Praemium Financial Statement Income Tax Analysis Assignment

VerifiedAdded on 2023/04/20

|12

|2970

|426

Homework Assignment

AI Summary

This assignment analyzes Praemium's income tax accounting based on its 2018 annual report. It examines the cash paid for income tax over two years, identifying the amounts and their locations within the financial statements. The analysis includes a comparison of income tax expenses, the reconciliation of tax expense with profit before tax, and a discussion of deferred tax assets and liabilities. The assignment explores the items that create these deferred taxes, distinguishing between assets and liabilities and assessing the closing balances. Furthermore, it compares and contrasts Praemium's income tax items with industry competitors, evaluating the effective income tax rate and potential tax benefits. The analysis also covers depreciation, intangible assets, shareholder equity, and changes in accounting policies, highlighting their relevance to the company's income tax position.

0PRAEMIUM TAX

PRAEMIUM TAX

Name of Student:

Name of University:

Author’s Name:

PRAEMIUM TAX

Name of Student:

Name of University:

Author’s Name:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1PRAEMIUM TAX

Table of Contents

Answers Part to Question 1.1:...................................................................................................2

Answer to Question Part 1.2:.....................................................................................................5

References:................................................................................................................................9

Table of Contents

Answers Part to Question 1.1:...................................................................................................2

Answer to Question Part 1.2:.....................................................................................................5

References:................................................................................................................................9

2PRAEMIUM TAX

Answers Part to Question 1.1:

The charges on income tax expense based on the profit of the company fetched in that year.

It is calculated based on tax rate, which was there on the reporting date. In the year 2018, the

company has paid $2,735,705 and in the year 2017, the company has paid $3,233,770. The

following information was provided in the 2018 annual report of Praemium from cash flow

statement. The company has paid this tax based on the profit fetched during the previous year.

The income tax expense for the company in the year 2018, $3,488,076 and in the year 2017, the

income tax expense for the company is $1,530,833 (www.praemium.com 2019).

The note can be found in the annual report of 2018 of the company where it is present in the

point (K) in which it is mentioned that the company charge income-tax expense based on the

profit for the year adjusted for any non-assessable or disallowed items. It is calculated using the

tax rates that have been enacted by the reporting date (Halbert 2016). It is similar to the income

tax paid in the cash flow statement which transaction is done in cash. It is also paid based on the

profit fetched by the company in the reporting year. The company has recognized the deferred

tax and deferred liabilities by utilizing the method of balance sheet liability with respect to the

rising differences between the tax basses assets and liabilities and the amount which is carried to

the financial statements and unused tax losses. No deferred tax assets or liabilities are recognized

from the assets and liabilities, which are recognized initially except the business combination.

The business combination does not affect the tax profit or loss statement or the accounting

profit or loss statement. The tax rate on which the deferred tax was calculated based on the rate,

which was present at that point of time. Defrred tax appears in the profit and loss statement of

the company. It also appears on the comprehensive statement of income. It does not appear

where it relates to the item, which relates to the equity. Defrred tax assets can be found out for

Answers Part to Question 1.1:

The charges on income tax expense based on the profit of the company fetched in that year.

It is calculated based on tax rate, which was there on the reporting date. In the year 2018, the

company has paid $2,735,705 and in the year 2017, the company has paid $3,233,770. The

following information was provided in the 2018 annual report of Praemium from cash flow

statement. The company has paid this tax based on the profit fetched during the previous year.

The income tax expense for the company in the year 2018, $3,488,076 and in the year 2017, the

income tax expense for the company is $1,530,833 (www.praemium.com 2019).

The note can be found in the annual report of 2018 of the company where it is present in the

point (K) in which it is mentioned that the company charge income-tax expense based on the

profit for the year adjusted for any non-assessable or disallowed items. It is calculated using the

tax rates that have been enacted by the reporting date (Halbert 2016). It is similar to the income

tax paid in the cash flow statement which transaction is done in cash. It is also paid based on the

profit fetched by the company in the reporting year. The company has recognized the deferred

tax and deferred liabilities by utilizing the method of balance sheet liability with respect to the

rising differences between the tax basses assets and liabilities and the amount which is carried to

the financial statements and unused tax losses. No deferred tax assets or liabilities are recognized

from the assets and liabilities, which are recognized initially except the business combination.

