Financial Management Report: Analysis of Pentag's Powerboat Projects

VerifiedAdded on 2022/12/30

|10

|2052

|24

Report

AI Summary

This financial management report assesses the viability of two powerboat projects, Q-Powerboat and S-Powerboat, for the Pentag Company. The analysis includes a detailed examination of financial metrics such as Net Present Value (NPV), Internal Rate of Return (IRR), and discounted payback period for each project. The report evaluates the quantitative and qualitative aspects of the Q-Powerboat project, comparing its performance with the S-Powerboat project, which is considered more environmentally friendly. The study also calculates the crossover rate, which identifies the point at which the projects' NPVs are equal. The conclusion recommends against pursuing either project because their discounted payback periods exceed the company's required timeframe, despite both projects meeting other financial acceptance criteria. The report incorporates financial tables, calculations, and references to support its findings and recommendations.

Running head: FINANCIAL MANAGEMENT

Financial management

Name of the student

Name of the university

Student ID

Author note

Financial management

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL MANAGEMENT

Table of Contents

Introduction................................................................................................................................2

Findings......................................................................................................................................2

Findings from the Q-Powerboat project.................................................................................2

Quantitative aspect.................................................................................................................3

Qualitative aspect...................................................................................................................5

Finding and comparison with S-Powerboat project...............................................................5

Cross over rate........................................................................................................................6

Conclusion and recommendation...............................................................................................7

Reference....................................................................................................................................8

Appendix....................................................................................................................................9

Table of Contents

Introduction................................................................................................................................2

Findings......................................................................................................................................2

Findings from the Q-Powerboat project.................................................................................2

Quantitative aspect.................................................................................................................3

Qualitative aspect...................................................................................................................5

Finding and comparison with S-Powerboat project...............................................................5

Cross over rate........................................................................................................................6

Conclusion and recommendation...............................................................................................7

Reference....................................................................................................................................8

Appendix....................................................................................................................................9

2FINANCIAL MANAGEMENT

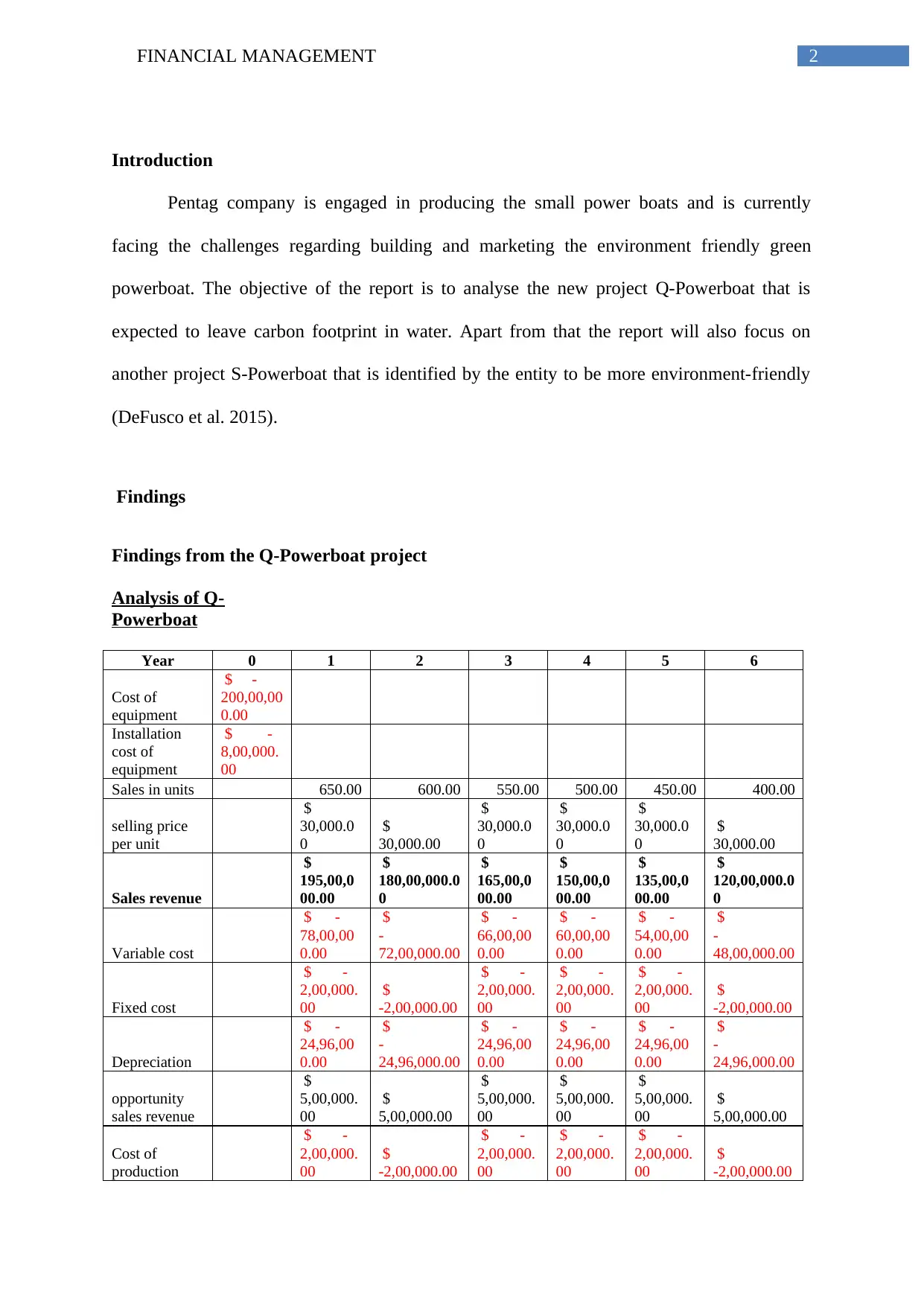

Introduction

Pentag company is engaged in producing the small power boats and is currently

facing the challenges regarding building and marketing the environment friendly green

powerboat. The objective of the report is to analyse the new project Q-Powerboat that is

expected to leave carbon footprint in water. Apart from that the report will also focus on

another project S-Powerboat that is identified by the entity to be more environment-friendly

(DeFusco et al. 2015).

