Portfolio Theory: Modern Approaches to Investment and Risk Analysis

VerifiedAdded on 2023/05/29

|14

|2432

|240

Report

AI Summary

This report delves into portfolio theory, a modern approach for risk-averse investors to optimize returns based on market risk. It highlights that risk is integral to reward and discusses the creation of an efficient frontier of optimal portfolios. The assignment covers risk premium, sources of uncertainty in future payments, and the interdependence of asset allocation decisions. It contrasts conventional and risk-adjusted methods for evaluating portfolio performance, elucidates capital market instruments like shares, debentures, bonds, and derivatives, and outlines the characteristics of a good financial market. The report also differentiates between primary and secondary capital markets, explores the purposes of security market indexes, and defines the efficient capital market theory. Finally, it discusses industry analysis, using tools like ratio analysis and Porter's five forces model, and evaluates the impact of the business cycle on investment decisions, concluding that portfolio theory is crucial for informed investor decision-making.

Running head: PORTFOLIO THEORY

Portfolio Theory

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Portfolio Theory

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1PORTFOLIO THEORY

Table of Contents

Introduction:....................................................................................................................................3

Question 1:.......................................................................................................................................3

Part A:..........................................................................................................................................3

Requirement i:.........................................................................................................................3

Requirement ii:........................................................................................................................3

Part B:..........................................................................................................................................4

Question 2:.......................................................................................................................................4

Part A:..........................................................................................................................................4

Part B:..........................................................................................................................................5

Question 3:.......................................................................................................................................6

Part A:..........................................................................................................................................6

Question 4:.......................................................................................................................................7

Part A:..........................................................................................................................................7

Requirement i:.........................................................................................................................7

Requirement ii:........................................................................................................................7

Requirement iii:.......................................................................................................................8

Question 5:.......................................................................................................................................8

Requirement i:.............................................................................................................................8

Table of Contents

Introduction:....................................................................................................................................3

Question 1:.......................................................................................................................................3

Part A:..........................................................................................................................................3

Requirement i:.........................................................................................................................3

Requirement ii:........................................................................................................................3

Part B:..........................................................................................................................................4

Question 2:.......................................................................................................................................4

Part A:..........................................................................................................................................4

Part B:..........................................................................................................................................5

Question 3:.......................................................................................................................................6

Part A:..........................................................................................................................................6

Question 4:.......................................................................................................................................7

Part A:..........................................................................................................................................7

Requirement i:.........................................................................................................................7

Requirement ii:........................................................................................................................7

Requirement iii:.......................................................................................................................8

Question 5:.......................................................................................................................................8

Requirement i:.............................................................................................................................8

2PORTFOLIO THEORY

Requirement ii:............................................................................................................................9

Requirement iii:...........................................................................................................................9

Question 6:.......................................................................................................................................9

Requirement i:.............................................................................................................................9

Requirement ii:..........................................................................................................................10

Conclusion:....................................................................................................................................11

References:....................................................................................................................................12

Requirement ii:............................................................................................................................9

Requirement iii:...........................................................................................................................9

Question 6:.......................................................................................................................................9

Requirement i:.............................................................................................................................9

Requirement ii:..........................................................................................................................10

Conclusion:....................................................................................................................................11

References:....................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3PORTFOLIO THEORY

Introduction:

Portfolio theory could be deemed as a modern theory focusing on the ways through

which the risk-averse investors could form portfolios for maximising or optimising expected

return depending on a provided market risk level. This emphasises that risk is a significant part

of greater reward1. The theory states that an efficient frontier of optimal portfolios could be

developed providing the maximum expected return for a provided risk level. This assignment

would shed light on the various aspects of portfolio theory based on the provided scenarios.

Question 1:

Part A:

Requirement i:

Risk premium could be defined as the excess of risk-free return that an investment is

estimated to yield. The risk premium of an asset is a kind of compensation for the investors

tolerating additional risk in contrast to that of an asset, which is risk-free, in a provided

investment. For instance, the enhanced quality corporate bonds that the established organisations

issue earning bigger profits have lower default risk.

