The Changing Global Landscape Post-Brexit: Trade and Finance

VerifiedAdded on 2020/05/28

|18

|4283

|60

Report

AI Summary

This report examines the multifaceted impacts of Brexit on the UK's trade and financial sectors, with a specific focus on its implications for the Commonwealth. The analysis begins with an executive summary outlining the key findings, followed by an introduction that defines Brexit and its context. The report investigates trade trends between Commonwealth countries, detailing the UK's role in this trade, and assessing the effects of Brexit on intra-Commonwealth trade. A significant portion of the report is dedicated to evaluating the impact of Brexit on the UK's finance sector, including potential challenges and opportunities for multinational enterprises. The report concludes with recommendations and a comprehensive conclusion, supported by relevant references. The report highlights the depreciation of the pound, market access concerns, and the need for the UK to provide similar trade benefits to the Commonwealth countries after Brexit. It also explores scenarios under WTO rules and MiFID 2, providing insights into the future of the UK's financial sector.

Running head: POST BREXIT AND CHANGING GLOBAL LANDSCAPE

Post Brexit and Changing Global Landscape

Name of the Student

Name of the University

Post Brexit and Changing Global Landscape

Name of the Student

Name of the University

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1POST BREXIT AND CHANGING GLOBAL LANDSCAPE

Executive Summary

Brexit stands for the Britain’s decision of exiting the European Union taken in June 23, 2016

through referendum. This decision was taken through public vote due to the limitations faced by

the UK population in their free movement. The focus of the report was on the trend of the

commonwealth trade and the impact of Brexit on the financial sector. The report identified that

the impact of the event is likely to impact on the commonwealth trade, where the multinational

financial organisations are will receive significant blow due to the economic slowdown. The

Britain is now to think of the post Brexit trading policies and taxations that will attract the

international finance organisation for helping UK to grow.

Executive Summary

Brexit stands for the Britain’s decision of exiting the European Union taken in June 23, 2016

through referendum. This decision was taken through public vote due to the limitations faced by

the UK population in their free movement. The focus of the report was on the trend of the

commonwealth trade and the impact of Brexit on the financial sector. The report identified that

the impact of the event is likely to impact on the commonwealth trade, where the multinational

financial organisations are will receive significant blow due to the economic slowdown. The

Britain is now to think of the post Brexit trading policies and taxations that will attract the

international finance organisation for helping UK to grow.

2POST BREXIT AND CHANGING GLOBAL LANDSCAPE

Contents

Introduction......................................................................................................................................3

Trends in Trade of Goods and Services between Commonwealth Countries.................................4

Commonwealth Trade with UK...................................................................................................5

Effect of Brexit on intra-commonwealth trade with UK.............................................................8

Impact of Brexit on trade and investment in Finance Sectors of UK..............................................9

Post Brexit Challenges and opportunities in MNE in Finance Sector...........................................11

Recommendation and Conclusion.................................................................................................13

Reference.......................................................................................................................................15

Contents

Introduction......................................................................................................................................3

Trends in Trade of Goods and Services between Commonwealth Countries.................................4

Commonwealth Trade with UK...................................................................................................5

Effect of Brexit on intra-commonwealth trade with UK.............................................................8

Impact of Brexit on trade and investment in Finance Sectors of UK..............................................9

Post Brexit Challenges and opportunities in MNE in Finance Sector...........................................11

Recommendation and Conclusion.................................................................................................13

Reference.......................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3POST BREXIT AND CHANGING GLOBAL LANDSCAPE

Introduction

Brexit stands for the Britain’s decision of exiting the European Union taken in June 23,

2016 through referendum. This decision was taken through public vote due to the limitations

faced by the UK population in their free movement. Value of the free movement of the

immigration resulted in limiting the accessibility in the countries under the union. This had over

powered the monetary benefits received by UK. The parties are under two years of negotiation

for determining the relation of UK with the EU for the post Brexit period, which is scheduled on