Findings

Findings from the Q-Powerboat project

Analysis of Q-

Powerboat

Year 0 1 2 3 4 5 6

Cost of

equipment

$ -

200,00,00

0.00

Installation

cost of

equipment

$ -

8,00,000.

00

Sales in units 650.00 600.00 550.00 500.00 450.00 400.00

selling price

per unit

$

30,000.0

0

$

30,000.00

$

30,000.0

0

$

30,000.0

0

$

30,000.0

0

$

30,000.00

Sales revenue

$

195,00,0

00.00

$

180,00,000.0

0

$

165,00,0

00.00

$

150,00,0

00.00

$

135,00,0

00.00

$

120,00,000.0

0

Variable cost

$ -

78,00,00

0.00

$

-

72,00,000.00

$ -

66,00,00

0.00

$ -

60,00,00

0.00

$ -

54,00,00

0.00

$

-

48,00,000.00

Fixed cost

$ -

2,00,000.

00

$

-2,00,000.00

$ -

2,00,000.

00

$ -

2,00,000.

00

$ -

2,00,000.

00

$

-2,00,000.00

Depreciation

$ -

24,96,00

0.00

$

-

24,96,000.00

$ -

24,96,00

0.00

$ -

24,96,00

0.00

$ -

24,96,00

0.00

$

-

24,96,000.00

opportunity

sales revenue

$

5,00,000.

00

$

5,00,000.00

$

5,00,000.

00

$

5,00,000.

00

$

5,00,000.

00

$

5,00,000.00

Cost of

production

$ -

2,00,000.

00

$

-2,00,000.00

$ -

2,00,000.

00

$ -

2,00,000.

00

$ -

2,00,000.

00

$

-2,00,000.00

Introduction

Pentag company is engaged in producing the small power boats and is currently

facing the challenges regarding building and marketing the environment friendly green

powerboat. The objective of the report is to analyse the new project Q-Powerboat that is

expected to leave carbon footprint in water. Apart from that the report will also focus on

another project S-Powerboat that is identified by the entity to be more environment-friendly

(DeFusco et al. 2015).

Findings

Findings from the Q-Powerboat project

Analysis of Q-

Powerboat

Year 0 1 2 3 4 5 6

Cost of

equipment

$ -

200,00,00

0.00

Installation

cost of

equipment

$ -

8,00,000.

00

Sales in units 650.00 600.00 550.00 500.00 450.00 400.00

selling price

per unit

$

30,000.0

0

$

30,000.00

$

30,000.0

0

$

30,000.0

0

$

30,000.0

0

$

30,000.00

Sales revenue

$

195,00,0

00.00

$

180,00,000.0

0

$

165,00,0

00.00

$

150,00,0

00.00

$

135,00,0

00.00

$

120,00,000.0

0

Variable cost

$ -

78,00,00

0.00

$

-

72,00,000.00

$ -

66,00,00

0.00

$ -

60,00,00

0.00

$ -

54,00,00

0.00

$

-

48,00,000.00

Fixed cost

$ -

2,00,000.

00

$

-2,00,000.00

$ -

2,00,000.

00

$ -

2,00,000.

00

$ -

2,00,000.

00

$

-2,00,000.00

Depreciation

$ -

24,96,00

0.00

$

-

24,96,000.00

$ -

24,96,00

0.00

$ -

24,96,00

0.00

$ -

24,96,00

0.00

$

-

24,96,000.00

opportunity

sales revenue

$

5,00,000.

00

$

5,00,000.00

$

5,00,000.

00

$

5,00,000.

00

$

5,00,000.

00

$

5,00,000.00

Cost of

production

$ -

2,00,000.

00

$

-2,00,000.00

$ -

2,00,000.

00

$ -

2,00,000.

00

$ -

2,00,000.

