In-depth Financial Analysis of PPHE Hotel Group and ABHL Report

VerifiedAdded on 2023/04/26

|28

|5899

|103

Report

AI Summary

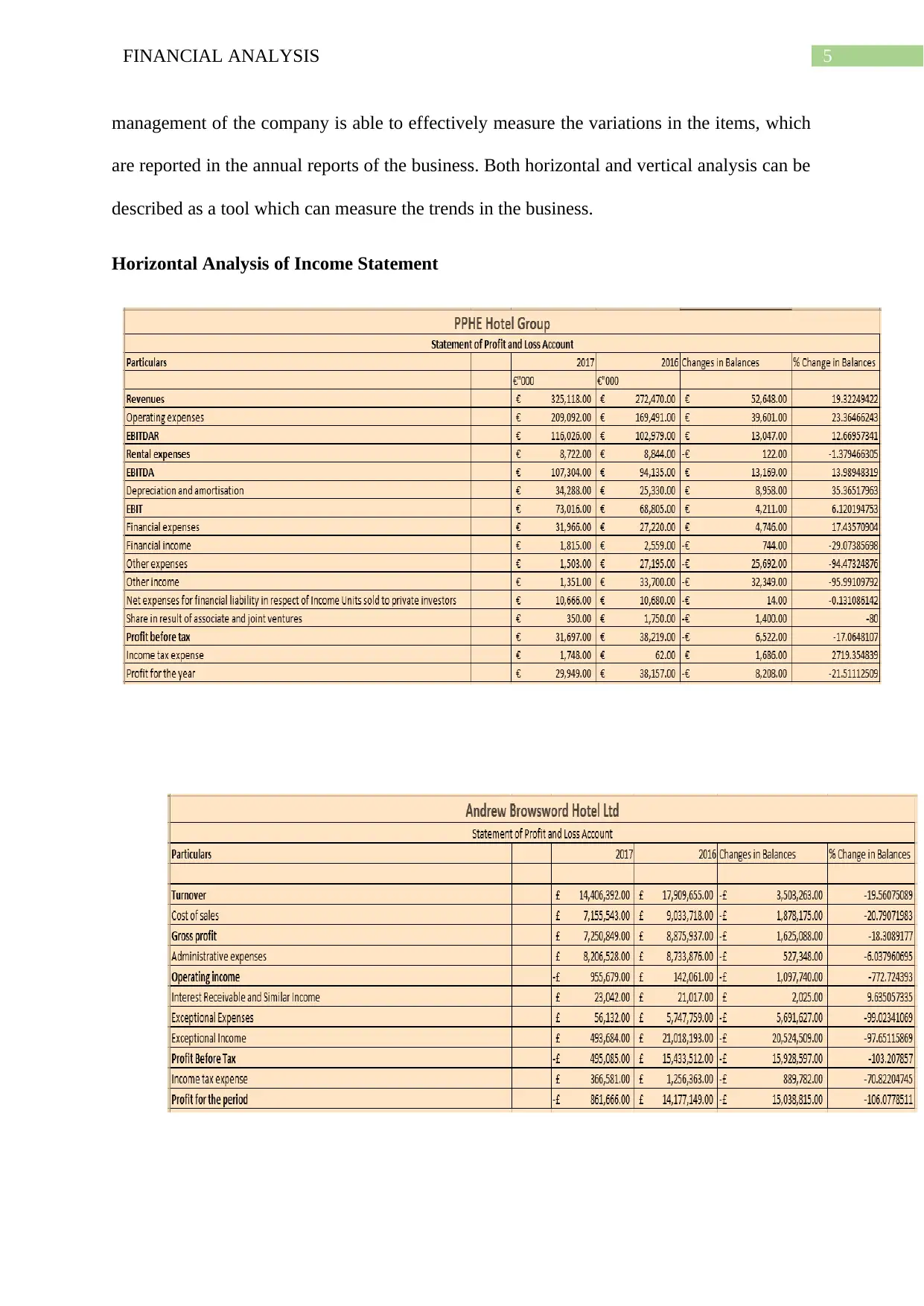

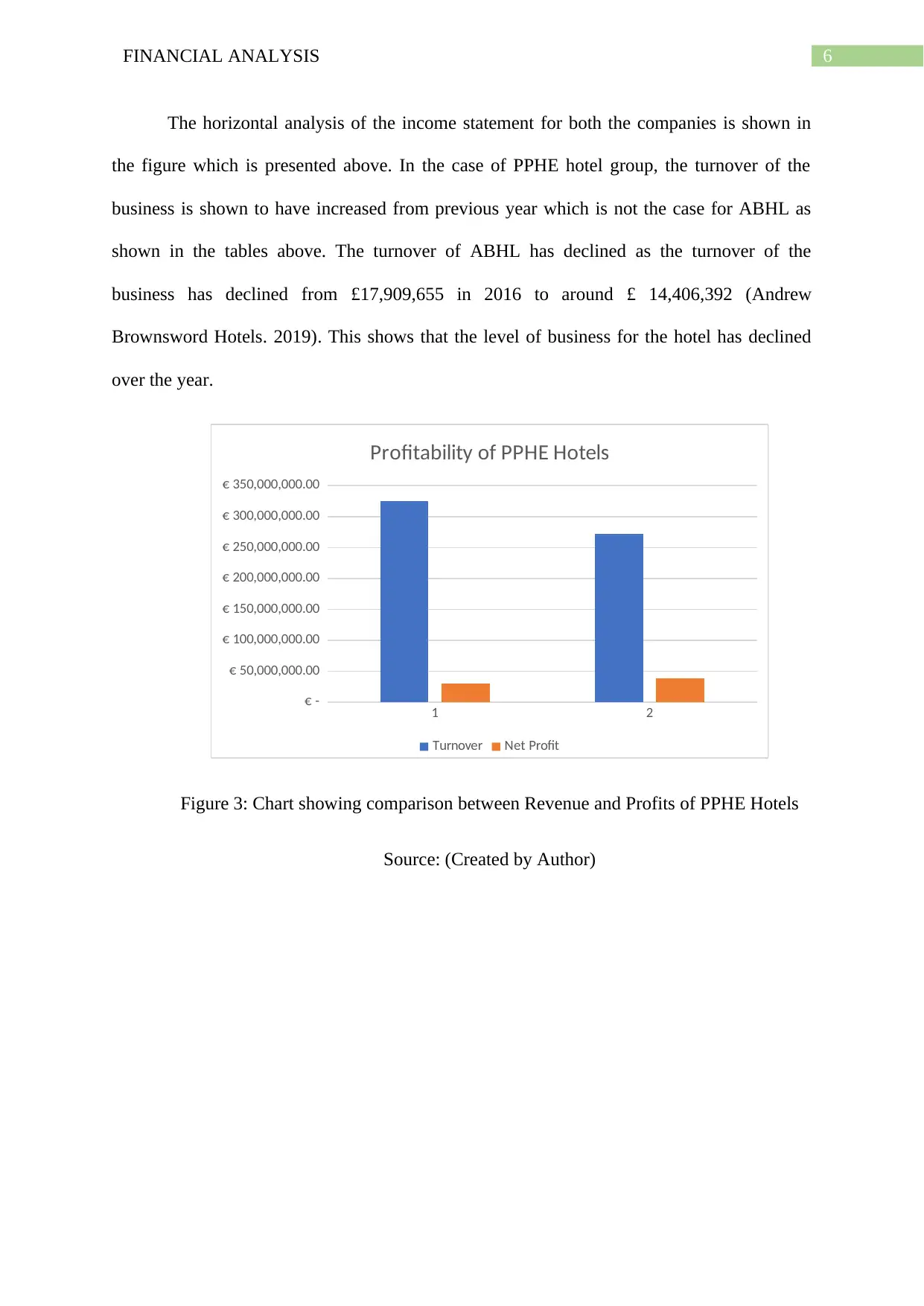