29th of March, 2019 (Hunt and Wheeler 2018). The decision was indeed shocking for the

political elite of UK, leaders of EU and the EU bureaucracy itself. Moreover, this event is likely

to draw some consequences for both UK and EU. The first consequence that can be identified is

the political unrest between both the parties. This can lead to an acrimonious tug of war between

them from the political stance. The financial market on the other hand will be effected and make

it vulnerable for over 19 nations under EU. This can be directly related with the trade. The exit

will redefine trade policies between UK and other EU members as the EU members enjoy free

tariffs on import and export of goods (independent.co.uk. 2018). Moreover, a large number of

populations of both the parties are living across the member states. Brexit is likely to cause

immigration of the population to their origin, which has further implication on the financial

sectors of the parties. This will also cause a recession in the market, as the people are likely to

lose their jobs. Over three million EU populations is employed in Britain alone, who are likely to

lose their job if the trade and investments are ceased between EU and UK after Brexit. This

report will further identify the trade of goods and services between the commonwealth countries

and the possible impact of Brexit on the trade and investment in finance sector of UK. The

Introduction

Brexit stands for the Britain’s decision of exiting the European Union taken in June 23,

2016 through referendum. This decision was taken through public vote due to the limitations

faced by the UK population in their free movement. Value of the free movement of the

immigration resulted in limiting the accessibility in the countries under the union. This had over

powered the monetary benefits received by UK. The parties are under two years of negotiation

for determining the relation of UK with the EU for the post Brexit period, which is scheduled on

29th of March, 2019 (Hunt and Wheeler 2018). The decision was indeed shocking for the

political elite of UK, leaders of EU and the EU bureaucracy itself. Moreover, this event is likely

to draw some consequences for both UK and EU. The first consequence that can be identified is

the political unrest between both the parties. This can lead to an acrimonious tug of war between

them from the political stance. The financial market on the other hand will be effected and make

it vulnerable for over 19 nations under EU. This can be directly related with the trade. The exit

will redefine trade policies between UK and other EU members as the EU members enjoy free

tariffs on import and export of goods (independent.co.uk. 2018). Moreover, a large number of

populations of both the parties are living across the member states. Brexit is likely to cause

immigration of the population to their origin, which has further implication on the financial

sectors of the parties. This will also cause a recession in the market, as the people are likely to

lose their jobs. Over three million EU populations is employed in Britain alone, who are likely to

lose their job if the trade and investments are ceased between EU and UK after Brexit. This

report will further identify the trade of goods and services between the commonwealth countries

and the possible impact of Brexit on the trade and investment in finance sector of UK. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4POST BREXIT AND CHANGING GLOBAL LANDSCAPE

challenges and opportunities for the multinational trade finance organisations will also be

evaluated in the report.

Trends in Trade of Goods and Services between Commonwealth Countries

Fifty-two countries around the globe that are geographically dispersed represent the

Commonwealth. Trade between the commonwealth countries are expected to be beneficial and

convenient compared to the trade outside the commonwealth. The FDI inflow between the

commonwealth countries are greater compared to the others. This supports the fact of stronger

effect of commonwealth trading, which is considered to have greater benefits for the countries.

The commonwealth countries have recovered from the global recession and are in a

growth phase. The intra-commonwealth trade reflects a figure of $592 billion as per 2013

commonwealth report, which they have achieved through an annual growth of 10% every year

since 1995 (Thecommonwealth.org 2018). The commonwealth reports expect to overshoot $1

trillion by 2020 (Thecommonwealth.org 2018). Moreover, the developing countries of Asia

represent the larger share in the product export with a percentage of 55 in the intra-

commonwealth activities. The major countries that contribute in the exports are India, Singapore

and Malaysia, which cumulatively exports more than half of the export done by Asia. Other

major exporters in the remaining intra-commonwealth goods trade are UK, Australia, Nigeria

and South Africa. The report further identifies one-third of the total trade coming from the

developing members of commonwealth.

The intra-commonwealth good trade reflects a significant growth of 5% in their exports

since 2000. This growth trend of intra-commonwealth export is largely represented by the small

states and the largest share in the respective matter is held by Swaziland, Grenada, Dominica,

challenges and opportunities for the multinational trade finance organisations will also be

evaluated in the report.

Trends in Trade of Goods and Services between Commonwealth Countries

Fifty-two countries around the globe that are geographically dispersed represent the

Commonwealth. Trade between the commonwealth countries are expected to be beneficial and

convenient compared to the trade outside the commonwealth. The FDI inflow between the

commonwealth countries are greater compared to the others. This supports the fact of stronger

effect of commonwealth trading, which is considered to have greater benefits for the countries.