00

$

-2,00,000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL MANAGEMENT

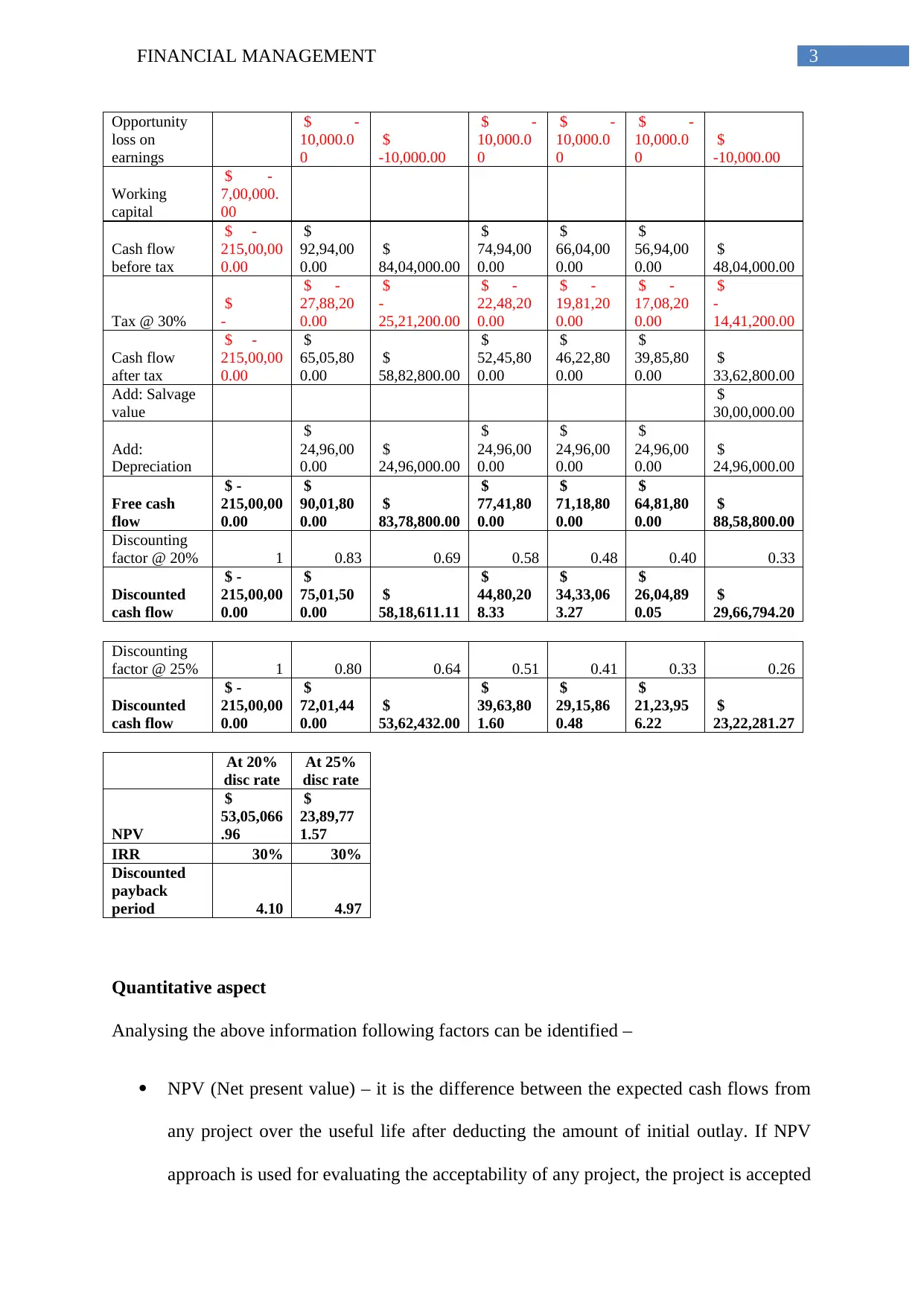

Opportunity

loss on

earnings

$ -

10,000.0

0

$

-10,000.00

$ -

10,000.0

0

$ -

10,000.0

0

$ -

10,000.0

0

$

-10,000.00

Working

capital

$ -

7,00,000.

00

Cash flow

before tax

$ -

215,00,00

0.00

$

92,94,00

0.00

$

84,04,000.00

$

74,94,00

0.00

$

66,04,00

0.00

$

56,94,00

0.00

$

48,04,000.00

Tax @ 30%

$

-

$ -

27,88,20

0.00

$

-

25,21,200.00

$ -

22,48,20

0.00

$ -

19,81,20

0.00

$ -

17,08,20

0.00

$

-

14,41,200.00

Cash flow

after tax

$ -

215,00,00

0.00

$

65,05,80

0.00

$

58,82,800.00

$

52,45,80

0.00

$

46,22,80

0.00

$

39,85,80

0.00

$

33,62,800.00

Add: Salvage

value

$

30,00,000.00

Add:

Depreciation

$

24,96,00

0.00

$

24,96,000.00

$

24,96,00

0.00

$

24,96,00

0.00

$

24,96,00

0.00

$

24,96,000.00

Free cash

flow

$ -

215,00,00

0.00

$

90,01,80

0.00

$

83,78,800.00

$

77,41,80

0.00

$

71,18,80

0.00

$

64,81,80

0.00

$

88,58,800.00

Discounting

factor @ 20% 1 0.83 0.69 0.58 0.48 0.40 0.33

Discounted

cash flow

$ -

215,00,00

0.00

$

75,01,50

0.00

$

58,18,611.11

$

44,80,20

8.33

$

34,33,06

3.27

$

26,04,89

0.05

$

29,66,794.20

Discounting

factor @ 25% 1 0.80 0.64 0.51 0.41 0.33 0.26

Discounted

cash flow

$ -

215,00,00

0.00

$

72,01,44

0.00

$

53,62,432.00

$

39,63,80

1.60

$

29,15,86

0.48

$

21,23,95

6.22

$

23,22,281.27

At 20%

disc rate

At 25%

disc rate

NPV

$

53,05,066

.96

$

23,89,77

1.57

IRR 30% 30%

Discounted

payback

period 4.10 4.97

Quantitative aspect

Analysing the above information following factors can be identified –

NPV (Net present value) – it is the difference between the expected cash flows from

any project over the useful life after deducting the amount of initial outlay. If NPV

approach is used for evaluating the acceptability of any project, the project is accepted

Opportunity

loss on

earnings

$ -

10,000.0

0

$

-10,000.00

$ -

10,000.0

0

$ -

10,000.0

0

$ -

10,000.0

0

$

-10,000.00

Working

capital

$ -

7,00,000.

00

Cash flow

before tax

$ -

215,00,00

0.00

$

92,94,00

0.00

$

84,04,000.00

$

74,94,00

0.00

$

66,04,00

0.00

$

56,94,00

0.00

$

48,04,000.00

Tax @ 30%

$

-

$ -

27,88,20

0.00

$

-

25,21,200.00

$ -

22,48,20

0.00

$ -

19,81,20

0.00

$ -

17,08,20

0.00

$

-

14,41,200.00

Cash flow

after tax

$ -

215,00,00

0.00

$

65,05,80

0.00

$

58,82,800.00

$

52,45,80

0.00

$

46,22,80

0.00

$

39,85,80

0.00

$

33,62,800.00

Add: Salvage

value

$

30,00,000.00

Add:

Depreciation

$

24,96,00

0.00

$

24,96,000.00

$

24,96,00

0.00

$

24,96,00

0.00

$

24,96,00

0.00

$

24,96,000.00

Free cash

flow

$ -

215,00,00

0.00

$

90,01,80

0.00

$

83,78,800.00

$

77,41,80

0.00

$

71,18,80

0.00

$

64,81,80

0.00

$

88,58,800.00

Discounting

factor @ 20% 1 0.83 0.69 0.58 0.48 0.40 0.33

Discounted

cash flow

$ -

215,00,00

0.00

$

75,01,50

0.00

$

58,18,611.11

$

44,80,20

8.33

$

34,33,06

3.27

$

26,04,89

0.05

$

29,66,794.20

Discounting

factor @ 25% 1 0.80 0.64 0.51 0.41 0.33 0.26

Discounted

cash flow

$ -

215,00,00

0.00

$

72,01,44

0.00

$

53,62,432.00

$

39,63,80

1.60

$

29,15,86

0.48

$

21,23,95

6.22

$

23,22,281.27

At 20%

disc rate

At 25%

disc rate

NPV

$

53,05,066

.96

$

23,89,77

1.57

IRR 30% 30%

Discounted

payback

period 4.10 4.97

Quantitative aspect

Analysing the above information following factors can be identified –

NPV (Net present value) – it is the difference between the expected cash flows from

any project over the useful life after deducting the amount of initial outlay. If NPV

approach is used for evaluating the acceptability of any project, the project is accepted

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL MANAGEMENT

if the NPV of the project is positive and conversely, it is rejected if NPV of the project

is negative (Shu, Zeithammer and Payne 2016). It is identified from the computation

for Q-Powerboat project that the NPV is $ 53,05,066.96 at the WACC of 20%.

