Portfolio Management Project: Investment Opportunity Set Analysis

VerifiedAdded on 2022/08/26

|14

|3291

|25

Project

AI Summary

This portfolio management project analyzes investment strategies based on modern portfolio theory. It examines historical stock data of two companies, calculating returns, volatility, and correlation to construct an investment opportunity set. The project explores portfolio construction, the importance of diversification, and the concepts of optimal risky and minimum variance portfolios. The analysis includes the capital allocation line and a comparison between the two portfolios. The project uses real-world data to demonstrate how to build and manage investment portfolios effectively, considering risk-return profiles and diversification benefits. The project provides a detailed analysis of portfolio construction, risk management, and return optimization, offering practical insights for students in finance.

Running head: PORTFOLIO MANAGEMENT

Portfolio Management

Name of the Student:

Name of the University:

Author Note:

Portfolio Management

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1PORTFOLIO MANAGEMENT

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Portfolio Construction:...........................................................................................................2

Importance of Diversification:...............................................................................................3

Stock Return and the Correlation:..........................................................................................5

Portfolio Opportunity Set:......................................................................................................6

Optimal Risky Portfolio, Capital Allocation Line and minimum variance portfolio:...........7

Comparison between the Two Portfolios:..............................................................................9

Conclusion:..............................................................................................................................10

References:...............................................................................................................................11

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Portfolio Construction:...........................................................................................................2

Importance of Diversification:...............................................................................................3

Stock Return and the Correlation:..........................................................................................5

Portfolio Opportunity Set:......................................................................................................6

Optimal Risky Portfolio, Capital Allocation Line and minimum variance portfolio:...........7

Comparison between the Two Portfolios:..............................................................................9

Conclusion:..............................................................................................................................10

References:...............................................................................................................................11

2PORTFOLIO MANAGEMENT

Introduction:

Modern portfolio theory highlights the concept of optimal risky portfolio and the

minimum variance portfolio in the investment universe. The investment universe highlights

the use of various asset classes for the purpose of investment of an investor’s portfolio. An

investor can be having different risk preference and return preference according to which a

portfolio manager makes investment decisions. The asset classes can be characterized as

bonds, equity, alternative investment and many other types of hybrid securities which is

included by the portfolio manager as per the risk return profile of the investor (Johannes

2018).

The report presented below aims to highlight the various theoretical concepts of the

modern portfolio theory. This report provides the efficient frontier or the investment

opportunity set of the securities selected for the portfolio. It also highlights the optimal risky

portfolio and the minimum variance portfolio of the securities. Also it tends to provide an

insight of the benefits of diversification which can be achieved by the mix of the securities in

the portfolio.

Discussion and Analysis

Historical Data

The historical data has been well collected for a sum of five year whereby relevant

changes in the stock price on a monthly basis has been considered. The monthly closing price

for each of the stock from the time period January 2015 to December 2019 has been well

considered for analysis purpose. The two stocks which have been selected for the portfolio

have provided the following return which would be used in the calculation of the portfolio

return. The historical stock price movements of the stocks have been taken for a period of 5

Introduction:

Modern portfolio theory highlights the concept of optimal risky portfolio and the

minimum variance portfolio in the investment universe. The investment universe highlights

the use of various asset classes for the purpose of investment of an investor’s portfolio. An

investor can be having different risk preference and return preference according to which a

portfolio manager makes investment decisions. The asset classes can be characterized as

bonds, equity, alternative investment and many other types of hybrid securities which is

included by the portfolio manager as per the risk return profile of the investor (Johannes

2018).

The report presented below aims to highlight the various theoretical concepts of the

modern portfolio theory. This report provides the efficient frontier or the investment

opportunity set of the securities selected for the portfolio. It also highlights the optimal risky

portfolio and the minimum variance portfolio of the securities. Also it tends to provide an

insight of the benefits of diversification which can be achieved by the mix of the securities in

the portfolio.

Discussion and Analysis

Historical Data

The historical data has been well collected for a sum of five year whereby relevant

changes in the stock price on a monthly basis has been considered. The monthly closing price

for each of the stock from the time period January 2015 to December 2019 has been well

considered for analysis purpose. The two stocks which have been selected for the portfolio

have provided the following return which would be used in the calculation of the portfolio

return. The historical stock price movements of the stocks have been taken for a period of 5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3PORTFOLIO MANAGEMENT

