Managerial Accounting Report: Pref Homes Profitability Analysis

VerifiedAdded on 2023/06/04

|4

|581

|187

Report

AI Summary

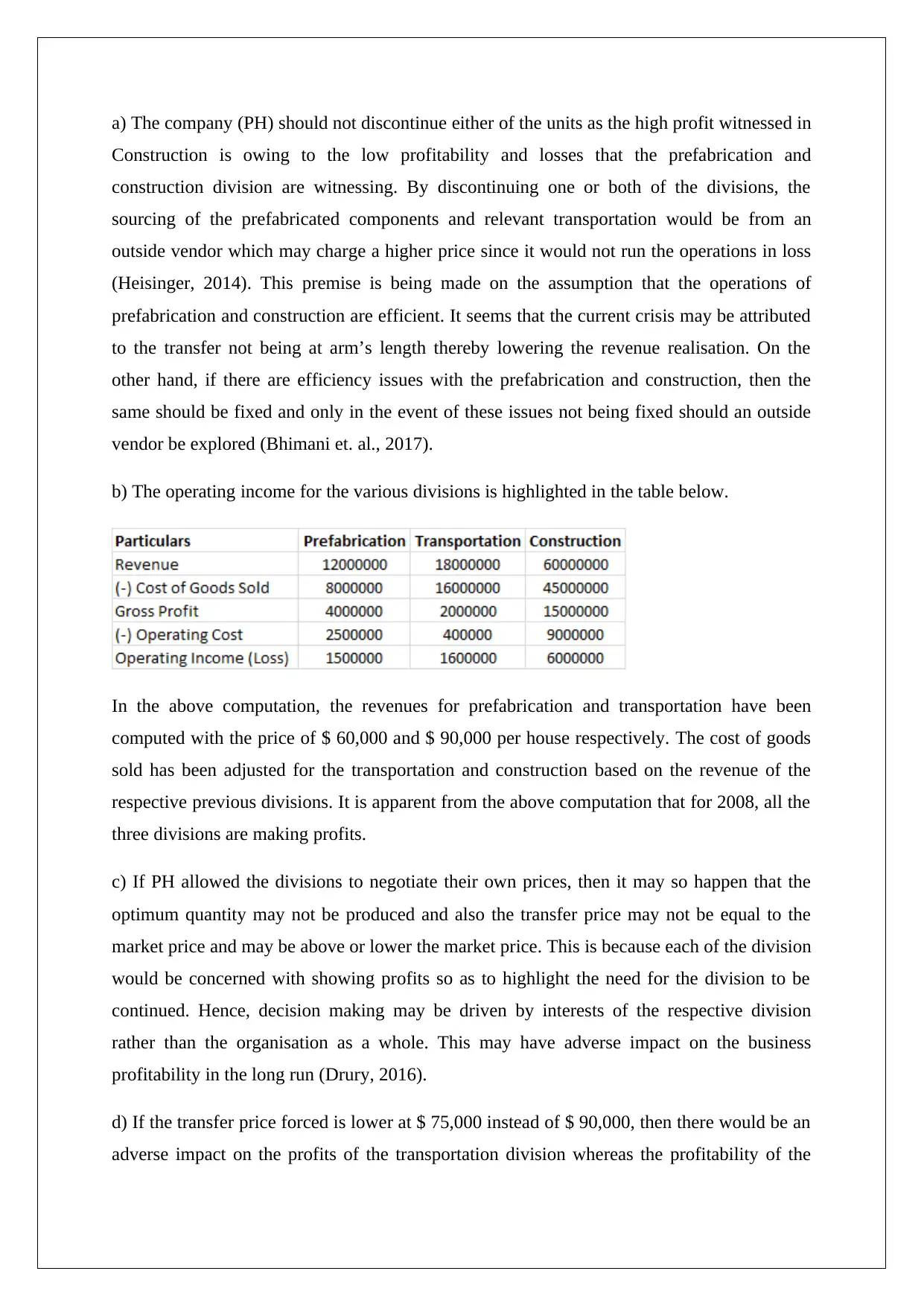

This report analyzes the managerial accounting case of Preferential Homes (PH), a residential home builder with three divisions: prefabrication, transportation, and construction. The analysis addresses the potential discontinuation of the prefabrication and transportation divisions, concluding that neither should be discontinued due to the potential cost implications of outsourcing components. The report includes calculations of operating income for each division, demonstrating profitability across all three in 2008. Furthermore, the report explores the impact of allowing divisions to negotiate their own prices, highlighting the risk of decisions being driven by divisional rather than organizational interests, and the consequences of a forced lower transfer price, which would adversely affect the transportation division's profits and potentially reduce construction output. References to relevant accounting literature are provided to support the analysis.

1 out of 4

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.