Positive NPV is indicating that the project will create value for the shareholders and

hence shall be proceed with.

IRR (internal rate of return) – at IRR, net present value of all the cash flow from the

project are zero. It is used for ranking 2 or more projects and analysing the

acceptability of the project. If IRR approach is used for evaluating the acceptability of

any project, the project is accepted if the IRR is more than the cost of capital for the

company. Conversely, if the IRR of the project is lower than the company’s cost of

capital it indicates that the project will not be able to generate sufficient return to

cover up the capital cost and hence is not acceptable (Dhavale and Sarkis 2018). It is

identified from the computation for Q-Powerboat project that the IRR of the project is

30% whereas the cost of capital of the project is 20%. IRR more than cost capital is

suggests that the project can be accepted as it will be able to generate return from the

project.

Discounted payback period – time required by any project to recover its initial outlay

is known as the discounted payback period. For calculating the discounted payback

period of any project, its discounted cash flows are considered. If discounted payback

period approach is used for evaluating the acceptability of any project, the project is

accepted if the discounted payback period is lower than the project’s useful life.

Conversely, the project is not accepted if the discounted payback period is higher than

the project’s useful life. It indicates that the project will not be able to recover the

initial capital outlay during its lifetime (Götze, Northcott and Schuster 2015). It is

identified from the computation for Q-Powerboat project that its discounted payback

if the NPV of the project is positive and conversely, it is rejected if NPV of the project

is negative (Shu, Zeithammer and Payne 2016). It is identified from the computation

for Q-Powerboat project that the NPV is $ 53,05,066.96 at the WACC of 20%.

Positive NPV is indicating that the project will create value for the shareholders and

hence shall be proceed with.

IRR (internal rate of return) – at IRR, net present value of all the cash flow from the

project are zero. It is used for ranking 2 or more projects and analysing the

acceptability of the project. If IRR approach is used for evaluating the acceptability of

any project, the project is accepted if the IRR is more than the cost of capital for the

company. Conversely, if the IRR of the project is lower than the company’s cost of

capital it indicates that the project will not be able to generate sufficient return to

cover up the capital cost and hence is not acceptable (Dhavale and Sarkis 2018). It is

identified from the computation for Q-Powerboat project that the IRR of the project is

30% whereas the cost of capital of the project is 20%. IRR more than cost capital is

suggests that the project can be accepted as it will be able to generate return from the

project.

Discounted payback period – time required by any project to recover its initial outlay

is known as the discounted payback period. For calculating the discounted payback

period of any project, its discounted cash flows are considered. If discounted payback

period approach is used for evaluating the acceptability of any project, the project is

accepted if the discounted payback period is lower than the project’s useful life.

Conversely, the project is not accepted if the discounted payback period is higher than

the project’s useful life. It indicates that the project will not be able to recover the

initial capital outlay during its lifetime (Götze, Northcott and Schuster 2015). It is

identified from the computation for Q-Powerboat project that its discounted payback