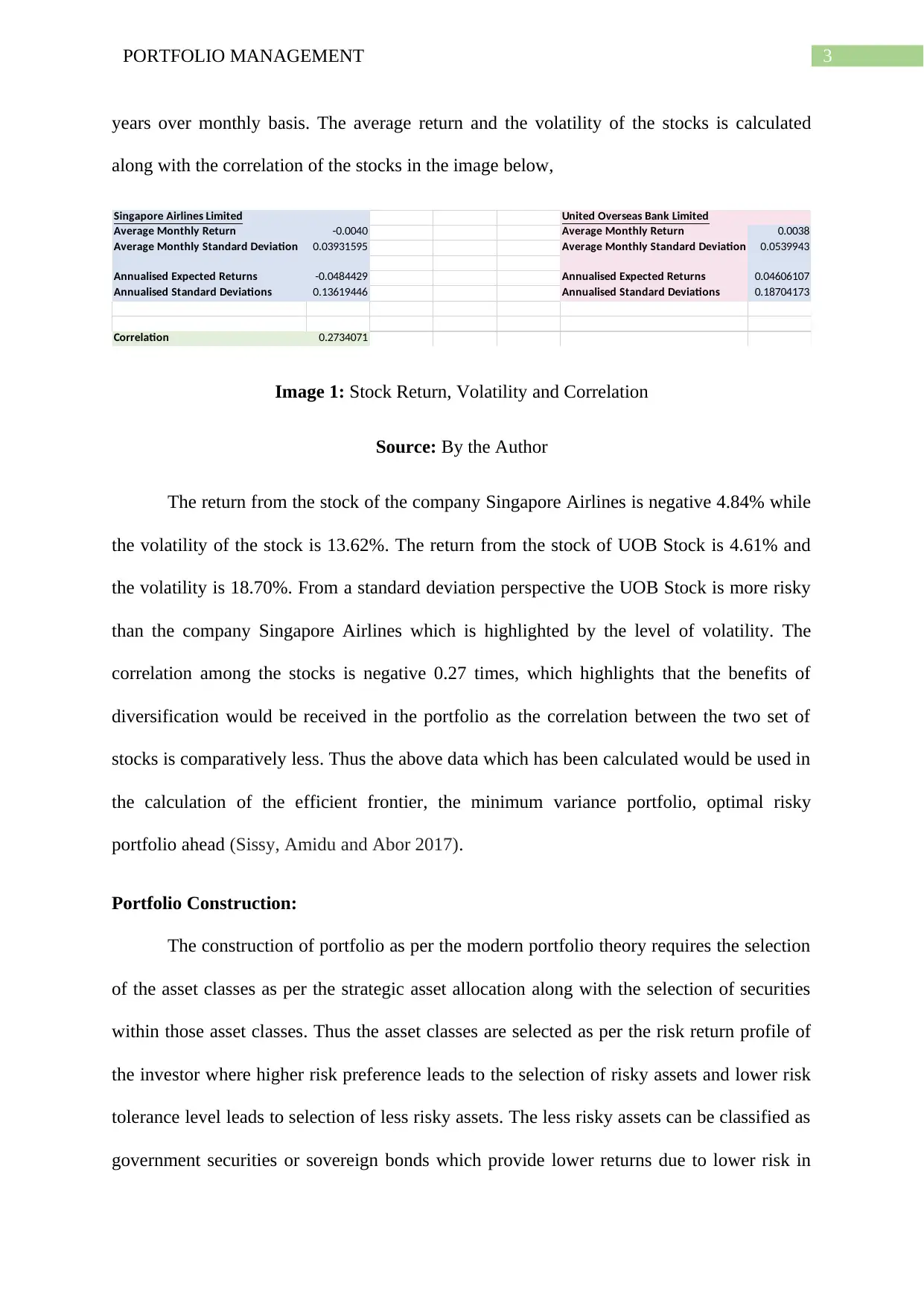

years over monthly basis. The average return and the volatility of the stocks is calculated

along with the correlation of the stocks in the image below,

Singapore Airlines Limited United Overseas Bank Limited

Average Monthly Return -0.0040 Average Monthly Return 0.0038

Average Monthly Standard Deviation 0.03931595 Average Monthly Standard Deviation 0.0539943

Annualised Expected Returns -0.0484429 Annualised Expected Returns 0.04606107

Annualised Standard Deviations 0.13619446 Annualised Standard Deviations 0.18704173

Correlation 0.2734071

Image 1: Stock Return, Volatility and Correlation

Source: By the Author

The return from the stock of the company Singapore Airlines is negative 4.84% while

the volatility of the stock is 13.62%. The return from the stock of UOB Stock is 4.61% and

the volatility is 18.70%. From a standard deviation perspective the UOB Stock is more risky

than the company Singapore Airlines which is highlighted by the level of volatility. The

correlation among the stocks is negative 0.27 times, which highlights that the benefits of

diversification would be received in the portfolio as the correlation between the two set of

stocks is comparatively less. Thus the above data which has been calculated would be used in

the calculation of the efficient frontier, the minimum variance portfolio, optimal risky

portfolio ahead (Sissy, Amidu and Abor 2017).

Portfolio Construction:

The construction of portfolio as per the modern portfolio theory requires the selection

of the asset classes as per the strategic asset allocation along with the selection of securities

within those asset classes. Thus the asset classes are selected as per the risk return profile of

the investor where higher risk preference leads to the selection of risky assets and lower risk

tolerance level leads to selection of less risky assets. The less risky assets can be classified as

government securities or sovereign bonds which provide lower returns due to lower risk in

years over monthly basis. The average return and the volatility of the stocks is calculated

along with the correlation of the stocks in the image below,

Singapore Airlines Limited United Overseas Bank Limited

Average Monthly Return -0.0040 Average Monthly Return 0.0038

Average Monthly Standard Deviation 0.03931595 Average Monthly Standard Deviation 0.0539943

Annualised Expected Returns -0.0484429 Annualised Expected Returns 0.04606107

Annualised Standard Deviations 0.13619446 Annualised Standard Deviations 0.18704173

