Practical Application of AASB Standards in Financial Reporting

VerifiedAdded on 2023/06/14

|8

|1968

|479

Practical Assignment

AI Summary

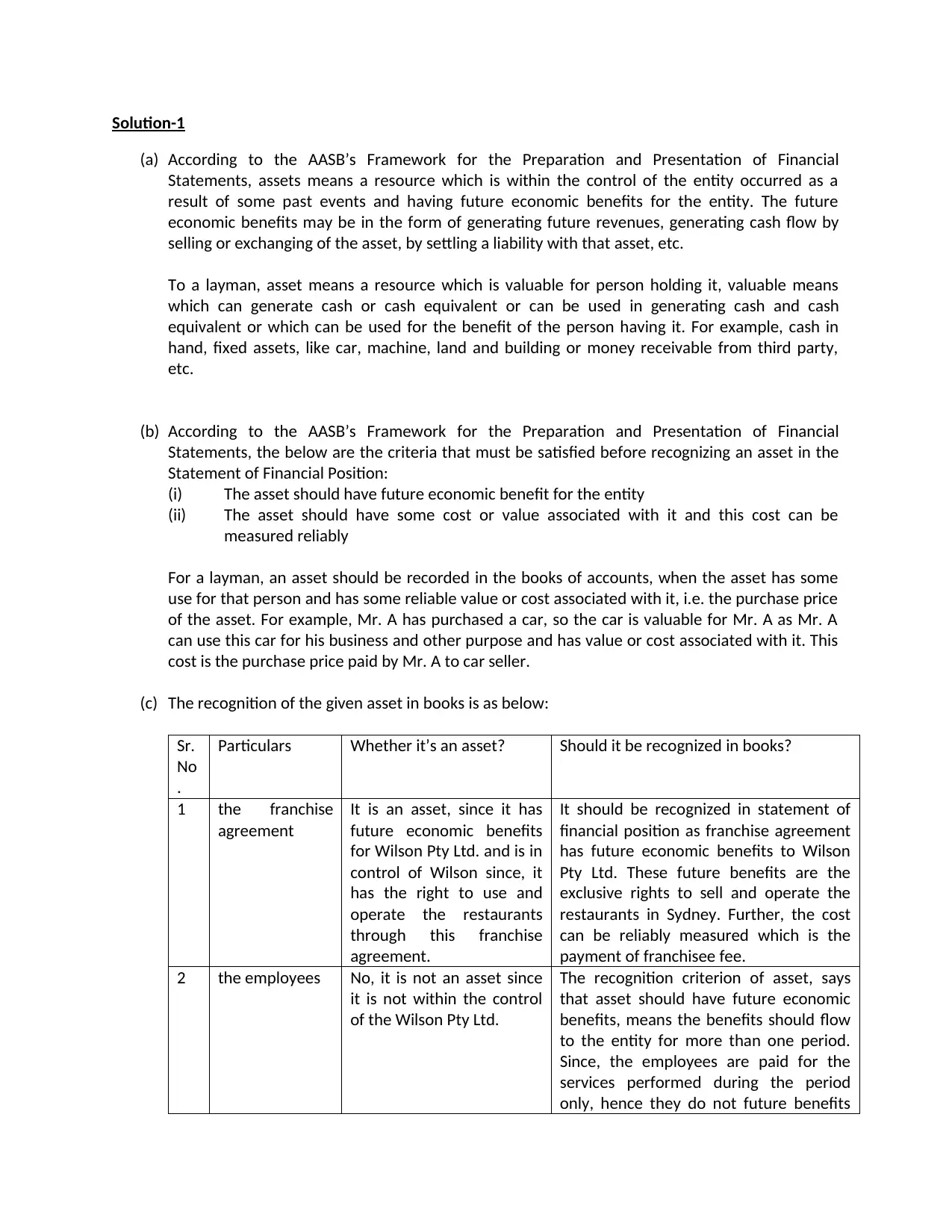

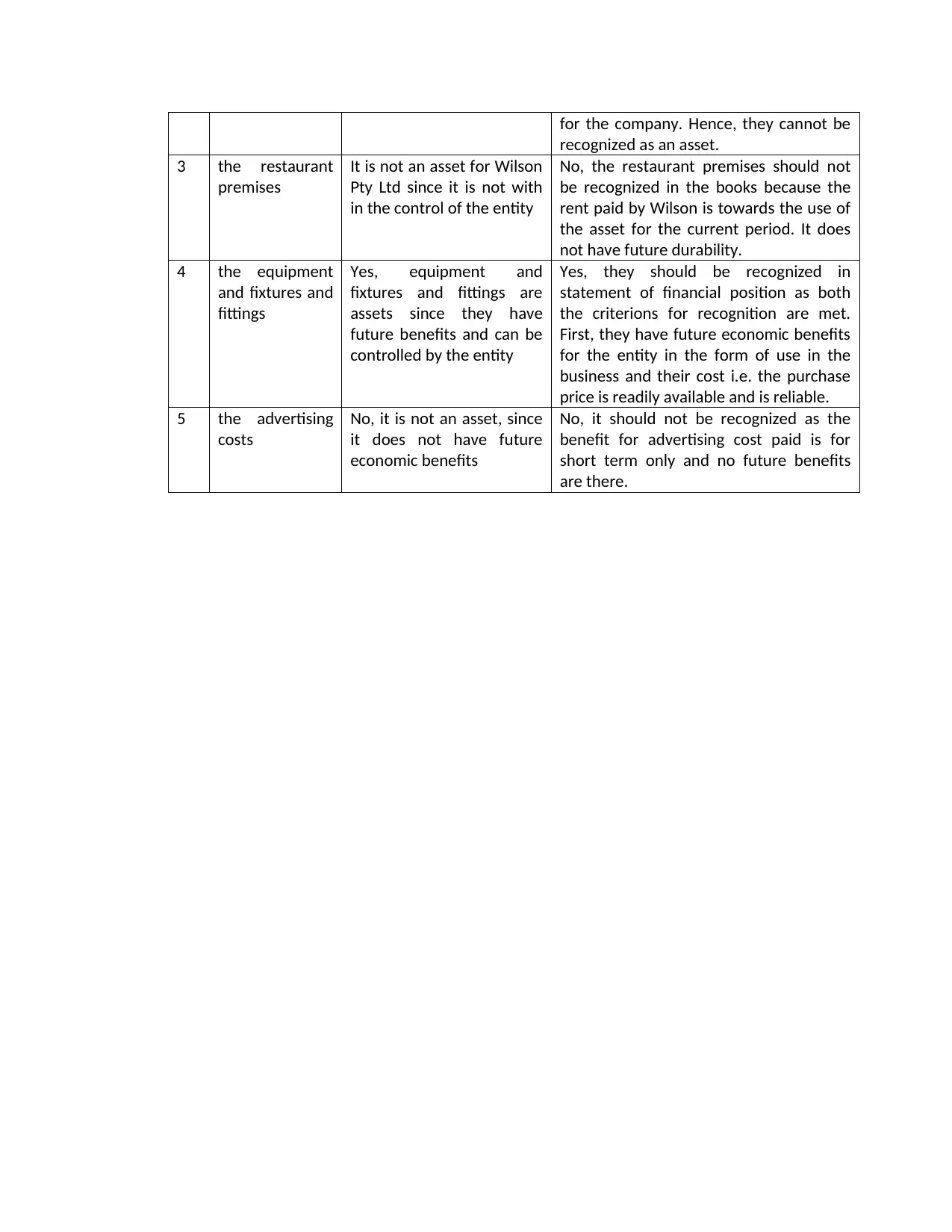