5FINANCIAL MANAGEMENT

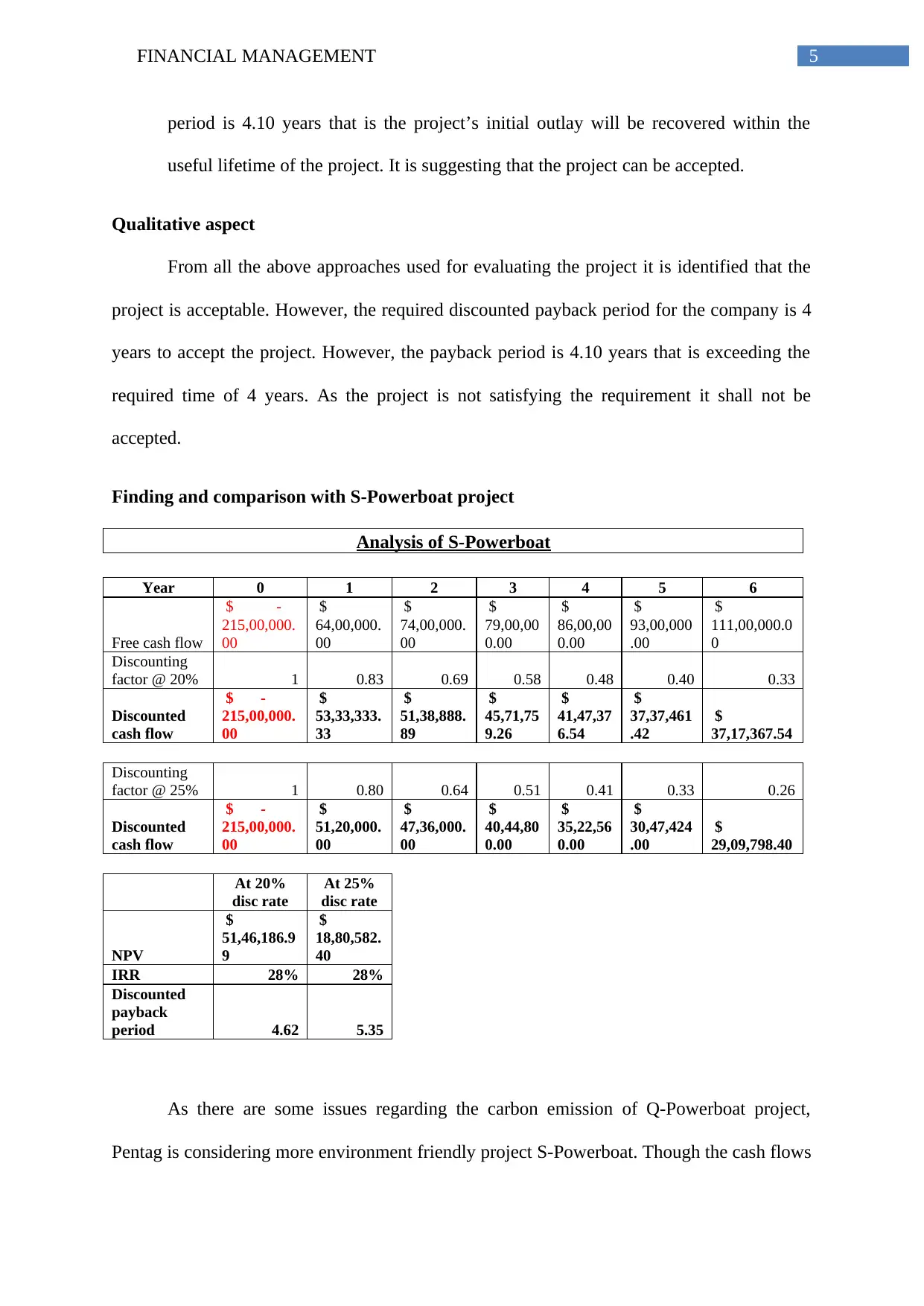

period is 4.10 years that is the project’s initial outlay will be recovered within the

useful lifetime of the project. It is suggesting that the project can be accepted.

Qualitative aspect

From all the above approaches used for evaluating the project it is identified that the

project is acceptable. However, the required discounted payback period for the company is 4

years to accept the project. However, the payback period is 4.10 years that is exceeding the

required time of 4 years. As the project is not satisfying the requirement it shall not be

accepted.

Finding and comparison with S-Powerboat project

Analysis of S-Powerboat

Year 0 1 2 3 4 5 6

Free cash flow

$ -

215,00,000.

00

$

64,00,000.

00

$

74,00,000.

00

$

79,00,00

0.00

$

86,00,00

0.00

$

93,00,000

.00

$

111,00,000.0

0

Discounting

factor @ 20% 1 0.83 0.69 0.58 0.48 0.40 0.33

Discounted

cash flow

$ -

215,00,000.

00

$

53,33,333.

33

$

51,38,888.

89

$

45,71,75

9.26

$

41,47,37

6.54

$

37,37,461

.42

$

37,17,367.54

Discounting

factor @ 25% 1 0.80 0.64 0.51 0.41 0.33 0.26

Discounted

cash flow

$ -

215,00,000.

00

$

51,20,000.

00

$

47,36,000.

00

$

40,44,80

0.00

$

35,22,56

0.00

$

30,47,424

.00

$

29,09,798.40

At 20%

disc rate

At 25%

disc rate

NPV

$

51,46,186.9

9

$

18,80,582.

