Predicting Apple Stock Prices Using Sentiment and Technical Analysis

VerifiedAdded on 2022/12/23

|13

|1598

|1

Project

AI Summary

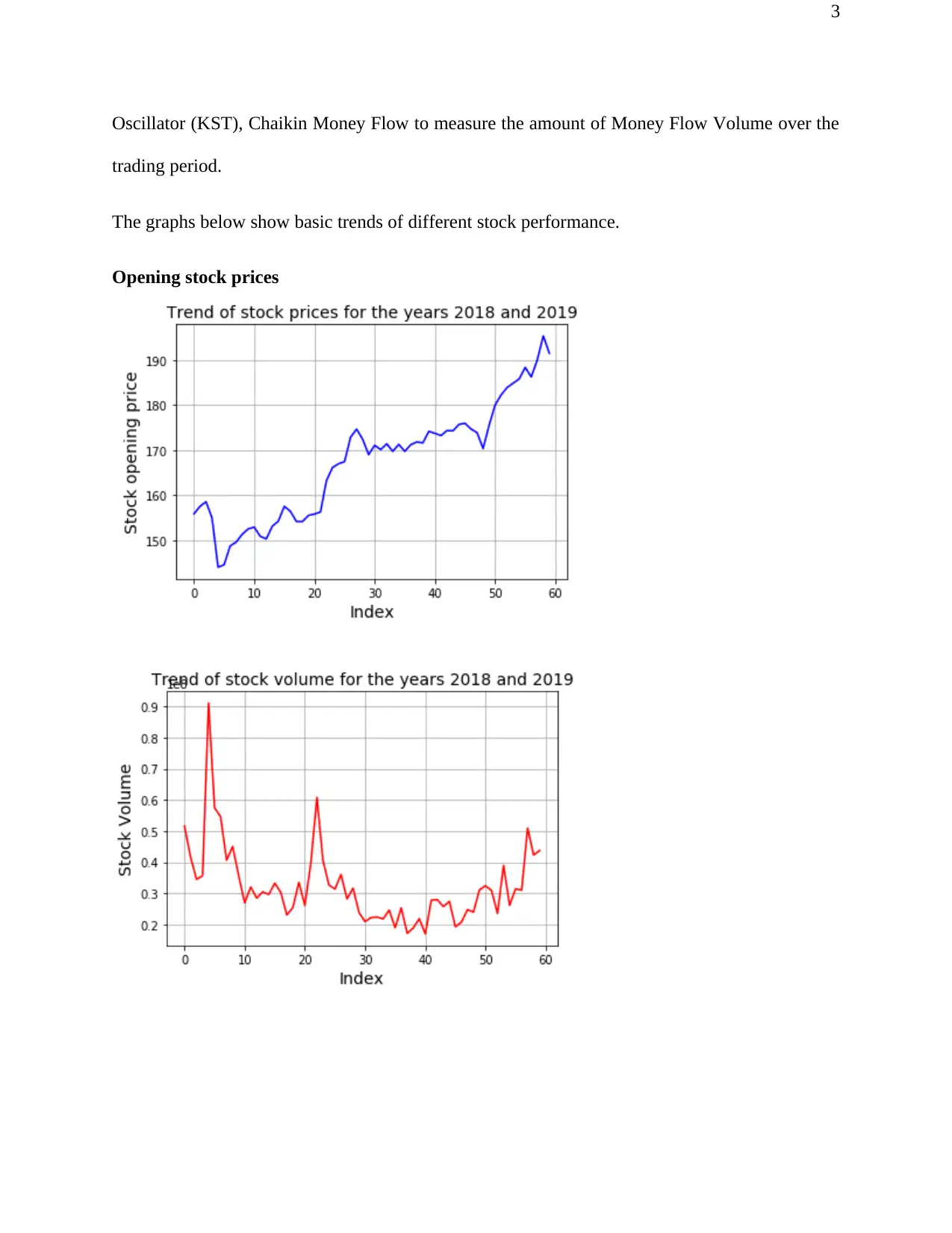

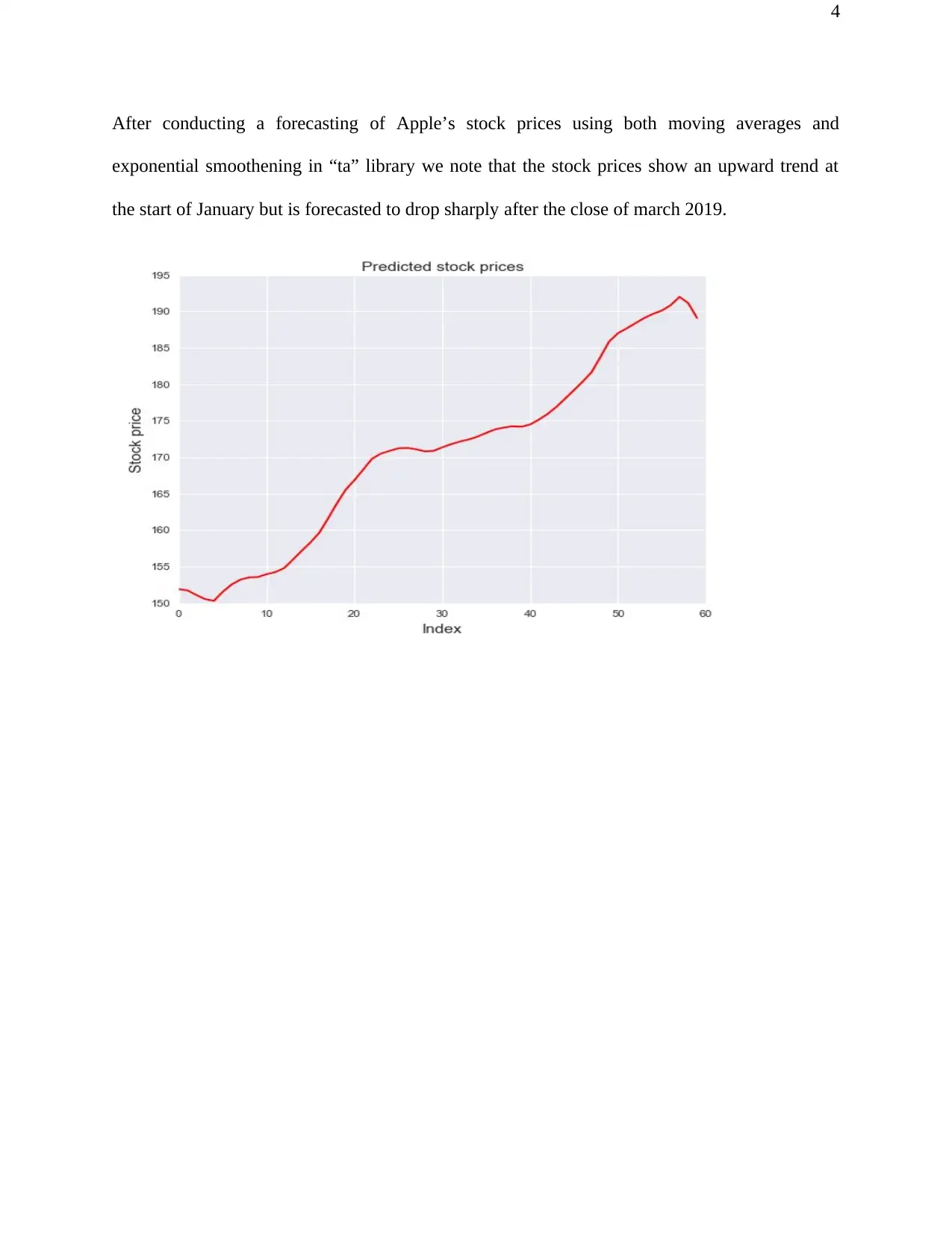

This project undertakes a comprehensive analysis of Apple's stock prices, leveraging both technical and sentiment data. The study begins by scraping and analyzing tweets related to Apple to gauge public sentiment, which is then correlated with technical indicators such as moving averages, exponential smoothing, and money flow indices. The analysis focuses on the 2018-2019 period. Forecasting methods like technical analysis algorithms and OLS regression are employed to predict stock prices. The findings reveal a weak positive correlation between polarity and sentiment with stock prices. Moreover, the sentiment variable demonstrates statistical significance in predicting stock prices. The project also examines the impact of cumulative and daily returns, concluding that cumulative returns, rather than daily returns, are a key factor in influencing stock prices. Overall, the project provides insights into how sentiment and technical indicators can be used to predict stock movements, and highlights the importance of cumulative returns in stock price analysis.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.