The business combination does not affect the tax profit or loss statement or the accounting

profit or loss statement. The tax rate on which the deferred tax was calculated based on the rate,

which was present at that point of time. Defrred tax appears in the profit and loss statement of

the company. It also appears on the comprehensive statement of income. It does not appear

where it relates to the item, which relates to the equity. Defrred tax assets can be found out for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3PRAEMIUM TAX

deductible temporary differences and tax losses, which are unused. It is only probable that future

taxable amount will be available to analyze the temporary differences and losses. Deferred tax

assets and liabilities are not analyzed when there is a difference between the carrying amounts

and tax basses of investment in the company por any kind of entity for which the deferred tax

will be calculated. This happened because when the parent entity able to control the timing of the

reversalof the temporary differences and it can be said that the differences will not be reversed in

future. Assets are the property or estate, which is hold by the company and it, has monetary value

associated with it.

On the other hand, liabilities are a debt, which the company owes from someone and needs to

pay to that entity in near future. Both assets and liabilities are the part of accounting equation

where it states that the assets are equal to liabilities plus owner’s capital. After analyzing the

financial statement of this company, it can be analyzed that the company has current assets of

$19,455,640 in the year 2018 and in the year of 2017, the company had total current assets of

$15,677,404. The company’s total current assets are $10,863,346 and $8,492,456 in 2018 and

2017 respectively (www.praemium.com 2019). The total assets of the company for the year of

2018 and 2017 are $30,318,986 and $24,170,060 respectively. In the case of fixed assets, the

straight line method is used for the depreciation purpose where the plant, furniture and

equipment depreciation rate is being taken 10-20% and computer equipment the depreciation rate

is 20-33% and deprecation rate on buildings and leasehold improvements is 15%.

In the case of intangible assets it is calculated the details taken in the consideration for the

calculation customer lists and databases acquired by the company and other intangible assets

namely goodwill are calculated using the fair value (Sacks,. et al 2015). Amortizations of the

non-financial assets are also realized. Goodwill is allocated based on cash generating units,

deductible temporary differences and tax losses, which are unused. It is only probable that future

taxable amount will be available to analyze the temporary differences and losses. Deferred tax

assets and liabilities are not analyzed when there is a difference between the carrying amounts

and tax basses of investment in the company por any kind of entity for which the deferred tax

will be calculated. This happened because when the parent entity able to control the timing of the

reversalof the temporary differences and it can be said that the differences will not be reversed in

future. Assets are the property or estate, which is hold by the company and it, has monetary value

associated with it.

On the other hand, liabilities are a debt, which the company owes from someone and needs to

pay to that entity in near future. Both assets and liabilities are the part of accounting equation

where it states that the assets are equal to liabilities plus owner’s capital. After analyzing the

financial statement of this company, it can be analyzed that the company has current assets of

$19,455,640 in the year 2018 and in the year of 2017, the company had total current assets of

$15,677,404. The company’s total current assets are $10,863,346 and $8,492,456 in 2018 and

2017 respectively (www.praemium.com 2019). The total assets of the company for the year of

2018 and 2017 are $30,318,986 and $24,170,060 respectively. In the case of fixed assets, the

straight line method is used for the depreciation purpose where the plant, furniture and

equipment depreciation rate is being taken 10-20% and computer equipment the depreciation rate

is 20-33% and deprecation rate on buildings and leasehold improvements is 15%.

In the case of intangible assets it is calculated the details taken in the consideration for the

calculation customer lists and databases acquired by the company and other intangible assets

namely goodwill are calculated using the fair value (Sacks,. et al 2015). Amortizations of the

non-financial assets are also realized. Goodwill is allocated based on cash generating units,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4PRAEMIUM TAX

which are hoped to be benefited from the synergies of the related business combination. The

group management fixes the goodwill coming from cash generating unit. On the other hand, the

company’s current liabilities are $9,776,614 and $67,719,961 of 2018 and 2017 respectively.

The company’s non-current liabilities are $262,429 and $356,842 in 2018 and 2017 respectively.