Requirement ii:

The major sources of uncertainty associated with the future payments include the

following:

Unpredictability of future events:

1 M. Capiński and P Kopp, Portfolio theory and risk management. in , Cambridge, Cambridge Univ. Press, 2014.

Introduction:

Portfolio theory could be deemed as a modern theory focusing on the ways through

which the risk-averse investors could form portfolios for maximising or optimising expected

return depending on a provided market risk level. This emphasises that risk is a significant part

of greater reward1. The theory states that an efficient frontier of optimal portfolios could be

developed providing the maximum expected return for a provided risk level. This assignment

would shed light on the various aspects of portfolio theory based on the provided scenarios.

Question 1:

Part A:

Requirement i:

Risk premium could be defined as the excess of risk-free return that an investment is

estimated to yield. The risk premium of an asset is a kind of compensation for the investors

tolerating additional risk in contrast to that of an asset, which is risk-free, in a provided

investment. For instance, the enhanced quality corporate bonds that the established organisations

issue earning bigger profits have lower default risk.

Requirement ii:

The major sources of uncertainty associated with the future payments include the

following:

Unpredictability of future events:

1 M. Capiński and P Kopp, Portfolio theory and risk management. in , Cambridge, Cambridge Univ. Press, 2014.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4PORTFOLIO THEORY

This implies the inability to gain an insight about the future. The analysts might

undertake efforts for addressing the same by estimation; however, the uncertainty might exist

despite of such attempt2.

Limitations on the precision of data:

This implies the inability in gauging many variables having greater degree of precision at

an affordable cost. As a result, the future payments could not be ensured.

