An Analysis of Positive and Normative Accounting Theories

VerifiedAdded on 2020/02/03

|8

|2094

|303

Report

AI Summary

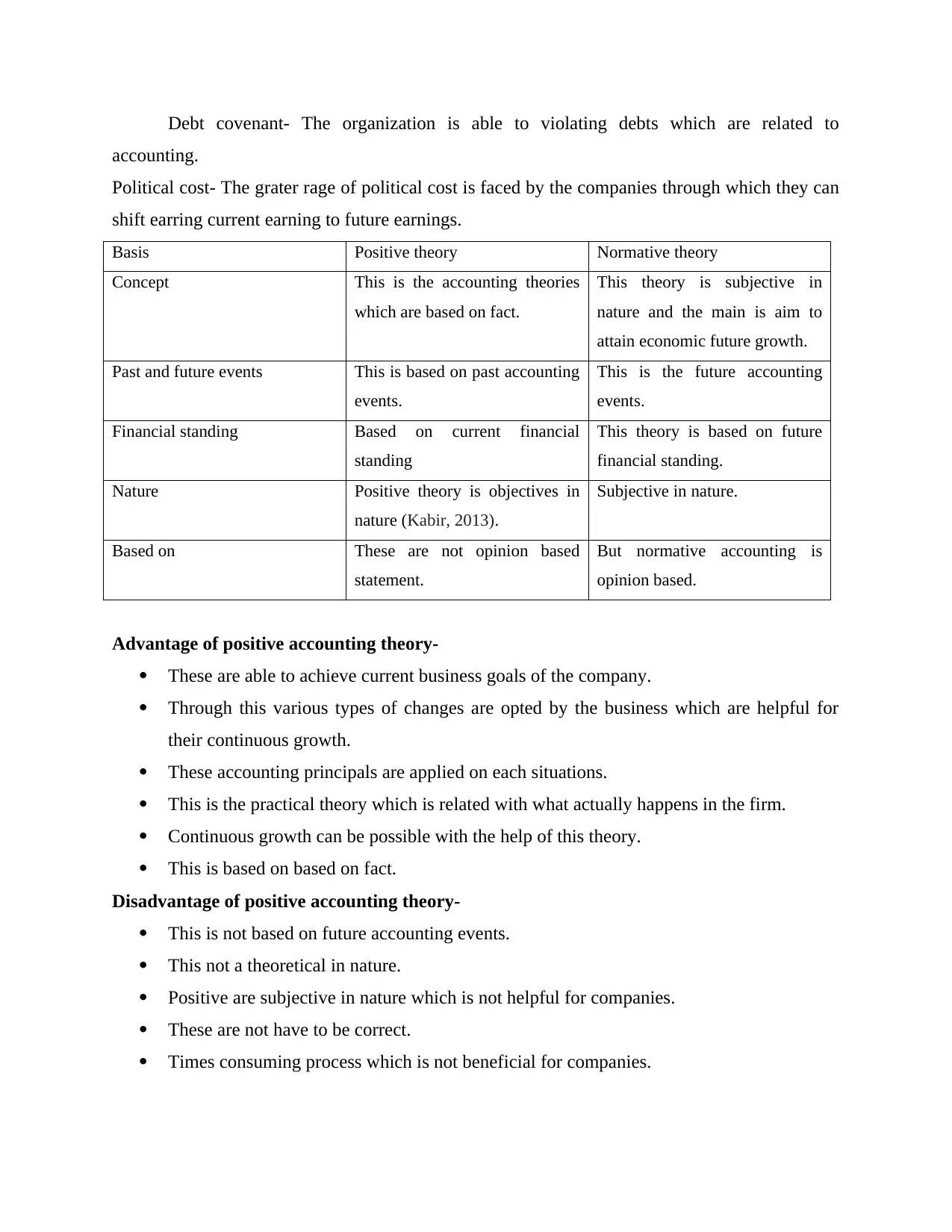

This report provides a comprehensive comparison of positive and normative accounting theories. It begins by defining positive accounting, which focuses on fact-based, objective analysis of economic data to improve company performance, and normative accounting, which is subjective and deals with morality in accounting, often addressing future events. The report then outlines the advantages and disadvantages of each theory, including the ability of positive accounting to achieve current business goals and the future-oriented focus of normative accounting. Key differences are highlighted, such as positive theory's basis in past events and current financial standing versus normative theory's focus on future events and financial standing. The report also explores the practical implications of each theory, emphasizing how managers can use them to improve financial planning, set objectives, and make informed decisions. Finally, the report concludes by underscoring the importance of understanding the distinctions between these theories for maximizing results in financial management.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.