The total liabilities of the company in the year 2018 and 2017 are $10,039,043 and $7,076,803

respectively. The company has fetched profit both the year of 2018 and 2017 respectively. The

company has fetched more profit in the year 2018 than the year 2017. This means that the

company’s growth chart is on the upper slope and hence the slope is improving.

which are hoped to be benefited from the synergies of the related business combination. The

group management fixes the goodwill coming from cash generating unit. On the other hand, the

company’s current liabilities are $9,776,614 and $67,719,961 of 2018 and 2017 respectively.

The company’s non-current liabilities are $262,429 and $356,842 in 2018 and 2017 respectively.

The total liabilities of the company in the year 2018 and 2017 are $10,039,043 and $7,076,803

respectively. The company has fetched profit both the year of 2018 and 2017 respectively. The

company has fetched more profit in the year 2018 than the year 2017. This means that the

company’s growth chart is on the upper slope and hence the slope is improving.

5PRAEMIUM TAX

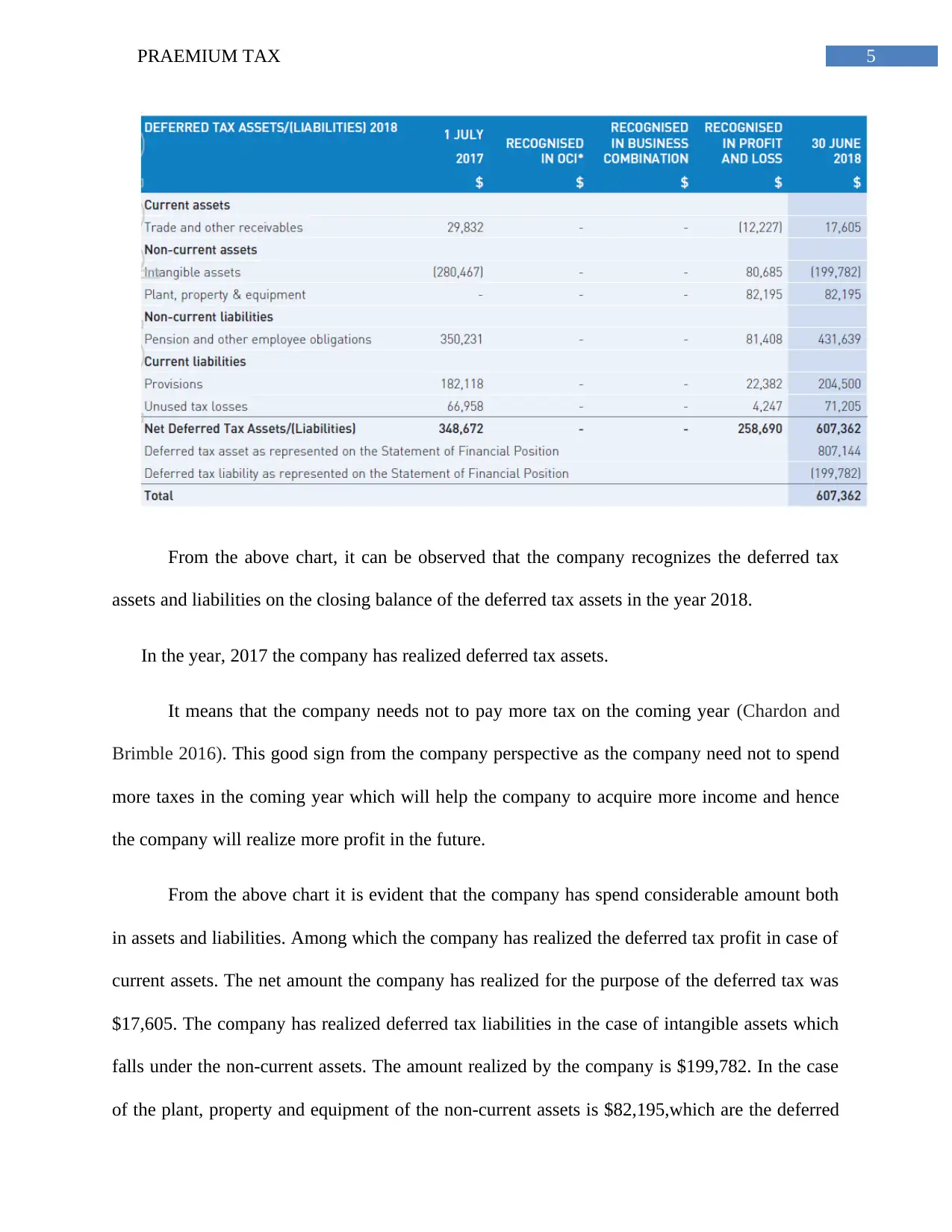

From the above chart, it can be observed that the company recognizes the deferred tax

assets and liabilities on the closing balance of the deferred tax assets in the year 2018.