Correlation 0.2734071

Image 1: Stock Return, Volatility and Correlation

Source: By the Author

The return from the stock of the company Singapore Airlines is negative 4.84% while

the volatility of the stock is 13.62%. The return from the stock of UOB Stock is 4.61% and

the volatility is 18.70%. From a standard deviation perspective the UOB Stock is more risky

than the company Singapore Airlines which is highlighted by the level of volatility. The

correlation among the stocks is negative 0.27 times, which highlights that the benefits of

diversification would be received in the portfolio as the correlation between the two set of

stocks is comparatively less. Thus the above data which has been calculated would be used in

the calculation of the efficient frontier, the minimum variance portfolio, optimal risky

portfolio ahead (Sissy, Amidu and Abor 2017).

Portfolio Construction:

The construction of portfolio as per the modern portfolio theory requires the selection

of the asset classes as per the strategic asset allocation along with the selection of securities

within those asset classes. Thus the asset classes are selected as per the risk return profile of

the investor where higher risk preference leads to the selection of risky assets and lower risk

tolerance level leads to selection of less risky assets. The less risky assets can be classified as

government securities or sovereign bonds which provide lower returns due to lower risk in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4PORTFOLIO MANAGEMENT

these assets. Risky assets can be like equity asset class or private equities, hedge funds which

are more risky assets (Lee, Trzcinka and Venkatesan 2019).

The two stocks which are selected are the company Singapore Airlines and the other

company which is selected for the portfolio is United Overseas Bank Ltd (Kopmann, Kock,

Killen and Gemünden 2017). Thus the details of the two companies is provided below,

Singapore Airlines Limited: The airlines company is the flagship carrier airline of the

Singapore with its major hub in the Singapore Changi Airport. The airline is well

notable for well using the Singapore Girl as its central figure for corporate branding.

The company is listed in the Singapore Index with its stock symbol as SGD and the

stock price of the company is currently trading at SGD6.50. The Company represents

the aviation industry of Singapore and provides travel and hospitality services to

individuals. The airlines operate it flights domestically as well as internationally to

almost all the popular destinations around the globe (Singapore Airlines 2020).

United Overseas Bank: United Overseas Bank Ltd is a major Singaporean

Multinational Bank, which is having most of its branches in the Southeast Asian

Countries. The bank was founded in the year 1935 by the United Chinese Bank and its

provides a range of commercial and various corporate banking services along with

personal banking and asset management services (UOB 2020).

Investment Opportunity Set:

The portfolio opportunity set is a line of specific return and risk which is provided

from the portfolio. It tends to provide the highest level of return for a specific level of risk.

The specific level of risk is calculated by the different level of weights provided to the stocks

in the portfolio. This provides a range of return for a specific level of risk which is

highlighted in the graph below:

these assets. Risky assets can be like equity asset class or private equities, hedge funds which

are more risky assets (Lee, Trzcinka and Venkatesan 2019).

The two stocks which are selected are the company Singapore Airlines and the other

company which is selected for the portfolio is United Overseas Bank Ltd (Kopmann, Kock,

Killen and Gemünden 2017). Thus the details of the two companies is provided below,

Singapore Airlines Limited: The airlines company is the flagship carrier airline of the

Singapore with its major hub in the Singapore Changi Airport. The airline is well

notable for well using the Singapore Girl as its central figure for corporate branding.

The company is listed in the Singapore Index with its stock symbol as SGD and the

stock price of the company is currently trading at SGD6.50. The Company represents

the aviation industry of Singapore and provides travel and hospitality services to

individuals. The airlines operate it flights domestically as well as internationally to

almost all the popular destinations around the globe (Singapore Airlines 2020).

United Overseas Bank: United Overseas Bank Ltd is a major Singaporean

Multinational Bank, which is having most of its branches in the Southeast Asian

Countries. The bank was founded in the year 1935 by the United Chinese Bank and its

provides a range of commercial and various corporate banking services along with

personal banking and asset management services (UOB 2020).

Investment Opportunity Set:

The portfolio opportunity set is a line of specific return and risk which is provided

from the portfolio. It tends to provide the highest level of return for a specific level of risk.

The specific level of risk is calculated by the different level of weights provided to the stocks

in the portfolio. This provides a range of return for a specific level of risk which is

highlighted in the graph below:

5PORTFOLIO MANAGEMENT

Investment Opportunity Set

W1 W2 Sp Erp

100

% 0.00%

0.13619

446

-

0.04844

29

95

% 5.00%

0.13224

797

-

0.04371

77

90

%

10.00

%

0.12895

015

-

0.03899

25

85

%

15.00

%

0.12635

18

-

0.03426

73

80

%

20.00

%

0.12449

671

-

0.02954

21

75

%

25.00

%

0.12341

842

-

0.02481

69

70

%

30.00

%

0.12313

733

-

0.02009

17

65

%

35.00

%

0.12365

887

-

0.01536

65

60

%

40.00

%

0.12497

299

-

0.01064

13

55

%

45.00

%

0.12705

512

-

0.00591

61

50

%

50.00

%

0.12986

831

-

0.00119

09

45

%

55.00

%

0.13336

63

0.00353

429

40

%

60.00

%

0.13749

685

0.00825

949

35

%

65.00

%

0.14220

485

0.01298

468

30

%

70.00

%

0.14743

497

0.01770

988

25

%

75.00

%

0.15313

375

0.02243

508

Investment Opportunity Set

W1 W2 Sp Erp

100

% 0.00%

0.13619

446

-

0.04844

29

95

% 5.00%

0.13224

797

-

0.04371

77

90

%

10.00

%

0.12895

015

-

0.03899

25

85

%

15.00

%

0.12635

18

-

0.03426

73

80

%

20.00

%

0.12449

671

-

0.02954

21

75

%

25.00

%

0.12341

842

-

0.02481

69

70

%

30.00

%

0.12313

733

-

0.02009

17

65

%

35.00

%

0.12365

887

-

0.01536

65

60

%

40.00

%

0.12497

299

-

0.01064

13

55

%

45.00

%

0.12705

512

-

0.00591

61

50

%

50.00

%

0.12986

831

-

0.00119

09

45

%

55.00

%

0.13336

63

0.00353

429

40

%

60.00

%

0.13749

685

0.00825

949

35

%

65.00

%

0.14220

485

0.01298

468

30

%

70.00

%

0.14743

497

0.01770

988

25

%

75.00

%

0.15313

375

0.02243

508

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6PORTFOLIO MANAGEMENT

20

%

80.00

%

0.15925

086

0.02716

028

15

%

85.00

%

0.16574

001

0.03188

547

10

%

90.00

%

0.17255

921

0.03661

067

5%

95.00

%

0.17967

091

0.04133

587

0%

100.0

0%

0.18704

173

0.04606

107

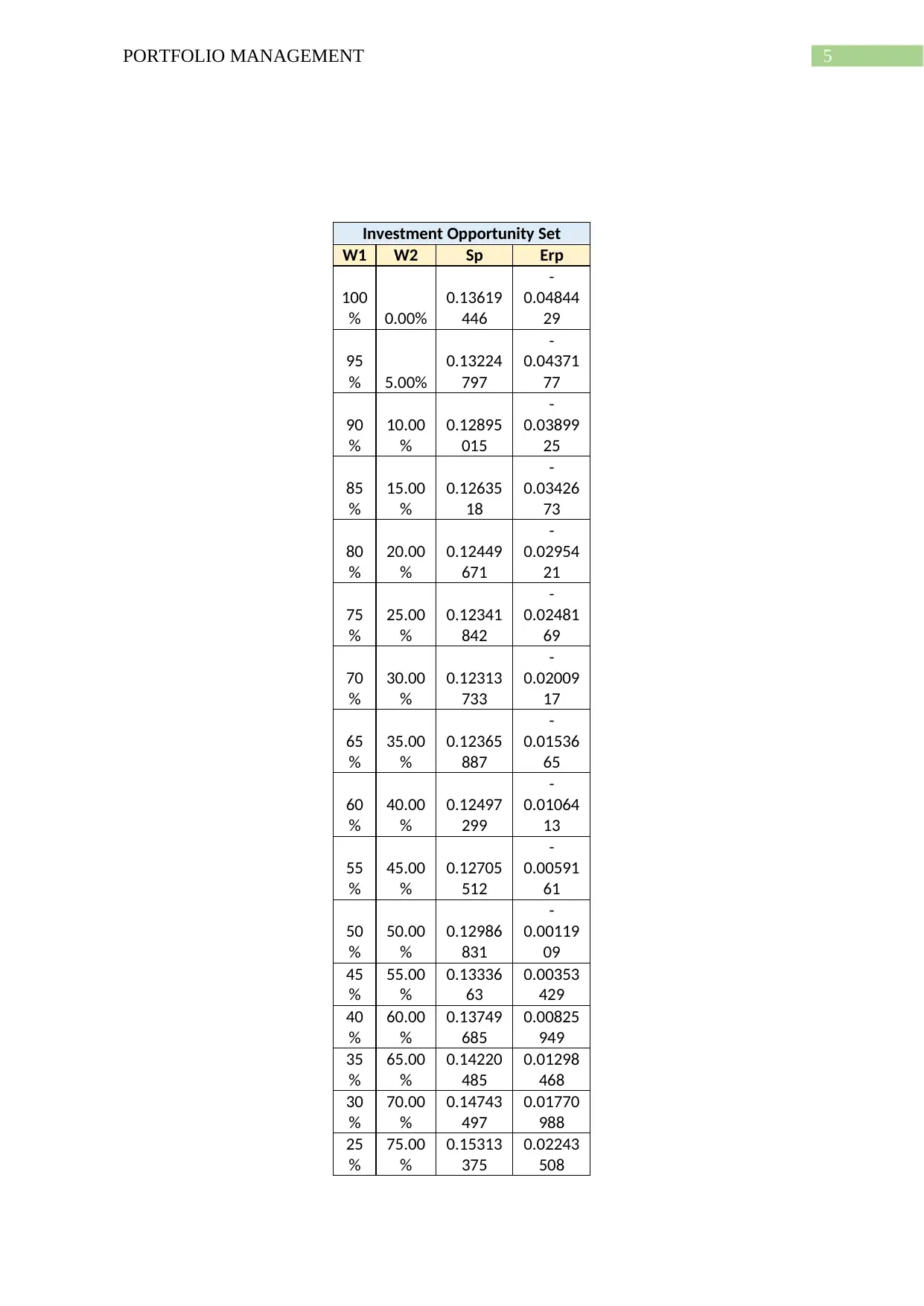

The table shown above well represents the various investment opportunities that are

available with the investors for the purpose of investment. The investment opportunity set

shows that various set of investment available with the investors which can well help them

maximize the given set of returns with the lowest possible standard deviation.