The commonwealth countries have recovered from the global recession and are in a

growth phase. The intra-commonwealth trade reflects a figure of $592 billion as per 2013

commonwealth report, which they have achieved through an annual growth of 10% every year

since 1995 (Thecommonwealth.org 2018). The commonwealth reports expect to overshoot $1

trillion by 2020 (Thecommonwealth.org 2018). Moreover, the developing countries of Asia

represent the larger share in the product export with a percentage of 55 in the intra-

commonwealth activities. The major countries that contribute in the exports are India, Singapore

and Malaysia, which cumulatively exports more than half of the export done by Asia. Other

major exporters in the remaining intra-commonwealth goods trade are UK, Australia, Nigeria

and South Africa. The report further identifies one-third of the total trade coming from the

developing members of commonwealth.

The intra-commonwealth good trade reflects a significant growth of 5% in their exports

since 2000. This growth trend of intra-commonwealth export is largely represented by the small

states and the largest share in the respective matter is held by Swaziland, Grenada, Dominica,

5POST BREXIT AND CHANGING GLOBAL LANDSCAPE

Botswana and Barbados. The total of intra-commonwealth service export on the other hand

according to the estimation reached $139 billion, out of which, UK, Singapore, India, Australia

and Canada cumulatively represents 80% of the total (Thecommonwealth.org 2018).

The flow of foreign direct investment between the commonwealth countries is greater

compared to the general FDI inflow. This represents one third of the total FDI inflow in the

commonwealth countries. The inflow had achieved the figure of $80 billion right before the

global financial crisis stroke in 2007. The recent commonwealth report reflects an accumulative

stock of $716 billion of the seven largest commonwealth members (Thecommonwealth.org

2018). This reflects a greater transaction between the commonwealth countries.

Commonwealth Trade with UK

UK has always been one of the largest players among the commonwealth members. The

import and export in 2015 surplus US$91 billion. The figure is a result of cumulative trade flow

of the goods and services with the other commonwealth members (thecommonwealth.org 2018).

This is due to the trade slowdown took place after 2012 when the figure reached its peak of

US$120 billion.

Botswana and Barbados. The total of intra-commonwealth service export on the other hand

according to the estimation reached $139 billion, out of which, UK, Singapore, India, Australia

and Canada cumulatively represents 80% of the total (Thecommonwealth.org 2018).

The flow of foreign direct investment between the commonwealth countries is greater

compared to the general FDI inflow. This represents one third of the total FDI inflow in the

commonwealth countries. The inflow had achieved the figure of $80 billion right before the

global financial crisis stroke in 2007. The recent commonwealth report reflects an accumulative

stock of $716 billion of the seven largest commonwealth members (Thecommonwealth.org

2018). This reflects a greater transaction between the commonwealth countries.

Commonwealth Trade with UK

UK has always been one of the largest players among the commonwealth members. The

import and export in 2015 surplus US$91 billion. The figure is a result of cumulative trade flow

of the goods and services with the other commonwealth members (thecommonwealth.org 2018).

This is due to the trade slowdown took place after 2012 when the figure reached its peak of

US$120 billion.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6POST BREXIT AND CHANGING GLOBAL LANDSCAPE

