Portfolio Management Project: Stock Performance and Risk Analysis

VerifiedAdded on 2020/10/22

|10

|1439

|188

Project

AI Summary

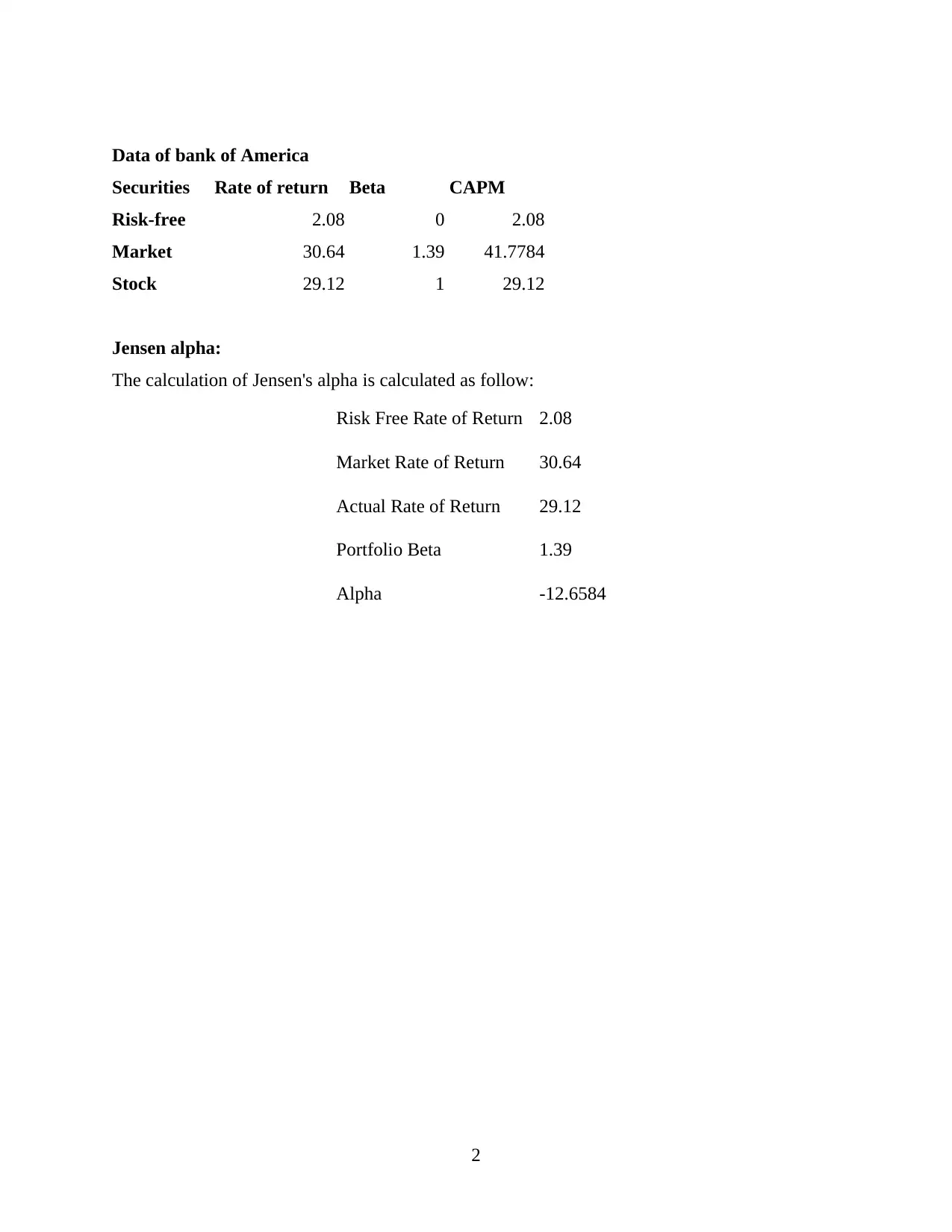

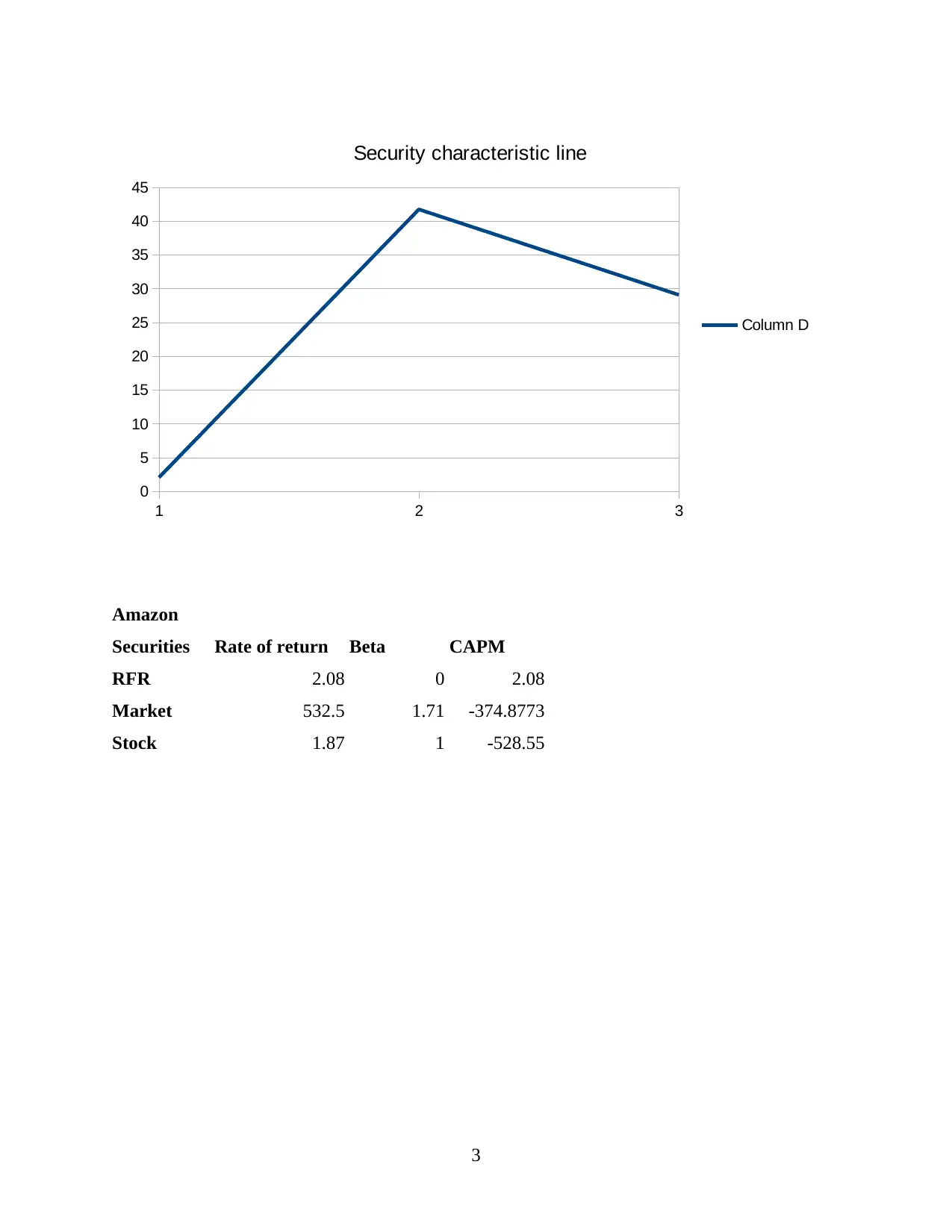

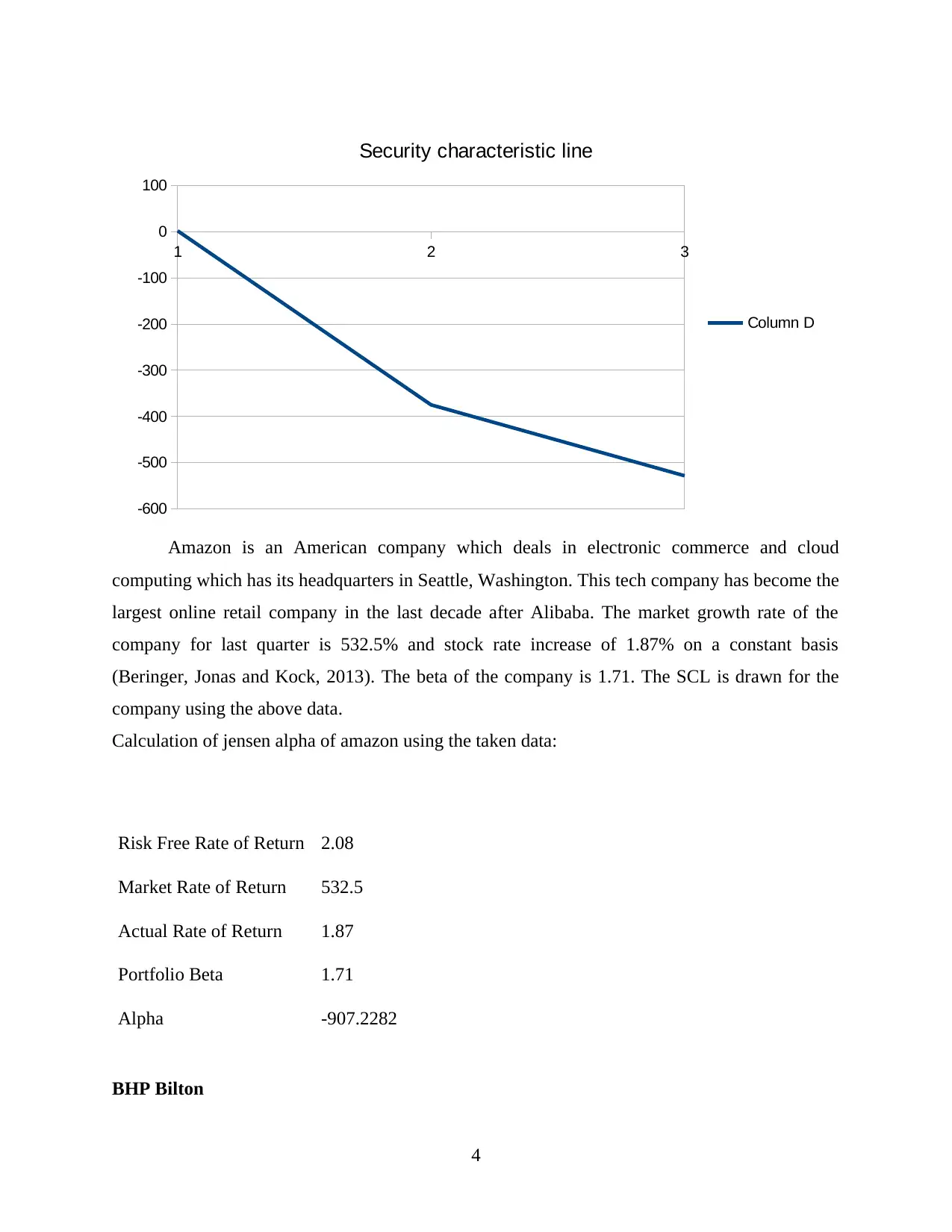

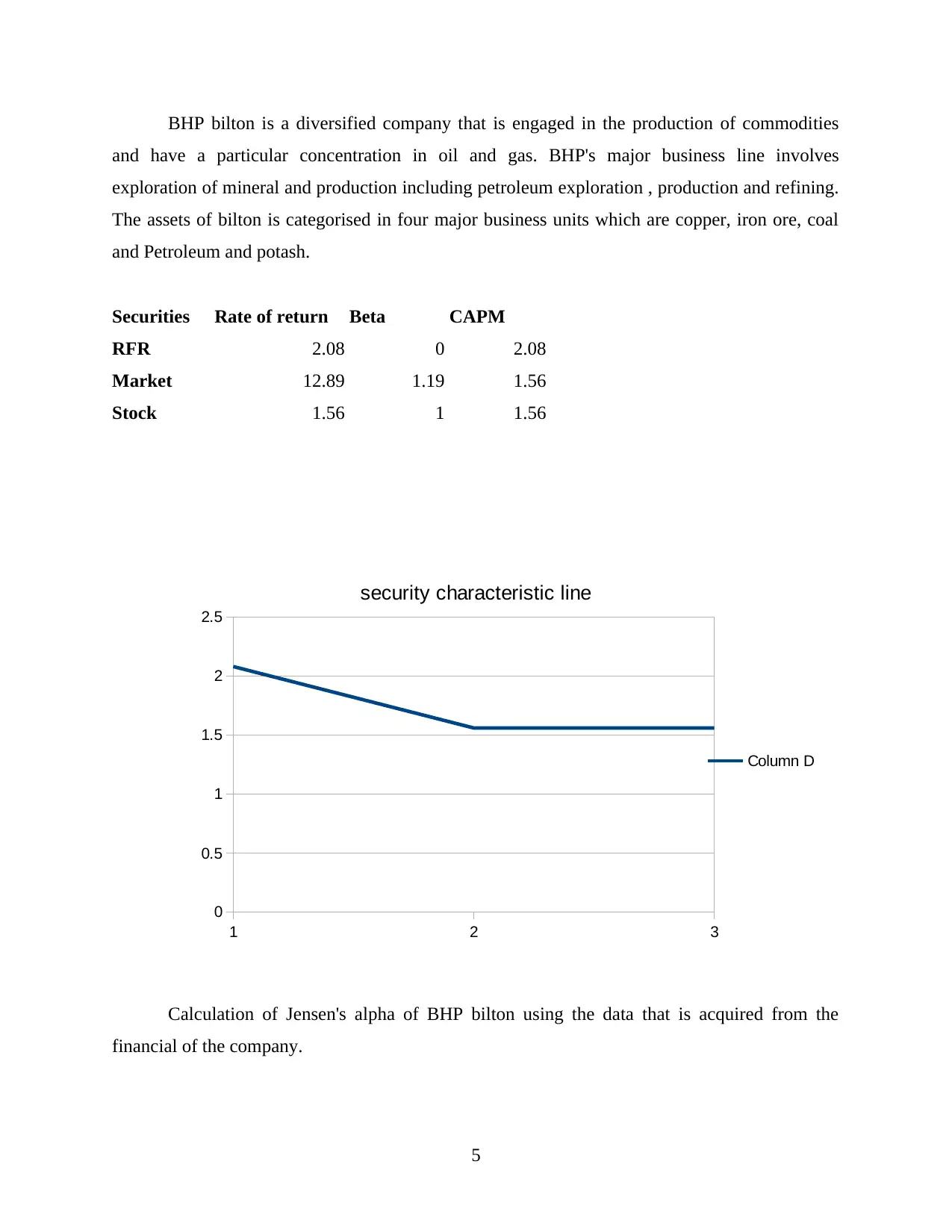

This project is a comprehensive analysis of portfolio management, focusing on the performance of stocks from Bank of America, Amazon, and BHP Bilton. The project begins with an introduction to portfolio management, outlining the process of decision-making, investment planning, and asset allocation. It proceeds to calculate the weekly treasury bill rate, used as a proxy for the risk-free rate, and estimates the security characteristic line (SCL) for each company, using regression analysis in Excel. The project then calculates the beta and Jensen's alpha for each stock, providing insights into their risk and return profiles. Furthermore, it delves into the calculation of total risk, distinguishing between systematic and unsystematic risks. The project comments on each stock's performance based on the calculated data, including market and actual returns. The conclusion summarizes the key findings, emphasizing the use of SCL and Jensen's alpha in assessing stock performance and risk. The project references various financial journals and books to support its analysis, providing a solid foundation for understanding portfolio management principles and their application to real-world stocks.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.