Optimal Risky Portfolio, Capital Allocation Line and minimum variance portfolio:

The optimal risky portfolio is the portfolio which just is tangent to the capital

allocation line. The line represents various set of investment sets which can be taken by the

investor for investing in risk free to risky assets, the point on the Y axis where the line is

starting from represents the risk free point in the portfolio. This is the return which is

generated by the investor from the portfolio when making a zero risk portfolio.

The minimum return which an investor can generate from the portfolio when

investing at the risk free investment and generate a return of 0.957%. This return increases

with the level of risk and the highest return which can be generated from the portfolio is the

level of around 4.61% with the risk of around 18.72%. This line represents the investment

opportunities available with the investor at the different level of risk. Thus a risk averse

would invest in a portfolio with the lowest level of risk near the Y axis, while a risk loving

investor would invest in a portfolio which is at the north-west corner of the portfolio (Henry

2017).

20

%

80.00

%

0.15925

086

0.02716

028

15

%

85.00

%

0.16574

001

0.03188

547

10

%

90.00

%

0.17255

921

0.03661

067

5%

95.00

%

0.17967

091

0.04133

587

0%

100.0

0%

0.18704

173

0.04606

107

The table shown above well represents the various investment opportunities that are

available with the investors for the purpose of investment. The investment opportunity set

shows that various set of investment available with the investors which can well help them

maximize the given set of returns with the lowest possible standard deviation.

Optimal Risky Portfolio, Capital Allocation Line and minimum variance portfolio:

The optimal risky portfolio is the portfolio which just is tangent to the capital

allocation line. The line represents various set of investment sets which can be taken by the

investor for investing in risk free to risky assets, the point on the Y axis where the line is

starting from represents the risk free point in the portfolio. This is the return which is

generated by the investor from the portfolio when making a zero risk portfolio.

The minimum return which an investor can generate from the portfolio when

investing at the risk free investment and generate a return of 0.957%. This return increases

with the level of risk and the highest return which can be generated from the portfolio is the

level of around 4.61% with the risk of around 18.72%. This line represents the investment

opportunities available with the investor at the different level of risk. Thus a risk averse

would invest in a portfolio with the lowest level of risk near the Y axis, while a risk loving

investor would invest in a portfolio which is at the north-west corner of the portfolio (Henry

