CASS International College: Management Accounting Information Report

VerifiedAdded on 2022/10/19

|14

|1969

|12

Report

AI Summary

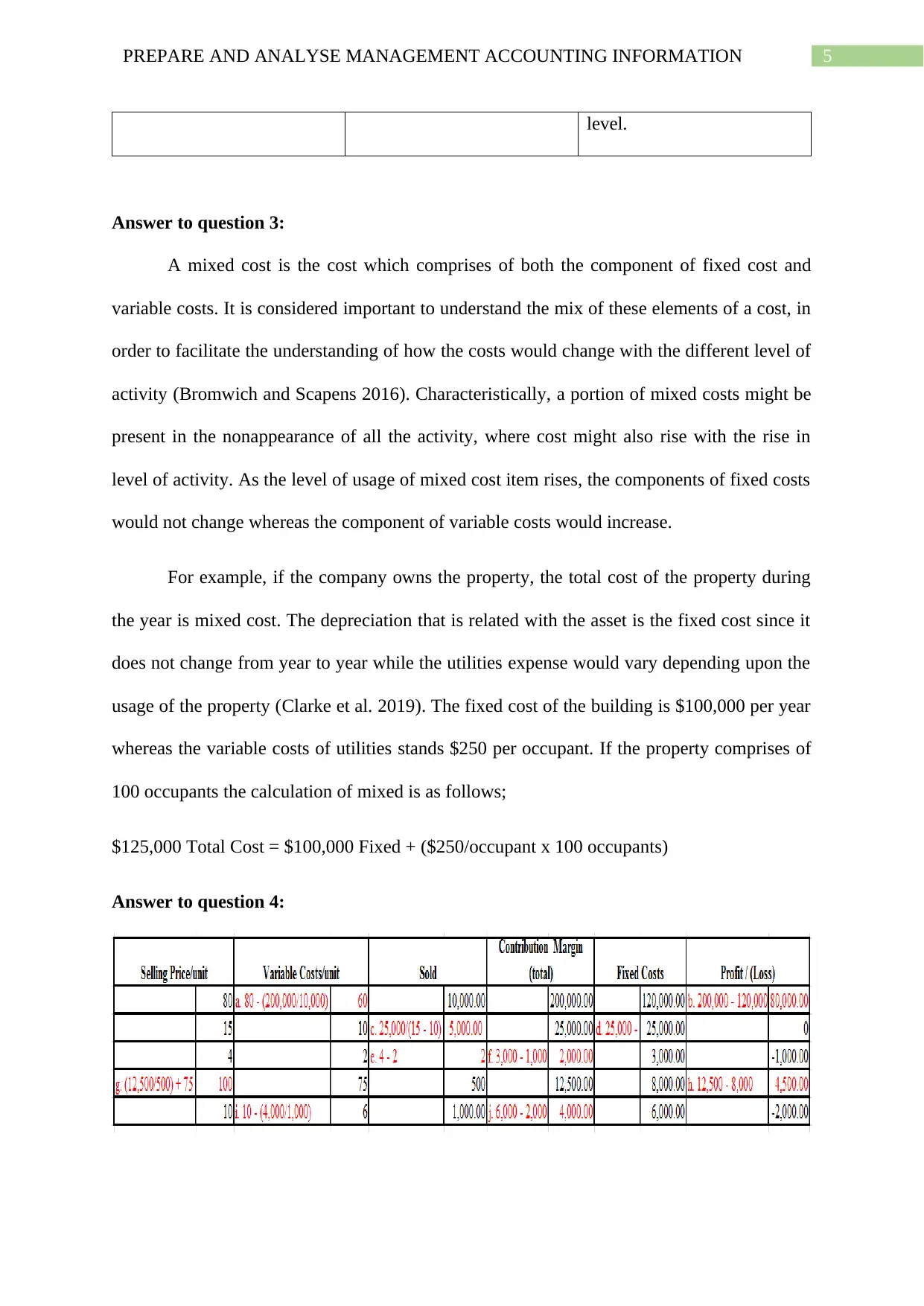

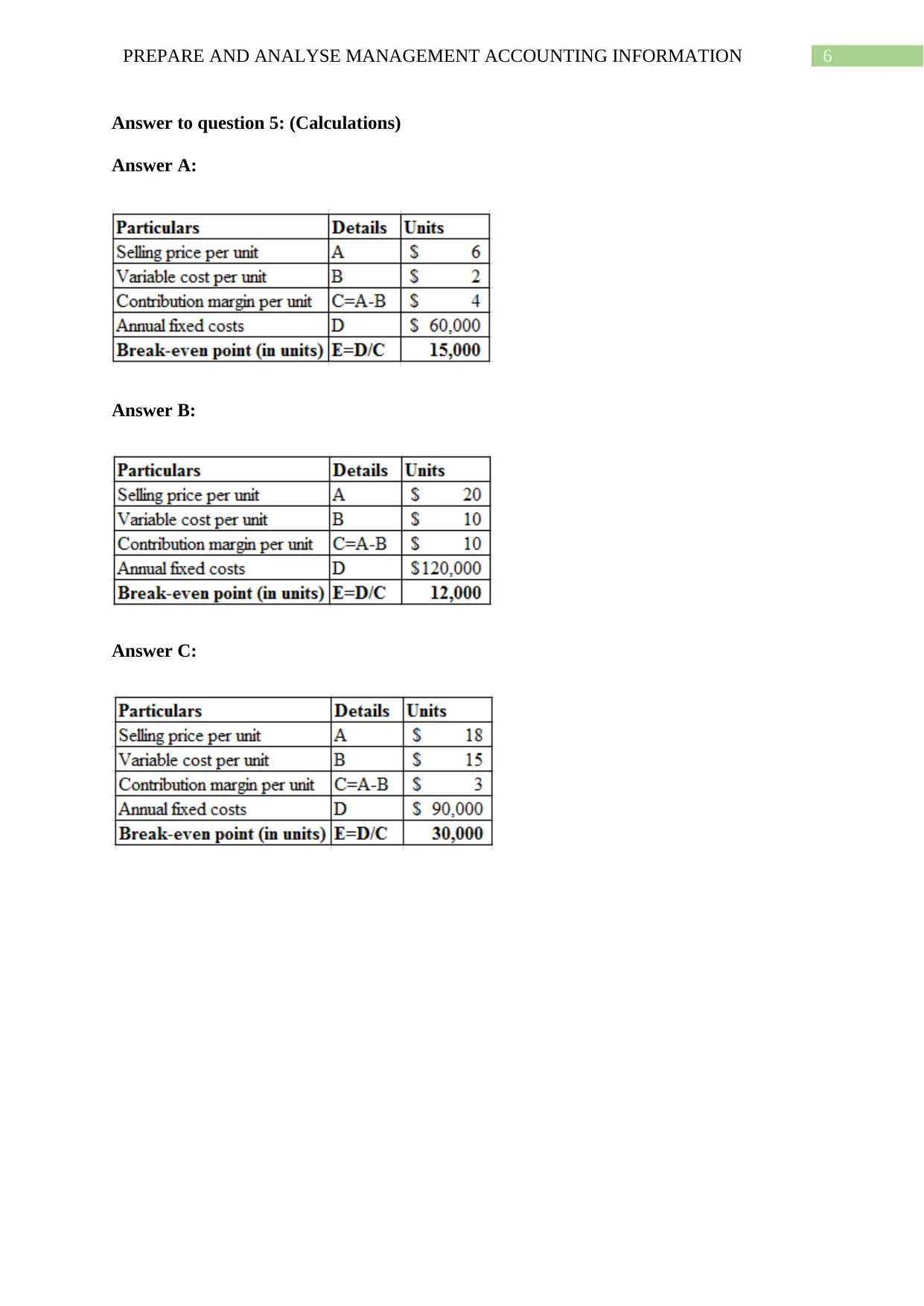