40

IRR 28% 28%

Discounted

payback

period 4.62 5.35

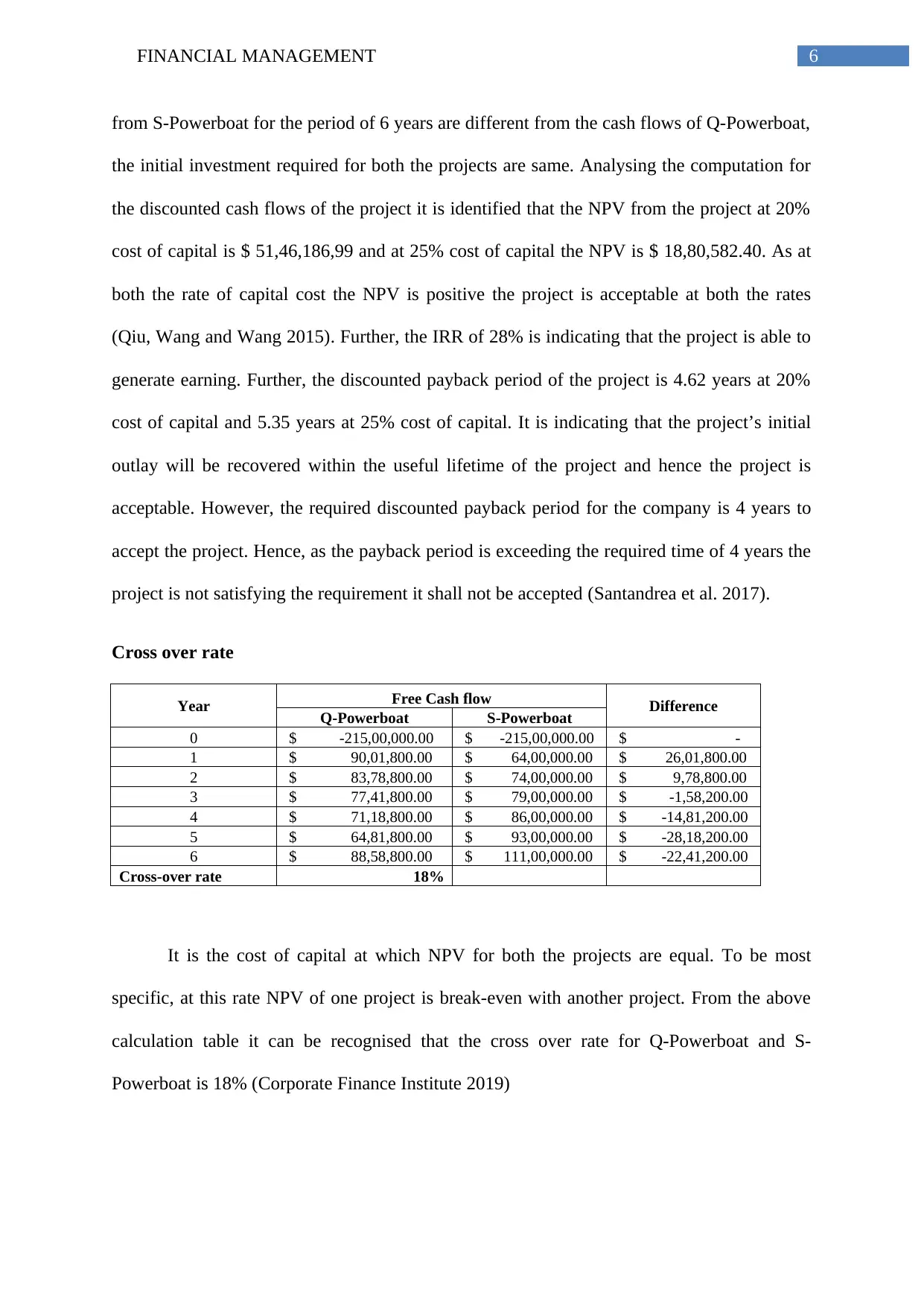

As there are some issues regarding the carbon emission of Q-Powerboat project,

Pentag is considering more environment friendly project S-Powerboat. Though the cash flows

period is 4.10 years that is the project’s initial outlay will be recovered within the

useful lifetime of the project. It is suggesting that the project can be accepted.

Qualitative aspect

From all the above approaches used for evaluating the project it is identified that the

project is acceptable. However, the required discounted payback period for the company is 4

years to accept the project. However, the payback period is 4.10 years that is exceeding the

required time of 4 years. As the project is not satisfying the requirement it shall not be

accepted.

Finding and comparison with S-Powerboat project

Analysis of S-Powerboat

Year 0 1 2 3 4 5 6

Free cash flow

$ -

215,00,000.

00

$

64,00,000.

00

$

74,00,000.

00

$

79,00,00

0.00

$

86,00,00

0.00

$

93,00,000

.00

$

111,00,000.0

0

Discounting

factor @ 20% 1 0.83 0.69 0.58 0.48 0.40 0.33

Discounted

cash flow

$ -

215,00,000.

00

$

53,33,333.

33

$

51,38,888.

89

$

45,71,75

9.26

$

41,47,37

6.54

$

37,37,461

.42

$

37,17,367.54

Discounting

factor @ 25% 1 0.80 0.64 0.51 0.41 0.33 0.26

Discounted

cash flow

$ -

215,00,000.

00

$

51,20,000.

00

$

47,36,000.

00

$

40,44,80

0.00

$

35,22,56

0.00

$

30,47,424

.00

$

29,09,798.40

At 20%

disc rate

At 25%

disc rate

NPV

$

51,46,186.9

9

$

18,80,582.

40

IRR 28% 28%

Discounted

payback

period 4.62 5.35

As there are some issues regarding the carbon emission of Q-Powerboat project,

Pentag is considering more environment friendly project S-Powerboat. Though the cash flows

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL MANAGEMENT

from S-Powerboat for the period of 6 years are different from the cash flows of Q-Powerboat,

the initial investment required for both the projects are same. Analysing the computation for

the discounted cash flows of the project it is identified that the NPV from the project at 20%

cost of capital is $ 51,46,186,99 and at 25% cost of capital the NPV is $ 18,80,582.40. As at

both the rate of capital cost the NPV is positive the project is acceptable at both the rates

(Qiu, Wang and Wang 2015). Further, the IRR of 28% is indicating that the project is able to

generate earning. Further, the discounted payback period of the project is 4.62 years at 20%

cost of capital and 5.35 years at 25% cost of capital. It is indicating that the project’s initial

outlay will be recovered within the useful lifetime of the project and hence the project is

acceptable. However, the required discounted payback period for the company is 4 years to

accept the project. Hence, as the payback period is exceeding the required time of 4 years the

project is not satisfying the requirement it shall not be accepted (Santandrea et al. 2017).