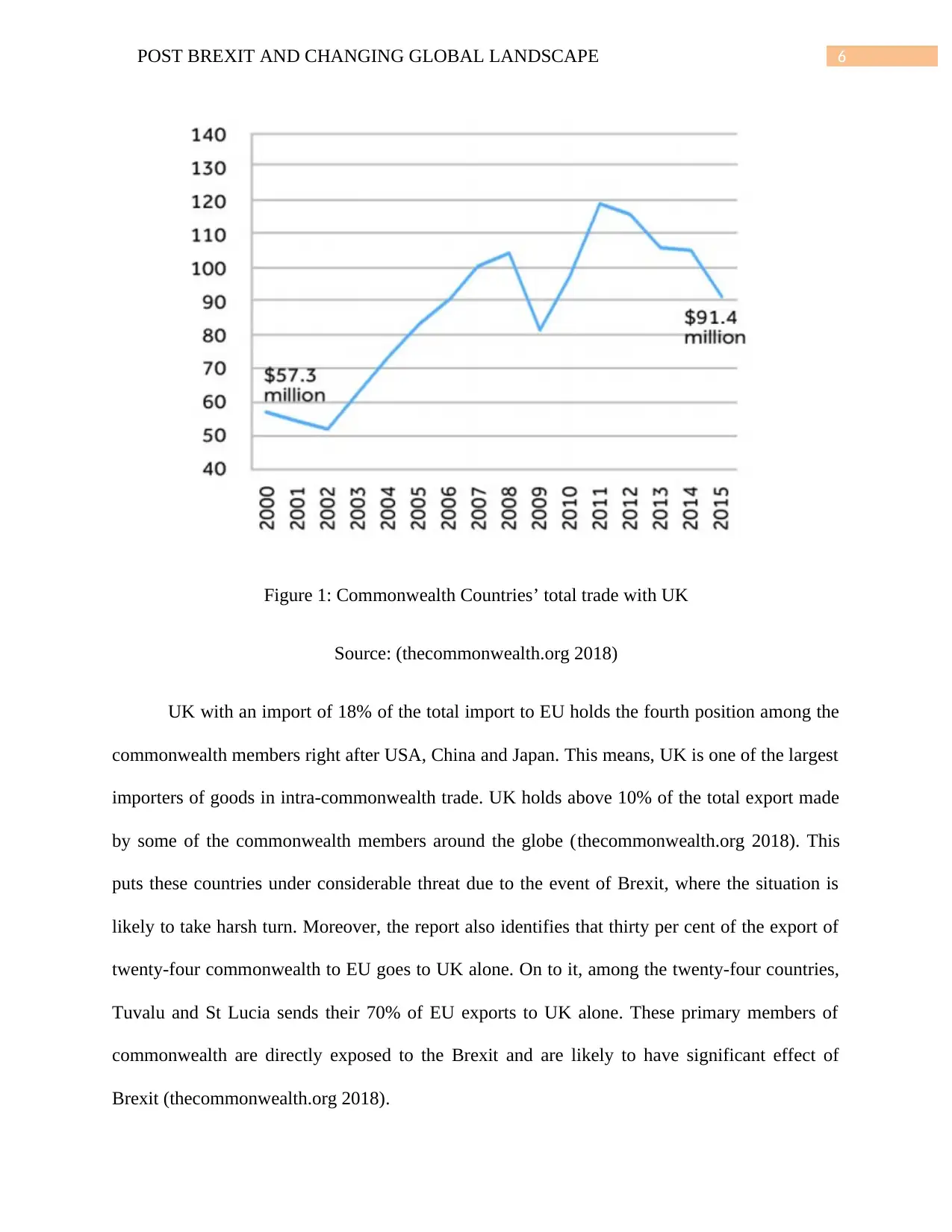

Figure 1: Commonwealth Countries’ total trade with UK

Source: (thecommonwealth.org 2018)

UK with an import of 18% of the total import to EU holds the fourth position among the

commonwealth members right after USA, China and Japan. This means, UK is one of the largest

importers of goods in intra-commonwealth trade. UK holds above 10% of the total export made

by some of the commonwealth members around the globe (thecommonwealth.org 2018). This

puts these countries under considerable threat due to the event of Brexit, where the situation is

likely to take harsh turn. Moreover, the report also identifies that thirty per cent of the export of

twenty-four commonwealth to EU goes to UK alone. On to it, among the twenty-four countries,

Tuvalu and St Lucia sends their 70% of EU exports to UK alone. These primary members of

commonwealth are directly exposed to the Brexit and are likely to have significant effect of

Brexit (thecommonwealth.org 2018).

Figure 1: Commonwealth Countries’ total trade with UK

Source: (thecommonwealth.org 2018)

UK with an import of 18% of the total import to EU holds the fourth position among the

commonwealth members right after USA, China and Japan. This means, UK is one of the largest

importers of goods in intra-commonwealth trade. UK holds above 10% of the total export made

by some of the commonwealth members around the globe (thecommonwealth.org 2018). This

puts these countries under considerable threat due to the event of Brexit, where the situation is

likely to take harsh turn. Moreover, the report also identifies that thirty per cent of the export of

twenty-four commonwealth to EU goes to UK alone. On to it, among the twenty-four countries,

Tuvalu and St Lucia sends their 70% of EU exports to UK alone. These primary members of

commonwealth are directly exposed to the Brexit and are likely to have significant effect of

