Accounting Report: Final Accounts for Sole Traders and Partnerships

VerifiedAdded on 2021/01/02

|19

|3954

|267

Report

AI Summary

This report provides a comprehensive overview of preparing final accounts for sole traders and partnerships. It details the reasons for closing accounts and producing a trial balance, the processes involved in preparing final accounts, and the limitations encountered. The report explores methods of constructing accounts from incomplete records, reasons for imbalances, and the impact of insufficient data. It includes calculations for opening and closing capital, cash/bank accounts, sales and purchase ledger control accounts, and the application of markups and margins. The components of final accounts, including profit and loss accounts and balance sheets, are thoroughly explained. The report also covers key elements of partnership agreements, partnership accounts, profit and loss appropriation accounts, allocation of profits, and the preparation of capital and current accounts. Finally, it includes calculations of closing balances and a statement of financial position.

Prepare final accounts

for sole traders and

partnerships

for sole traders and

partnerships

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Reasons for closing off and producing trial balance..............................................................3

1.2 Process and limitation of preparing final accounts................................................................4

1.3 Methods of constructing accounts from incomplete records.................................................5

1.4 Reasons for imbalance resulting from incorrect entries........................................................5

1.5 Reasons for incomplete records arising from insufficient data.............................................5

TASK 2............................................................................................................................................6

2.1 Calculation of opening and closing capital............................................................................6

2.2 Calculation of opening and closing cash/ bank account........................................................7

2.3 Preparation of sales and purchase ledger control account.....................................................7

2.4 Mark ups and margins............................................................................................................8

TASK 3............................................................................................................................................9

3.1 Components of final accounts of the sole trader....................................................................9

3.2 Representation of profit and loss accounts according to the given information....................9

3.3 Representation of the balance sheet as per the given information.........................................9

TASK 4............................................................................................................................................9

4.1 Explanation regarding the key elements of a partnership agreement....................................9

4.2 Key components of partnership accounts............................................................................10

TASK 5..........................................................................................................................................11

5.1 Statement of profit and loss appropriation account.............................................................11

5.2 Allocation of profits to the partners.....................................................................................12

5.3 Capital and current account for each partner.......................................................................12

TASK 6 .........................................................................................................................................13

6.1 Calculation of closing balance of each partner's capital and current account......................13

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Reasons for closing off and producing trial balance..............................................................3

1.2 Process and limitation of preparing final accounts................................................................4

1.3 Methods of constructing accounts from incomplete records.................................................5

1.4 Reasons for imbalance resulting from incorrect entries........................................................5

1.5 Reasons for incomplete records arising from insufficient data.............................................5

TASK 2............................................................................................................................................6

2.1 Calculation of opening and closing capital............................................................................6

2.2 Calculation of opening and closing cash/ bank account........................................................7

2.3 Preparation of sales and purchase ledger control account.....................................................7

2.4 Mark ups and margins............................................................................................................8

TASK 3............................................................................................................................................9

3.1 Components of final accounts of the sole trader....................................................................9

3.2 Representation of profit and loss accounts according to the given information....................9

3.3 Representation of the balance sheet as per the given information.........................................9

TASK 4............................................................................................................................................9

4.1 Explanation regarding the key elements of a partnership agreement....................................9

4.2 Key components of partnership accounts............................................................................10

TASK 5..........................................................................................................................................11

5.1 Statement of profit and loss appropriation account.............................................................11

5.2 Allocation of profits to the partners.....................................................................................12

5.3 Capital and current account for each partner.......................................................................12

TASK 6 .........................................................................................................................................13

6.1 Calculation of closing balance of each partner's capital and current account......................13

6.2Statement of financial position.............................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In Accounting term, final accounts are consider to be accounts that are made at the end

of accounting year and help to disclose the actual financial position of business (Reid 2018).

Accountant of company follow a systematic process to prepare final accounts such as all

necessary business transaction are first recorded in journals and then transferred to ledger and

other important financial statements. Final accounts of partnership company and sole proprietary

are identical but the net income are separated on different basis. Sole proprietor is the only owner

of the company hence income statement and balance sheet is generated in sole proprietorship.

In this project report, process to form final accounts from incomplete data for partnership

and sole trader are discussed, closing account of legislative and accounting requirement for

partnership companies. Report also shows statements of P&L appropriation account, allocation

of profit to partnership and calculation for closing balance on capital and current account are

discussed.

TASK 1

1.1 Reasons for closing off and producing trial balance

In business world, every business organisation are used to close their expense and

revenues account at the end of fiscal year that help create to create new accounts with zero

balance for upcoming year. In general closing entry is consider to be journal entry that are made

at the end of financial year in which collected data is moved into permanent accounts on the

balance sheet from impermanent accounts on the income statement. There are different reason to

close account at the end of accounting year but the primary one if to transfer the current amount

of temporary accounts to the final accounts. This is done because some accounts are only

prepared for a certain period of time and are helpful to create financial reports and statements for

one financial period. It is observed that partnership firm and sole trader are used to close only

revenues, dividend and expenses account just because in case the balance of these accounts are

being carried forwards that may lead to create error in accounts and increase liabilities for

companies (Zeff, 2016).