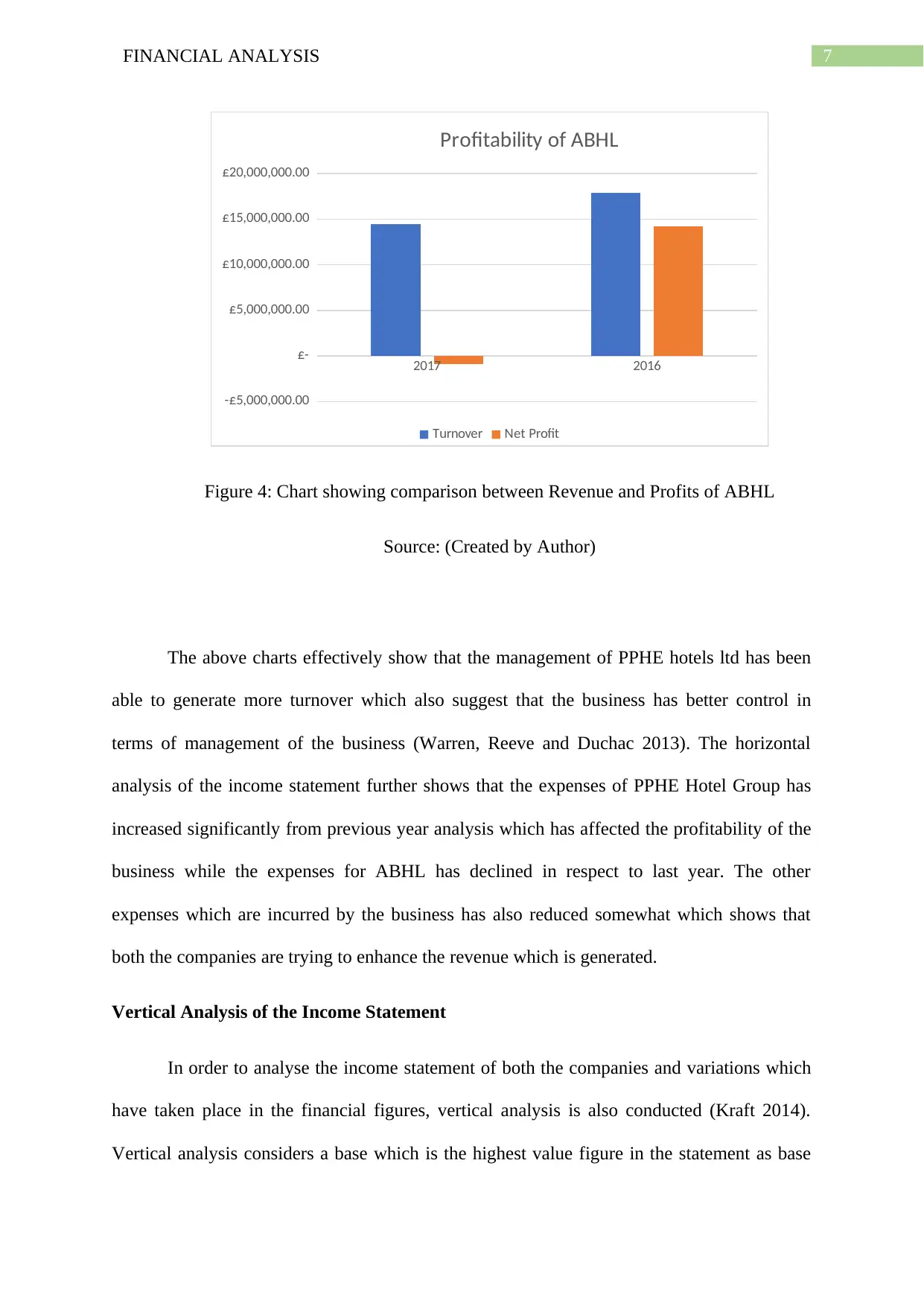

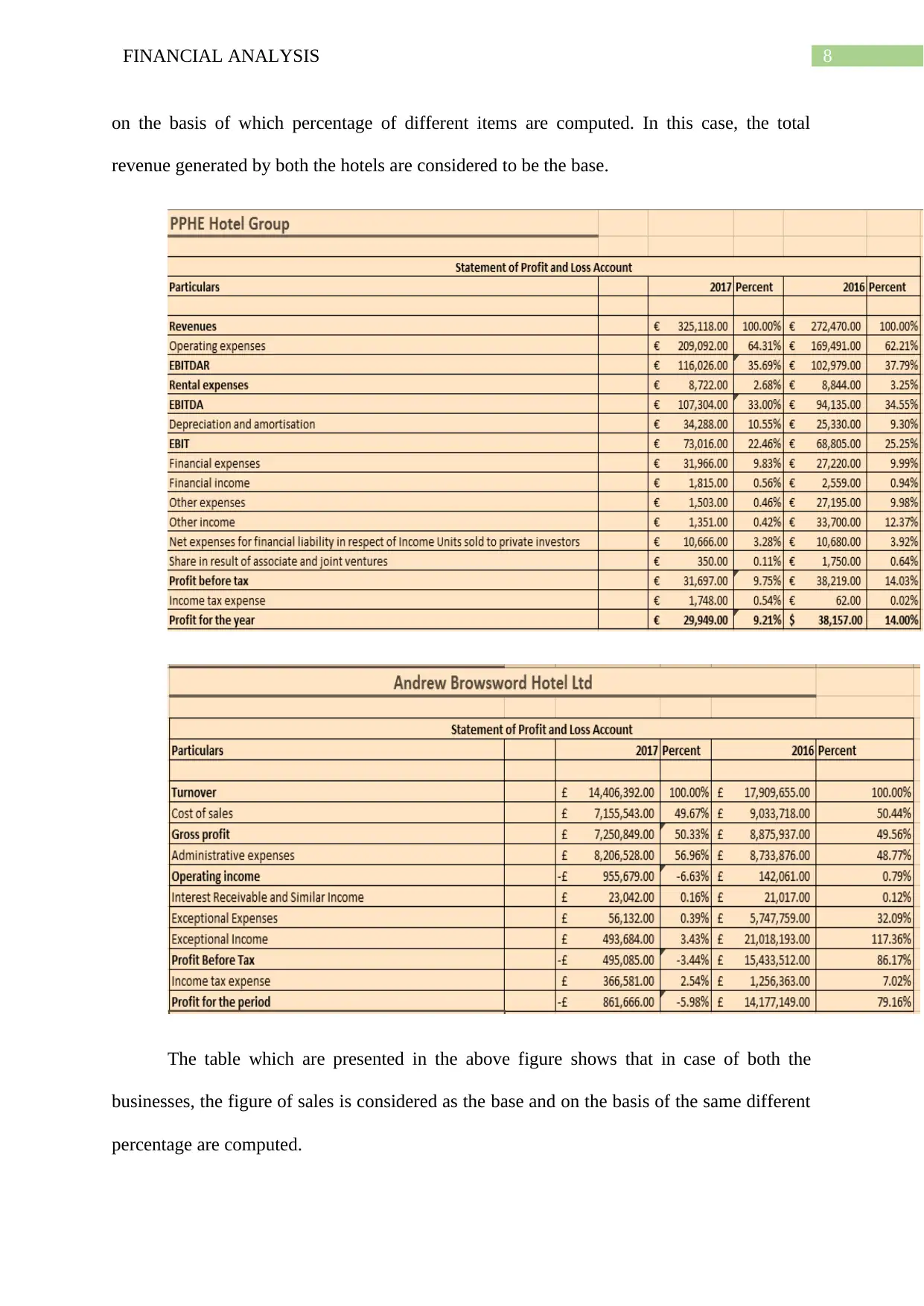

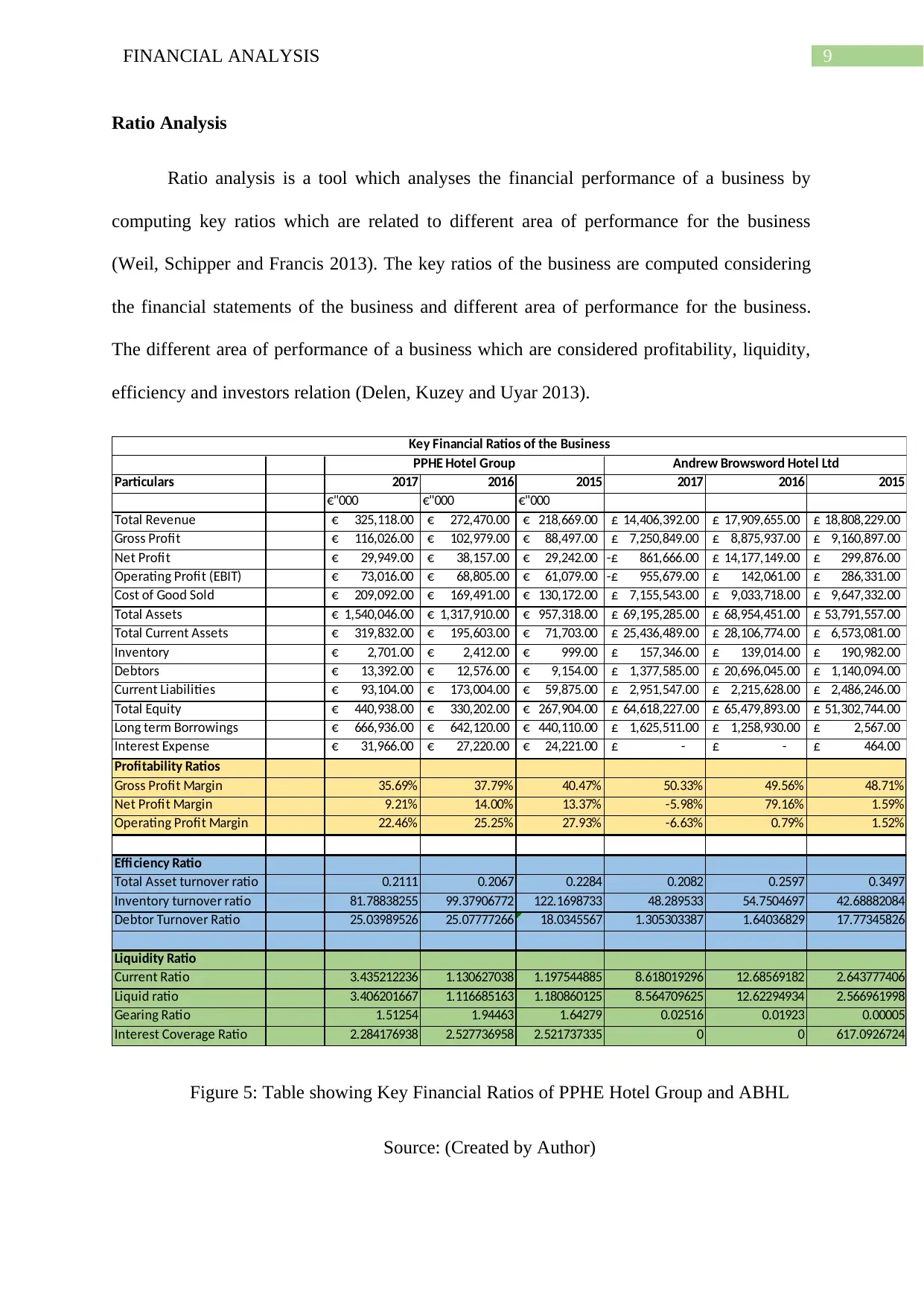

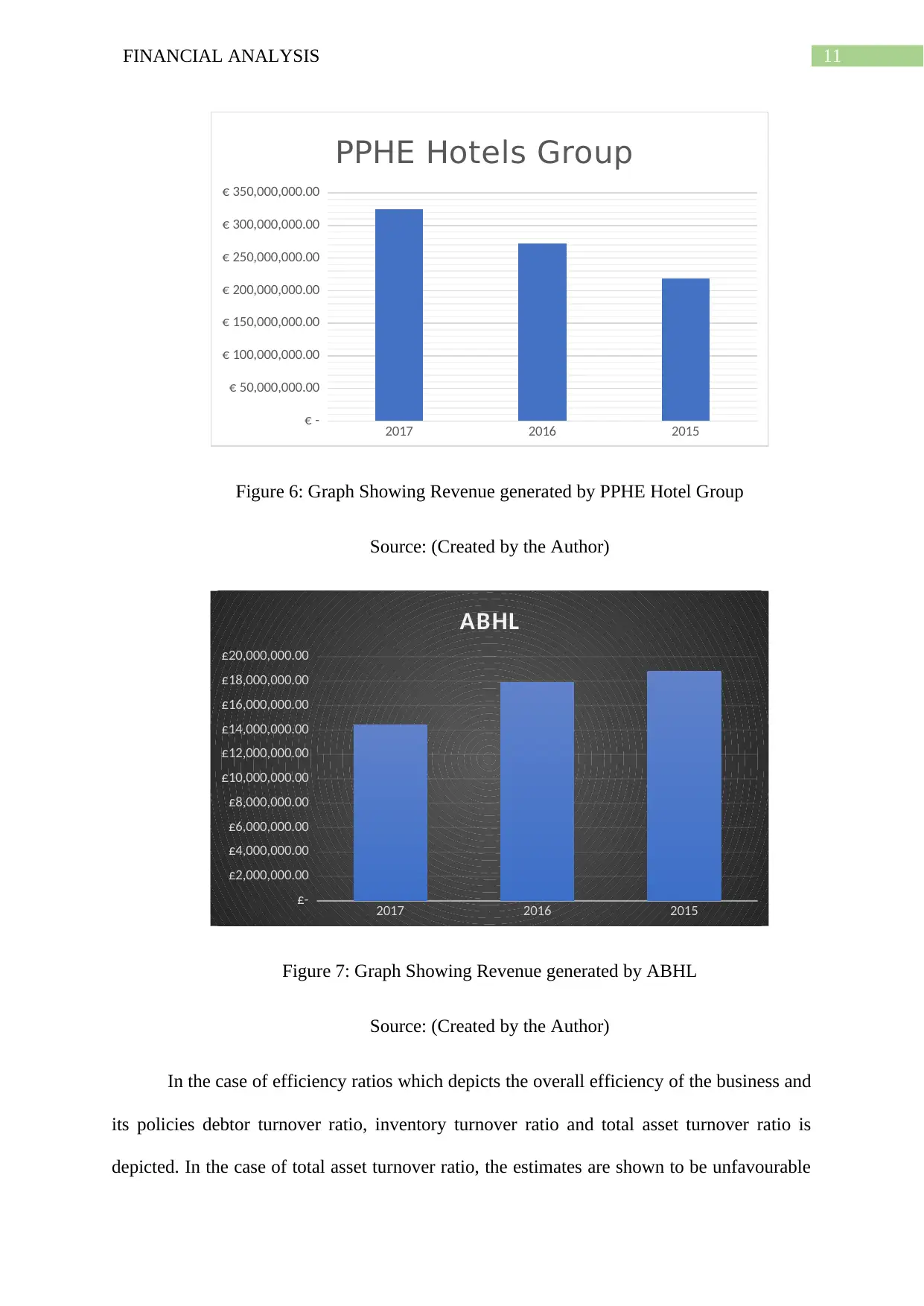

This report delivers a comprehensive financial analysis of PPHE Hotel Group and Andrew Brownsword Hotels Limited, utilizing ratio analysis to evaluate profitability, asset management, liquidity, and investor relations for both entities. It delves into the cost of capital for PPHE, determining its cost of equity and valuing its share price through forecasting and growth factor analysis. Furthermore, the report examines PPHE's share price movements, identifying key influencing factors, and assesses the potential impact of acquiring Andrew Brownsword Hotels on PPHE's financial statements, exploring possible synergy effects. The analysis includes horizontal and vertical assessments of financial statements, supported by charts and graphs visualizing revenue and profit trends. Key financial ratios are computed and compared over a three-year period (2015-2017) to provide insights into the financial health and performance of both hotel groups.

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.