Brexit (thecommonwealth.org 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7POST BREXIT AND CHANGING GLOBAL LANDSCAPE

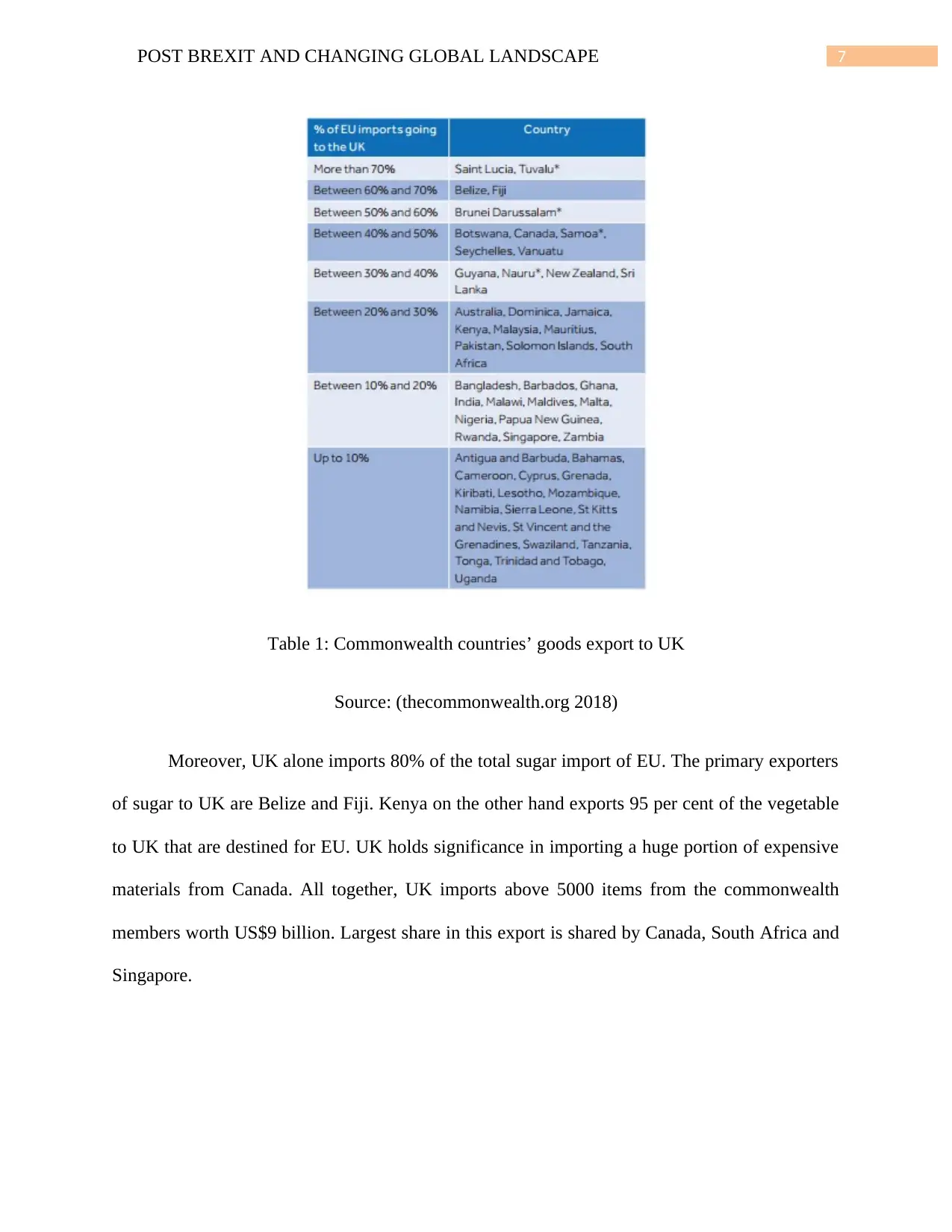

Table 1: Commonwealth countries’ goods export to UK

Source: (thecommonwealth.org 2018)

Moreover, UK alone imports 80% of the total sugar import of EU. The primary exporters

of sugar to UK are Belize and Fiji. Kenya on the other hand exports 95 per cent of the vegetable

to UK that are destined for EU. UK holds significance in importing a huge portion of expensive

materials from Canada. All together, UK imports above 5000 items from the commonwealth

members worth US$9 billion. Largest share in this export is shared by Canada, South Africa and

Singapore.