Trail balance: In accounting term, a statements of each credit and debit in a double entry

book, that is shows with any disagreement that shows an error is known as trail balance. In

general it is defined as the list of all general ledger accounts that have been created during an

In Accounting term, final accounts are consider to be accounts that are made at the end

of accounting year and help to disclose the actual financial position of business (Reid 2018).

Accountant of company follow a systematic process to prepare final accounts such as all

necessary business transaction are first recorded in journals and then transferred to ledger and

other important financial statements. Final accounts of partnership company and sole proprietary

are identical but the net income are separated on different basis. Sole proprietor is the only owner

of the company hence income statement and balance sheet is generated in sole proprietorship.

In this project report, process to form final accounts from incomplete data for partnership

and sole trader are discussed, closing account of legislative and accounting requirement for

partnership companies. Report also shows statements of P&L appropriation account, allocation

of profit to partnership and calculation for closing balance on capital and current account are

discussed.

TASK 1

1.1 Reasons for closing off and producing trial balance

In business world, every business organisation are used to close their expense and

revenues account at the end of fiscal year that help create to create new accounts with zero

balance for upcoming year. In general closing entry is consider to be journal entry that are made

at the end of financial year in which collected data is moved into permanent accounts on the

balance sheet from impermanent accounts on the income statement. There are different reason to

close account at the end of accounting year but the primary one if to transfer the current amount

of temporary accounts to the final accounts. This is done because some accounts are only

prepared for a certain period of time and are helpful to create financial reports and statements for

one financial period. It is observed that partnership firm and sole trader are used to close only

revenues, dividend and expenses account just because in case the balance of these accounts are

being carried forwards that may lead to create error in accounts and increase liabilities for

companies (Zeff, 2016).

Trail balance: In accounting term, a statements of each credit and debit in a double entry

book, that is shows with any disagreement that shows an error is known as trail balance. In

general it is defined as the list of all general ledger accounts that have been created during an

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounting year. Basically accountant of companies prepare trail balance in order to determine

any mathematical error that have been posted while preparing journal ledger accounts. In case if

balance of debit and credit side are not equal than to adjust error accountant use to open suspense

account. It is usually observed that sole trader and partnership firm use to maintain trail balance

account to examine the arithmetical accuracy of the transaction for financial year.

1.2 Process and limitation of preparing final accounts.

In accounting term, trail balance is formulated for the main motive to determine the

balance of debit and credit. Accountant of company use to follow the process of maintaining trail

balance by closing the ledger account, cash book, all kind of subsidiary account and also bank

book prepared during an accounting year (Kumar and Sharma, 2015). Then the use to prepare

three column statements that contain actual name of all account showing their credit or debit

balance. Thus it is stated that trail balance acts as the main base of preparing financial statements

so that valuable decision can be taken. It is observed that preparation of trail balance must follow

the specific process in certain manner that is assets, liabilities, treatment of dividend, revenue

and expenses. Therefore particular procedure of speculate financial accounts from the trail

balance is discussed below:

Analyse the listing of trail balance dealing and all relevant modification accurately.

Then all the debit items from trail balance are posted on expenditure side of trading as

well as P&L accounts.

Record of all credit item shown in the trail balance are posted on income side of trading

profit & loss account.

Then before posting transaction all types of modification are done so that balance are

equal.

Profit & loss account balance are then used to ascertain net profit/ loss.

Add this profit acquire with the particular capital on the debt part of the balance sheet

Take the total of the balance sheet.

Limitation of formulating a trail balance

The trail balance is only able to display the actual error in account but not able to

determine the exact reason.

The main limitation is that trail balance is not able to find out the error that are occur

because of posting correct amount in incorrect ledger account (Bull, 2014).

any mathematical error that have been posted while preparing journal ledger accounts. In case if

balance of debit and credit side are not equal than to adjust error accountant use to open suspense

account. It is usually observed that sole trader and partnership firm use to maintain trail balance

account to examine the arithmetical accuracy of the transaction for financial year.

1.2 Process and limitation of preparing final accounts.

In accounting term, trail balance is formulated for the main motive to determine the

balance of debit and credit. Accountant of company use to follow the process of maintaining trail

balance by closing the ledger account, cash book, all kind of subsidiary account and also bank

book prepared during an accounting year (Kumar and Sharma, 2015). Then the use to prepare

three column statements that contain actual name of all account showing their credit or debit

balance. Thus it is stated that trail balance acts as the main base of preparing financial statements

so that valuable decision can be taken. It is observed that preparation of trail balance must follow

the specific process in certain manner that is assets, liabilities, treatment of dividend, revenue

and expenses. Therefore particular procedure of speculate financial accounts from the trail

balance is discussed below:

Analyse the listing of trail balance dealing and all relevant modification accurately.