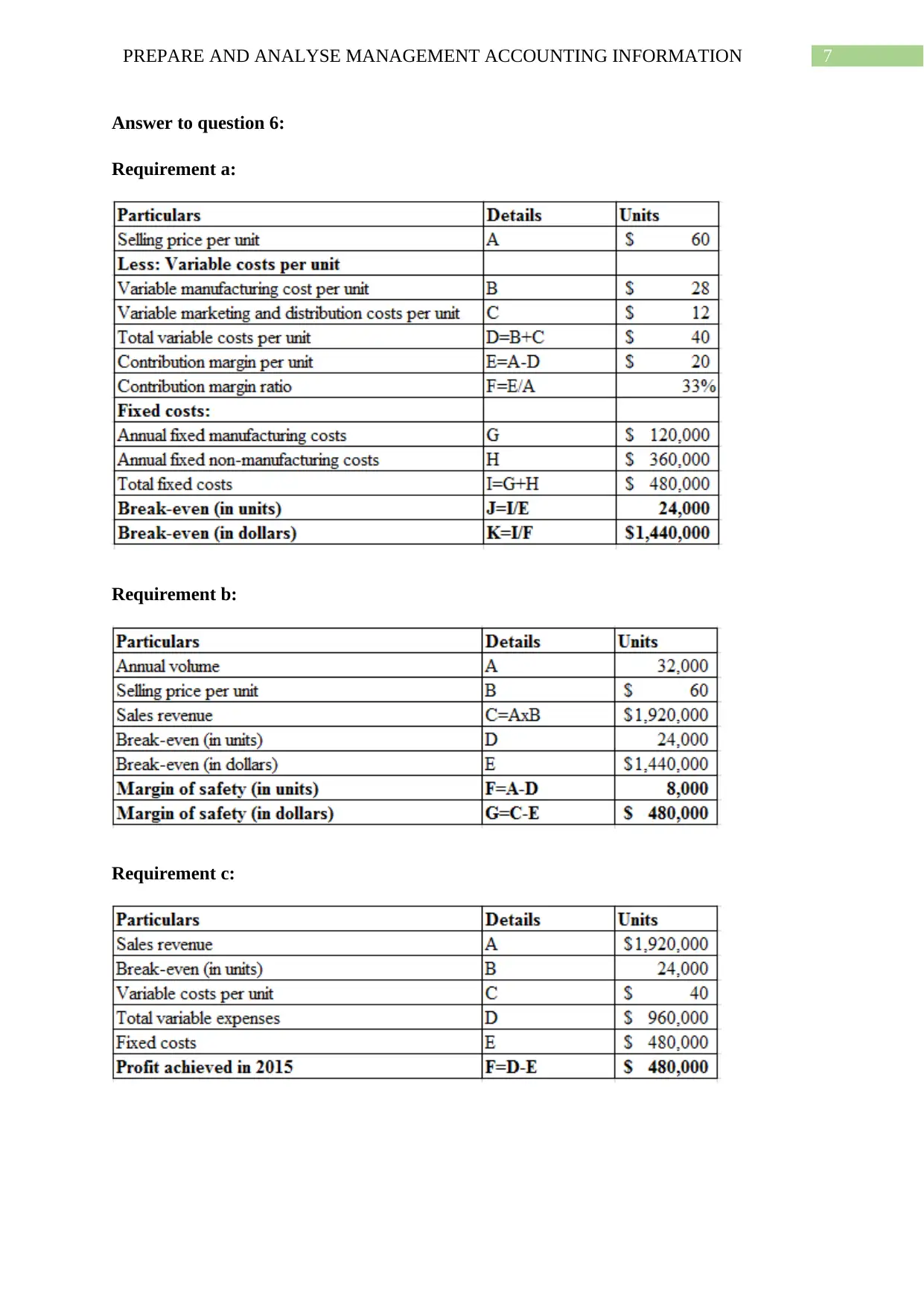

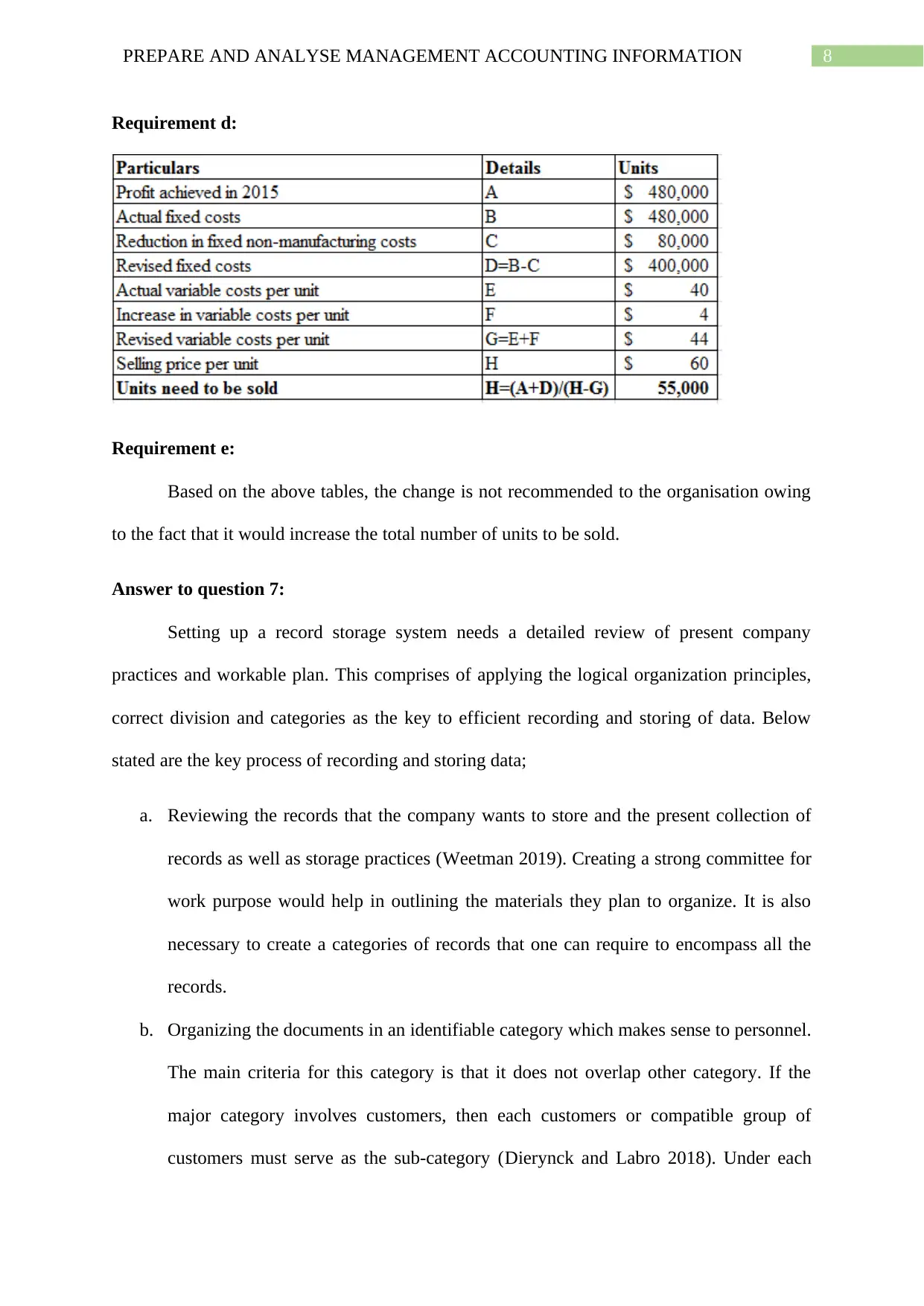

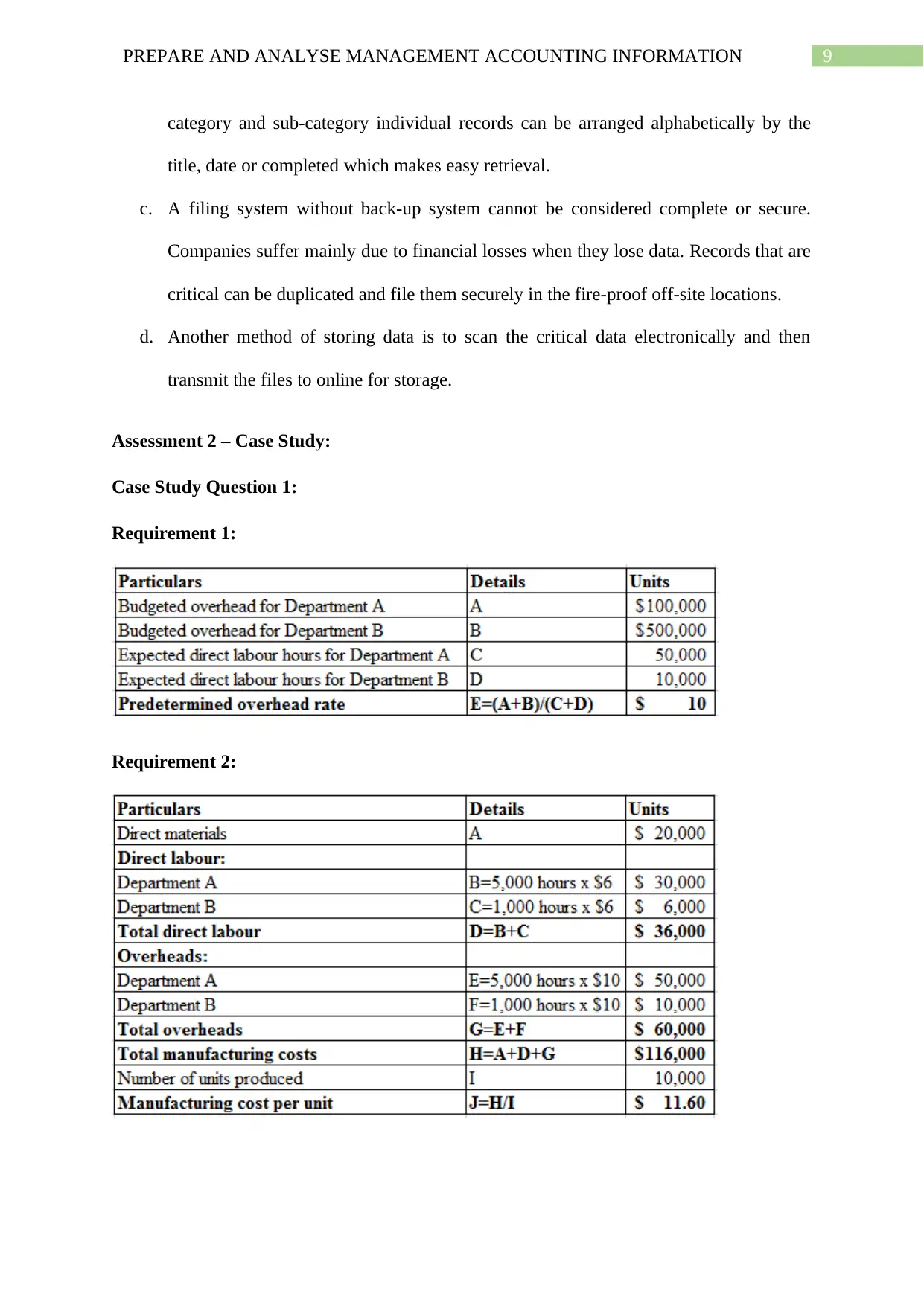

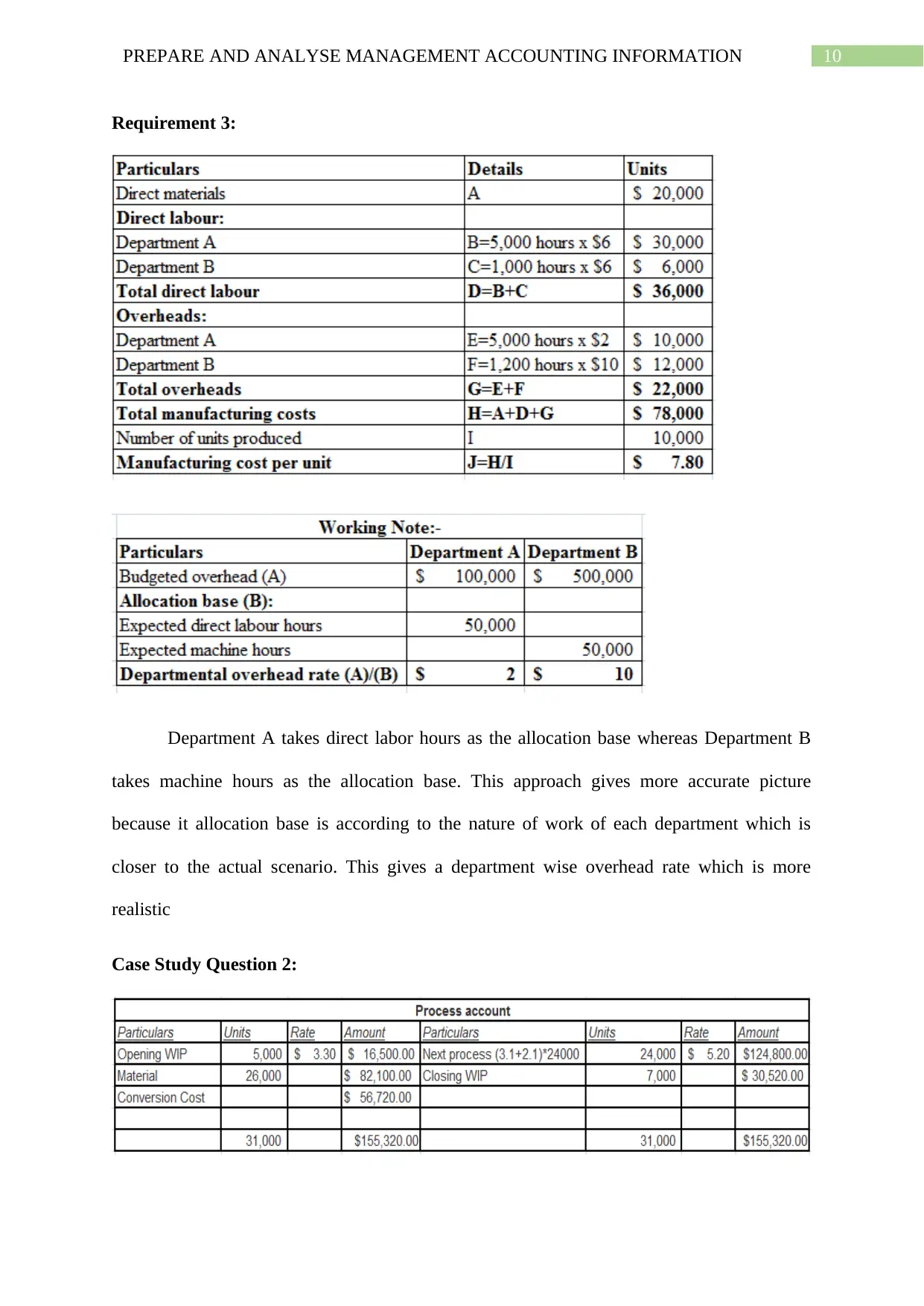

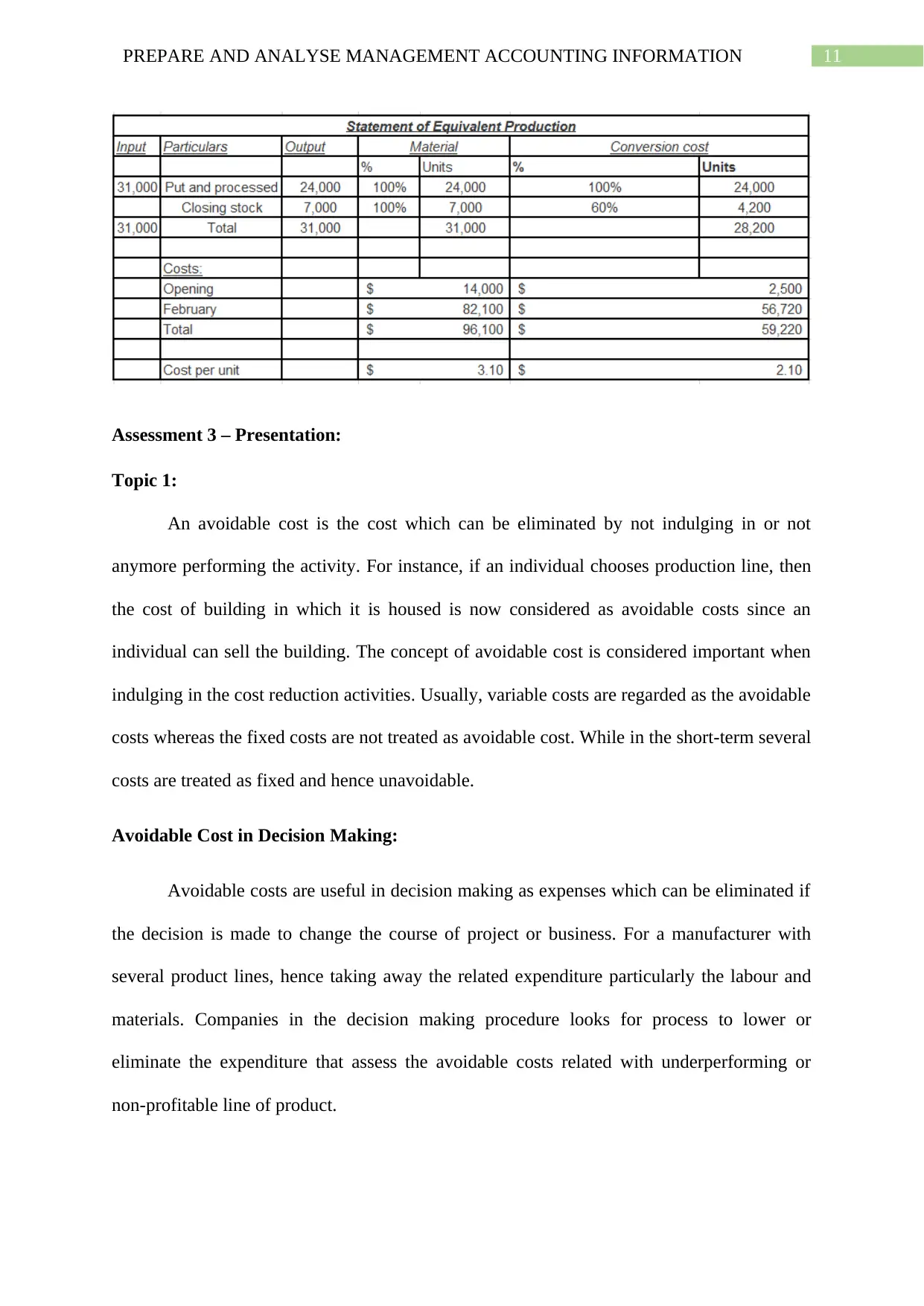

This report, prepared for the FNSACC613 course at CASS International College, delves into the core principles of management accounting. It begins with an exploration of the double-entry system, emphasizing its role in ensuring accuracy and financial clarity. The report then provides a detailed comparison of fixed and variable costs, along with an analysis of mixed costs and their implications. It further includes calculations and answers related to cost management. The report also addresses the importance of record storage systems and provides a case study analysis, examining overhead allocation methods. Additionally, the report covers avoidable costs in decision-making, the relevance of costs in production decisions, and contrasts authoritarian and participative budgeting styles. The report is well-structured, covering various aspects of management accounting, providing insights into cost analysis, budgeting, and decision-making processes.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.