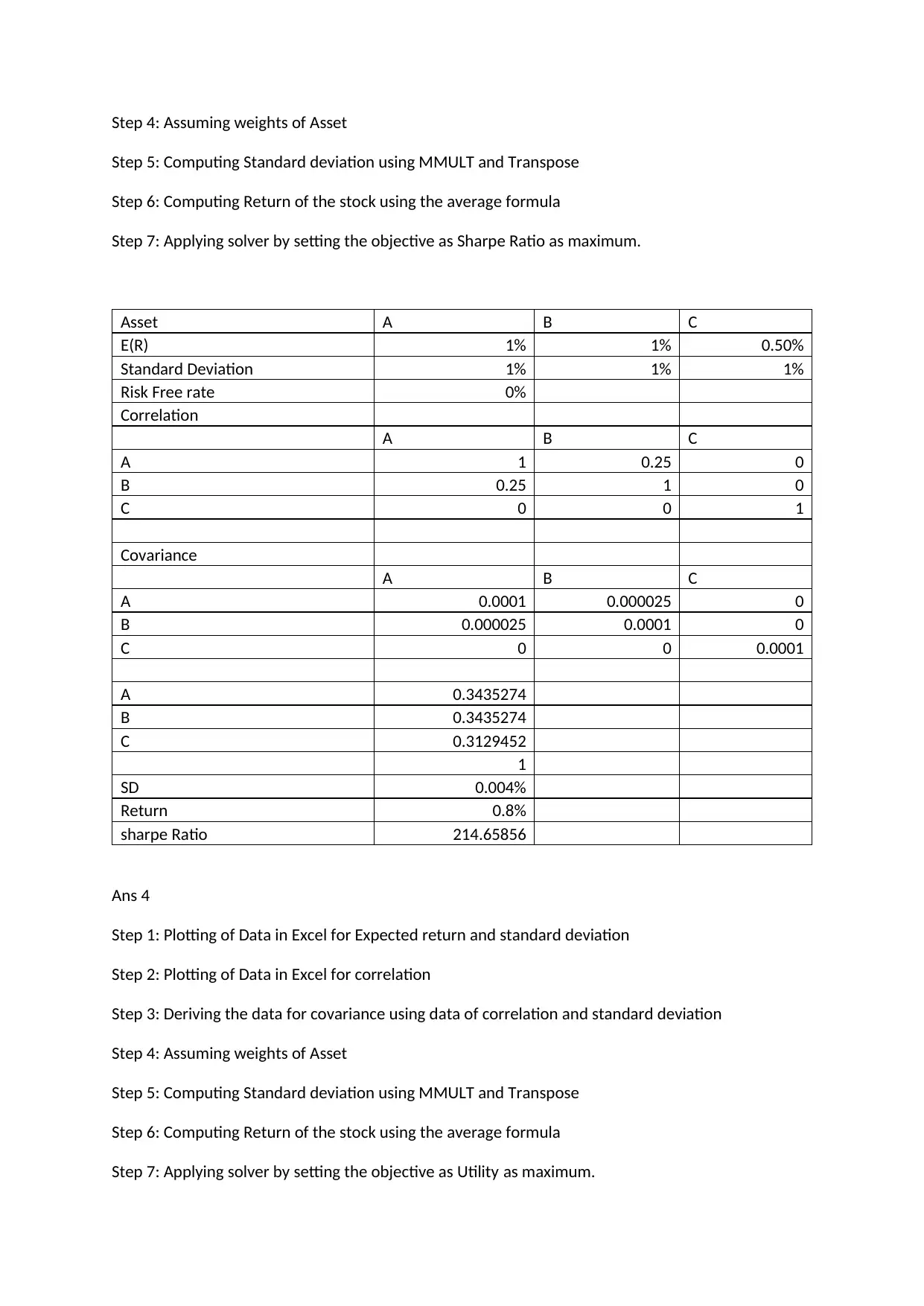

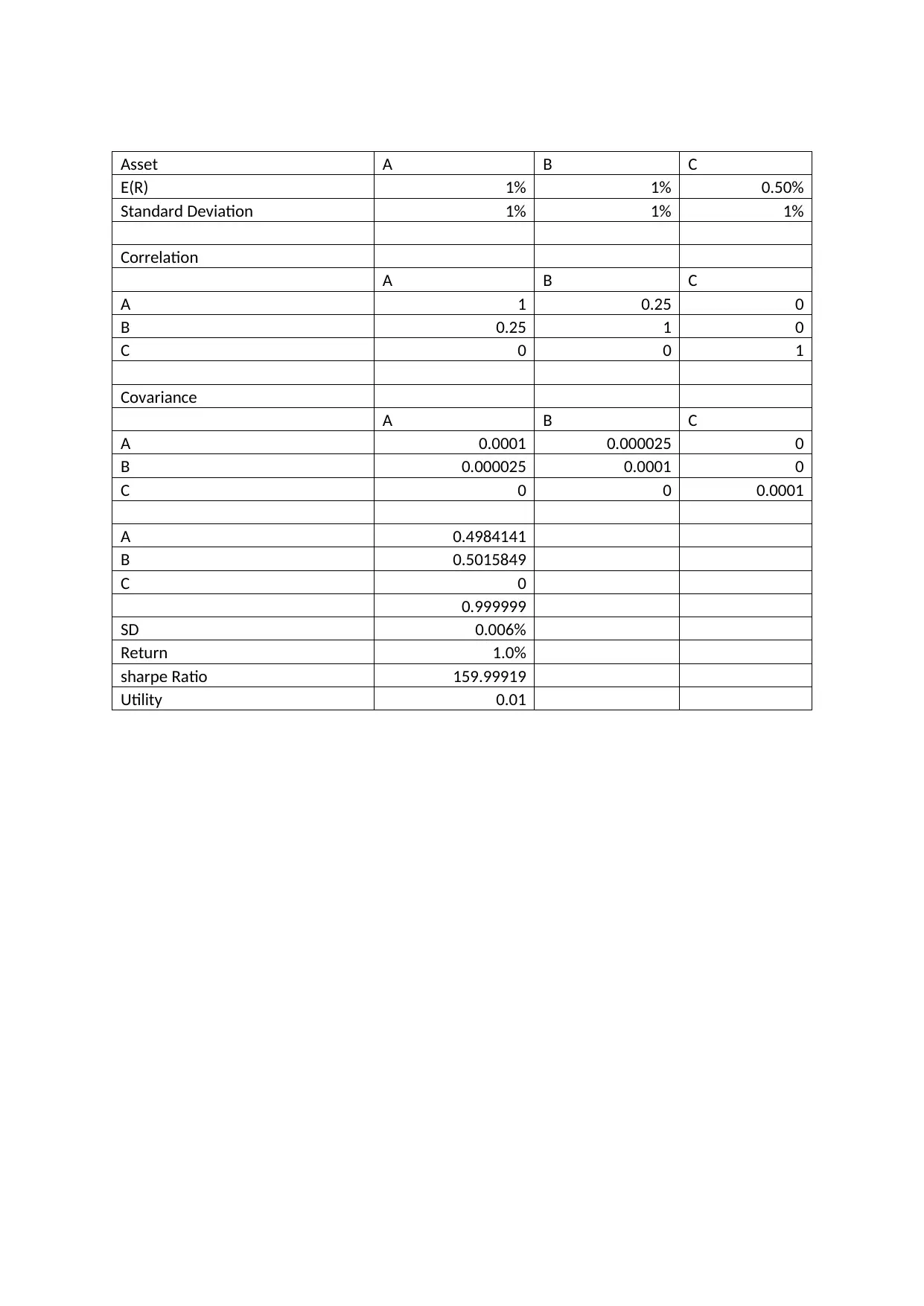

This homework assignment focuses on portfolio optimization using Excel, analyzing the risk and return of different assets. The solution demonstrates the process of plotting data, calculating covariance, and applying the Excel Solver to determine optimal asset weights. The assignment covers three scenarios: minimizing standard deviation for a target return, maximizing the Sharpe ratio, and maximizing utility. Each scenario involves detailed steps, including the use of correlation matrices, covariance calculations, and the application of the MMULT and TRANSPOSE functions in Excel. The results include the optimized weights for each asset, the resulting standard deviation, return, Sharpe ratio, and utility, providing a practical guide to portfolio construction and risk management. The assignment also highlights the importance of understanding these concepts in making informed investment decisions.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.