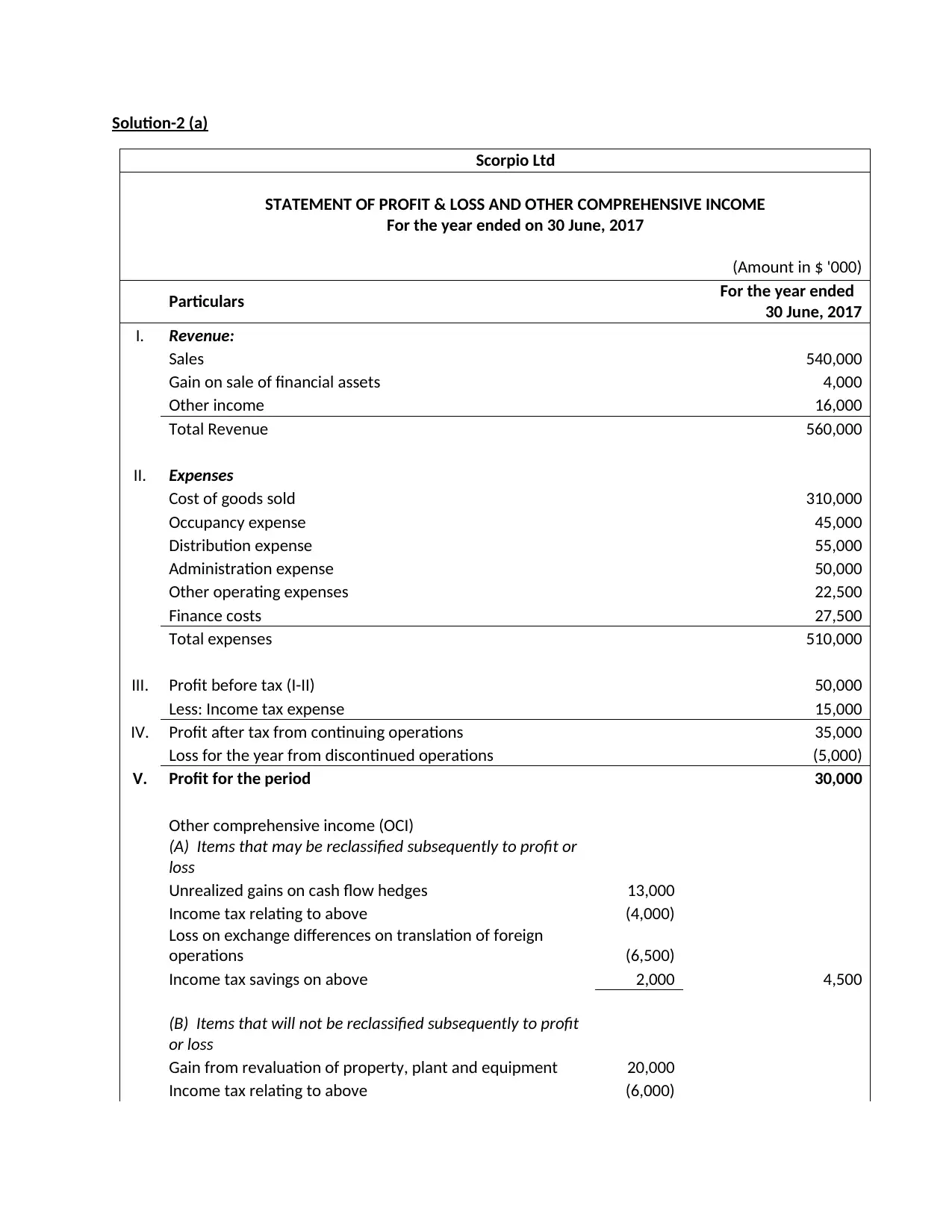

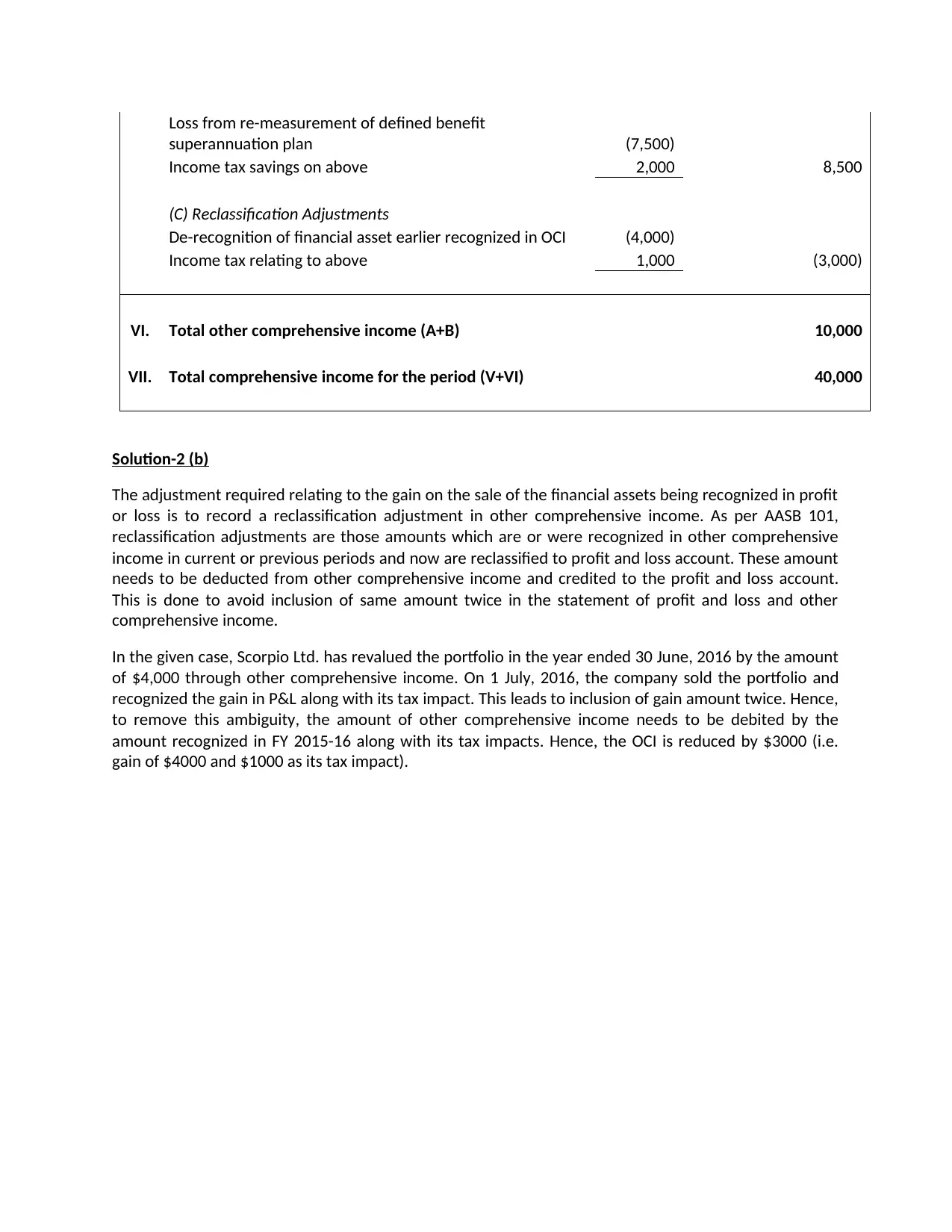

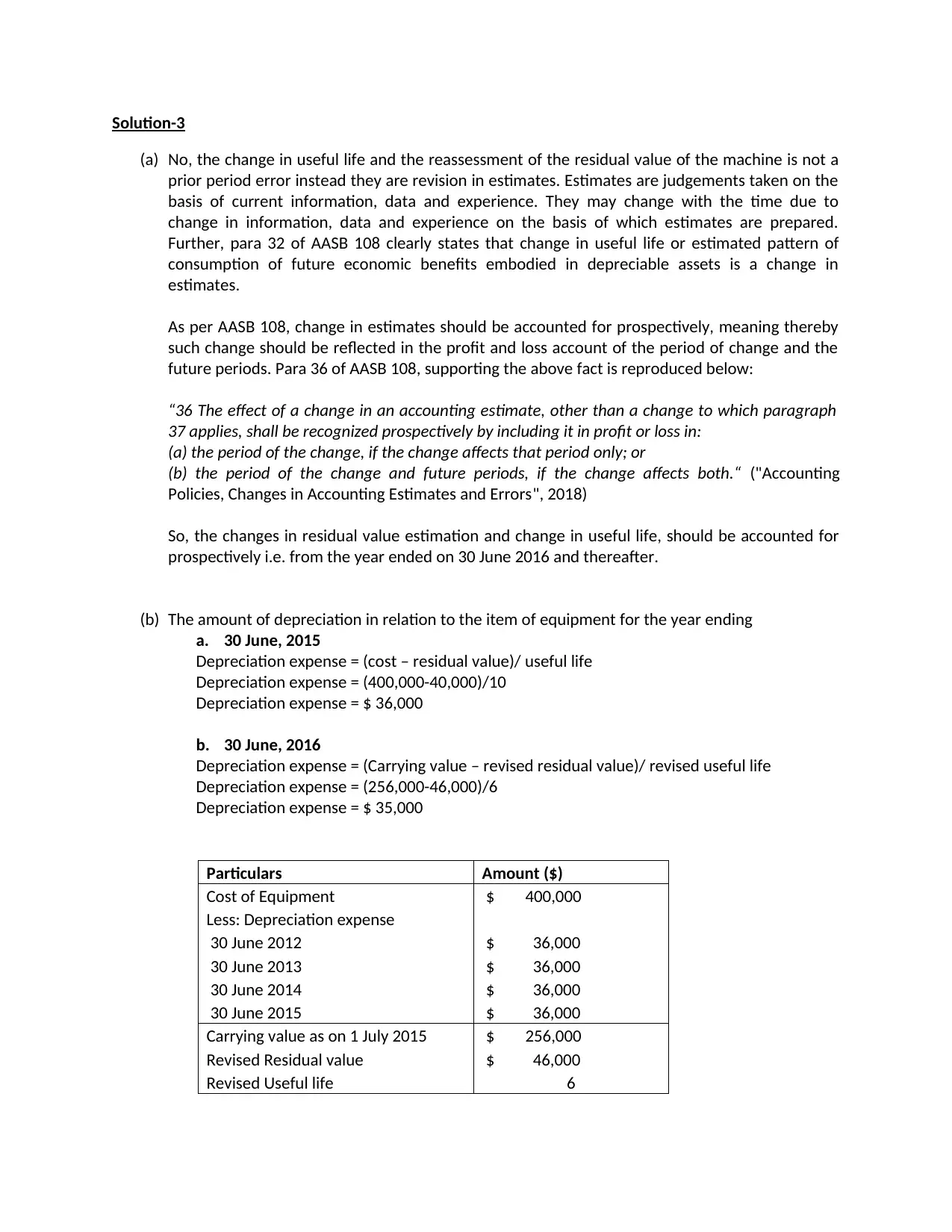

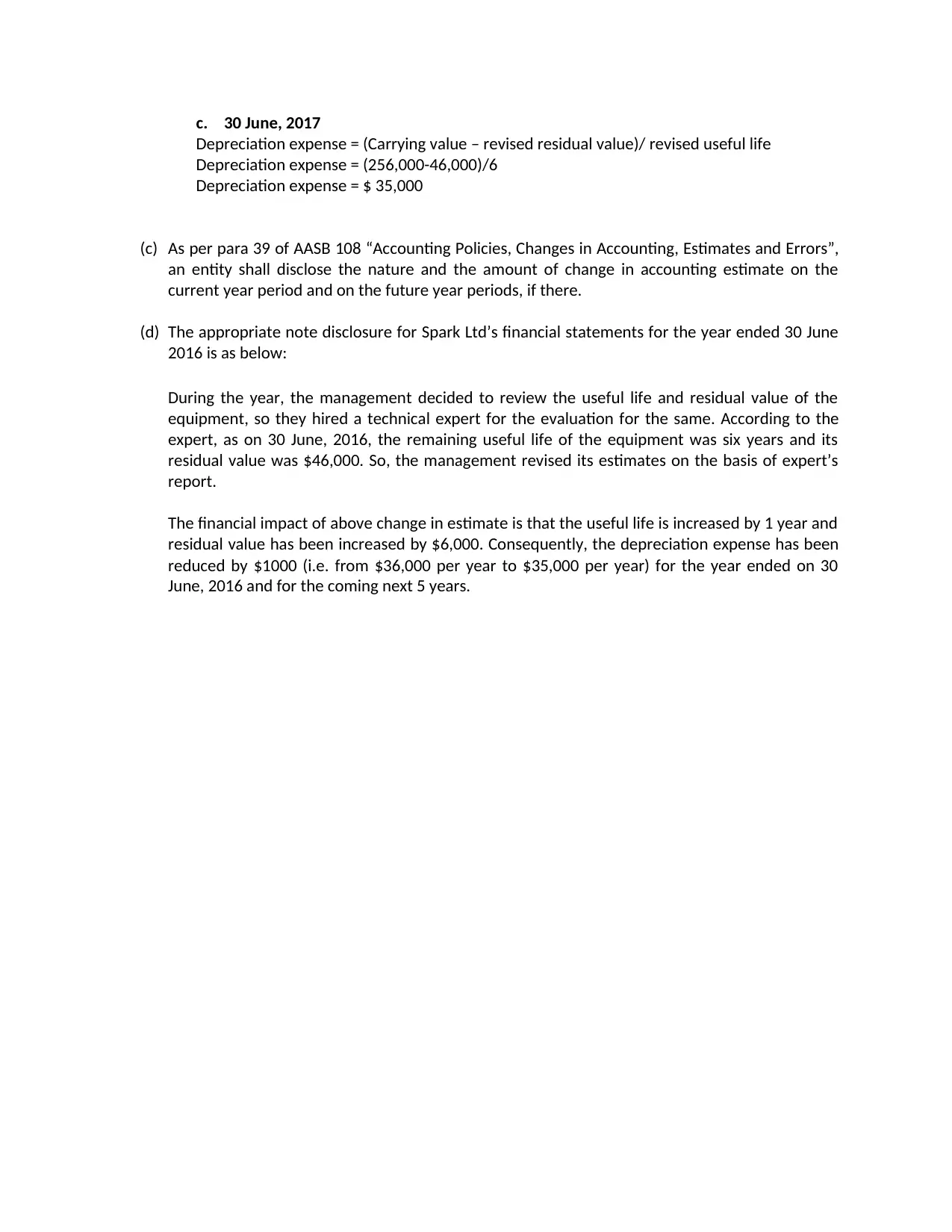

This assignment provides detailed solutions related to the application of Australian Accounting Standards Board (AASB) standards in various financial reporting scenarios. It covers topics such as asset recognition, including the criteria for recognizing assets like franchise agreements, employees, restaurant premises, equipment, and advertising costs, according to the AASB's Framework for the Preparation and Presentation of Financial Statements. Furthermore, it includes the preparation of a Statement of Profit & Loss and Other Comprehensive Income for Scorpio Ltd, addressing adjustments required for gains on the sale of financial assets. Finally, it discusses the treatment of changes in the useful life and residual value of equipment, providing calculations for depreciation expenses and appropriate note disclosures for financial statements. The assignment uses references to specific AASB standards to support its analysis and conclusions.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.