Report: Predicting Share Prices of Colgate Palmolive Using Regression

VerifiedAdded on 2021/06/15

|13

|2122

|340

Report

AI Summary

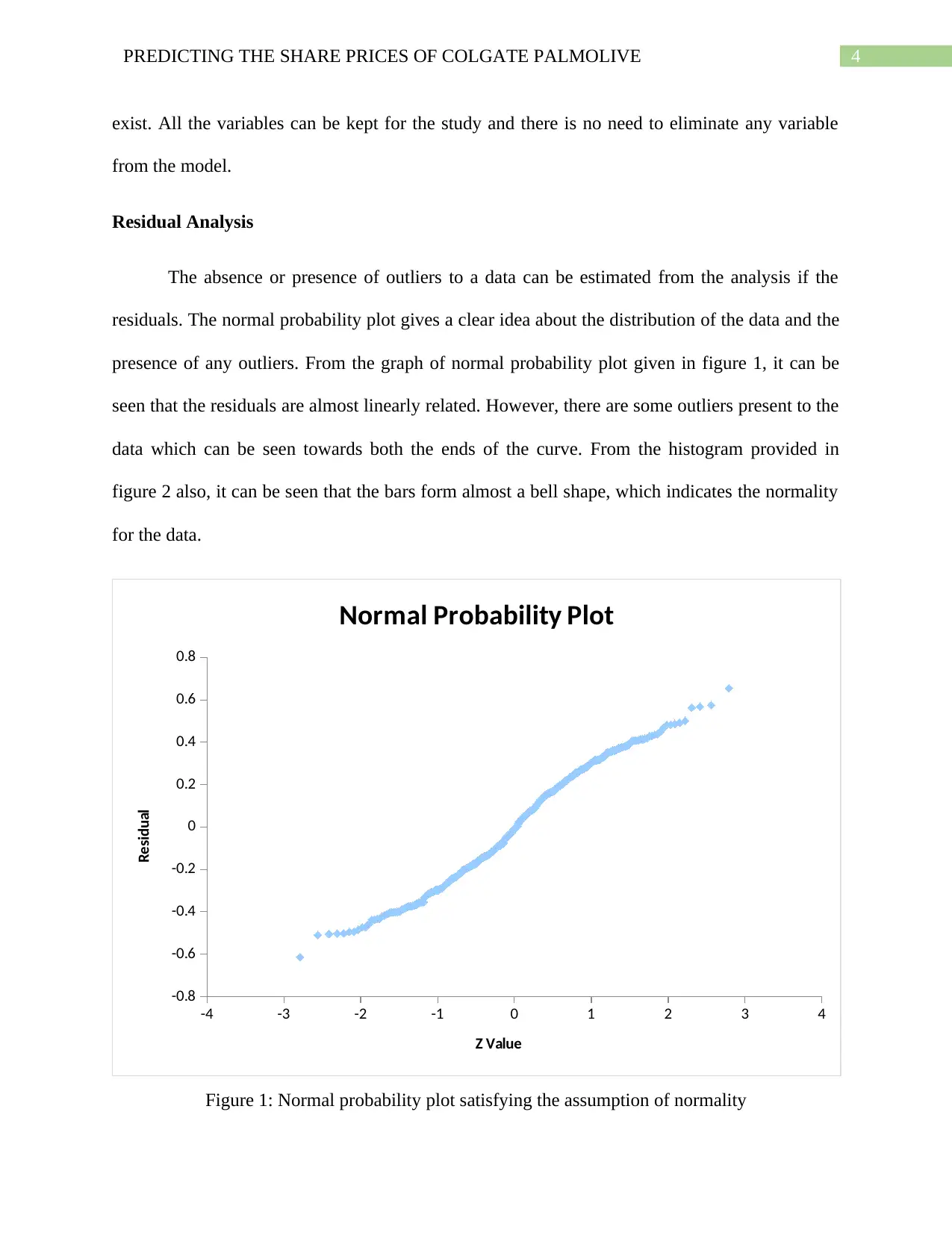

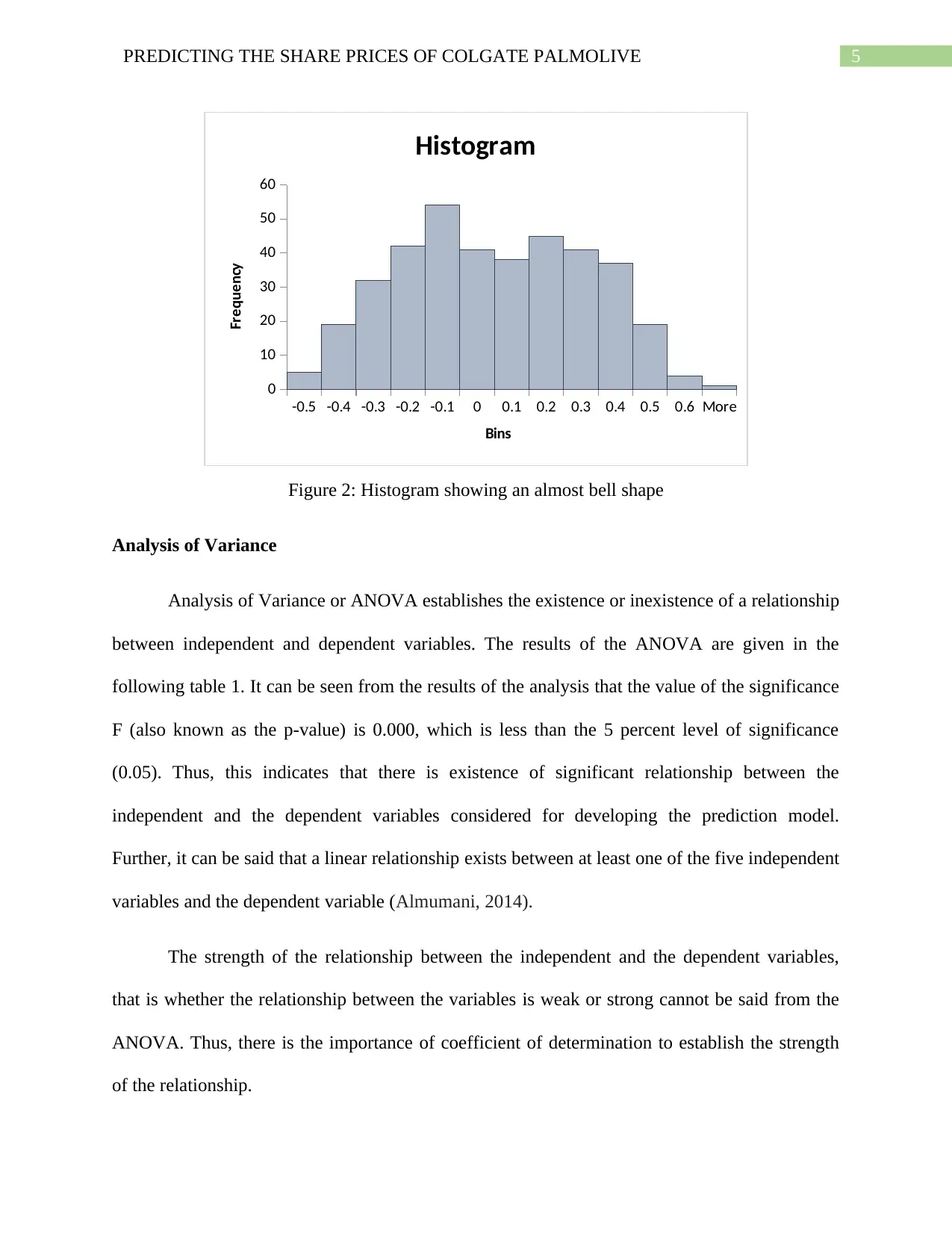

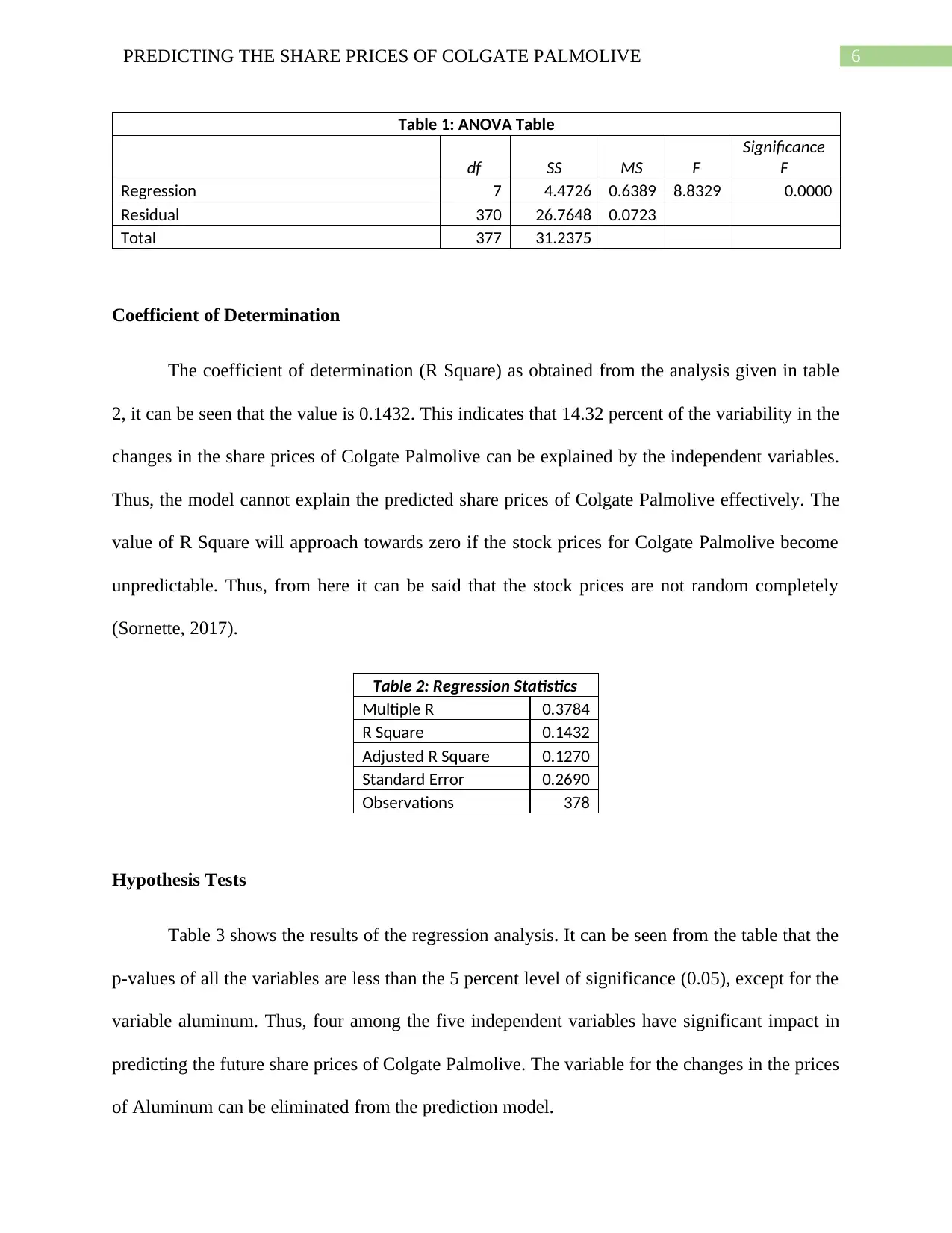

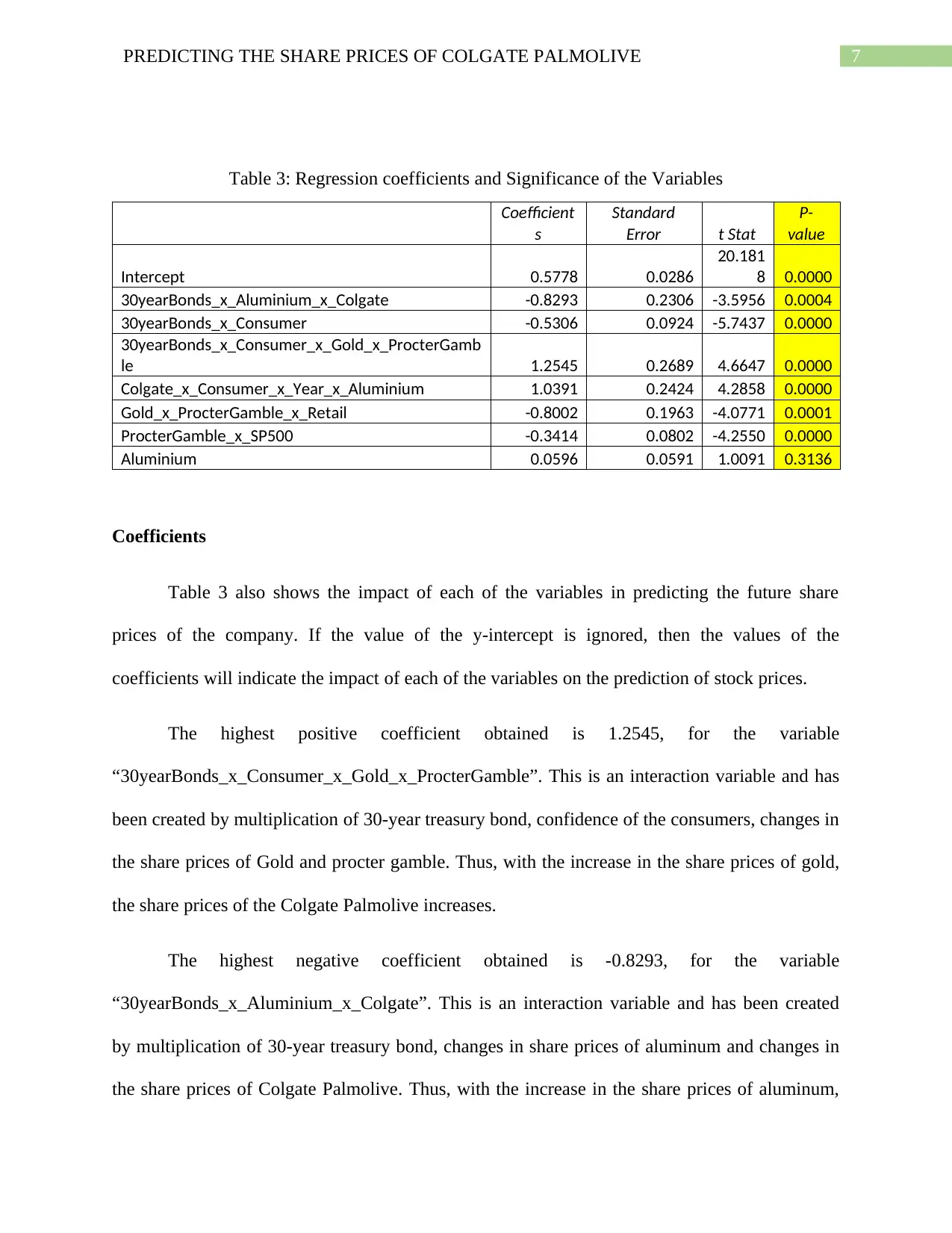

