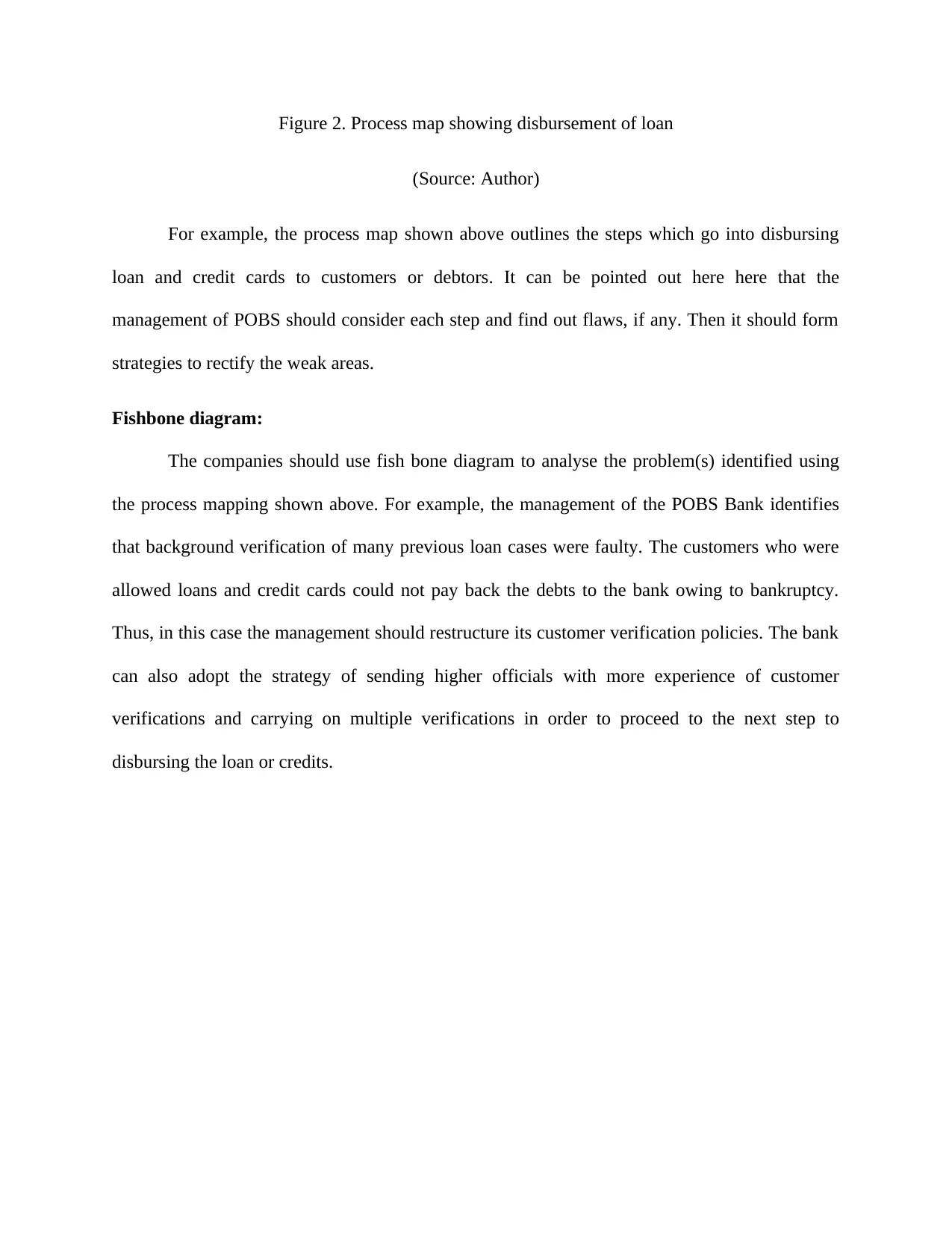

Financial Analysis: POSB Bank's Operations, Six Sigma & TQM Strategies

VerifiedAdded on 2023/01/23

|15

|2430

|97

Report

AI Summary

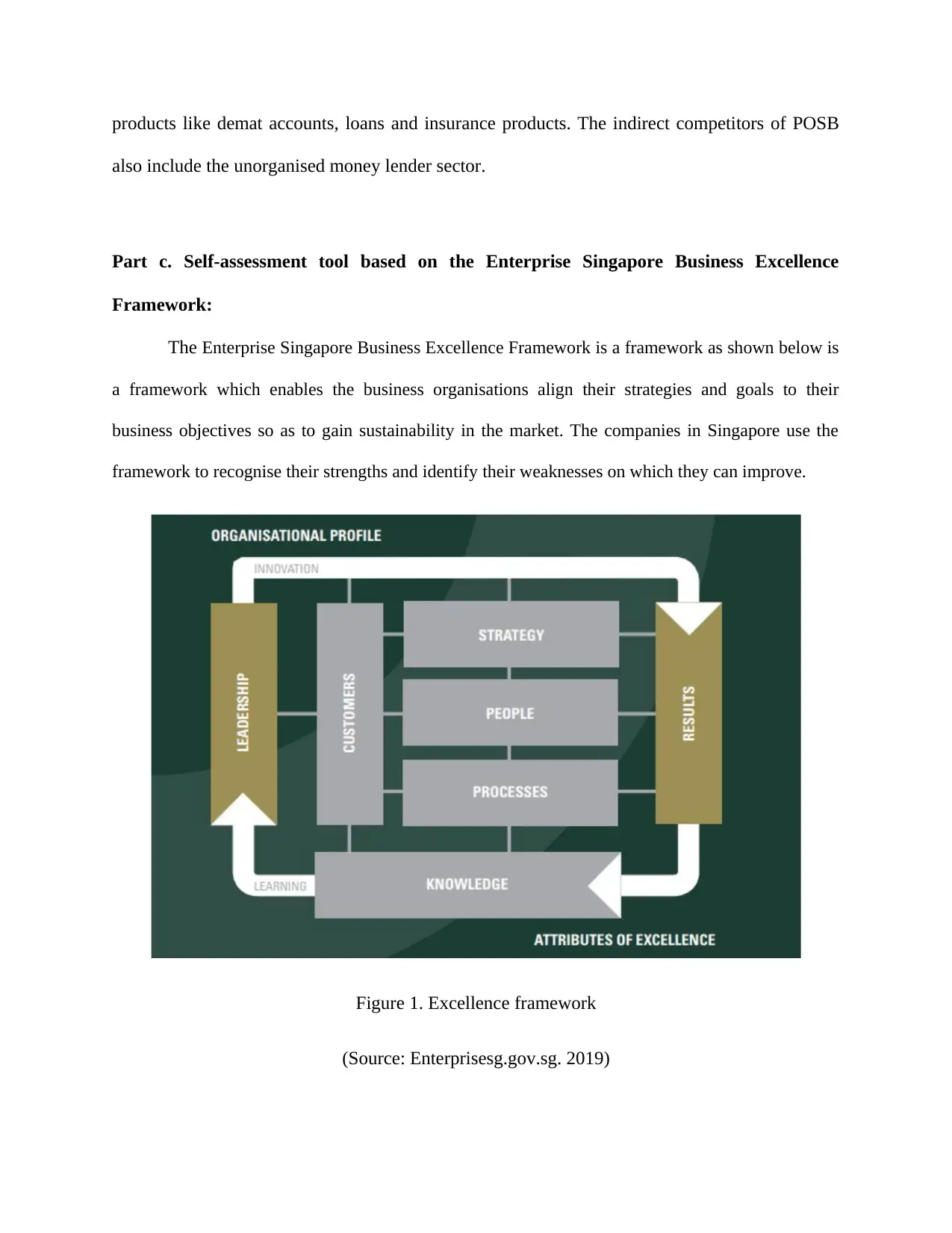

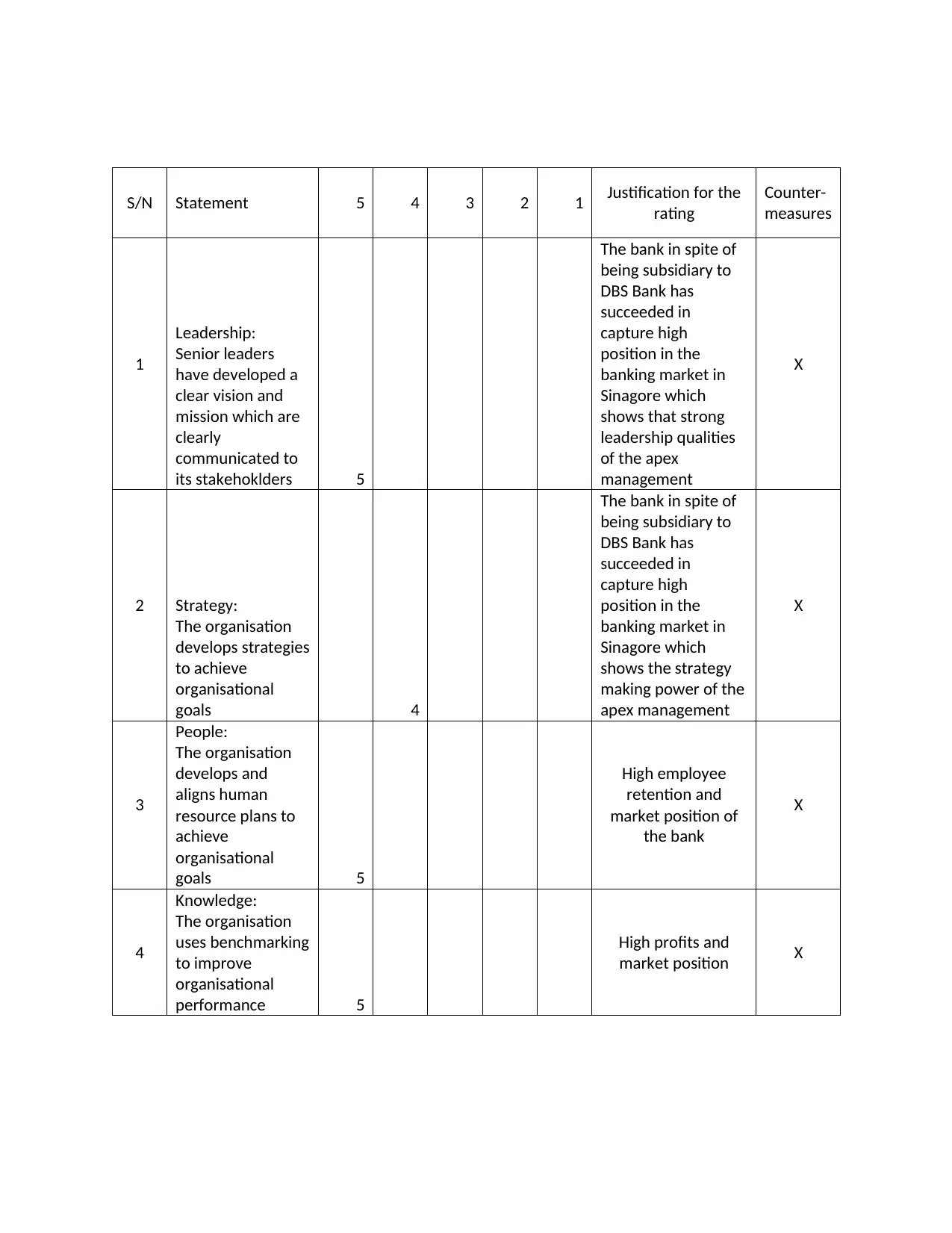

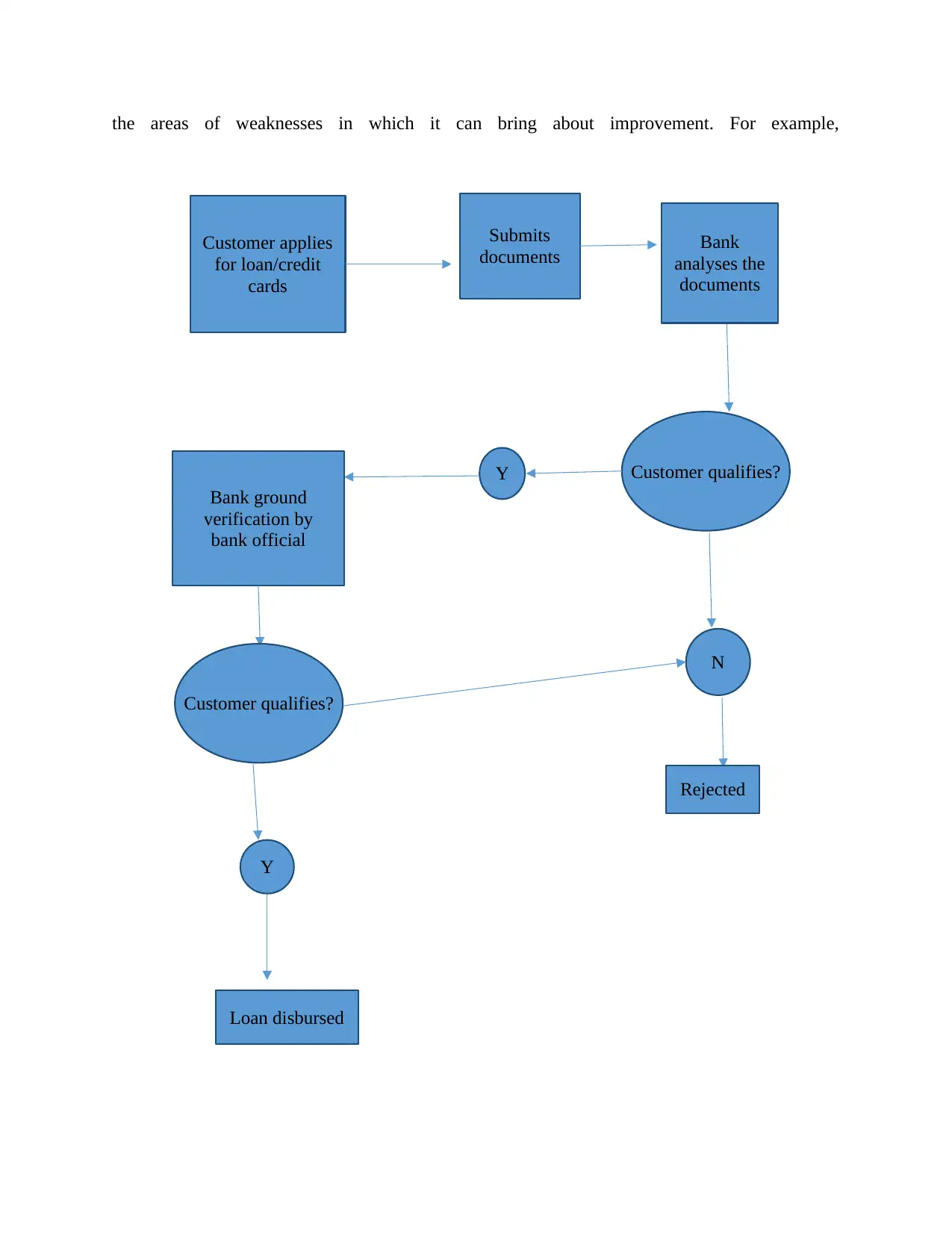

This report provides a comprehensive analysis of POSB Bank, a subsidiary of DBS Bank Limited in Singapore. It begins with an overview of POSB's business operations, detailing its financial products and services categorized into liability and asset groups, including savings accounts, loans, and investment services. The report then identifies key customer segments (business and individual) and suppliers (MasterCard, mobile app developers), along with its main competitors in the Singaporean banking market, such as OCBC Bank and UOB. Furthermore, it applies the Enterprise Singapore Business Excellence Framework to assess POSB's strengths and weaknesses, highlighting areas for improvement. The core of the report focuses on applying Six Sigma and Total Quality Management (TQM) to enhance key areas like reducing accounts receivable aging and improving customer response time. It proposes the use of DMAIC methodology, process mapping, fishbone diagrams, and Pareto charts to identify and address quality issues, ultimately aiming to improve loan recovery and customer satisfaction. The report concludes with a discussion on the importance of lean six sigma applications to deal with losses due to poor quality of loan recovery and a section on a PPT presentation.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.