In the year, 2017 the company has realized deferred tax assets.

It means that the company needs not to pay more tax on the coming year (Chardon and

Brimble 2016). This good sign from the company perspective as the company need not to spend

more taxes in the coming year which will help the company to acquire more income and hence

the company will realize more profit in the future.

From the above chart it is evident that the company has spend considerable amount both

in assets and liabilities. Among which the company has realized the deferred tax profit in case of

current assets. The net amount the company has realized for the purpose of the deferred tax was

$17,605. The company has realized deferred tax liabilities in the case of intangible assets which

falls under the non-current assets. The amount realized by the company is $199,782. In the case

of the plant, property and equipment of the non-current assets is $82,195,which are the deferred

From the above chart, it can be observed that the company recognizes the deferred tax

assets and liabilities on the closing balance of the deferred tax assets in the year 2018.

In the year, 2017 the company has realized deferred tax assets.

It means that the company needs not to pay more tax on the coming year (Chardon and

Brimble 2016). This good sign from the company perspective as the company need not to spend

more taxes in the coming year which will help the company to acquire more income and hence

the company will realize more profit in the future.

From the above chart it is evident that the company has spend considerable amount both

in assets and liabilities. Among which the company has realized the deferred tax profit in case of

current assets. The net amount the company has realized for the purpose of the deferred tax was

$17,605. The company has realized deferred tax liabilities in the case of intangible assets which

falls under the non-current assets. The amount realized by the company is $199,782. In the case

of the plant, property and equipment of the non-current assets is $82,195,which are the deferred

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6PRAEMIUM TAX

tax assets. In case of liabilities, the company has provided the deferred tax assets all throughout.

The carrying amount, which is being transferred to the next year, is $607,362. No, the carrying

amount is not greater than the previous year. The carrying amount in the year 2017, is

$1,435,292 and in the case of the the year 2018, the carrying amount is $607,362.

