Capital Budgeting Report: Comparing Powerboat Investment Options

VerifiedAdded on 2020/12/18

|10

|2046

|447

Report

AI Summary

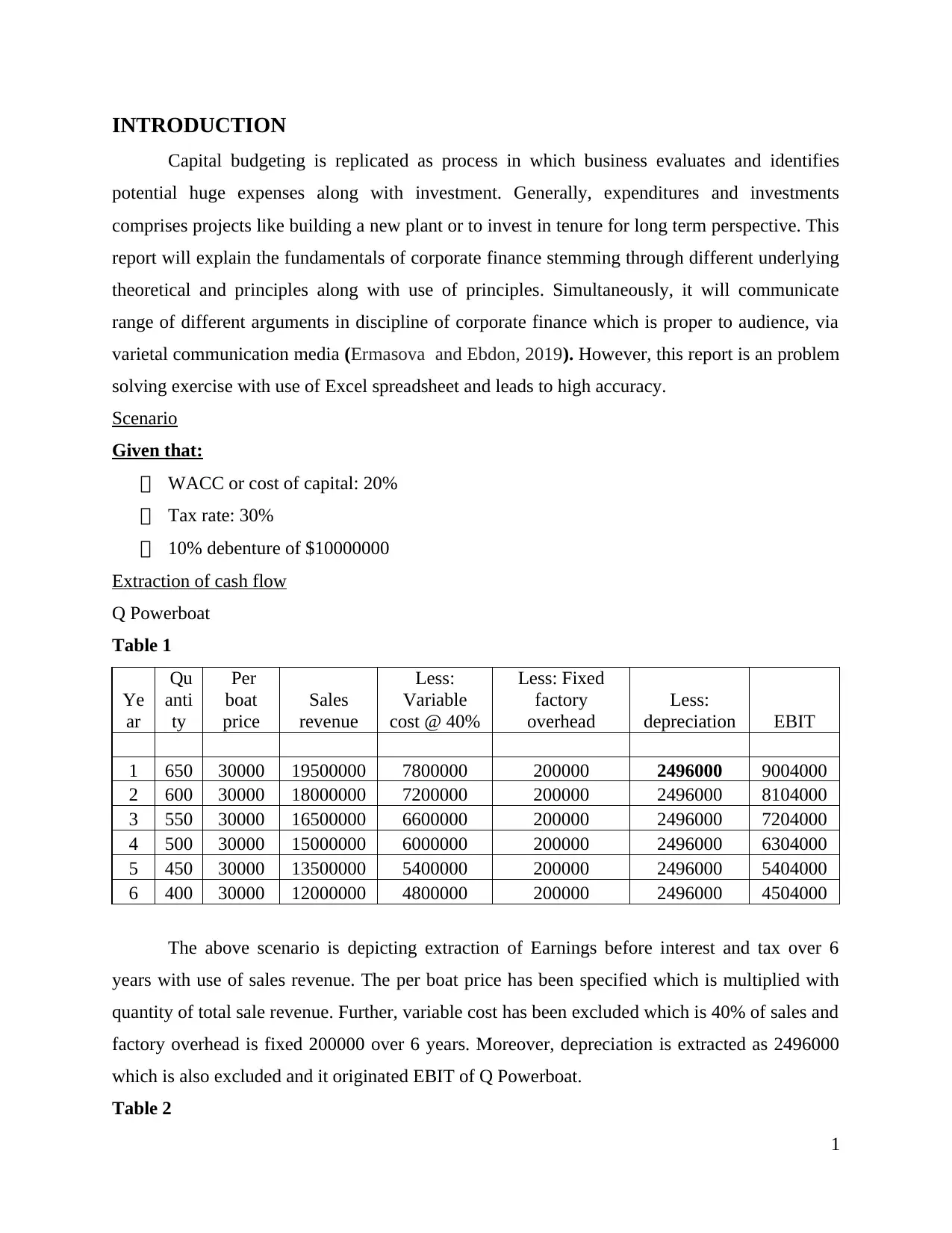

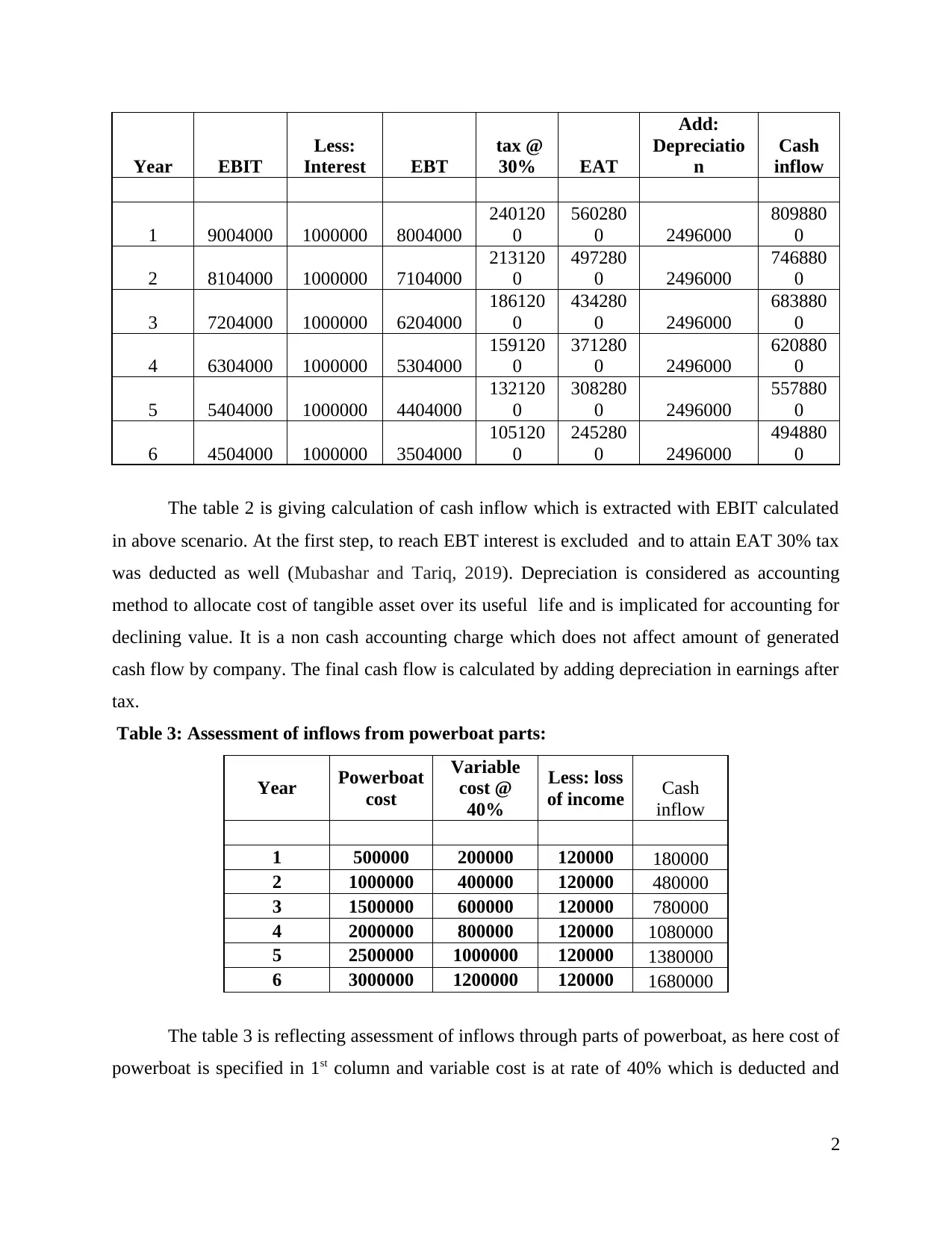

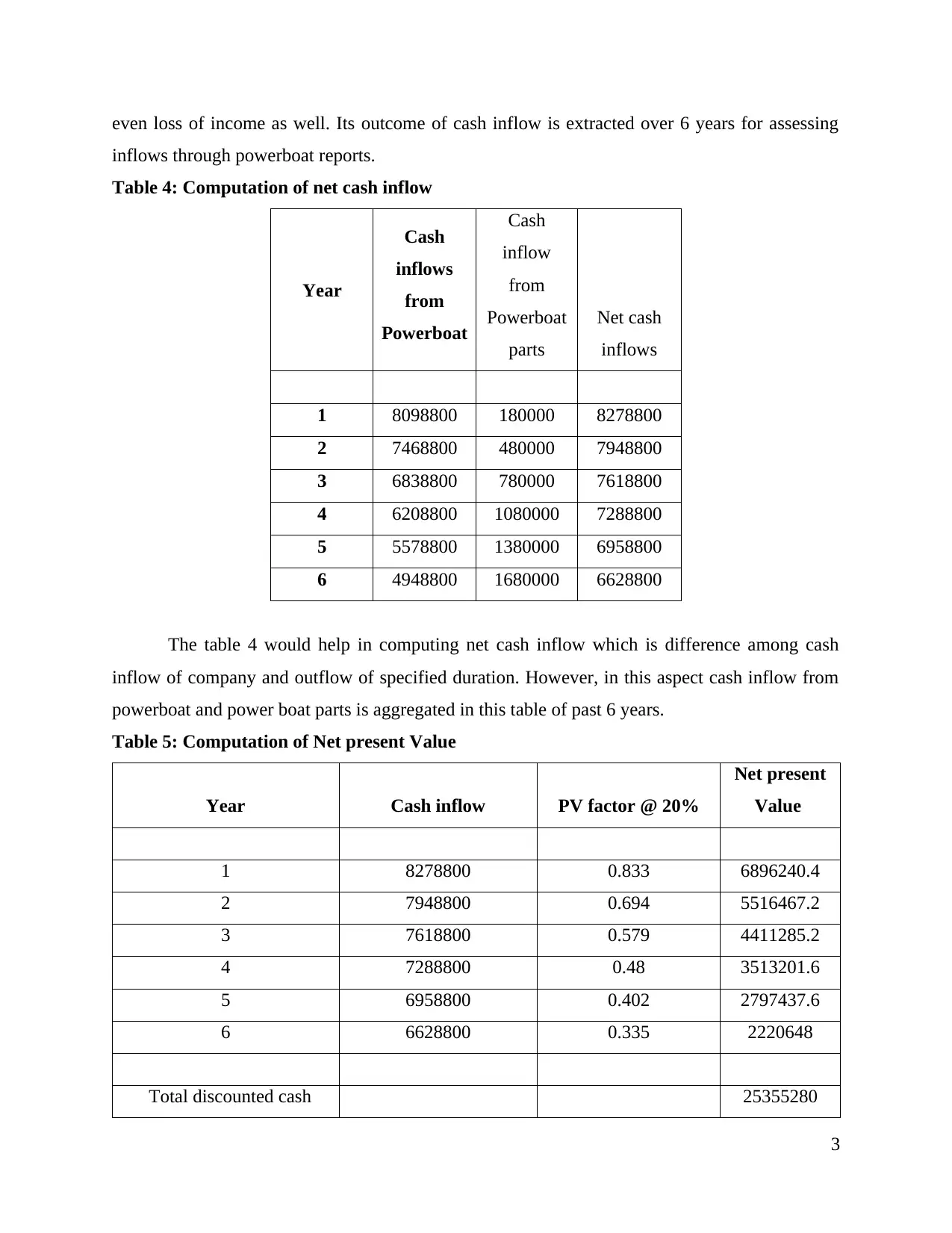