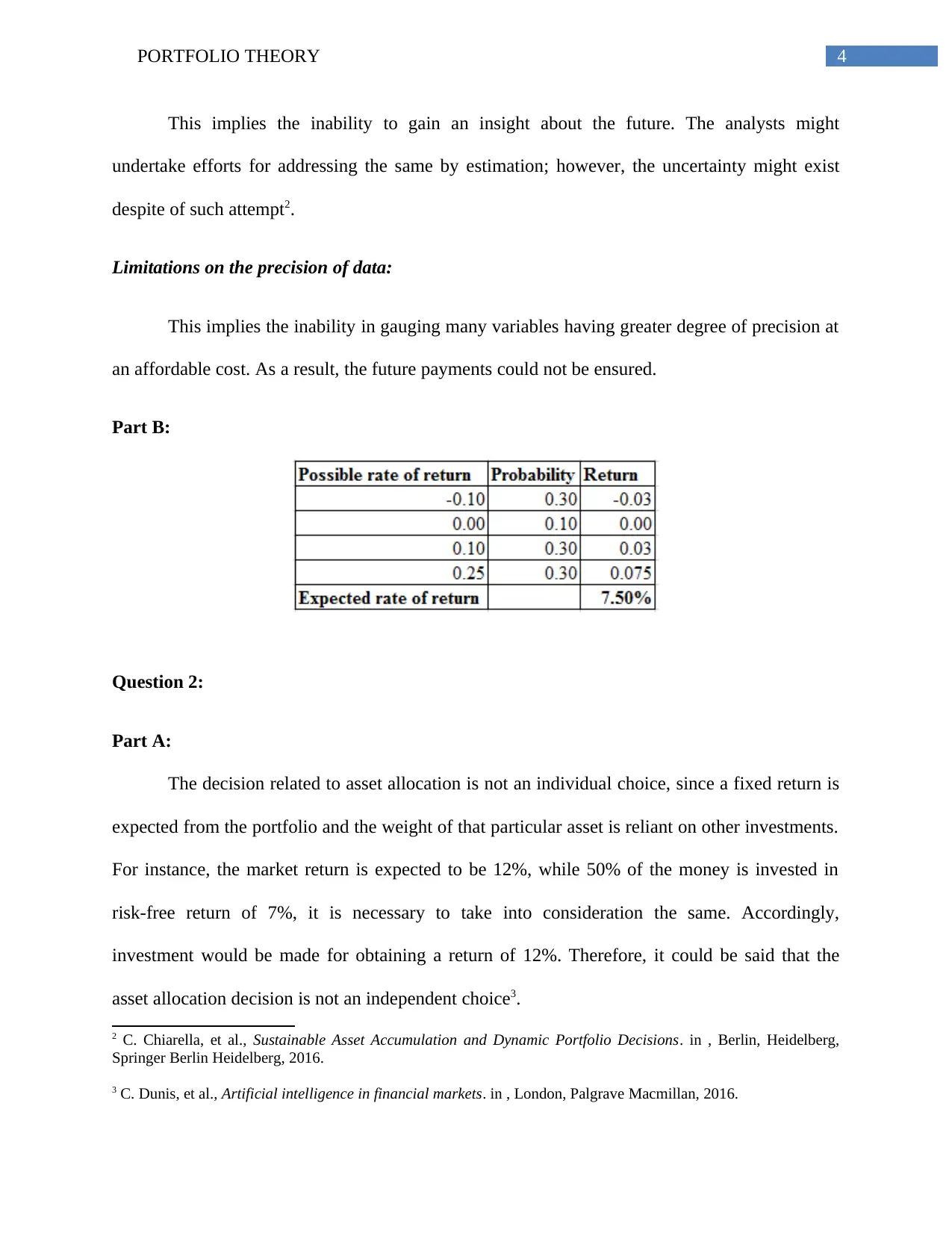

Part B:

Question 2:

Part A:

The decision related to asset allocation is not an individual choice, since a fixed return is

expected from the portfolio and the weight of that particular asset is reliant on other investments.

For instance, the market return is expected to be 12%, while 50% of the money is invested in

risk-free return of 7%, it is necessary to take into consideration the same. Accordingly,

investment would be made for obtaining a return of 12%. Therefore, it could be said that the

asset allocation decision is not an independent choice3.

2 C. Chiarella, et al., Sustainable Asset Accumulation and Dynamic Portfolio Decisions. in , Berlin, Heidelberg,

Springer Berlin Heidelberg, 2016.

3 C. Dunis, et al., Artificial intelligence in financial markets. in , London, Palgrave Macmillan, 2016.

This implies the inability to gain an insight about the future. The analysts might

undertake efforts for addressing the same by estimation; however, the uncertainty might exist

despite of such attempt2.

Limitations on the precision of data:

This implies the inability in gauging many variables having greater degree of precision at

an affordable cost. As a result, the future payments could not be ensured.

Part B:

Question 2:

Part A:

The decision related to asset allocation is not an individual choice, since a fixed return is

expected from the portfolio and the weight of that particular asset is reliant on other investments.

For instance, the market return is expected to be 12%, while 50% of the money is invested in

risk-free return of 7%, it is necessary to take into consideration the same. Accordingly,

investment would be made for obtaining a return of 12%. Therefore, it could be said that the

asset allocation decision is not an independent choice3.

2 C. Chiarella, et al., Sustainable Asset Accumulation and Dynamic Portfolio Decisions. in , Berlin, Heidelberg,

Springer Berlin Heidelberg, 2016.

3 C. Dunis, et al., Artificial intelligence in financial markets. in , London, Palgrave Macmillan, 2016.

5PORTFOLIO THEORY

Part B:

It is not possible to know whether an investment is sound or bad by looking into the

return of the portfolio and thus, it is necessary to compare the same with other investors making

similar investments. There are two standards to evaluate portfolio performance, which are

enumerated briefly as follows:

Conventional method:

This method does not consider the risks undertaken by the portfolio managers. In this

method, the portfolio performance is assessed by contrasting the returns of the portfolio with

those of the benchmark, which could be a market index or another identical portfolio.

Risk-adjusted methods:

In these methods, the portfolio return is contrasted with the benchmark returns by taking

into account the risk level difference. Sharpe ratio and Treynor ratio are the two popular

techniques used to carry out the same.

Question 3:

Part A:

Capital market instruments are long-term financial instruments in the form of equity or

debt, which are traded either on stock exchanges or between the borrowers and the investors.

Capital market instruments are of various types, which include the following:

Shares:

Part B:

It is not possible to know whether an investment is sound or bad by looking into the

return of the portfolio and thus, it is necessary to compare the same with other investors making

similar investments. There are two standards to evaluate portfolio performance, which are

enumerated briefly as follows:

Conventional method:

This method does not consider the risks undertaken by the portfolio managers. In this

method, the portfolio performance is assessed by contrasting the returns of the portfolio with

those of the benchmark, which could be a market index or another identical portfolio.