Then all the debit items from trail balance are posted on expenditure side of trading as

well as P&L accounts.

Record of all credit item shown in the trail balance are posted on income side of trading

profit & loss account.

Then before posting transaction all types of modification are done so that balance are

equal.

Profit & loss account balance are then used to ascertain net profit/ loss.

Add this profit acquire with the particular capital on the debt part of the balance sheet

Take the total of the balance sheet.

Limitation of formulating a trail balance

The trail balance is only able to display the actual error in account but not able to

determine the exact reason.

The main limitation is that trail balance is not able to find out the error that are occur

because of posting correct amount in incorrect ledger account (Bull, 2014).

1.3 Methods of constructing accounts from incomplete records.

In present era, there are several kind of methods which are used to prepare accounts

through incomplete information. Some of these are described below:

Control accounts:

In this methods missed amount of assorted accounts are control in order to give valuable

decision (Collis, Holt and Hussey, 2017). For instance, in bank accounts if any information is

missing than bank control account is prepared with the support of acquirable information and at

last the amount of debit or credit side are assumed to be missing.

Accounting equation:

With the help of accounting equation method the evaluation actual value of capital could

be ascertain. The method state that total liabilities are deducted from amount of total assets In

order to evaluate the balancing figure of capital.

Margin method:

This method of accounting state that margin percentage is used in order to determine the

result for missing items. For example if accountant wants to calculate cost of sales then

balancing figure of sales and margin percentage is used to ascertain the values with the support

of available information.

1.4 Reasons for imbalance resulting from incorrect entries.

There are few ground behinds the instability of the outcome that have emerged due to

wrong double entries. Some of these are described below:

In case if accounting transaction are recorded only on single side of accounts and other

side is missed.

In case if incorrect balance is recorded in wrong ledger.

If the wrong or correct transaction are recorded double time in ledger accounts that lead

to false result (Chappell and Dunn, 2015).

In case if accountant are omitted to post ledger balance into final accounts.

1.5 Reasons for incomplete records arising from insufficient data.

In accounting term incomplete records basically arises due to insufficient data and there

are some specific reason also. Some of these are mention below:

In case if information is missing related to preparation of financial reports or statements.

Lack of information such as purchase, sales, depreciation etc.

In present era, there are several kind of methods which are used to prepare accounts

through incomplete information. Some of these are described below:

Control accounts:

In this methods missed amount of assorted accounts are control in order to give valuable

decision (Collis, Holt and Hussey, 2017). For instance, in bank accounts if any information is

missing than bank control account is prepared with the support of acquirable information and at

last the amount of debit or credit side are assumed to be missing.

Accounting equation:

With the help of accounting equation method the evaluation actual value of capital could

be ascertain. The method state that total liabilities are deducted from amount of total assets In

order to evaluate the balancing figure of capital.

Margin method:

This method of accounting state that margin percentage is used in order to determine the

result for missing items. For example if accountant wants to calculate cost of sales then

balancing figure of sales and margin percentage is used to ascertain the values with the support

of available information.

1.4 Reasons for imbalance resulting from incorrect entries.

There are few ground behinds the instability of the outcome that have emerged due to

wrong double entries. Some of these are described below:

In case if accounting transaction are recorded only on single side of accounts and other

side is missed.

In case if incorrect balance is recorded in wrong ledger.

If the wrong or correct transaction are recorded double time in ledger accounts that lead

to false result (Chappell and Dunn, 2015).

In case if accountant are omitted to post ledger balance into final accounts.

1.5 Reasons for incomplete records arising from insufficient data.

In accounting term incomplete records basically arises due to insufficient data and there

are some specific reason also. Some of these are mention below:

In case if information is missing related to preparation of financial reports or statements.

Lack of information such as purchase, sales, depreciation etc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

There are few error that arise while calculating balance of assets and equity at the period

of revaluation.

Some time error also occurs when business owner intentionally make error in the

accounting books to save tax or for some other reason.

TASK 2

2.1 Calculation of opening and closing capital

Capital accounts:

This is consider to be main accounts that are required to formulated to record all those

transaction that are related to capital. In this account the amount that have been paid by the

business owner and drawing used in business are recorded in capital accounts. To evaluate the

capital balance the formula is

Total assets- Total liabilities.

(1) Closing capital for the year

Capital Account

Particulars Amount Particulars Amount

To drawings 600 By balance b/d 1000

To balance c/d (b.f.) 3000 By net profits 2600

3600 3600

In the above calculation the closing capital for the current year has been determined that

is 3000.