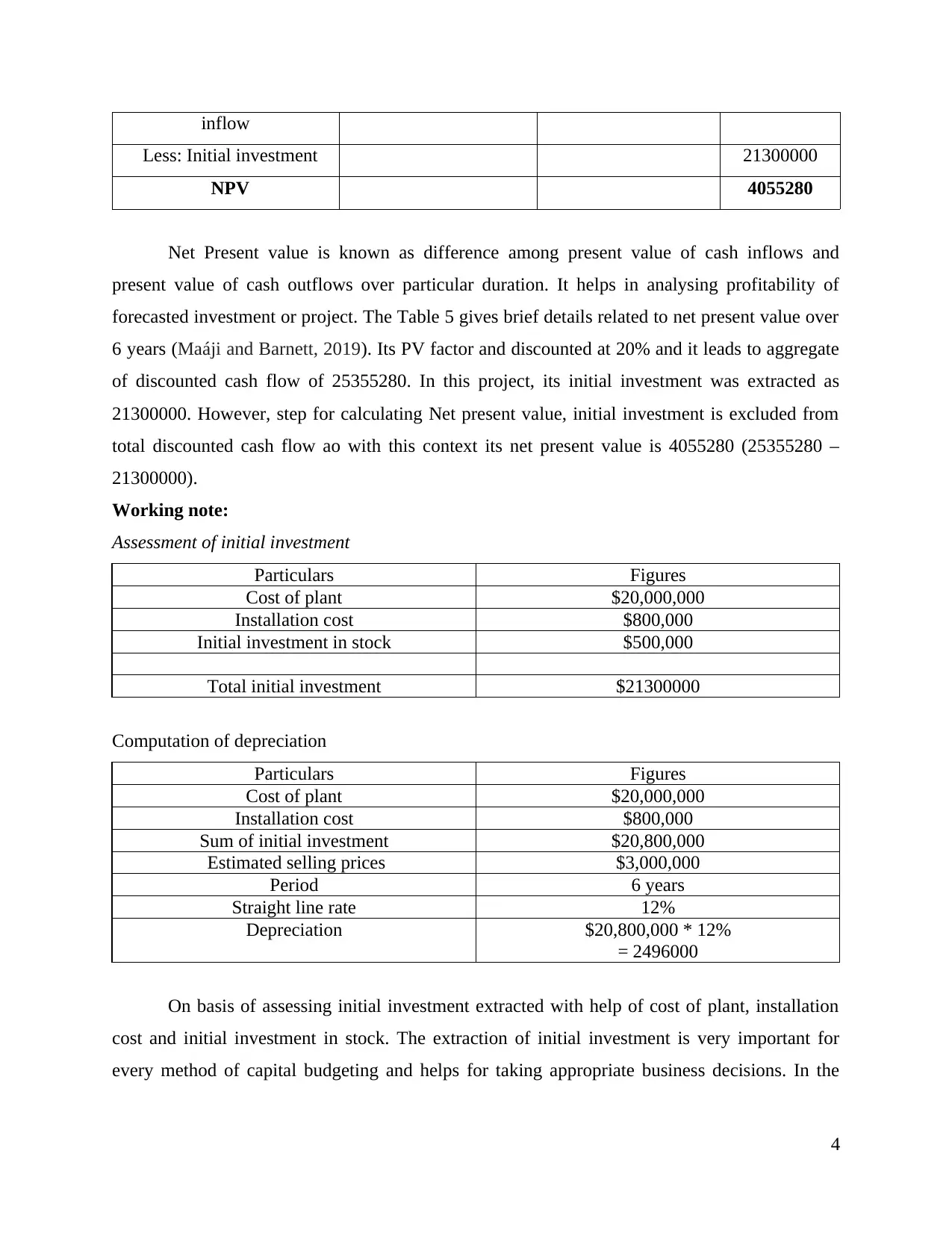

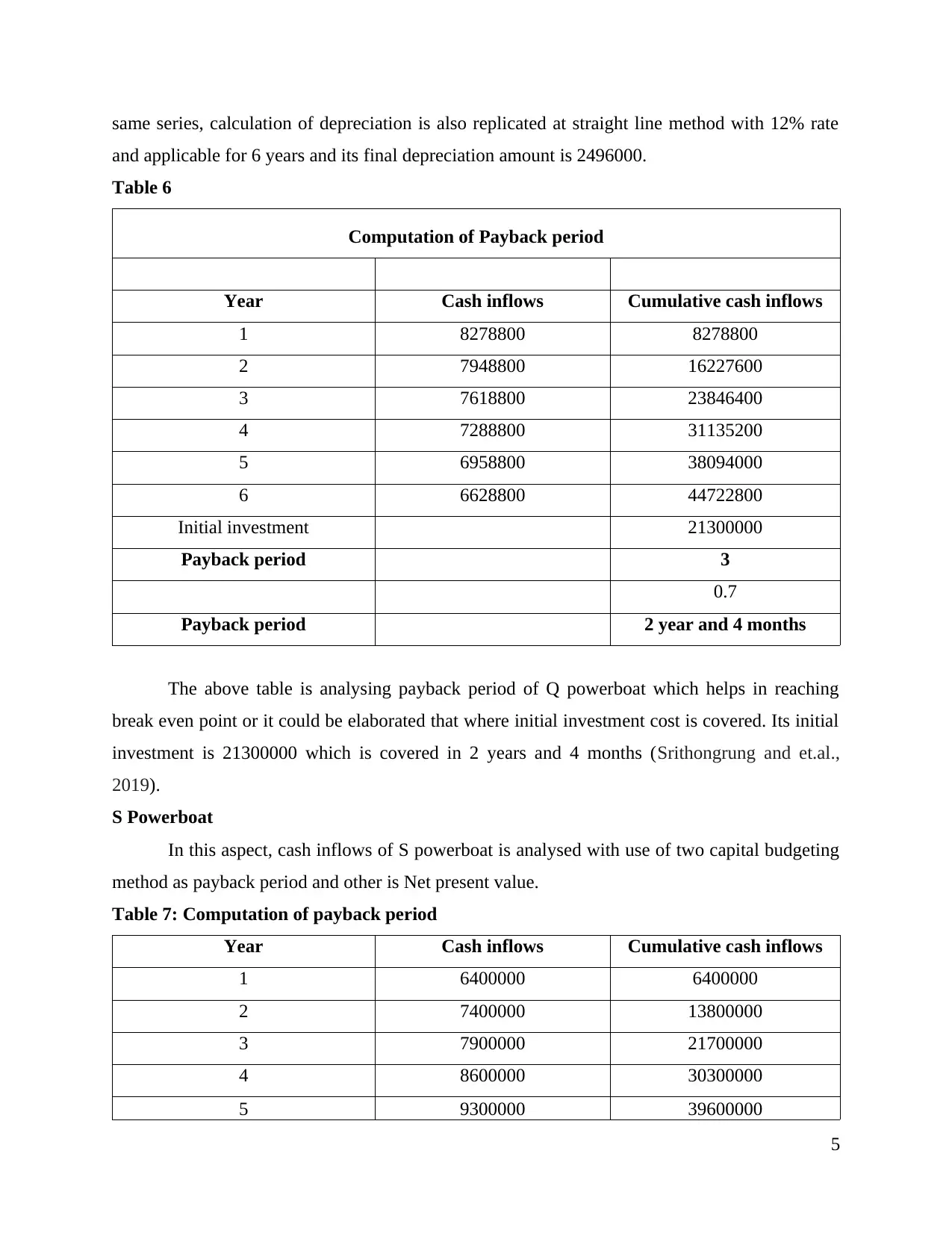

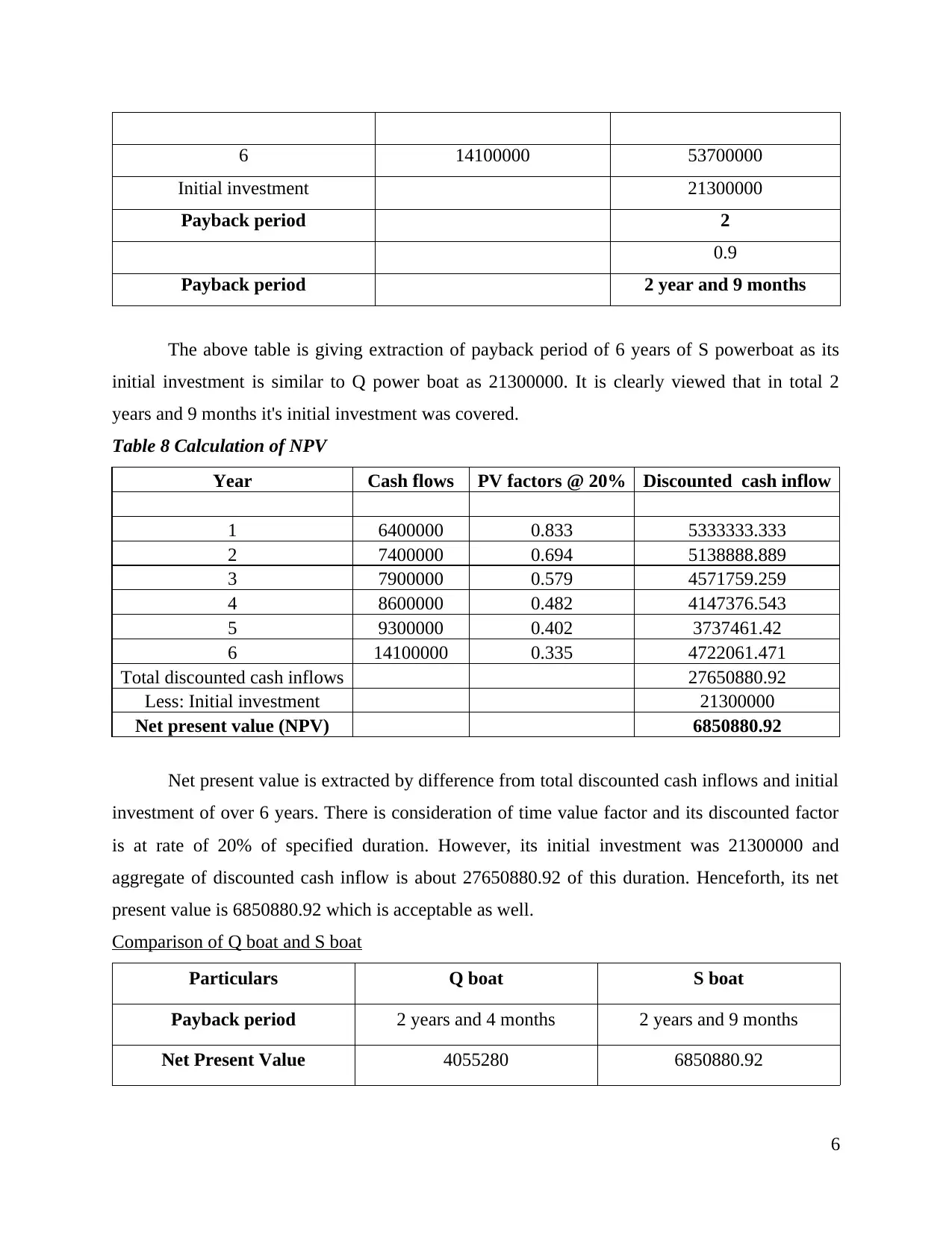

This report provides a detailed analysis of capital budgeting, focusing on two powerboat investment options, Q boat and S boat. It begins with an introduction to capital budgeting and its importance in evaluating potential investments, including building new plants and long-term projects. The report uses Excel spreadsheets to extract and analyze cash flows over a six-year period, considering factors like sales revenue, variable costs, fixed overheads, and depreciation to calculate EBIT and EAT. The report calculates cash inflows, net cash inflows, and net present value (NPV) for each boat, along with payback periods. The analysis includes working notes on initial investment and depreciation calculations. A comparison of the Q boat and S boat is provided, highlighting the payback period and NPV for each, and ultimately recommending the S powerboat for investment due to its higher NPV. The report concludes by emphasizing the importance of capital budgeting in strategic planning and decision-making, and it references relevant academic sources.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.