Table 1: Commonwealth countries’ goods export to UK

Source: (thecommonwealth.org 2018)

Moreover, UK alone imports 80% of the total sugar import of EU. The primary exporters

of sugar to UK are Belize and Fiji. Kenya on the other hand exports 95 per cent of the vegetable

to UK that are destined for EU. UK holds significance in importing a huge portion of expensive

materials from Canada. All together, UK imports above 5000 items from the commonwealth

members worth US$9 billion. Largest share in this export is shared by Canada, South Africa and

Singapore.

8POST BREXIT AND CHANGING GLOBAL LANDSCAPE

The existing trade links between UK and rest of the commonwealth countries are strong,

which is again being strengthened by mobilising pro-active policy support. It will help them in

expanding further trade.

Effect of Brexit on intra-commonwealth trade with UK

Brexit will have significant impact on the developing and developed countries due to the

alteration that will be made between UK and EU with the other commonwealth members

depending on the trade relation. The Brexit have significantly altered the value of pound and

caused a depreciation of 10 to 20 per cent. This means that the trade with UK after Brexit will

generate less revenue for the exporting commonwealth members. Market access on the other

hand is another concern for the commonwealth countries as they receive duty-free and quota-free

access in the EU market. UK’s Separation from EU is likely to alter the situation that might

affect the export of the developing commonwealth countries. The commonwealth report reflects

a total of US$800 million duties if the UK takes away the EU benefits from the least developed

countries (thecommonwealth.org 2018). Hence, it will be of absolute necessity for UK to provide

similar facilities to the least developing commonwealth countries after their divorce from

European Union. This will facilitate the countries to hold their continuous economic growth and

international expansion. The service trade on the other hand is under direct threat as the value of

pound is likely to remain similar for considerably long period if not face further depreciation.

This will result the result into less revenue from UK for the export of their services. Moreover,

Brexit is likely to dampen the demand for import from the developing countries due to the lower

economic growth as anticipated. This will cease the import from the under developed countries,

hence effecting the economy of those commonwealth members.

The existing trade links between UK and rest of the commonwealth countries are strong,

which is again being strengthened by mobilising pro-active policy support. It will help them in

expanding further trade.

Effect of Brexit on intra-commonwealth trade with UK

Brexit will have significant impact on the developing and developed countries due to the

alteration that will be made between UK and EU with the other commonwealth members

depending on the trade relation. The Brexit have significantly altered the value of pound and

caused a depreciation of 10 to 20 per cent. This means that the trade with UK after Brexit will

generate less revenue for the exporting commonwealth members. Market access on the other

hand is another concern for the commonwealth countries as they receive duty-free and quota-free

access in the EU market. UK’s Separation from EU is likely to alter the situation that might

affect the export of the developing commonwealth countries. The commonwealth report reflects

a total of US$800 million duties if the UK takes away the EU benefits from the least developed

countries (thecommonwealth.org 2018). Hence, it will be of absolute necessity for UK to provide

similar facilities to the least developing commonwealth countries after their divorce from

European Union. This will facilitate the countries to hold their continuous economic growth and

international expansion. The service trade on the other hand is under direct threat as the value of

pound is likely to remain similar for considerably long period if not face further depreciation.

This will result the result into less revenue from UK for the export of their services. Moreover,

Brexit is likely to dampen the demand for import from the developing countries due to the lower

economic growth as anticipated. This will cease the import from the under developed countries,

hence effecting the economy of those commonwealth members.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9POST BREXIT AND CHANGING GLOBAL LANDSCAPE

Impact of Brexit on trade and investment in Finance Sectors of UK

Brexit or Britain’s exit from the European Union is likely to have its impact on many of

the business sectors. However, the impact assumed for the finance sector of UK is significantly

high, which has already started reflecting its effects. The value of pound has received

considerable fall of 10 to 20 per cent, which is the worst scenario in recent decades (Chapman

2018). The impacts on finance organisations based in UK market are likely to have greater effect

compared to the ones in EU. Three determinants will contribute in directing the impact. These

determinants are the resilience of UK financial sector to Brexit, using its greater international

relation and position; shift of the UK finance organisations’ operation around EU before the exit

on 2019; and withdrawal agreement adequacy between EU and UK.