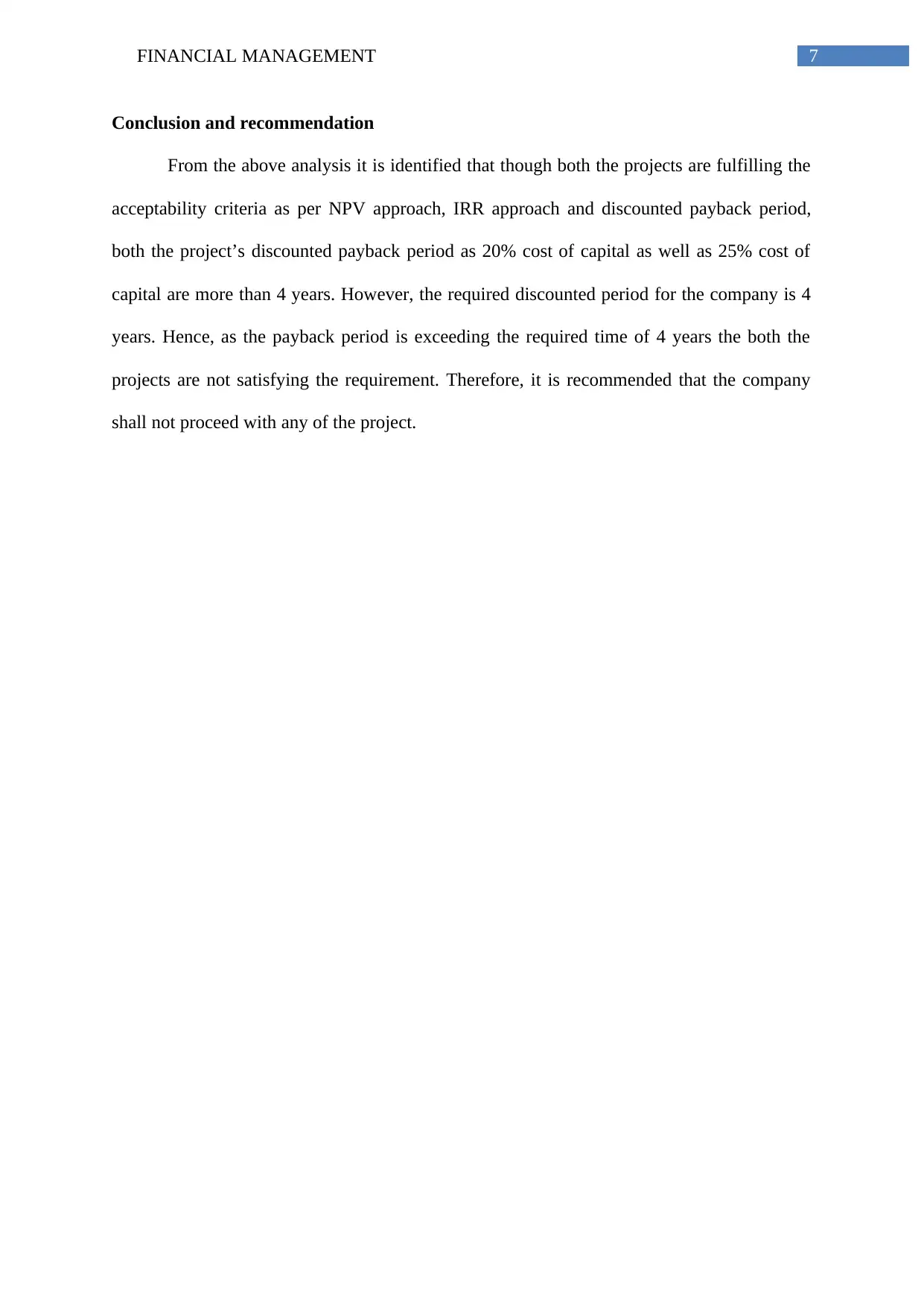

Cross over rate

Year Free Cash flow Difference

Q-Powerboat S-Powerboat

0 $ -215,00,000.00 $ -215,00,000.00 $ -

1 $ 90,01,800.00 $ 64,00,000.00 $ 26,01,800.00

2 $ 83,78,800.00 $ 74,00,000.00 $ 9,78,800.00

3 $ 77,41,800.00 $ 79,00,000.00 $ -1,58,200.00

4 $ 71,18,800.00 $ 86,00,000.00 $ -14,81,200.00

5 $ 64,81,800.00 $ 93,00,000.00 $ -28,18,200.00

6 $ 88,58,800.00 $ 111,00,000.00 $ -22,41,200.00

Cross-over rate 18%

It is the cost of capital at which NPV for both the projects are equal. To be most

specific, at this rate NPV of one project is break-even with another project. From the above

calculation table it can be recognised that the cross over rate for Q-Powerboat and S-

Powerboat is 18% (Corporate Finance Institute 2019)

from S-Powerboat for the period of 6 years are different from the cash flows of Q-Powerboat,

the initial investment required for both the projects are same. Analysing the computation for

the discounted cash flows of the project it is identified that the NPV from the project at 20%

cost of capital is $ 51,46,186,99 and at 25% cost of capital the NPV is $ 18,80,582.40. As at

both the rate of capital cost the NPV is positive the project is acceptable at both the rates

(Qiu, Wang and Wang 2015). Further, the IRR of 28% is indicating that the project is able to

generate earning. Further, the discounted payback period of the project is 4.62 years at 20%

cost of capital and 5.35 years at 25% cost of capital. It is indicating that the project’s initial

outlay will be recovered within the useful lifetime of the project and hence the project is

acceptable. However, the required discounted payback period for the company is 4 years to

accept the project. Hence, as the payback period is exceeding the required time of 4 years the

project is not satisfying the requirement it shall not be accepted (Santandrea et al. 2017).

Cross over rate

Year Free Cash flow Difference

Q-Powerboat S-Powerboat

0 $ -215,00,000.00 $ -215,00,000.00 $ -

1 $ 90,01,800.00 $ 64,00,000.00 $ 26,01,800.00

2 $ 83,78,800.00 $ 74,00,000.00 $ 9,78,800.00

3 $ 77,41,800.00 $ 79,00,000.00 $ -1,58,200.00

4 $ 71,18,800.00 $ 86,00,000.00 $ -14,81,200.00

5 $ 64,81,800.00 $ 93,00,000.00 $ -28,18,200.00

6 $ 88,58,800.00 $ 111,00,000.00 $ -22,41,200.00

Cross-over rate 18%

It is the cost of capital at which NPV for both the projects are equal. To be most

specific, at this rate NPV of one project is break-even with another project. From the above

calculation table it can be recognised that the cross over rate for Q-Powerboat and S-

Powerboat is 18% (Corporate Finance Institute 2019)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MANAGEMENT

Conclusion and recommendation

From the above analysis it is identified that though both the projects are fulfilling the

acceptability criteria as per NPV approach, IRR approach and discounted payback period,

both the project’s discounted payback period as 20% cost of capital as well as 25% cost of

capital are more than 4 years. However, the required discounted period for the company is 4

years. Hence, as the payback period is exceeding the required time of 4 years the both the

projects are not satisfying the requirement. Therefore, it is recommended that the company

shall not proceed with any of the project.

Conclusion and recommendation

From the above analysis it is identified that though both the projects are fulfilling the

acceptability criteria as per NPV approach, IRR approach and discounted payback period,

both the project’s discounted payback period as 20% cost of capital as well as 25% cost of

capital are more than 4 years. However, the required discounted period for the company is 4

years. Hence, as the payback period is exceeding the required time of 4 years the both the

projects are not satisfying the requirement. Therefore, it is recommended that the company

shall not proceed with any of the project.

8FINANCIAL MANAGEMENT

Reference

Corporate Finance Institute., 2019. Crossover Rate - Formula, Examples, and Guide to

Discount Rate, NPV. [online] Available at:

https://corporatefinanceinstitute.com/resources/knowledge/valuation/crossover-rate/

[Accessed 9 May 2019].

DeFusco, R.A., McLeavey, D.W., Pinto, J.E., Anson, M.J. and Runkle, D.E.,

2015. Quantitative investment analysis. John Wiley & Sons.

Dhavale, D. G., and Sarkis, J., 2018. Stochastic internal rate of return on investments in

sustainable assets generating carbon credits. Computers & Operations Research, 89, 324-336.

Götze, U., Northcott, D., and Schuster, P., 2015. Discounted Cash Flow Methods.

In Investment Appraisal (pp. 47-83). Springer, Berlin, Heidelberg.