2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7PORTFOLIO MANAGEMENT

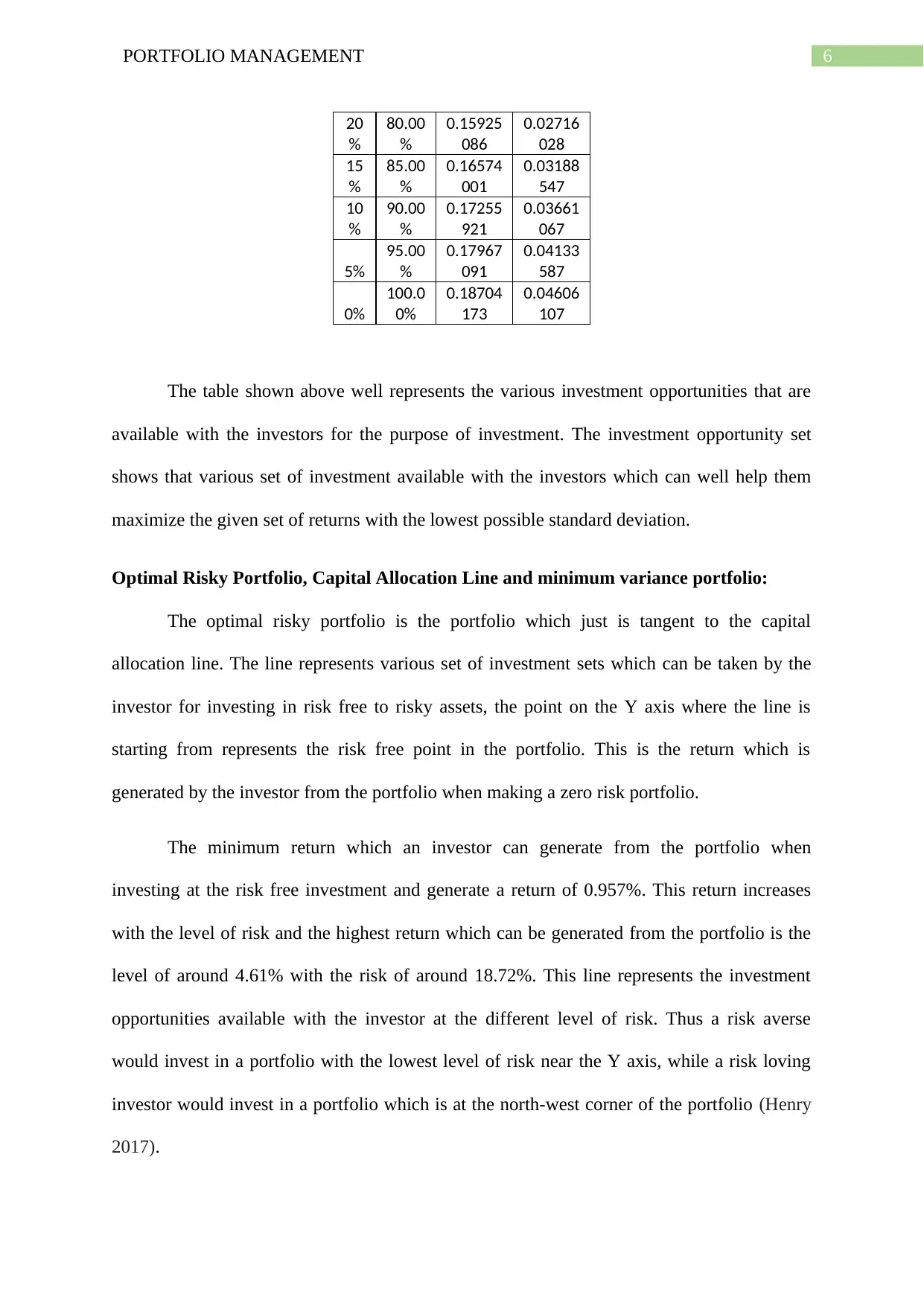

0 0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0.18 0.2

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

Effi cient Frontier

Erp Risk Free

Optimal Risky Minimum Variance Portfolio

This line represents the direct relationship between the return and the level of risk, a

higher level of risk signifies a higher level of return which can be generated from a portfolio.

The optimal risky portfolio is the portfolio which provides the optimal level of return

with the level of risk, which is suitable for the investor. The investor can invest in any of the

portfolio in the efficient frontier, however the optimal risky portfolio provides the best

optimal return at that level of risk. The capital allocation line highlights the various levels at

which the investor can invest its capital. The point of tangency between the optimal risky

portfolio and the capital allocation line present the suitable allocation of investment for an

investor (Klaassen and Van Eeghen 2018).

The minimum variance portfolio tends to provide the portfolio with the lowest level

of risk for a certain level of return. The aim of this portfolio is to provide the lowest level of

risk with a certain return.

The optimal risky portfolio is highlighted by the grey dot on the graph, which

represents the point of tangency between the portfolio and the capital allocation line. The

minimum variance portfolio is represented by the yellow dot which is the return which can be

generated by the portfolio at the lowest level of risk (Maggiori, Neiman and Schreger 2018).

0 0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0.18 0.2

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

Effi cient Frontier

Erp Risk Free

Optimal Risky Minimum Variance Portfolio

This line represents the direct relationship between the return and the level of risk, a

higher level of risk signifies a higher level of return which can be generated from a portfolio.

The optimal risky portfolio is the portfolio which provides the optimal level of return

with the level of risk, which is suitable for the investor. The investor can invest in any of the

portfolio in the efficient frontier, however the optimal risky portfolio provides the best

optimal return at that level of risk. The capital allocation line highlights the various levels at

which the investor can invest its capital. The point of tangency between the optimal risky

portfolio and the capital allocation line present the suitable allocation of investment for an

investor (Klaassen and Van Eeghen 2018).

The minimum variance portfolio tends to provide the portfolio with the lowest level

of risk for a certain level of return. The aim of this portfolio is to provide the lowest level of

risk with a certain return.

The optimal risky portfolio is highlighted by the grey dot on the graph, which

represents the point of tangency between the portfolio and the capital allocation line. The

minimum variance portfolio is represented by the yellow dot which is the return which can be

generated by the portfolio at the lowest level of risk (Maggiori, Neiman and Schreger 2018).

8PORTFOLIO MANAGEMENT

Minimum Variance Portfolio

Minimum variance portfolio shows the maximum return that an investors can well get

with the help of lowest possible set of risks. The optimal risky portfolio is the suitable

portfolio for the investor as per his risk return profile and should be used for the investment

purpose. However, with the change of the risk return preference of the investor the optimal

risky portfolio changes as the capital allocation line changes for the investor. The minimum

variance portfolio highlights the level of risk and seeks to provide the investor with a

portfolio which has the lowest level of risk and is suitable for a risk hating investor who does

not wish to take excessive risk (Larrain and Stumpner 2017). The return generated by the

minimum variance portfolio has been around -2.08% and the level of risk at the same time for

the portfolio has been around 12.31%.

The optimal portfolio seeks to provide the highest reward in terms of risk undertaken

by the investor and is a suitable investment for a rational investor. The minimum variance

portfolio seeks to lower the risk for the investor without considering the return factor from

the investment. As this is highlighted in the graph above the minimum variance portfolio

provides a negative return while reducing the risk from the portfolio (Christensen, Irle and

Ludwig 2017).