(2) Opening capital for the period

Capital Account

Particulars Amount Particulars Amount

To drawings 800 To balance b/d (b.f.) 4640

To balance c/d 4200 By net profits 360

5000 5000

From the above calculation it has been concluded that opening balance of capital is 4200

for the accounting year.

of revaluation.

Some time error also occurs when business owner intentionally make error in the

accounting books to save tax or for some other reason.

TASK 2

2.1 Calculation of opening and closing capital

Capital accounts:

This is consider to be main accounts that are required to formulated to record all those

transaction that are related to capital. In this account the amount that have been paid by the

business owner and drawing used in business are recorded in capital accounts. To evaluate the

capital balance the formula is

Total assets- Total liabilities.

(1) Closing capital for the year

Capital Account

Particulars Amount Particulars Amount

To drawings 600 By balance b/d 1000

To balance c/d (b.f.) 3000 By net profits 2600

3600 3600

In the above calculation the closing capital for the current year has been determined that

is 3000.

(2) Opening capital for the period

Capital Account

Particulars Amount Particulars Amount

To drawings 800 To balance b/d (b.f.) 4640

To balance c/d 4200 By net profits 360

5000 5000

From the above calculation it has been concluded that opening balance of capital is 4200

for the accounting year.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

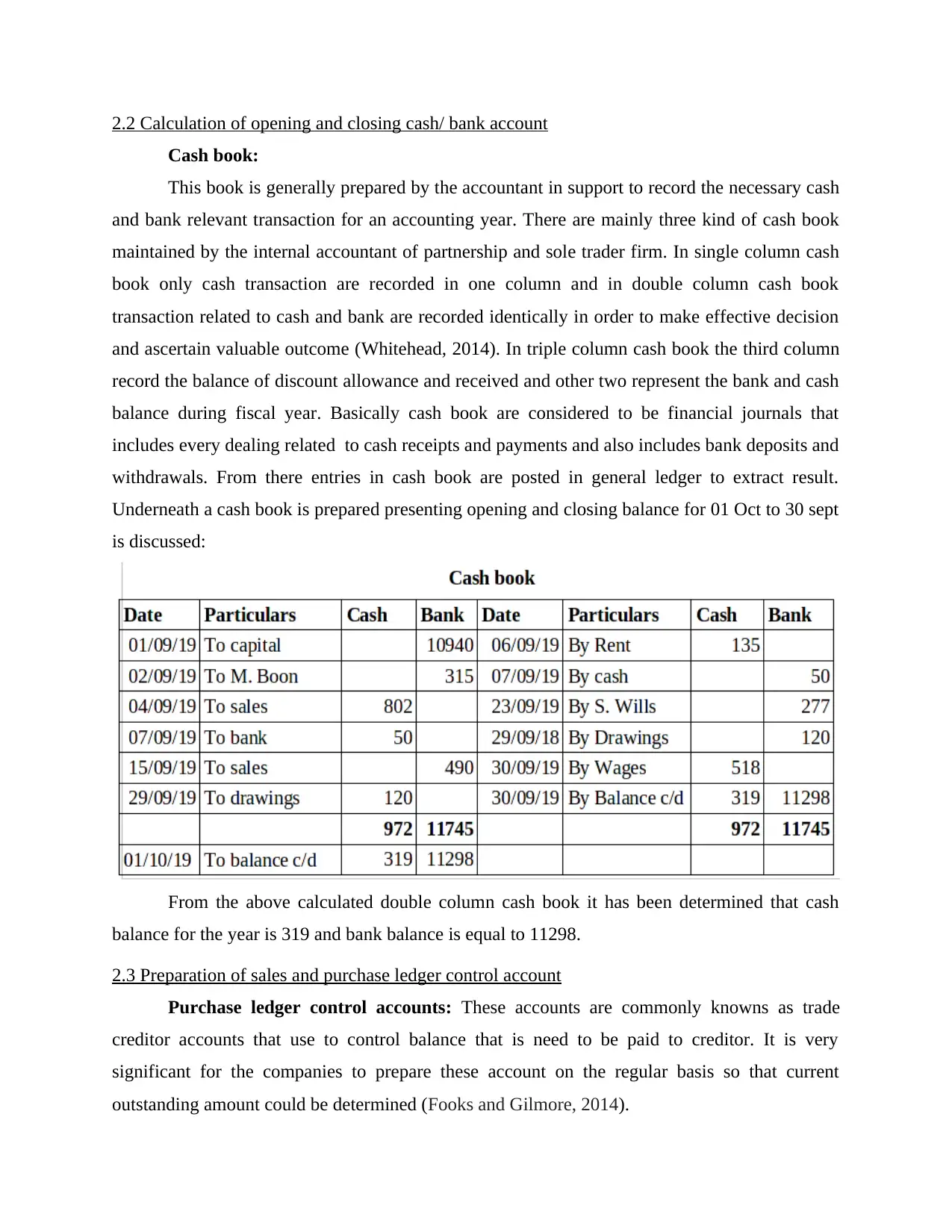

2.2 Calculation of opening and closing cash/ bank account

Cash book:

This book is generally prepared by the accountant in support to record the necessary cash

and bank relevant transaction for an accounting year. There are mainly three kind of cash book

maintained by the internal accountant of partnership and sole trader firm. In single column cash

book only cash transaction are recorded in one column and in double column cash book

transaction related to cash and bank are recorded identically in order to make effective decision

and ascertain valuable outcome (Whitehead, 2014). In triple column cash book the third column

record the balance of discount allowance and received and other two represent the bank and cash

balance during fiscal year. Basically cash book are considered to be financial journals that

includes every dealing related to cash receipts and payments and also includes bank deposits and

withdrawals. From there entries in cash book are posted in general ledger to extract result.

Underneath a cash book is prepared presenting opening and closing balance for 01 Oct to 30 sept

is discussed:

From the above calculated double column cash book it has been determined that cash

balance for the year is 319 and bank balance is equal to 11298.

2.3 Preparation of sales and purchase ledger control account

Purchase ledger control accounts: These accounts are commonly knowns as trade

creditor accounts that use to control balance that is need to be paid to creditor. It is very

significant for the companies to prepare these account on the regular basis so that current

outstanding amount could be determined (Fooks and Gilmore, 2014).

Cash book:

This book is generally prepared by the accountant in support to record the necessary cash

and bank relevant transaction for an accounting year. There are mainly three kind of cash book

maintained by the internal accountant of partnership and sole trader firm. In single column cash

book only cash transaction are recorded in one column and in double column cash book

transaction related to cash and bank are recorded identically in order to make effective decision

and ascertain valuable outcome (Whitehead, 2014). In triple column cash book the third column

record the balance of discount allowance and received and other two represent the bank and cash

balance during fiscal year. Basically cash book are considered to be financial journals that

includes every dealing related to cash receipts and payments and also includes bank deposits and

withdrawals. From there entries in cash book are posted in general ledger to extract result.

Underneath a cash book is prepared presenting opening and closing balance for 01 Oct to 30 sept

is discussed:

From the above calculated double column cash book it has been determined that cash

balance for the year is 319 and bank balance is equal to 11298.

2.3 Preparation of sales and purchase ledger control account

Purchase ledger control accounts: These accounts are commonly knowns as trade

creditor accounts that use to control balance that is need to be paid to creditor. It is very

significant for the companies to prepare these account on the regular basis so that current

outstanding amount could be determined (Fooks and Gilmore, 2014).