The single market of EU allows the financial organisations of the member countries

operate around the EU using their home country licence. The union rejects the need of separate

licensing for operating within each of the target market under EU (Emmerson, Johnson and

Mitchell 2016). The area is referred as European Economic Area and the process as referred by

the Union is passport. UK leaving the union will require the financial organisations of UK to

produce separate licence for continuing their operation around the member states of EU. Some of

the possible scenario that might take place after the end of the negotiation period is highlighted

below.

WTO Rules – Access of UK finance sector in the EU market will be regulated by the WTO

norms under most favoured nation terms. This means that UK will have no preferential treatment

in the EU single market. Moreover, the General Agreement on Trade in Services will regulate

the financial operation of UK in the EU province (Daugbjerg and Swinbank 2015). UK under

this regulation has to open subsidiaries in the target market of EU member states for avoiding the

Impact of Brexit on trade and investment in Finance Sectors of UK

Brexit or Britain’s exit from the European Union is likely to have its impact on many of

the business sectors. However, the impact assumed for the finance sector of UK is significantly

high, which has already started reflecting its effects. The value of pound has received

considerable fall of 10 to 20 per cent, which is the worst scenario in recent decades (Chapman

2018). The impacts on finance organisations based in UK market are likely to have greater effect

compared to the ones in EU. Three determinants will contribute in directing the impact. These

determinants are the resilience of UK financial sector to Brexit, using its greater international

relation and position; shift of the UK finance organisations’ operation around EU before the exit

on 2019; and withdrawal agreement adequacy between EU and UK.

The single market of EU allows the financial organisations of the member countries

operate around the EU using their home country licence. The union rejects the need of separate

licensing for operating within each of the target market under EU (Emmerson, Johnson and

Mitchell 2016). The area is referred as European Economic Area and the process as referred by

the Union is passport. UK leaving the union will require the financial organisations of UK to

produce separate licence for continuing their operation around the member states of EU. Some of

the possible scenario that might take place after the end of the negotiation period is highlighted

below.

WTO Rules – Access of UK finance sector in the EU market will be regulated by the WTO

norms under most favoured nation terms. This means that UK will have no preferential treatment

in the EU single market. Moreover, the General Agreement on Trade in Services will regulate

the financial operation of UK in the EU province (Daugbjerg and Swinbank 2015). UK under

this regulation has to open subsidiaries in the target market of EU member states for avoiding the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10POST BREXIT AND CHANGING GLOBAL LANDSCAPE

discrimination and to concede passport rights. However, the countries can discriminate UK’s

financial services using justified prudential regularity purposes that will surely threaten the profit

of UK made from the EU market.

MiFID 2 – This asks the third country regulatory authorities to cooperate with ESMA under

cooperation agreement. The third country in that case has to agree on the terms of supervising

subsidiary in EU and have to open subsidiaries in all the EU countries in order to gain operation

permission. In addition, the subsidiaries opened have to be larger in size, which requires greater

capital investment and separate capitalisation (Batlle, Mastropietro and Gómez-Elvira 2014).

Moreover, UK then has to have equivalent regime. This means that UK will then have to set

regulatory framework similar to that of EU. This can be considered as a burdensome process for

UK and considerably limit the profit margin. Moreover, this will likely to increase the barriers to

trade in EU market.

Free Trade Agreement – This will provide opportunity to UK for gaining duty free access into

EU. However, the products must have benefit (Wouters et al 2014). However, this is limited to

the products and does not comply with the services.

European Economic Area – UK can establish relation with EU under the EEA regulation. This

will enable the financial sector of UK to free trade with the members of EU. Furthermore, UK

will be able to enjoy the more or less similar trading facility as pre Brexit terms (De Vries et al

2014). However, UK then will have to significantly contribute in EU’s financial budget and obey

a large number of EU regulations that are considerably costly.

Customised Relationship – It is possible for UK to customise their relationship with EU

regarding to the trade of finance sector that will be newly modified for continuing trade

discrimination and to concede passport rights. However, the countries can discriminate UK’s

financial services using justified prudential regularity purposes that will surely threaten the profit

of UK made from the EU market.