Diversification in Portfolio

The diversification is an important aspect of portfolio management which seeks to

reduce the risk of the investor while maximizing the return at that level of risk. Thus, the

level of diversification which can be received by investments in the portfolio depend on the

correlation among the securities. Thus the lower the correlation the higher the diversification

from the portfolio, while higher the correlation the lesser the diversification from the

portfolio (Grinold 2018).

Minimum Variance Portfolio

Minimum variance portfolio shows the maximum return that an investors can well get

with the help of lowest possible set of risks. The optimal risky portfolio is the suitable

portfolio for the investor as per his risk return profile and should be used for the investment

purpose. However, with the change of the risk return preference of the investor the optimal

risky portfolio changes as the capital allocation line changes for the investor. The minimum

variance portfolio highlights the level of risk and seeks to provide the investor with a

portfolio which has the lowest level of risk and is suitable for a risk hating investor who does

not wish to take excessive risk (Larrain and Stumpner 2017). The return generated by the

minimum variance portfolio has been around -2.08% and the level of risk at the same time for

the portfolio has been around 12.31%.

The optimal portfolio seeks to provide the highest reward in terms of risk undertaken

by the investor and is a suitable investment for a rational investor. The minimum variance

portfolio seeks to lower the risk for the investor without considering the return factor from

the investment. As this is highlighted in the graph above the minimum variance portfolio

provides a negative return while reducing the risk from the portfolio (Christensen, Irle and

Ludwig 2017).

Diversification in Portfolio

The diversification is an important aspect of portfolio management which seeks to

reduce the risk of the investor while maximizing the return at that level of risk. Thus, the

level of diversification which can be received by investments in the portfolio depend on the

correlation among the securities. Thus the lower the correlation the higher the diversification

from the portfolio, while higher the correlation the lesser the diversification from the

portfolio (Grinold 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9PORTFOLIO MANAGEMENT

The diversification of the portfolio does not only limits itself to the securities but can

also extend asset classes. As per the Empirical theory suggest the equity asset class have a

lower or negative correlation with the bond asset class, while it has a 0 or lower positive

correlation with the alternative investment asset class. Thus greater diversification benefits

are achieved in a portfolio when different asset classes comprise the portfolio coupled with

securities which also have lower correlation. The investor then tends to reduce risk

substantially without foregoing the level of return (Maheshwari, Gupta and Li 2018).

However, equity is also classified as domestic and international which tends to have

higher correlation, while bonds can be risk free bonds or junk bonds which also have a higher

correlation. Thus, the selection of the asset class which is suitable for the investors risk

tolerance level is of utmost importance for the portfolio manager which is followed by the

selection of securities by the portfolio manager (Anderson, Ward and Shelton 2017).

The benefit of diversification can be well explained with the help of the above optimal

portfolio developed above. The return generated by the United Overseas Bank Ltd has been

around 4.60% and the associated standard deviation for the stock was around 18.7%.

However, at the same time from the portfolio perspective this can be well seen that the return

generated by the optimal portfolio has been around 4.62% with a standard deviation of

18.7%. So from a portfolio perspective with the same level of risk the investor is able to

generate a consistent or a better set of return, this would not allow the investor to diversify its

investment but also increase the return which the investors will be earning by taking a single

unit of risk. Application of diversification can be well seen with the help of the above

portfolio process where it has well satisfied the rule and condition of modifying the return

while lowering or maintain the same level of risk. Diversification of investments into a group

of stocks would in turn be allowing the investors to get a better set of risk and reduce the

unsystematic risk that is associated with the stock.

The diversification of the portfolio does not only limits itself to the securities but can

also extend asset classes. As per the Empirical theory suggest the equity asset class have a

lower or negative correlation with the bond asset class, while it has a 0 or lower positive

correlation with the alternative investment asset class. Thus greater diversification benefits

are achieved in a portfolio when different asset classes comprise the portfolio coupled with

securities which also have lower correlation. The investor then tends to reduce risk

substantially without foregoing the level of return (Maheshwari, Gupta and Li 2018).

However, equity is also classified as domestic and international which tends to have

higher correlation, while bonds can be risk free bonds or junk bonds which also have a higher

correlation. Thus, the selection of the asset class which is suitable for the investors risk

tolerance level is of utmost importance for the portfolio manager which is followed by the

selection of securities by the portfolio manager (Anderson, Ward and Shelton 2017).

The benefit of diversification can be well explained with the help of the above optimal

portfolio developed above. The return generated by the United Overseas Bank Ltd has been

around 4.60% and the associated standard deviation for the stock was around 18.7%.

However, at the same time from the portfolio perspective this can be well seen that the return

generated by the optimal portfolio has been around 4.62% with a standard deviation of

18.7%. So from a portfolio perspective with the same level of risk the investor is able to

generate a consistent or a better set of return, this would not allow the investor to diversify its

investment but also increase the return which the investors will be earning by taking a single

unit of risk. Application of diversification can be well seen with the help of the above

portfolio process where it has well satisfied the rule and condition of modifying the return

while lowering or maintain the same level of risk. Diversification of investments into a group

of stocks would in turn be allowing the investors to get a better set of risk and reduce the

unsystematic risk that is associated with the stock.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10PORTFOLIO MANAGEMENT

Conclusion

The report provides the concepts of modern portfolio theory which is used by

portfolio managers in the portfolio management process. The importance of diversification

benefits has been observed in the above report in the portfolio management process. The

diversification benefits which is received when selecting different asset classes is highlighted

in the above report. The securities which have been selected in the above portfolio have also

provided diversification benefits due to the low correlation among them. The correlation is an

important factor which provides benefits of diversification to a portfolio.