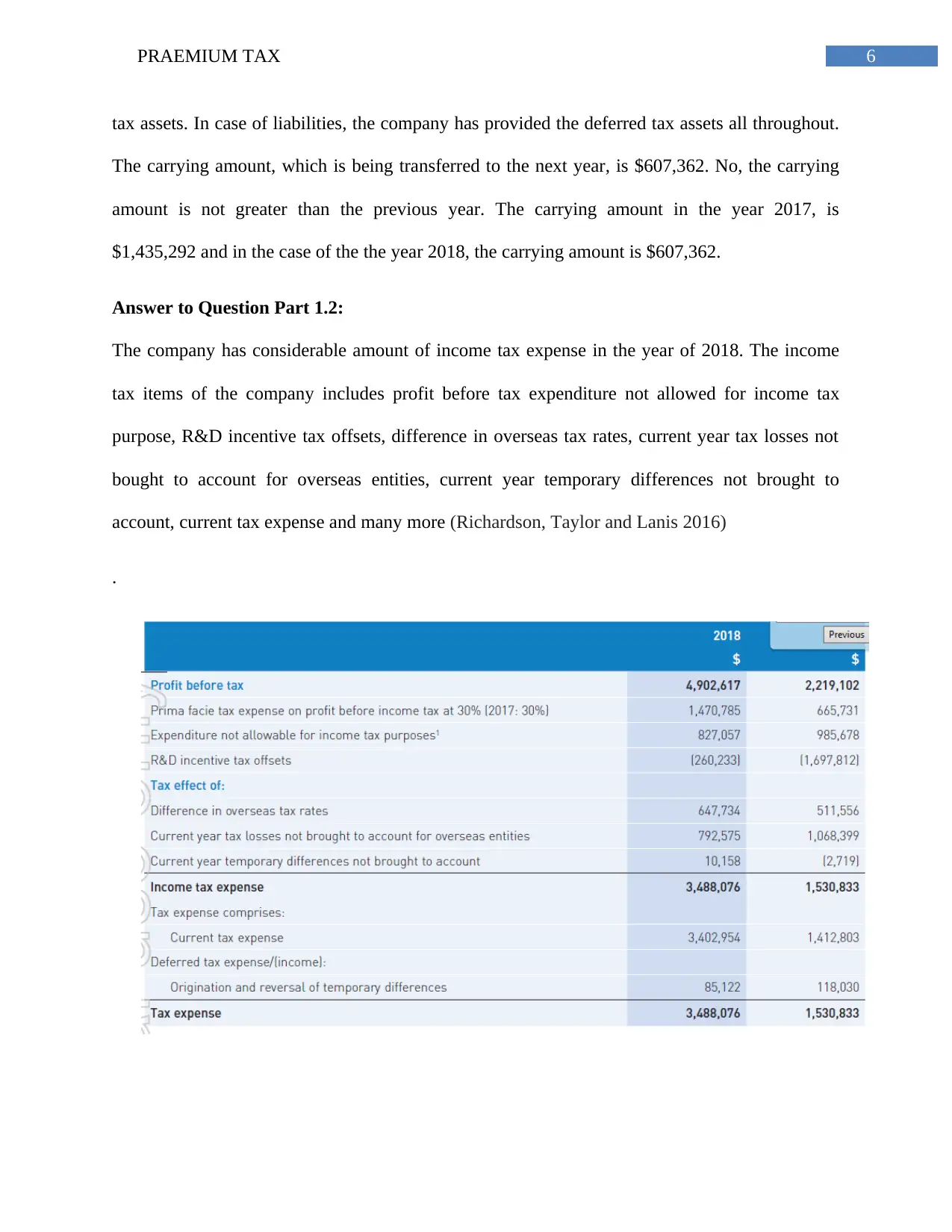

Answer to Question Part 1.2:

The company has considerable amount of income tax expense in the year of 2018. The income

tax items of the company includes profit before tax expenditure not allowed for income tax

purpose, R&D incentive tax offsets, difference in overseas tax rates, current year tax losses not

bought to account for overseas entities, current year temporary differences not brought to

account, current tax expense and many more (Richardson, Taylor and Lanis 2016)

.

tax assets. In case of liabilities, the company has provided the deferred tax assets all throughout.

The carrying amount, which is being transferred to the next year, is $607,362. No, the carrying

amount is not greater than the previous year. The carrying amount in the year 2017, is

$1,435,292 and in the case of the the year 2018, the carrying amount is $607,362.

Answer to Question Part 1.2:

The company has considerable amount of income tax expense in the year of 2018. The income

tax items of the company includes profit before tax expenditure not allowed for income tax

purpose, R&D incentive tax offsets, difference in overseas tax rates, current year tax losses not

bought to account for overseas entities, current year temporary differences not brought to

account, current tax expense and many more (Richardson, Taylor and Lanis 2016)

.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7PRAEMIUM TAX

From the above chart, it is evident that the difference between the income tax expense

differences is big. In the case of deferred tax assets and liabilities it is seen that in the year 2017

the company has incurred less deferred tax than the year in 2018. The basic difference among the

two year is $1,957,243. It is evident that the income tax expense has increased to a considerable

height in comparison to the previous year of the company (Bauman and Shaw 2016). The

potential tax benefit for the company in 2018 is $17,006,724, which is much more in comparison

to the last year.However, the company holds a considerable amount of market share in the

industry.

The company is also one of the market competitor in the company. The main competitor of

the company in the industry is HUB 24, Locums Group and Prime. These three are the top

competitor for the company in the market. Among these three prime is termed to be the biggest

rival of this company. It is a multinational firm and has more employees than than the Praemium.

HUB 24 is also one of the largest competitors of Praemium (Tran 2015). The company’s revenue

$52m more than the Praemium. The effective tax rate for the Praemium Company is 30% in the

year 2018. This is the tax rate used by the company for analyzing the potential tax benefit of the

company. According to the annual report of the company of 2018 the company’s potential tax

benefit of the company in the year 2018 is $17,006,284 and in the year 2017, the potential tax

benefit is $9,832,495. From the above mentioned number it is evident that the company has more

potential tax benefit in the year 2018 than in the year 2017.

