Exploring the Impact of Positive Accounting Theory on Qantas Airlines

VerifiedAdded on 2020/05/28

|7

|1480

|97

AI Summary

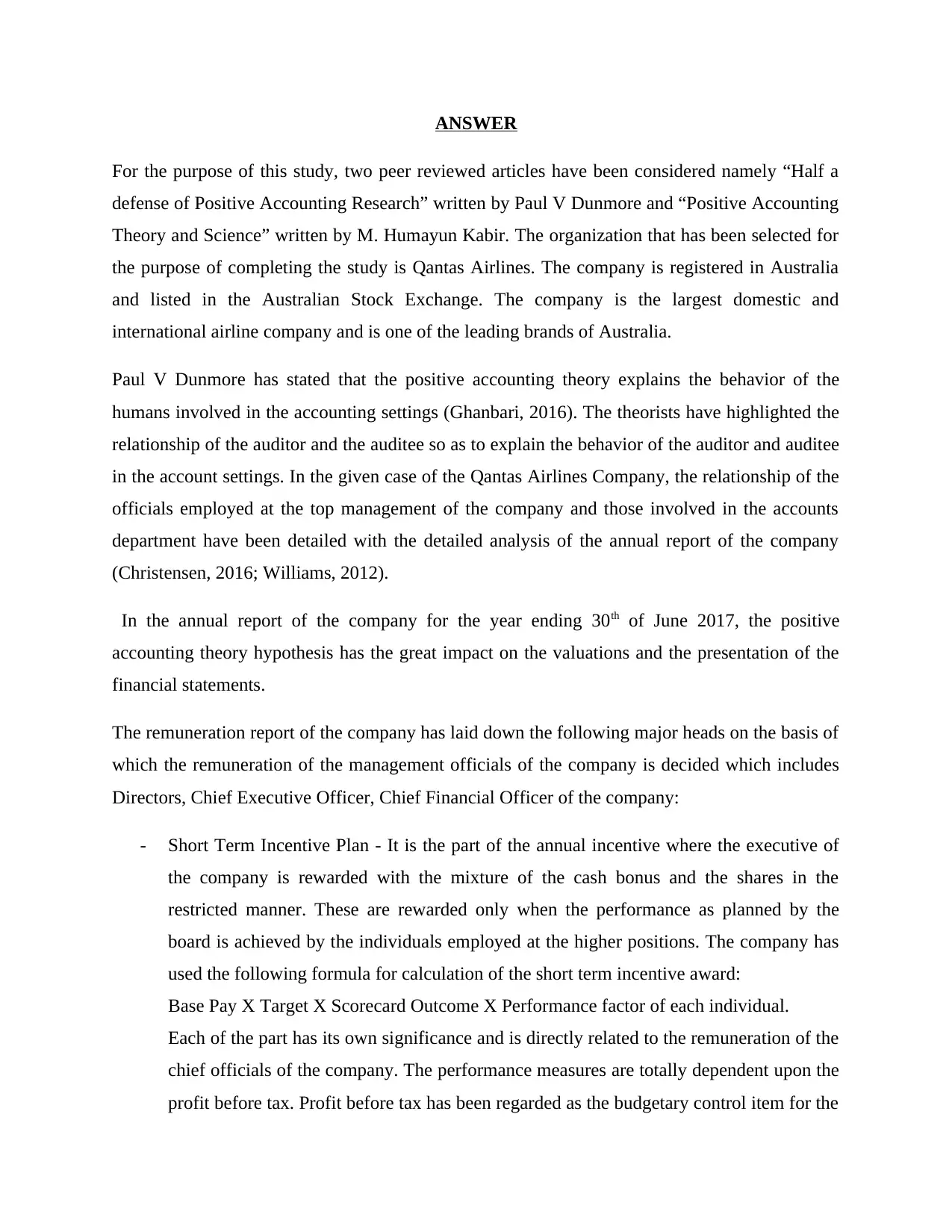

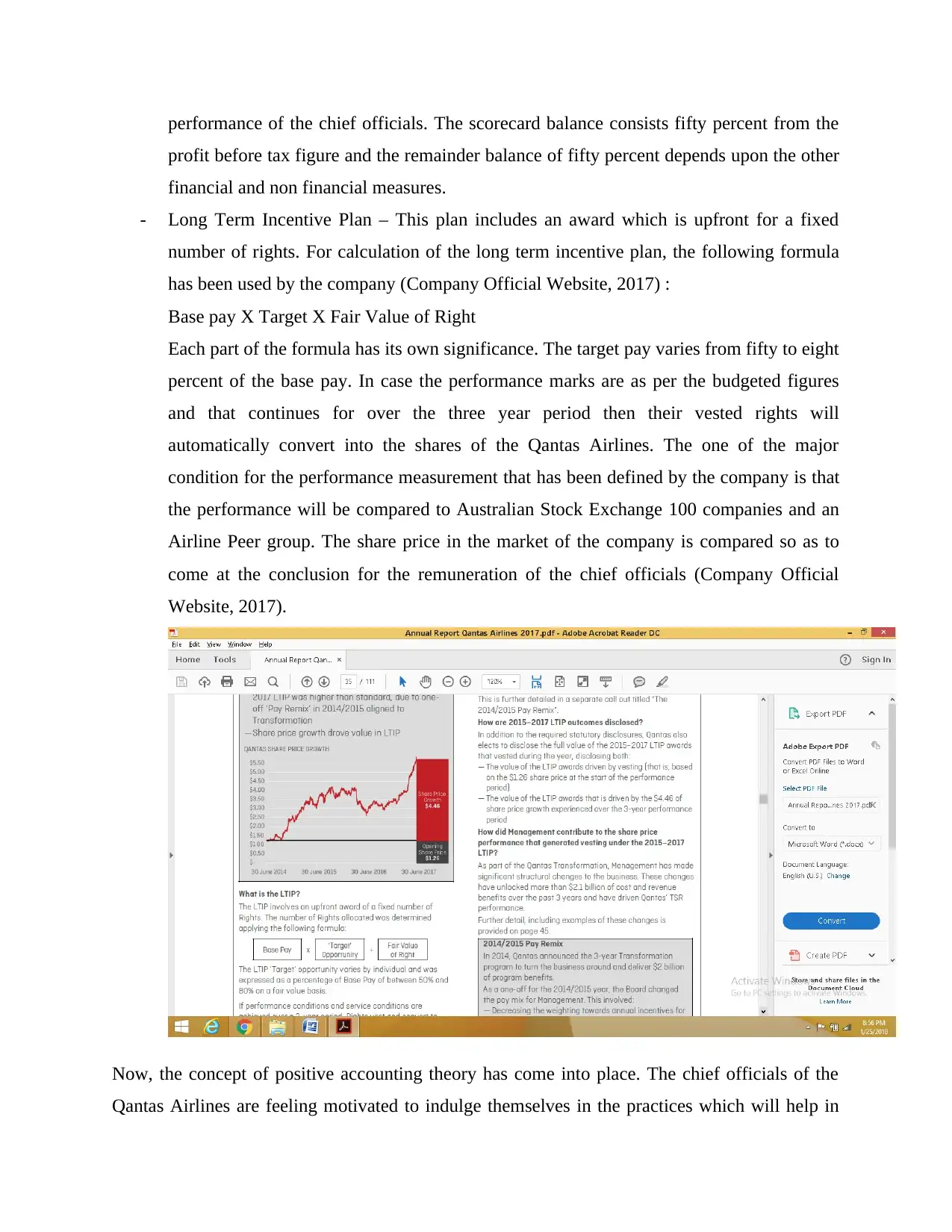

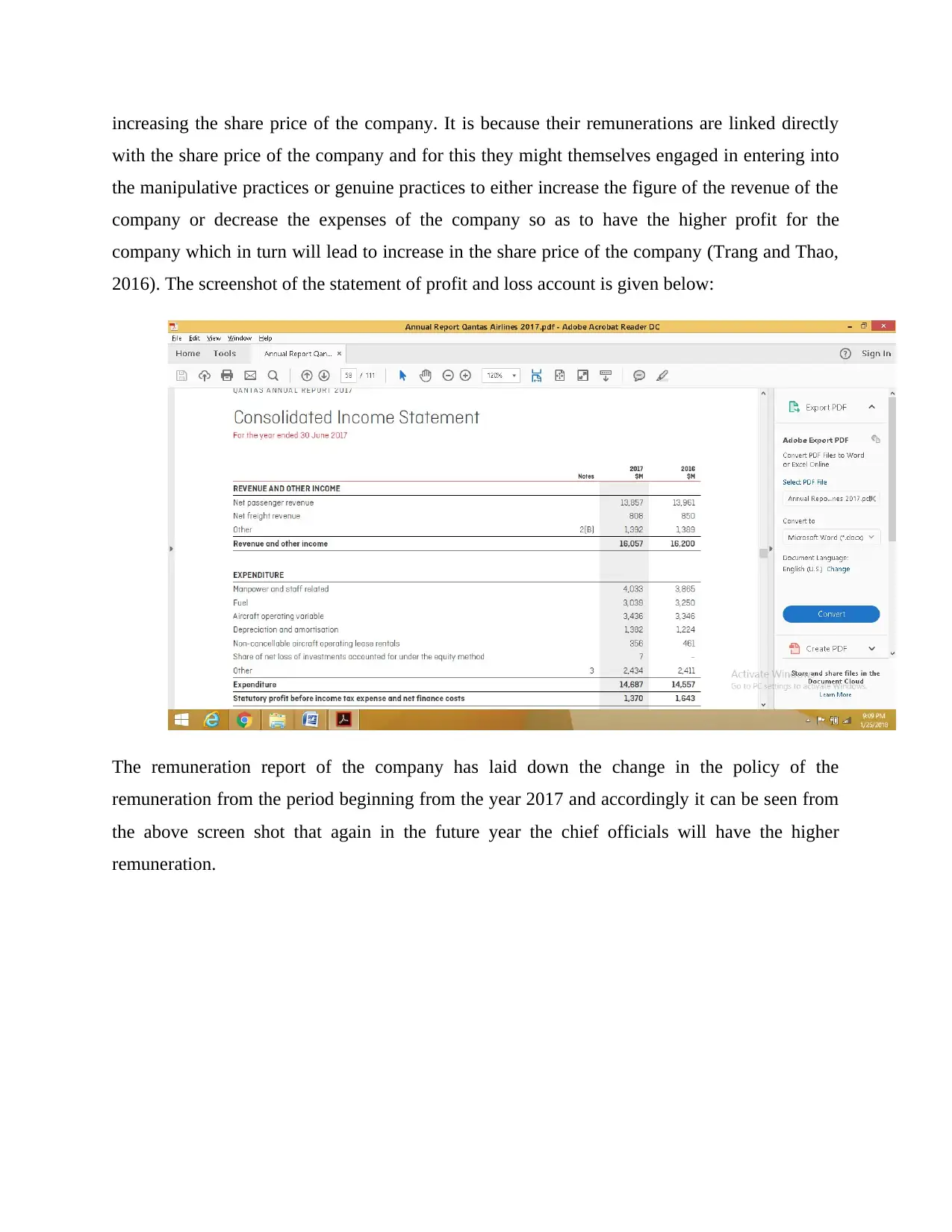

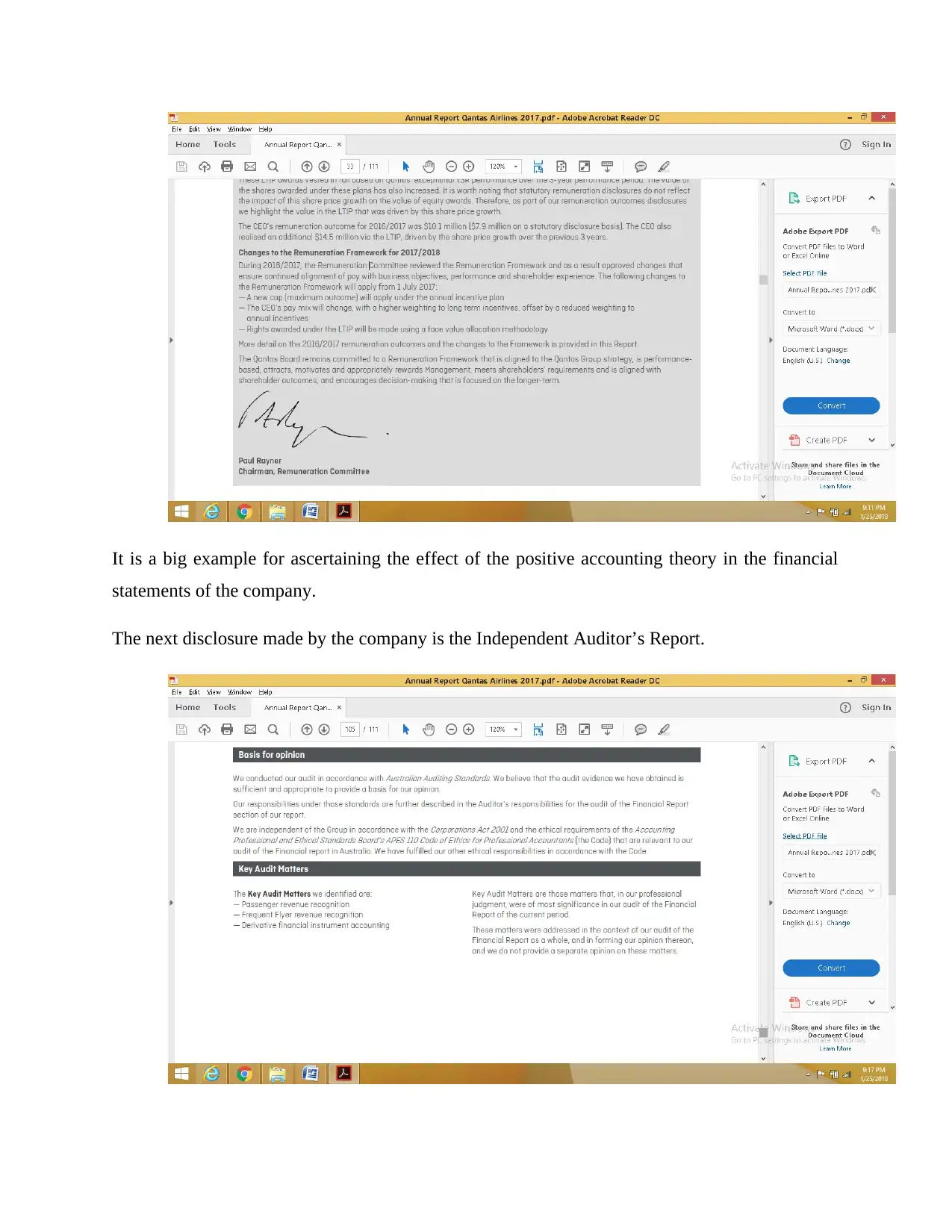

The study explores how Positive Accounting Theory (PAT) explains the behavior of individuals in accounting settings at Qantas Airlines. It analyzes instances from the annual report, such as executive remuneration practices, auditor relationships, and debt covenants, to illustrate how PAT elucidates managerial actions. The findings suggest that executives may engage in manipulative practices influenced by contractual arrangements, which are evident in financial reporting patterns. Additionally, the study highlights potential conflicts of interest with auditors due to additional non-audit fees, aligning with PAT's predictions about auditor behavior under economic incentives. Finally, debt covenant compliance indicates possible managerial strategies to optimize financial ratios. Overall, Positive Accounting Theory provides a valuable framework for understanding these behaviors in Qantas Airlines.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.