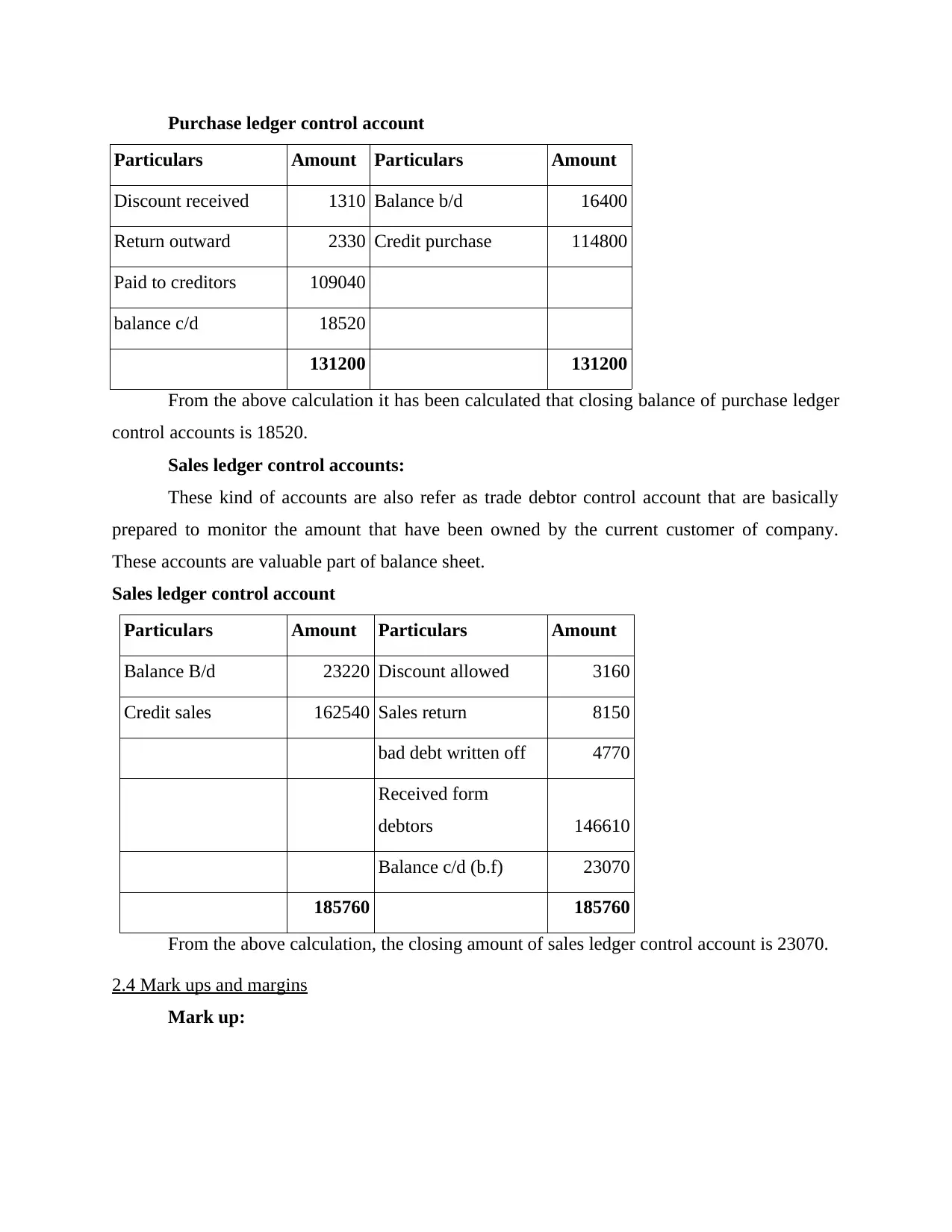

Purchase ledger control account

Particulars Amount Particulars Amount

Discount received 1310 Balance b/d 16400

Return outward 2330 Credit purchase 114800

Paid to creditors 109040

balance c/d 18520

131200 131200

From the above calculation it has been calculated that closing balance of purchase ledger

control accounts is 18520.

Sales ledger control accounts:

These kind of accounts are also refer as trade debtor control account that are basically

prepared to monitor the amount that have been owned by the current customer of company.

These accounts are valuable part of balance sheet.

Sales ledger control account

Particulars Amount Particulars Amount

Balance B/d 23220 Discount allowed 3160

Credit sales 162540 Sales return 8150

bad debt written off 4770

Received form

debtors 146610

Balance c/d (b.f) 23070

185760 185760

From the above calculation, the closing amount of sales ledger control account is 23070.

2.4 Mark ups and margins

Mark up:

Particulars Amount Particulars Amount

Discount received 1310 Balance b/d 16400

Return outward 2330 Credit purchase 114800

Paid to creditors 109040

balance c/d 18520

131200 131200

From the above calculation it has been calculated that closing balance of purchase ledger

control accounts is 18520.

Sales ledger control accounts:

These kind of accounts are also refer as trade debtor control account that are basically

prepared to monitor the amount that have been owned by the current customer of company.

These accounts are valuable part of balance sheet.

Sales ledger control account

Particulars Amount Particulars Amount

Balance B/d 23220 Discount allowed 3160

Credit sales 162540 Sales return 8150

bad debt written off 4770

Received form

debtors 146610

Balance c/d (b.f) 23070

185760 185760

From the above calculation, the closing amount of sales ledger control account is 23070.

2.4 Mark ups and margins

Mark up:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is consider to be the ration among the selling price and cost of a specific product that is

usually characterized as the percent over cost. In general it is known as the fixed balance or

percent of selling price or cost of companies services and goods.

Margins:

This is a type of margin percentage is often refer to sales to profitability that can aid to

several key understanding about the organisation business model (Gilbert and Pfuderer, 2014). It

is also used to determine how successful the business firm is maintaining its cost structure to

gain the accurate amount of sales.

TASK 3

3.1 Components of final accounts of the sole trader.

There are basically two components of financial accounts that are prepared by the

accountant of sole trader and partnership firm. These final accounts are profit & loss account and

balance sheet that are discussed below:

Profit and loss accounts:

In accounting term, P&L account are prepare by the companies at the end of accounting

year in order to determine the profit or loss for that particular year (Hoffmann and Zuelch,

2014). In general, it is commonly known as income statements or consolidate P&L accounts that

is used to be evaluated with the support of trail balance and other ledger accounts that are

formulated in accounting process. Basically all the relevant income and expenses are included in

P&L account in order to figure out actual loss and profit for partnership as well as sole trader

firms. Companies usually prepare trading profit and loss statements at the end of fiscal year after

the preparation of all other necessary accounts.