Risk-adjusted methods:

In these methods, the portfolio return is contrasted with the benchmark returns by taking

into account the risk level difference. Sharpe ratio and Treynor ratio are the two popular

techniques used to carry out the same.

Question 3:

Part A:

Capital market instruments are long-term financial instruments in the form of equity or

debt, which are traded either on stock exchanges or between the borrowers and the investors.

Capital market instruments are of various types, which include the following:

Shares:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6PORTFOLIO THEORY

Shares could be deemed as the share capital of an organisation. It is a unit into which the

business capital is divided. Any individual holding the shares of an organisation is termed as its

shareholders and thus, the person is considered a part of the business owner4. Shares could be

classified further into preference shares and equity shares.

Debentures:

Debentures are those borrowed funds for an organisation, which are for long-term. The

maturity periods and interest rates of the debentures are fixed. More precisely, debentures are the

certificates, which are issued in accordance with the common seal of the organisation.

Bonds:

Bonds are funds borrowed from the government as well as organisations, which are for

long-term. The bonds have fixed interest rates and maturity periods like bonds. The interest,

which is charged on bonds, is considered as the coupon rate.

Derivatives:

Derivatives are derived from other securities and they are termed as underlying assets as

well. The riskiness, function and price of the derivative rely on the underlying assets, as the

factors influencing the underlying assets would influence the derivative as well. For instance,

derivatives include options, swaps, futures and exchange-traded commodities and funds.

4 S. Ellersgaard Nielsen, Essays on rational portfolio theory. in , Copenhagen, Department of Mathematical

Sciences, University of Copenhagen, 2016.

Shares could be deemed as the share capital of an organisation. It is a unit into which the

business capital is divided. Any individual holding the shares of an organisation is termed as its

shareholders and thus, the person is considered a part of the business owner4. Shares could be

classified further into preference shares and equity shares.

Debentures:

Debentures are those borrowed funds for an organisation, which are for long-term. The

maturity periods and interest rates of the debentures are fixed. More precisely, debentures are the

certificates, which are issued in accordance with the common seal of the organisation.

Bonds:

Bonds are funds borrowed from the government as well as organisations, which are for

long-term. The bonds have fixed interest rates and maturity periods like bonds. The interest,

which is charged on bonds, is considered as the coupon rate.

Derivatives:

Derivatives are derived from other securities and they are termed as underlying assets as

well. The riskiness, function and price of the derivative rely on the underlying assets, as the

factors influencing the underlying assets would influence the derivative as well. For instance,

derivatives include options, swaps, futures and exchange-traded commodities and funds.

4 S. Ellersgaard Nielsen, Essays on rational portfolio theory. in , Copenhagen, Department of Mathematical

Sciences, University of Copenhagen, 2016.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7PORTFOLIO THEORY

Question 4:

Part A:

Requirement i:

A financial market is a process by which the purchasers and sellers could communicate

about the pertinent aspects of the transactions. There are agents in the markets, who provide vital

information as well as logistics support for passing over the ownership of the traded securities. A

good financial market possesses the following characteristics:

Correct and quick information for the investors needed for share transactions

Ensuring that there is not variation of prices from one transaction to another until the

availability of new information

Trading is made at prices below and exceeding the existing market price

There is minimum transaction cost

All information regarding demand and supply factors should be readily available5

Requirement ii:

In primary capital market, the investors purchase securities directly from the

organisations issuing them and the organisations mainly use this market when they sell new

bonds and stocks for the first time publicly as initial public offering. The organisations issuing

shares in this market mainly hire investment bankers for gaining commitments from big

institutional investors to buy the securities at the time of initial offering6.

