School of Business FINANCE Assignment 3: Portfolio and Bonds

VerifiedAdded on 2023/05/31

|5

|913

|208

Homework Assignment

AI Summary

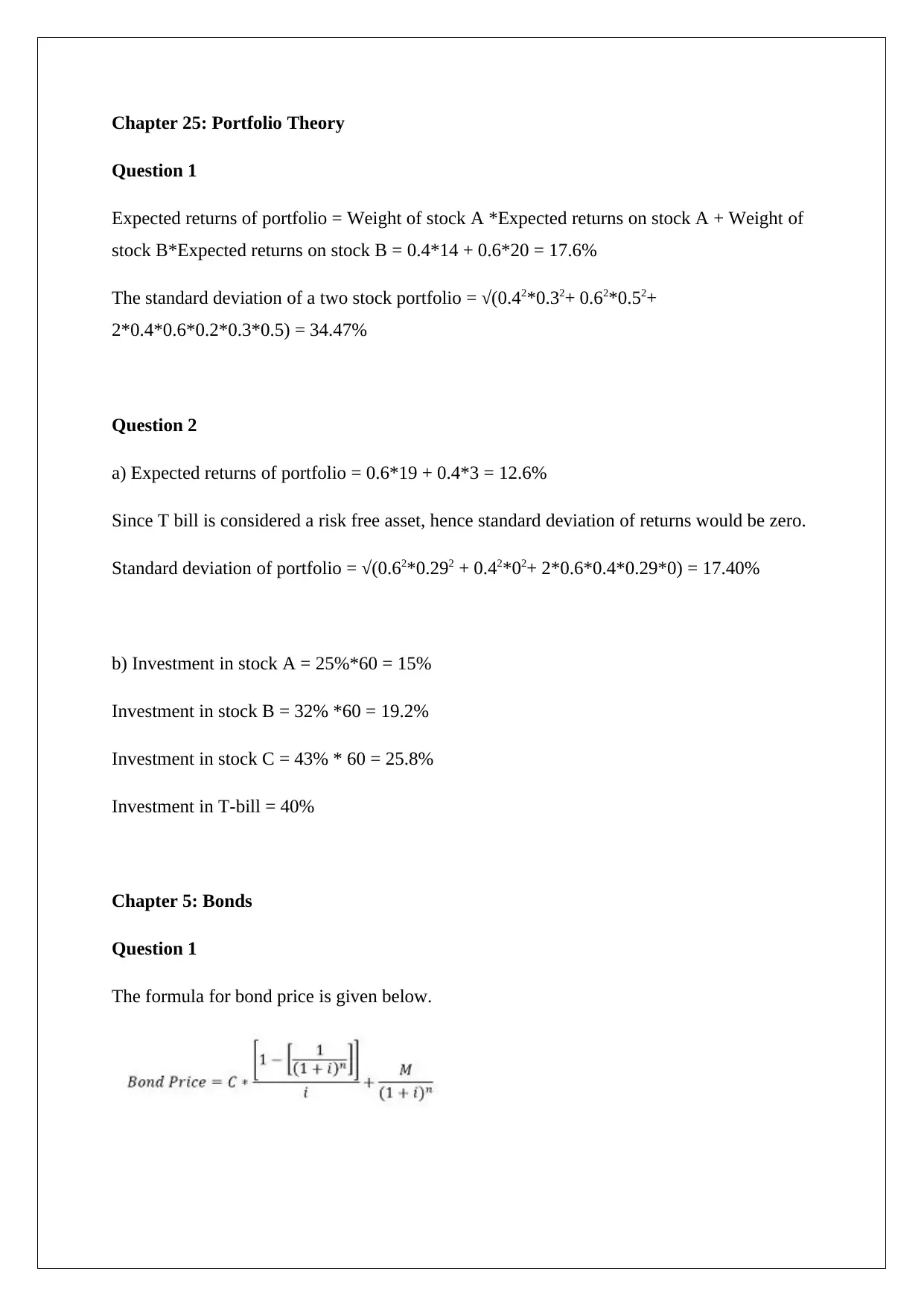

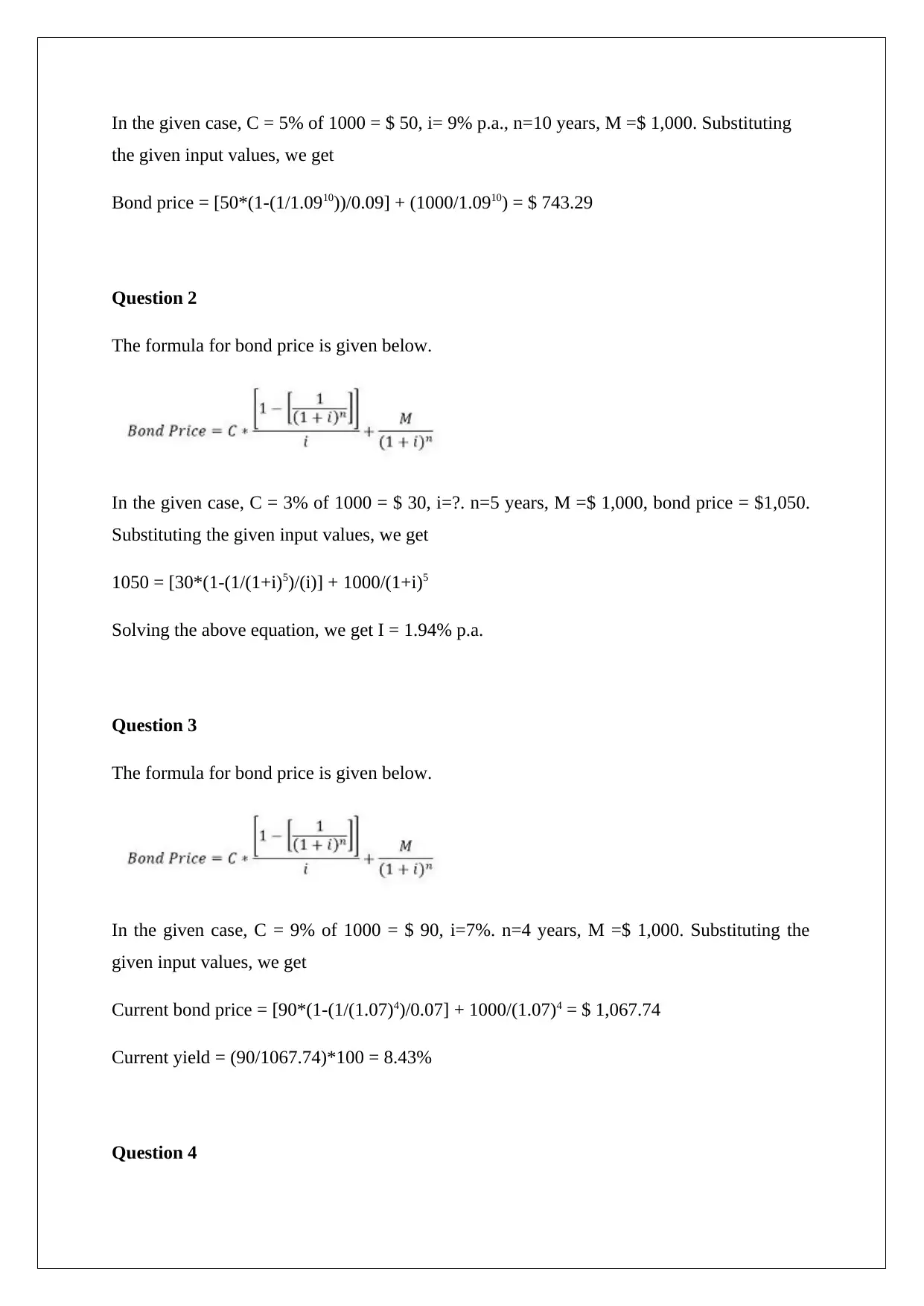

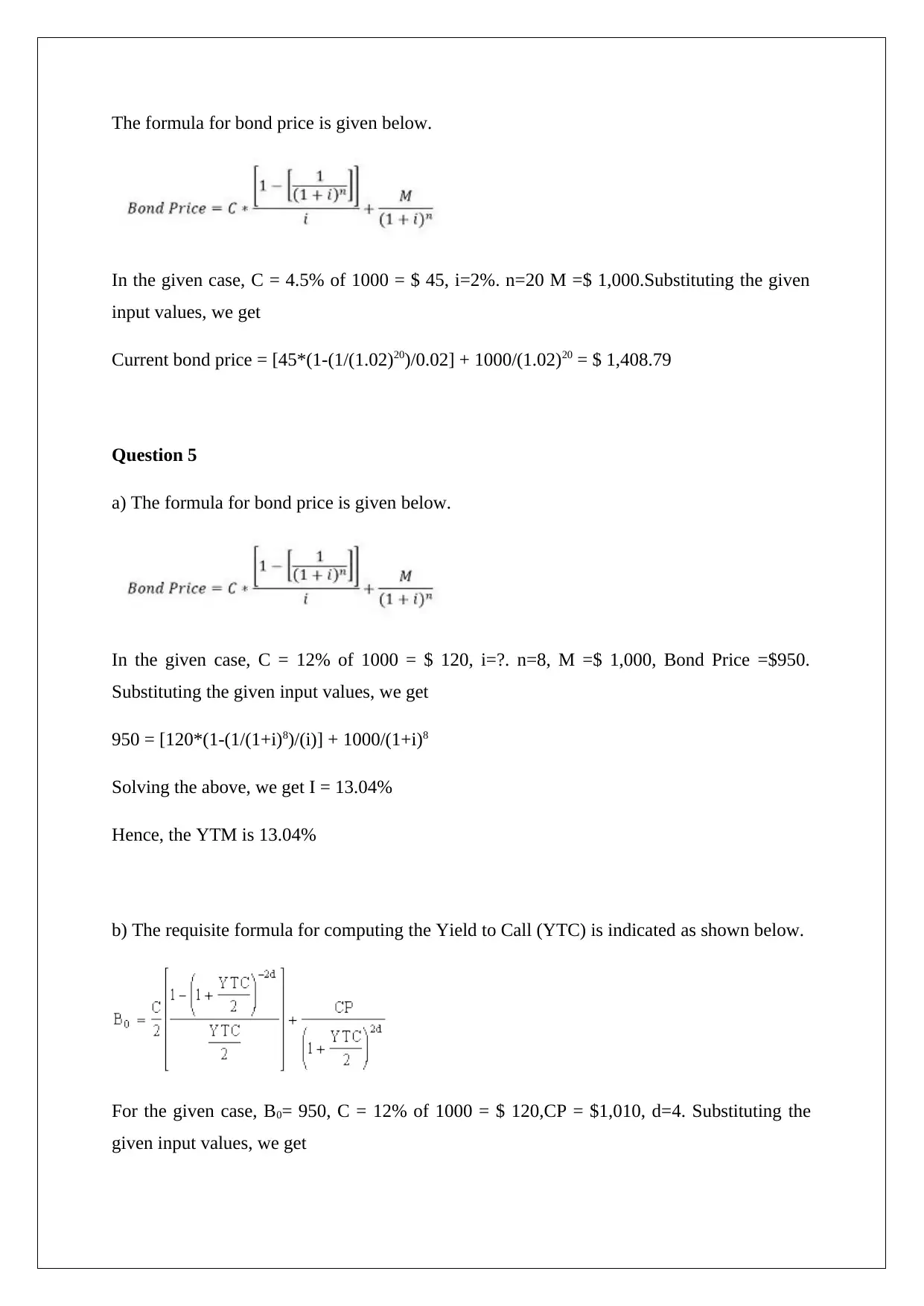