Balance sheet:

The finally prepared balance sheet use to display the actual financial position of business

entity. Balance sheet represent the appropriate and accurate figure of assets, liabilities, owner

equities. Capital, revenues and expenses with the main objective to determine the net worth of

the company. Basically balance sheet also includes the previous year information that help to do

comparative analysis in order to make useful decision. Mainly accountant use to prepare

financial balance sheet in order to present the financial status to external shareholder so that they

can analyse the fiscal growth and make suitable investment.

usually characterized as the percent over cost. In general it is known as the fixed balance or

percent of selling price or cost of companies services and goods.

Margins:

This is a type of margin percentage is often refer to sales to profitability that can aid to

several key understanding about the organisation business model (Gilbert and Pfuderer, 2014). It

is also used to determine how successful the business firm is maintaining its cost structure to

gain the accurate amount of sales.

TASK 3

3.1 Components of final accounts of the sole trader.

There are basically two components of financial accounts that are prepared by the

accountant of sole trader and partnership firm. These final accounts are profit & loss account and

balance sheet that are discussed below:

Profit and loss accounts:

In accounting term, P&L account are prepare by the companies at the end of accounting

year in order to determine the profit or loss for that particular year (Hoffmann and Zuelch,

2014). In general, it is commonly known as income statements or consolidate P&L accounts that

is used to be evaluated with the support of trail balance and other ledger accounts that are

formulated in accounting process. Basically all the relevant income and expenses are included in

P&L account in order to figure out actual loss and profit for partnership as well as sole trader

firms. Companies usually prepare trading profit and loss statements at the end of fiscal year after

the preparation of all other necessary accounts.

Balance sheet:

The finally prepared balance sheet use to display the actual financial position of business

entity. Balance sheet represent the appropriate and accurate figure of assets, liabilities, owner

equities. Capital, revenues and expenses with the main objective to determine the net worth of

the company. Basically balance sheet also includes the previous year information that help to do

comparative analysis in order to make useful decision. Mainly accountant use to prepare

financial balance sheet in order to present the financial status to external shareholder so that they

can analyse the fiscal growth and make suitable investment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