Qiu, Y., Wang, Y. D., and Wang, J., 2015. Implied discount rate and payback threshold of

energy efficiency investment in the industrial sector. Applied Economics, 47(21), 2218-2233.

Santandrea, M., Sironi, A., Grassi, L., and Giorgino, M., 2017. Concentration risk and

internal rate of return: Evidence from the infrastructure equity market. International Journal

of Project Management, 35(3), 241-251.

Shu, S. B., Zeithammer, R., and Payne, J. W., 2016. Consumer preferences for annuity

attributes: Beyond net present value. Journal of Marketing Research, 53(2), 240-262.

Reference

Corporate Finance Institute., 2019. Crossover Rate - Formula, Examples, and Guide to

Discount Rate, NPV. [online] Available at:

https://corporatefinanceinstitute.com/resources/knowledge/valuation/crossover-rate/

[Accessed 9 May 2019].

DeFusco, R.A., McLeavey, D.W., Pinto, J.E., Anson, M.J. and Runkle, D.E.,

2015. Quantitative investment analysis. John Wiley & Sons.

Dhavale, D. G., and Sarkis, J., 2018. Stochastic internal rate of return on investments in

sustainable assets generating carbon credits. Computers & Operations Research, 89, 324-336.

Götze, U., Northcott, D., and Schuster, P., 2015. Discounted Cash Flow Methods.

In Investment Appraisal (pp. 47-83). Springer, Berlin, Heidelberg.

Qiu, Y., Wang, Y. D., and Wang, J., 2015. Implied discount rate and payback threshold of

energy efficiency investment in the industrial sector. Applied Economics, 47(21), 2218-2233.

Santandrea, M., Sironi, A., Grassi, L., and Giorgino, M., 2017. Concentration risk and

internal rate of return: Evidence from the infrastructure equity market. International Journal

of Project Management, 35(3), 241-251.

Shu, S. B., Zeithammer, R., and Payne, J. W., 2016. Consumer preferences for annuity

attributes: Beyond net present value. Journal of Marketing Research, 53(2), 240-262.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL MANAGEMENT

Appendix

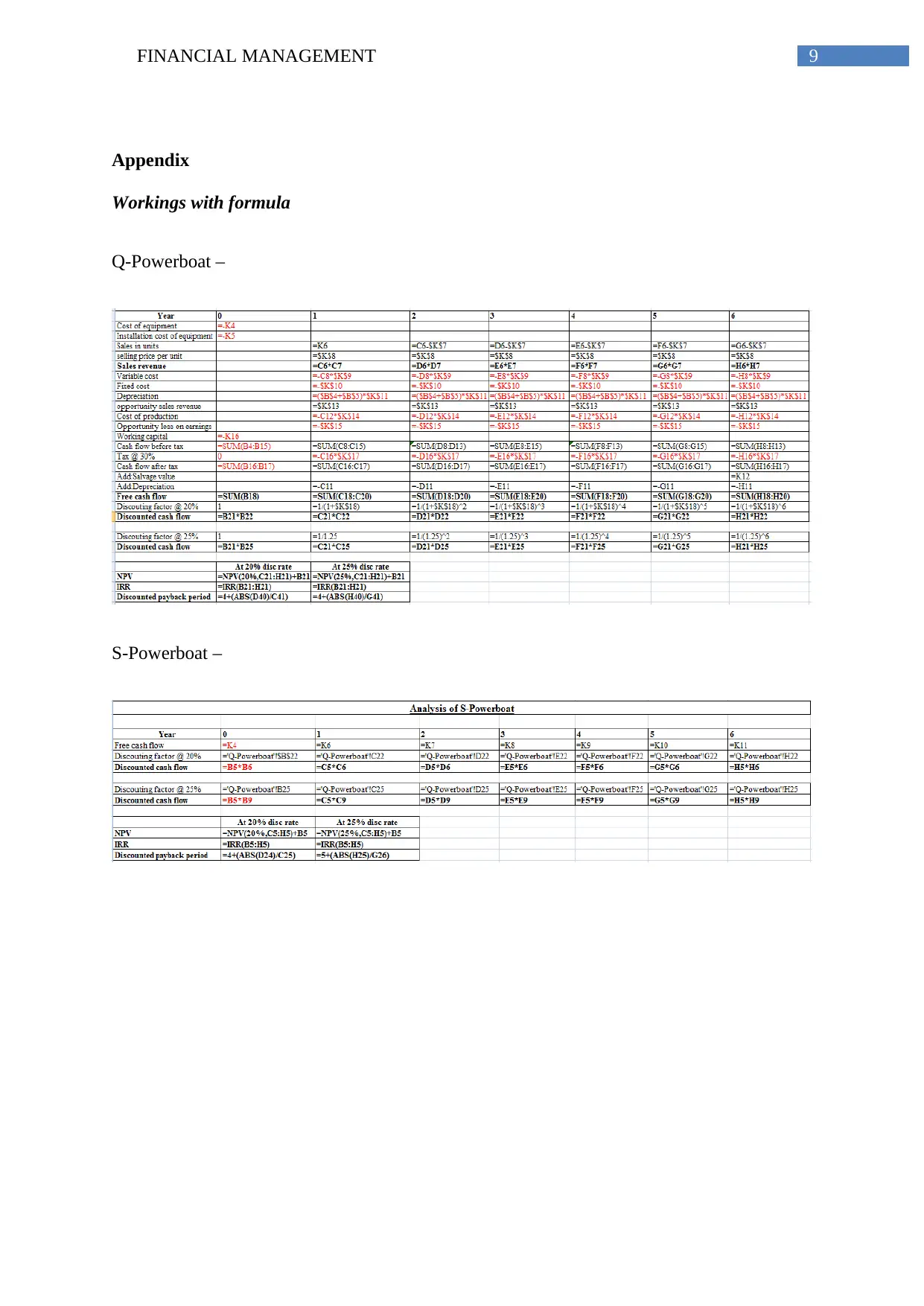

Workings with formula

Q-Powerboat –

S-Powerboat –

Appendix

Workings with formula

Q-Powerboat –

S-Powerboat –

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.