5 E. Elton, et al., Modern portfolio theory and investment analysis. in , Hoboken, NJ, Wiley, 2015.

6 M. Erickson, Asset Rotation. in , New York, NY, John Wiley and Sons, 2014.

Question 4:

Part A:

Requirement i:

A financial market is a process by which the purchasers and sellers could communicate

about the pertinent aspects of the transactions. There are agents in the markets, who provide vital

information as well as logistics support for passing over the ownership of the traded securities. A

good financial market possesses the following characteristics:

Correct and quick information for the investors needed for share transactions

Ensuring that there is not variation of prices from one transaction to another until the

availability of new information

Trading is made at prices below and exceeding the existing market price

There is minimum transaction cost

All information regarding demand and supply factors should be readily available5

Requirement ii:

In primary capital market, the investors purchase securities directly from the

organisations issuing them and the organisations mainly use this market when they sell new

bonds and stocks for the first time publicly as initial public offering. The organisations issuing

shares in this market mainly hire investment bankers for gaining commitments from big

institutional investors to buy the securities at the time of initial offering6.

5 E. Elton, et al., Modern portfolio theory and investment analysis. in , Hoboken, NJ, Wiley, 2015.

6 M. Erickson, Asset Rotation. in , New York, NY, John Wiley and Sons, 2014.

8PORTFOLIO THEORY

Requirement iii:

In secondary capital market, the investors are involved in trading shares among them and

there is no participation of the organisations in such transactions. More precisely, shares are

traded in this market after all stocks and bonds are sold in the primary market7.

Question 5:

Requirement i:

The security market indexes are used for the following purposes:

It could be used in the form of a benchmark for analysing the performance of the

professional money managers

To develop as well as monitor index fund

To gauge the market rate of return in economic analysis

To estimate the movements in the future market by technical experts

It serves in the form of a substitute for the market portfolio of assets that are risky at the

time of computing systematic risk8

Requirement ii:

Efficient capital market could be defined as the market where shares are traded and there

is quick incorporation of new information regarding prices. Despite the fact that this theory is

7 A. Geromichalos and I Simonovska, "Asset liquidity and international portfolio choice.". in Journal of Economic

Theory, 151, 2014, 342-380.

8 C. Jones, "Modern Portfolio Theory, Digital Portfolio Theory and Intertemporal Portfolio Choice.". in SSRN

Electronic Journal, , 2017.

Requirement iii:

In secondary capital market, the investors are involved in trading shares among them and

there is no participation of the organisations in such transactions. More precisely, shares are

traded in this market after all stocks and bonds are sold in the primary market7.

Question 5:

Requirement i:

The security market indexes are used for the following purposes:

It could be used in the form of a benchmark for analysing the performance of the

professional money managers

To develop as well as monitor index fund

To gauge the market rate of return in economic analysis

To estimate the movements in the future market by technical experts

It serves in the form of a substitute for the market portfolio of assets that are risky at the

time of computing systematic risk8

Requirement ii:

Efficient capital market could be defined as the market where shares are traded and there

is quick incorporation of new information regarding prices. Despite the fact that this theory is

7 A. Geromichalos and I Simonovska, "Asset liquidity and international portfolio choice.". in Journal of Economic

Theory, 151, 2014, 342-380.

8 C. Jones, "Modern Portfolio Theory, Digital Portfolio Theory and Intertemporal Portfolio Choice.". in SSRN

Electronic Journal, , 2017.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9PORTFOLIO THEORY

applicable to all kinds of financial securities, it mainly emphasises on one type of security, which

are shares of a common stock in any business organisation9.

Requirement iii:

The capital market theory is based on certain assumptions, which are discussed as

follows:

It becomes easy for the investors to lend or borrow money that are risk-free

All investors in the market are perceived to be efficient

All the investors have the same time horizon

It is possible to divide the assets indefinitely

There is no existence of transaction costs and taxes

Inflation is not considered at all in this theory

All the investors have identical probability for outcomes10

Question 6:

Requirement i:

Industry analysis could be defined as a tool facilitating an organisation in gaining an

understanding of its position compared to the other organisations in the industry offering

identical products or services. This analysis mainly comprises of these elements. They include

underlying forces of work in the industry, overall industry attractiveness and crucial factors

ascertaining the success of an organisation. A technique that could be used to evaluate is by

9 L. MacLean and W Ziemba, Problems in portfolio theory and the fundamentals of financial decision making. in .

10 R. Mansini, W Ogryczak, and M Speranza, Linear and mixed integer programming for portfolio optimization. in ,

Cham, Springer, 2015.

applicable to all kinds of financial securities, it mainly emphasises on one type of security, which

are shares of a common stock in any business organisation9.