The deferred assets tax as a percentage of total assets is as follows:

Total Defeffred Tax Assets

Total Assets ∗100 %

= $807,144/30,318,986 * 100% = 2.67% (approx.)

From the above chart, it is evident that the difference between the income tax expense

differences is big. In the case of deferred tax assets and liabilities it is seen that in the year 2017

the company has incurred less deferred tax than the year in 2018. The basic difference among the

two year is $1,957,243. It is evident that the income tax expense has increased to a considerable

height in comparison to the previous year of the company (Bauman and Shaw 2016). The

potential tax benefit for the company in 2018 is $17,006,724, which is much more in comparison

to the last year.However, the company holds a considerable amount of market share in the

industry.

The company is also one of the market competitor in the company. The main competitor of

the company in the industry is HUB 24, Locums Group and Prime. These three are the top

competitor for the company in the market. Among these three prime is termed to be the biggest

rival of this company. It is a multinational firm and has more employees than than the Praemium.

HUB 24 is also one of the largest competitors of Praemium (Tran 2015). The company’s revenue

$52m more than the Praemium. The effective tax rate for the Praemium Company is 30% in the

year 2018. This is the tax rate used by the company for analyzing the potential tax benefit of the

company. According to the annual report of the company of 2018 the company’s potential tax

benefit of the company in the year 2018 is $17,006,284 and in the year 2017, the potential tax

benefit is $9,832,495. From the above mentioned number it is evident that the company has more

potential tax benefit in the year 2018 than in the year 2017.

The deferred assets tax as a percentage of total assets is as follows:

Total Defeffred Tax Assets

Total Assets ∗100 %

= $807,144/30,318,986 * 100% = 2.67% (approx.)

8PRAEMIUM TAX

The deferred tax liabilities as a percentage of Total Liabilities are as follows:

Total Deferred Tax Liabilities

Total Liabilities ∗100 %

= $199782/10039043*100% = 2.00% (approx.)

The information that is relevant to the analysis of the company’s accounting for income tax

are as follows:

Depreciation: The Company has shown some depreciation in many of its fixed assets. It is

observed from the financial report of the company of 2018 that the company has taken

depreciation in capitalised lease assets, which are depreciated using the straight-line method.

Leasehold improvement of the company is depreciated over the shorter period or the unexpired

period of the lease of the estimated useful lives of improvement (Libby 2017). The depreciated

amount carrying value of the asset less estimated residual amount. The residual amount, which

comes out based on the expected lives of the similar kind of the asset at the end of the period,

which could be sold for (Burkhauser, Hahn and Wilkins 2015). It can be safely say that the

beside the other unit of the income tax depreciation is also one of the most important factor

which is relevant to the companies’ income tax.

Intangible Assets: Intangible assets are also one of the major parts of the company’s balance

sheet and other financial statement. Intangible assets include goodwill, intellectual property, and

more (Sánchez-Segura, Ruiz-Robles and Medina-Dominguez 2016). Goodwill of the company is

one of the most important factor of the company which not only helps the company to create a

brand reputation in the market but it also attracts new customers, new stakeholders and new

investors for the company (Thum-Thysen, et al. 2017). Intellectual property is a very broad term

which states that the company’s one of the valuable assets are brand identity, trained employees,

The deferred tax liabilities as a percentage of Total Liabilities are as follows:

Total Deferred Tax Liabilities

Total Liabilities ∗100 %

= $199782/10039043*100% = 2.00% (approx.)

The information that is relevant to the analysis of the company’s accounting for income tax

are as follows:

Depreciation: The Company has shown some depreciation in many of its fixed assets. It is

observed from the financial report of the company of 2018 that the company has taken

depreciation in capitalised lease assets, which are depreciated using the straight-line method.

Leasehold improvement of the company is depreciated over the shorter period or the unexpired

period of the lease of the estimated useful lives of improvement (Libby 2017). The depreciated

amount carrying value of the asset less estimated residual amount. The residual amount, which

comes out based on the expected lives of the similar kind of the asset at the end of the period,

which could be sold for (Burkhauser, Hahn and Wilkins 2015). It can be safely say that the

beside the other unit of the income tax depreciation is also one of the most important factor

which is relevant to the companies’ income tax.