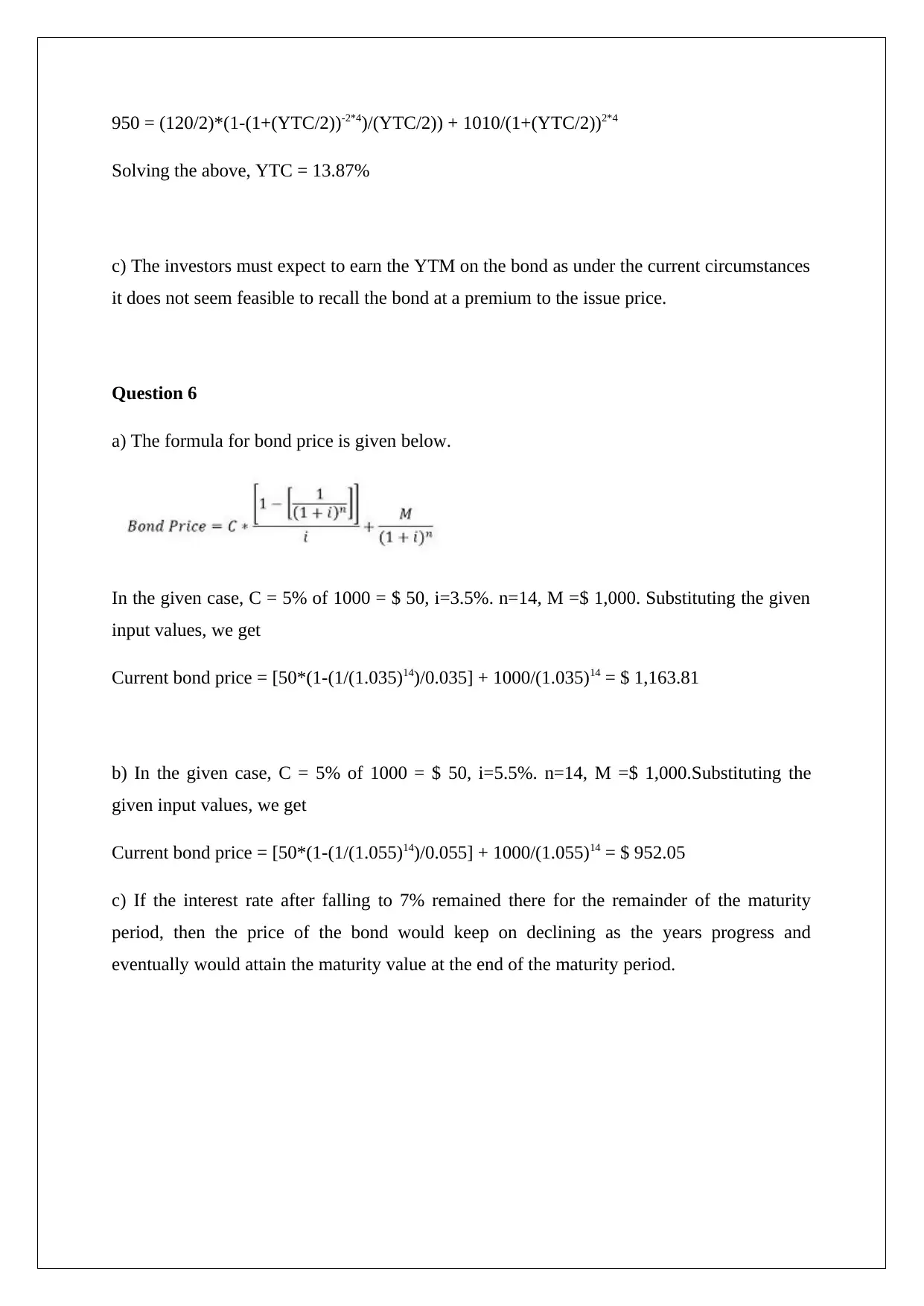

This document provides a comprehensive solution to a Finance assignment focusing on portfolio theory and bond valuation. The assignment covers key concepts such as calculating expected returns and standard deviations for portfolios, as well as determining investment proportions. It also includes detailed calculations for bond pricing, yield to maturity (YTM), and yield to call (YTC). The solutions demonstrate the application of relevant formulas and provide step-by-step explanations for each problem, ensuring a thorough understanding of the concepts. The document provides a complete breakdown of the assignment problems, making it a useful resource for students studying finance. The assignment covers topics from Chapter 25: Portfolio Theory and Chapter 5: Bonds.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.