The efficient frontier which is the opportunity set which is available with the investor

using the two securities in the portfolio. The capital allocation line has well highlighted the

ways in which the investor can invest the capital which the investor has in the portfolio. The

portfolio which forms a tangent with the capital allocation line is the optimal risky portfolio,

while the minimum variance portfolio tends to reduce the risk in a portfolio.

Conclusion

The report provides the concepts of modern portfolio theory which is used by

portfolio managers in the portfolio management process. The importance of diversification

benefits has been observed in the above report in the portfolio management process. The

diversification benefits which is received when selecting different asset classes is highlighted

in the above report. The securities which have been selected in the above portfolio have also

provided diversification benefits due to the low correlation among them. The correlation is an

important factor which provides benefits of diversification to a portfolio.

The efficient frontier which is the opportunity set which is available with the investor

using the two securities in the portfolio. The capital allocation line has well highlighted the

ways in which the investor can invest the capital which the investor has in the portfolio. The

portfolio which forms a tangent with the capital allocation line is the optimal risky portfolio,

while the minimum variance portfolio tends to reduce the risk in a portfolio.

11PORTFOLIO MANAGEMENT

References:

Anderson, S.C., Ward, E.J., Shelton, A.O., Adkison, M.D., Beaudreau, A.H., Brenner, R.E.,

Haynie, A.C., Shriver, J.C., Watson, J.T. and Williams, B.C., 2017. Benefits and risks of

diversification for individual fishers. Proceedings of the National Academy of

Sciences, 114(40), pp.10797-10802.

Birthal, P.S. and Hazrana, J., 2019. Crop diversification and resilience of agriculture to

climatic shocks: evidence from India. Agricultural systems, 173, pp.345-354.

Bodnar, T., Parolya, N. and Schmid, W., 2018. Estimation of the global minimum variance

portfolio in high dimensions. European Journal of Operational Research, 266(1), pp.371-

390.

Branger, N., Lučivjanská, K. and Weissensteiner, A., 2019. Optimal granularity for portfolio

choice. Journal of Empirical Finance, 50, pp.125-146.

Cai, T.T., Hu, J., Li, Y. and Zheng, X., 2020. High-dimensional minimum variance portfolio

estimation based on high-frequency data. Journal of Econometrics, 214(2), pp.482-494.

Christensen, S., Irle, A. and Ludwig, A., 2017. Optimal portfolio selection under vanishing

fixed transaction costs. Advances in Applied Probability, 49(4), pp.1116-1143.

Cui, H., Gao, Z., Kim, Y.J. and Shi, Y., 2017. Review on Capital Allocation Principles.

Grinold, R., 2018. Linear Trading Rules for Portfolio Management. The Journal of Portfolio

Management, 44(6), pp.109-119.

Henry, C., 2017. Managing Natural Capital in Line with Malinvaud's Approach to Efficient

Allocation of Capital. Annals of Economics and Statistics/Annales d'Économie et de

Statistique, (125/126), pp.165-168.

References:

Anderson, S.C., Ward, E.J., Shelton, A.O., Adkison, M.D., Beaudreau, A.H., Brenner, R.E.,

Haynie, A.C., Shriver, J.C., Watson, J.T. and Williams, B.C., 2017. Benefits and risks of

diversification for individual fishers. Proceedings of the National Academy of

Sciences, 114(40), pp.10797-10802.

Birthal, P.S. and Hazrana, J., 2019. Crop diversification and resilience of agriculture to

climatic shocks: evidence from India. Agricultural systems, 173, pp.345-354.

Bodnar, T., Parolya, N. and Schmid, W., 2018. Estimation of the global minimum variance

portfolio in high dimensions. European Journal of Operational Research, 266(1), pp.371-

390.

Branger, N., Lučivjanská, K. and Weissensteiner, A., 2019. Optimal granularity for portfolio

choice. Journal of Empirical Finance, 50, pp.125-146.

Cai, T.T., Hu, J., Li, Y. and Zheng, X., 2020. High-dimensional minimum variance portfolio

estimation based on high-frequency data. Journal of Econometrics, 214(2), pp.482-494.

Christensen, S., Irle, A. and Ludwig, A., 2017. Optimal portfolio selection under vanishing

fixed transaction costs. Advances in Applied Probability, 49(4), pp.1116-1143.

Cui, H., Gao, Z., Kim, Y.J. and Shi, Y., 2017. Review on Capital Allocation Principles.

Grinold, R., 2018. Linear Trading Rules for Portfolio Management. The Journal of Portfolio

Management, 44(6), pp.109-119.

Henry, C., 2017. Managing Natural Capital in Line with Malinvaud's Approach to Efficient

Allocation of Capital. Annals of Economics and Statistics/Annales d'Économie et de

Statistique, (125/126), pp.165-168.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.