Requirement iii:

The capital market theory is based on certain assumptions, which are discussed as

follows:

It becomes easy for the investors to lend or borrow money that are risk-free

All investors in the market are perceived to be efficient

All the investors have the same time horizon

It is possible to divide the assets indefinitely

There is no existence of transaction costs and taxes

Inflation is not considered at all in this theory

All the investors have identical probability for outcomes10

Question 6:

Requirement i:

Industry analysis could be defined as a tool facilitating an organisation in gaining an

understanding of its position compared to the other organisations in the industry offering

identical products or services. This analysis mainly comprises of these elements. They include

underlying forces of work in the industry, overall industry attractiveness and crucial factors

ascertaining the success of an organisation. A technique that could be used to evaluate is by

9 L. MacLean and W Ziemba, Problems in portfolio theory and the fundamentals of financial decision making. in .

10 R. Mansini, W Ogryczak, and M Speranza, Linear and mixed integer programming for portfolio optimization. in ,

Cham, Springer, 2015.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10PORTFOLIO THEORY

contrasting a specific business with the average of all participants in the sector by using ratio

analysis and comparison. Another technique is the Porter’s five forces model, which depends on

certain attributes. These attributes mainly include bargaining power of the suppliers, rivals and

nature of rivalry, bargaining power of the buyers, potential for new entrants and ability of

substitute products11. Despite after assessing if the industry is in maturity stage or declining

stage, it is not a feasible option to invest in the industry. On the other hand, despite performing

well in a slow growth sector or the sector is not performing, as the forces such as climatic,

political and inflation are influencing the sector, it is not viable to invest in the sector.

Requirement ii:

Business cycle, termed as trade cycle or economic scale, is the upward and downward

movement of the gross domestic product (GDP) around its long-term trend of growth. The

business cycle duration is the timeframe containing only one contraction and boom in place.

Such cycle is gauged by taking into account the real GDP growth rate. If any business is

associated with infrastructure in a developing nation, then the investment is advantageous, since

the nation requires infrastructure greatly12.

Conclusion:

It is evaluated from the above discussion that portfolio theory plays a crucial role in the

decision-making process of the investors. This is because it takes into account all the risks and

returns that the investors could earn by evaluating the stock market scenarios and industrial

nature.

11 K. Shell, Portfolio Theory. in , Elsevier Science, 2014.

12 F. Viole, "Portfolio Theory.". in SSRN Electronic Journal, , 2016.

contrasting a specific business with the average of all participants in the sector by using ratio

analysis and comparison. Another technique is the Porter’s five forces model, which depends on

certain attributes. These attributes mainly include bargaining power of the suppliers, rivals and

nature of rivalry, bargaining power of the buyers, potential for new entrants and ability of

substitute products11. Despite after assessing if the industry is in maturity stage or declining

stage, it is not a feasible option to invest in the industry. On the other hand, despite performing

well in a slow growth sector or the sector is not performing, as the forces such as climatic,

political and inflation are influencing the sector, it is not viable to invest in the sector.

Requirement ii:

Business cycle, termed as trade cycle or economic scale, is the upward and downward

movement of the gross domestic product (GDP) around its long-term trend of growth. The

business cycle duration is the timeframe containing only one contraction and boom in place.

Such cycle is gauged by taking into account the real GDP growth rate. If any business is

associated with infrastructure in a developing nation, then the investment is advantageous, since

the nation requires infrastructure greatly12.

Conclusion:

It is evaluated from the above discussion that portfolio theory plays a crucial role in the

decision-making process of the investors. This is because it takes into account all the risks and

returns that the investors could earn by evaluating the stock market scenarios and industrial

nature.

11 K. Shell, Portfolio Theory. in , Elsevier Science, 2014.

12 F. Viole, "Portfolio Theory.". in SSRN Electronic Journal, , 2016.

11PORTFOLIO THEORY

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.