MiFID 2 – This asks the third country regulatory authorities to cooperate with ESMA under

cooperation agreement. The third country in that case has to agree on the terms of supervising

subsidiary in EU and have to open subsidiaries in all the EU countries in order to gain operation

permission. In addition, the subsidiaries opened have to be larger in size, which requires greater

capital investment and separate capitalisation (Batlle, Mastropietro and Gómez-Elvira 2014).

Moreover, UK then has to have equivalent regime. This means that UK will then have to set

regulatory framework similar to that of EU. This can be considered as a burdensome process for

UK and considerably limit the profit margin. Moreover, this will likely to increase the barriers to

trade in EU market.

Free Trade Agreement – This will provide opportunity to UK for gaining duty free access into

EU. However, the products must have benefit (Wouters et al 2014). However, this is limited to

the products and does not comply with the services.

European Economic Area – UK can establish relation with EU under the EEA regulation. This

will enable the financial sector of UK to free trade with the members of EU. Furthermore, UK

will be able to enjoy the more or less similar trading facility as pre Brexit terms (De Vries et al

2014). However, UK then will have to significantly contribute in EU’s financial budget and obey

a large number of EU regulations that are considerably costly.

Customised Relationship – It is possible for UK to customise their relationship with EU

regarding to the trade of finance sector that will be newly modified for continuing trade

11POST BREXIT AND CHANGING GLOBAL LANDSCAPE

relationship between the parties. However, the possibilities in this scenario is hard to assume as

this will purely base on the negotiation made between the parties (Pisani-Ferry et al 2016).

However, this is inevitable that the financial sector of UK will face barriers in multiple

dimensions that will considerably limit the profit margin and free operations.

Hence, it can be stated that the UK’s financial sector’s operation in the EU single market

is likely to be hampered due to the event of Brexit. The companies will face significant challenge

in making profit in the EU market while requiring greater investment on the same.

Post Brexit Challenges and opportunities in MNE in Finance Sector

The event of Brexit as identified in various grounds in the earlier section of the report is

likely bring turmoil on the international trading as it will change the relation of multination

organisation with both UK and EU in case of trade relation. The import–export policies of UK is

likely to change that will influence the trading of goods and services with other countries (Begg

and Mushövel 2016). This will further effect MNCs considering expanding their business in the

UK. Finance sector is anticipated to receive significant impact. Some of challenges and

opportunities are critically evaluated below.

As stated by Chu 2018 economic slowdown of UK economy is the most common

anticipation in the future international trade market. This will have significant implication for the

financial service providers, as they are likely to lose confidence for further investing in Britain.

However, Dhingra et al (2016) identified this as an opportunity for the finance companies as UK

is likely to lose their negotiation power. This will force UK to offer preferential market for

multinational finance organisations. Moreover, this is likely to create a huge gap in the European

Union, as UK was the primary moneylender to EU companies and government as well.

relationship between the parties. However, the possibilities in this scenario is hard to assume as

this will purely base on the negotiation made between the parties (Pisani-Ferry et al 2016).

However, this is inevitable that the financial sector of UK will face barriers in multiple

dimensions that will considerably limit the profit margin and free operations.

Hence, it can be stated that the UK’s financial sector’s operation in the EU single market

is likely to be hampered due to the event of Brexit. The companies will face significant challenge

in making profit in the EU market while requiring greater investment on the same.

Post Brexit Challenges and opportunities in MNE in Finance Sector

The event of Brexit as identified in various grounds in the earlier section of the report is

likely bring turmoil on the international trading as it will change the relation of multination

organisation with both UK and EU in case of trade relation. The import–export policies of UK is

likely to change that will influence the trading of goods and services with other countries (Begg

and Mushövel 2016). This will further effect MNCs considering expanding their business in the

UK. Finance sector is anticipated to receive significant impact. Some of challenges and

opportunities are critically evaluated below.

As stated by Chu 2018 economic slowdown of UK economy is the most common

anticipation in the future international trade market. This will have significant implication for the

financial service providers, as they are likely to lose confidence for further investing in Britain.

However, Dhingra et al (2016) identified this as an opportunity for the finance companies as UK

is likely to lose their negotiation power. This will force UK to offer preferential market for

multinational finance organisations. Moreover, this is likely to create a huge gap in the European

Union, as UK was the primary moneylender to EU companies and government as well.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.