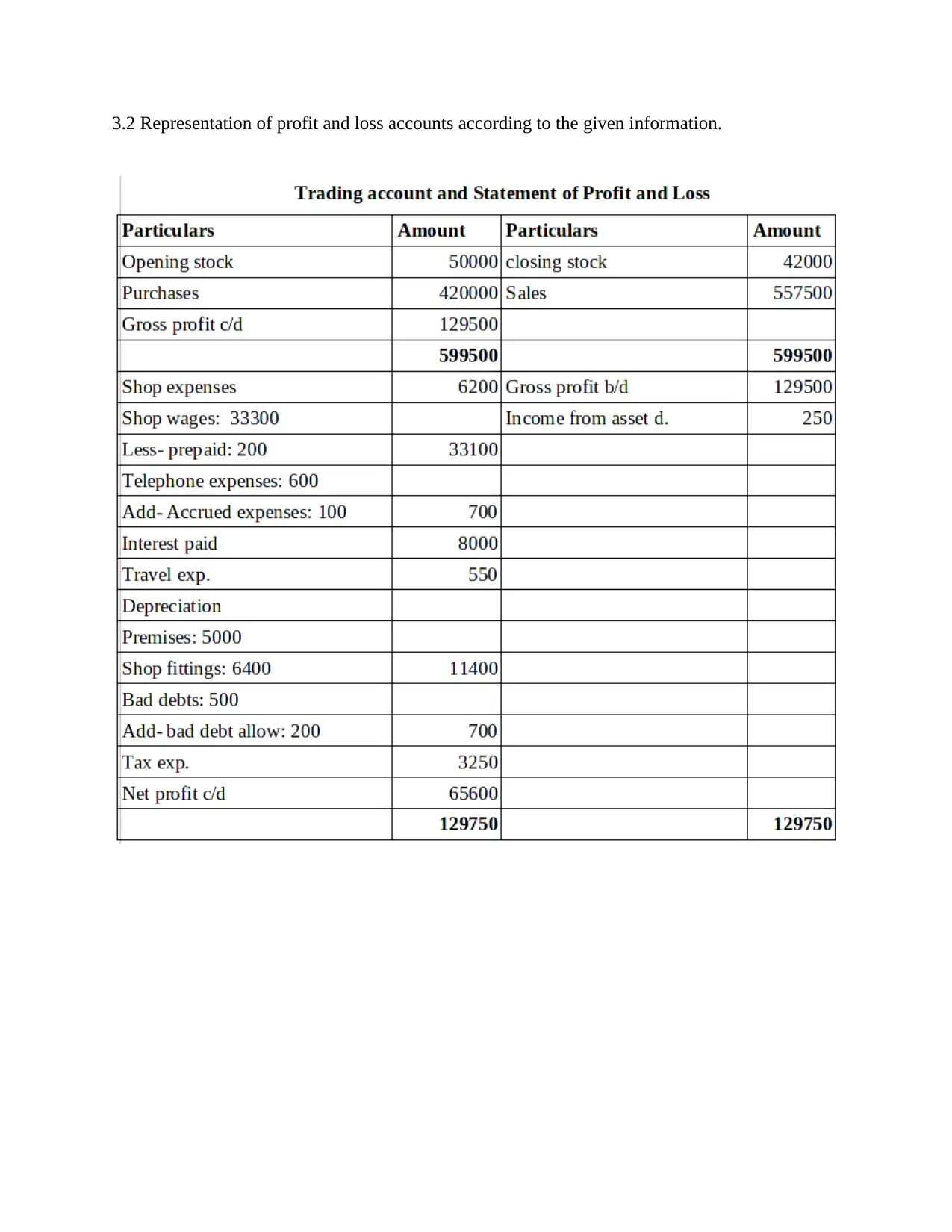

3.2 Representation of profit and loss accounts according to the given information.

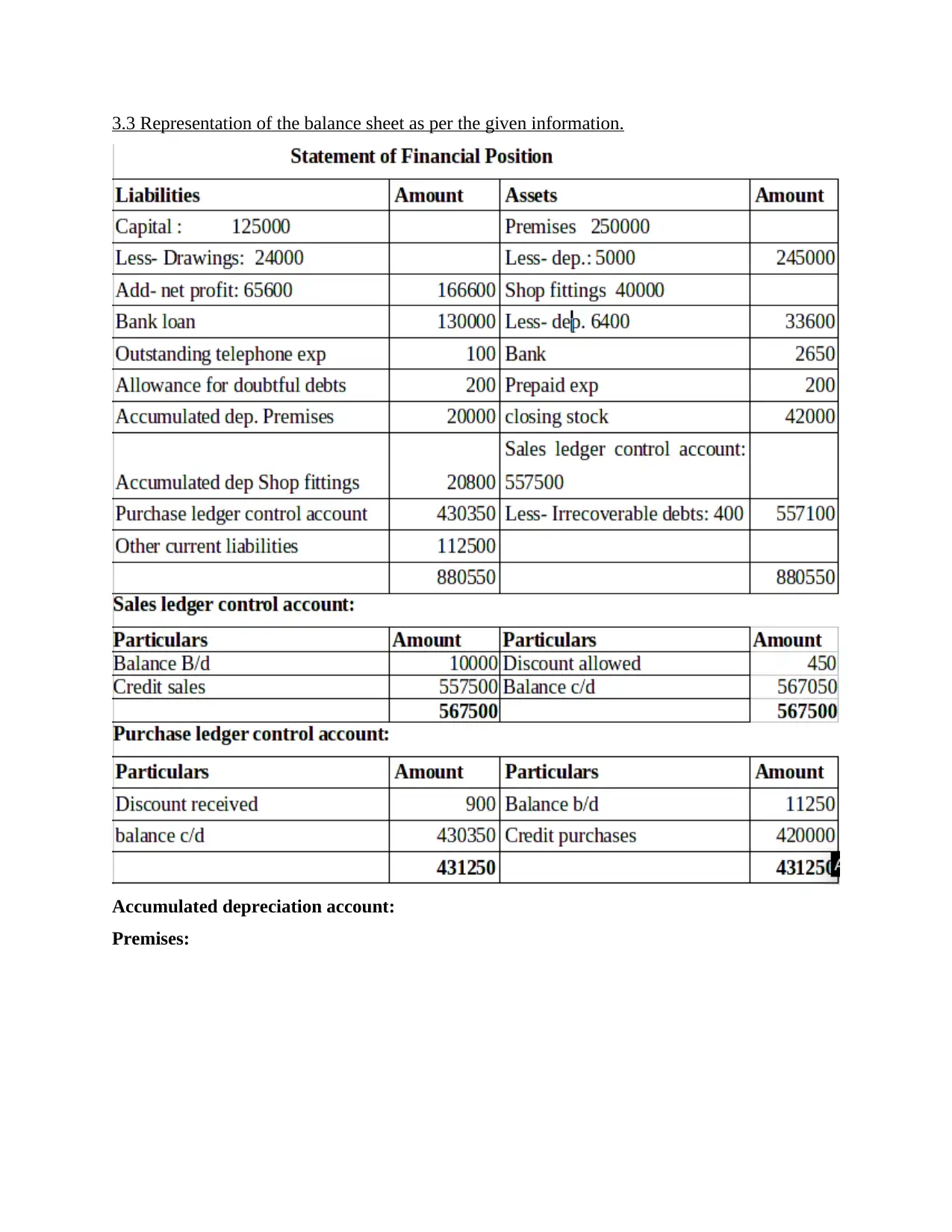

3.3 Representation of the balance sheet as per the given information.

Accumulated depreciation account:

Premises:

Accumulated depreciation account:

Premises:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.