Intangible Assets: Intangible assets are also one of the major parts of the company’s balance

sheet and other financial statement. Intangible assets include goodwill, intellectual property, and

more (Sánchez-Segura, Ruiz-Robles and Medina-Dominguez 2016). Goodwill of the company is

one of the most important factor of the company which not only helps the company to create a

brand reputation in the market but it also attracts new customers, new stakeholders and new

investors for the company (Thum-Thysen, et al. 2017). Intellectual property is a very broad term

which states that the company’s one of the valuable assets are brand identity, trained employees,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9PRAEMIUM TAX

customer loyalty and many more (Francis, et al 2015). This does affect the company’s growth

for a single year. This is the reason behind the importance of the company’s effort for increasing

the part. This also holds the same importance like the analysis of the income tax in the annual

report of the company.

Shareholder Equity: Shareholder equity is one of the major part of any company’s growth. The

involvement of the shareholder will help the company to grow or expand in the future by

utilising the amount gained by the company from the market or from the stakeholders (Kaura and

Gharma, 2015). Any important decision regarding expanding or diversification the stakeholders

are called because they are the owner of the company of the percentage of share they hold (Vegh

and Vuletin 2015). Therefore, it is very important to make the shareholder equity to analyse from

the annual report of the company beside the income tax of the company.

Change in accounting policies: Another important factor for the company is changing in

accounting policies. According to the recent change in the accounting policies of Australia leads

to change the way the accounting is done and every company who doing their business inside the

boundary of the Australian land and irrespective of their industry, the company needs to follow

the rules and regulations of the new accounting policies which are implanted in the country

(Daly et al 2015). From the above explanation it is clearly be seen that the change in accounting

policies is one of the major reasons besides analysing income tax of the company from the

annual report of the company.

customer loyalty and many more (Francis, et al 2015). This does affect the company’s growth

for a single year. This is the reason behind the importance of the company’s effort for increasing

the part. This also holds the same importance like the analysis of the income tax in the annual

report of the company.

Shareholder Equity: Shareholder equity is one of the major part of any company’s growth. The

involvement of the shareholder will help the company to grow or expand in the future by

utilising the amount gained by the company from the market or from the stakeholders (Kaura and

Gharma, 2015). Any important decision regarding expanding or diversification the stakeholders

are called because they are the owner of the company of the percentage of share they hold (Vegh

and Vuletin 2015). Therefore, it is very important to make the shareholder equity to analyse from

the annual report of the company beside the income tax of the company.

Change in accounting policies: Another important factor for the company is changing in

accounting policies. According to the recent change in the accounting policies of Australia leads

to change the way the accounting is done and every company who doing their business inside the

boundary of the Australian land and irrespective of their industry, the company needs to follow

the rules and regulations of the new accounting policies which are implanted in the country

(Daly et al 2015). From the above explanation it is clearly be seen that the change in accounting

policies is one of the major reasons besides analysing income tax of the company from the

annual report of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10PRAEMIUM TAX

References:

Bauman, M.P. and Shaw, K.W., 2016. Balance sheet classification and the valuation of deferred

taxes. Research in Accounting Regulation, 28(2), pp.77-85.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), pp.181-205

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

Daly, A., Hoy, S., Hughes, M., Islam, J. and Mak, A.S., 2015. Using group work to develop

intercultural skills in the accounting curriculum in Australia. Accounting Education, 24(1),

pp.27-40.

Francis, B., Hasan, I., Park, J.C. and Wu, Q., 2015. Gender differences in financial reporting

decision making: Evidence from accounting conservatism. Contemporary Accounting

Research, 32(3), pp.1285-1318.

Halbert, D., 2016. Intellectual property theft and national security: Agendas and

assumptions. The Information Society, 32(4), pp.256-268.

Kaura, V., Durga Prasad, C.S. and Sharma, S., 2015. Service quality, service convenience, price

and fairness, customer loyalty, and the mediating role of customer satisfaction. International

Journal of Bank Marketing, 33(4), pp.404-422.

Libby, R., 2017. Accounting and human information processing. In The Routledge Companion to

Behavioural Accounting Research (pp. 42-54). Routledge.