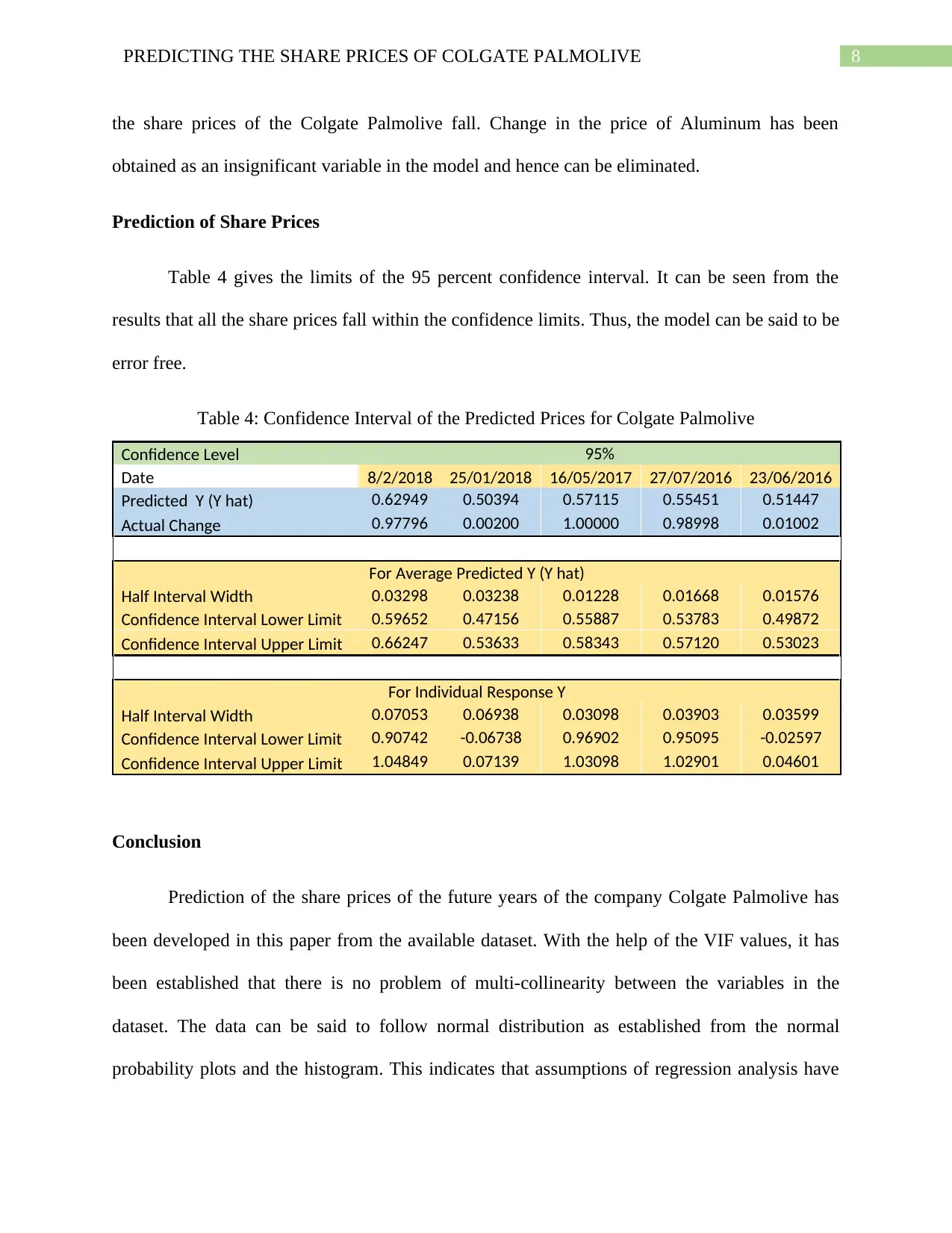

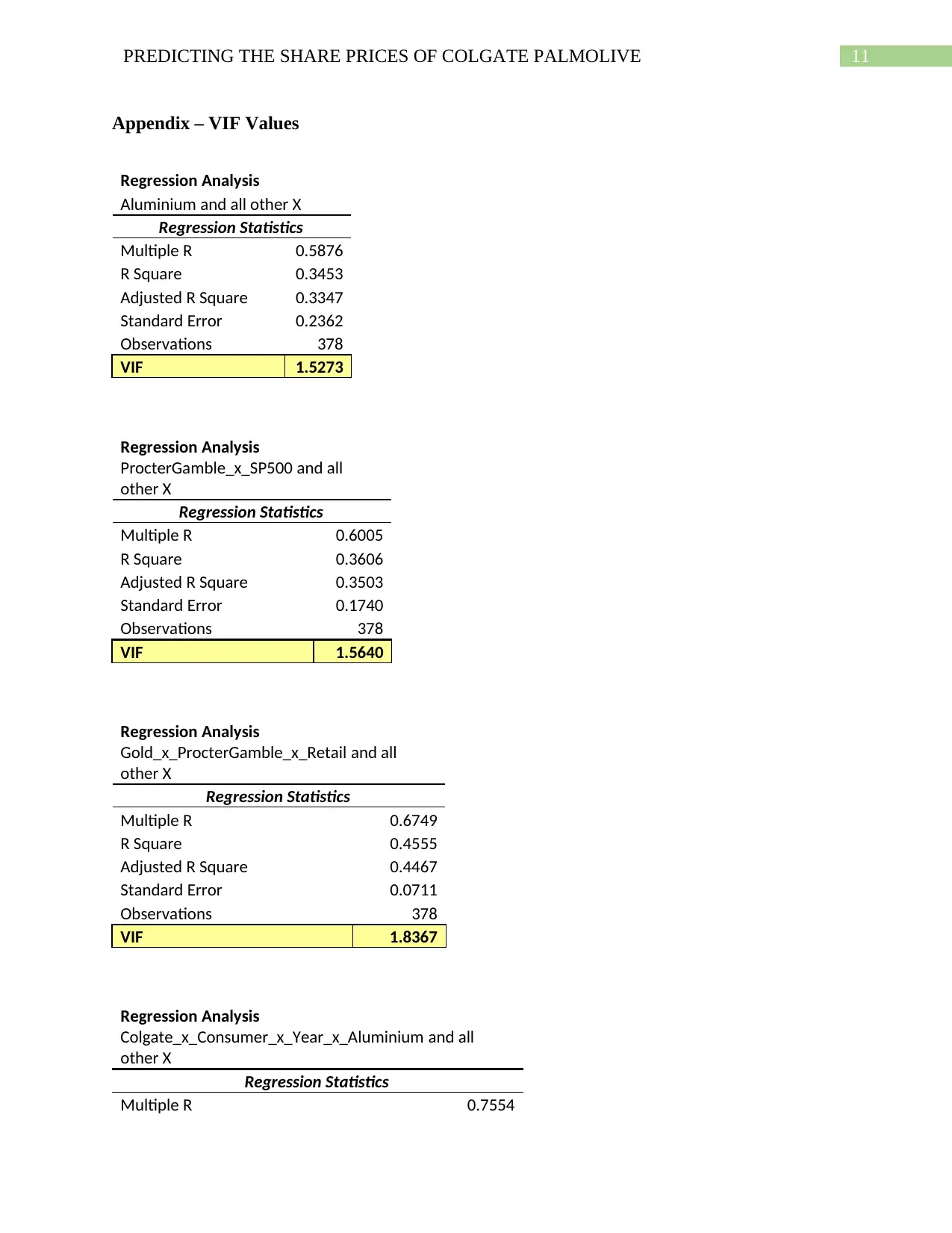

This report provides a detailed analysis aimed at predicting the future share prices of Colgate Palmolive. The analysis is conducted using stock market data from April 2016 to March 2018, encompassing 378 trading days. The study employs a multiple regression model to establish relationships between changes in share prices and various independent factors, including the prices of assets like aluminum and gold, consumer confidence, interest rates, and the S&P 500 index. The report assesses the presence of multicollinearity using the Variance Inflation Factor (VIF) and evaluates the significance of the independent variables through Analysis of Variance (ANOVA). It also discusses the coefficient of determination (R-squared) to gauge the model's explanatory power. The findings suggest that the model can explain 14.32 percent of the variability in Colgate Palmolive's share prices. The study also includes a residual analysis and hypothesis tests to validate the model's assumptions and identify significant variables, with the aluminum variable being found insignificant. The predicted share prices fall within the confidence limits. The report concludes that the model offers some predictive capability, while acknowledging the limitations of the R-squared value.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.