References:

Bauman, M.P. and Shaw, K.W., 2016. Balance sheet classification and the valuation of deferred

taxes. Research in Accounting Regulation, 28(2), pp.77-85.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), pp.181-205

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

Daly, A., Hoy, S., Hughes, M., Islam, J. and Mak, A.S., 2015. Using group work to develop

intercultural skills in the accounting curriculum in Australia. Accounting Education, 24(1),

pp.27-40.

Francis, B., Hasan, I., Park, J.C. and Wu, Q., 2015. Gender differences in financial reporting

decision making: Evidence from accounting conservatism. Contemporary Accounting

Research, 32(3), pp.1285-1318.

Halbert, D., 2016. Intellectual property theft and national security: Agendas and

assumptions. The Information Society, 32(4), pp.256-268.

Kaura, V., Durga Prasad, C.S. and Sharma, S., 2015. Service quality, service convenience, price

and fairness, customer loyalty, and the mediating role of customer satisfaction. International

Journal of Bank Marketing, 33(4), pp.404-422.

Libby, R., 2017. Accounting and human information processing. In The Routledge Companion to

Behavioural Accounting Research (pp. 42-54). Routledge.

11PRAEMIUM TAX

Richardson, G., Taylor, G. and Lanis, R., 2016. Women on the board of directors and corporate

tax aggressiveness in Australia: An empirical analysis. Accounting Research Journal, 29(3),

pp.313-331.

Sacks, G., Mialon, M., Vandevijvere, S., Trevena, H., Snowdon, W., Crino, M. and Swinburn,

B., 2015. Comparison of food industry policies and commitments on marketing to children and

product (re) formulation in Australia, New Zealand and Fiji. Critical public health, 25(3),

pp.299-319.

Sánchez-Segura, M.I., Ruiz-Robles, A. and Medina-Dominguez, F., 2016. Uncovering hidden

process assets: A case study. Information Systems Frontiers, 18(6), pp.1041-1049.

Thum-Thysen, A., Voigt, P., Maier, C., Bilbao-Osorio, B. and Ognyanova, D., 2017. Unlocking

investment in intangible assets in Europe. Quarterly Report on the Euro Area (QREA), 16(1),

pp.23-35.

Tran, A., 2015. Can taxable income be estimated from financial reports of listed companies in

Australia. Austl. Tax F., 30, p.569.

Vegh, C.A. and Vuletin, G., 2015. How is tax policy conducted over the business

cycle?. American Economic Journal: Economic Policy, 7(3), pp.327-70.

www.praemium.com (2019). Financial reports. [online] www.praemium.com. Available at:

https://www.praemium.com/intl/about-us/shareholders/financial-reports/ [Accessed 9 May

2019].

Richardson, G., Taylor, G. and Lanis, R., 2016. Women on the board of directors and corporate

tax aggressiveness in Australia: An empirical analysis. Accounting Research Journal, 29(3),

pp.313-331.

Sacks, G., Mialon, M., Vandevijvere, S., Trevena, H., Snowdon, W., Crino, M. and Swinburn,

B., 2015. Comparison of food industry policies and commitments on marketing to children and

product (re) formulation in Australia, New Zealand and Fiji. Critical public health, 25(3),

pp.299-319.

Sánchez-Segura, M.I., Ruiz-Robles, A. and Medina-Dominguez, F., 2016. Uncovering hidden

process assets: A case study. Information Systems Frontiers, 18(6), pp.1041-1049.

Thum-Thysen, A., Voigt, P., Maier, C., Bilbao-Osorio, B. and Ognyanova, D., 2017. Unlocking

investment in intangible assets in Europe. Quarterly Report on the Euro Area (QREA), 16(1),

pp.23-35.

Tran, A., 2015. Can taxable income be estimated from financial reports of listed companies in

Australia. Austl. Tax F., 30, p.569.

Vegh, C.A. and Vuletin, G., 2015. How is tax policy conducted over the business

cycle?. American Economic Journal: Economic Policy, 7(3), pp.327-70.

www.praemium.com (2019). Financial reports. [online] www.praemium.com. Available at:

https://www.praemium.com/intl/about-us/shareholders/financial-reports/ [Accessed 9 May

2019].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.