FNSFMB401: Preparing Loan Applications for Finance Clients

VerifiedAdded on 2022/11/29

|14

|4050

|268

Report

AI Summary

This report provides a detailed overview of the process of preparing loan applications within the context of finance and mortgage broking. It begins by outlining the key features of relevant legislation and codes of practice governing the industry. The report then delves into the different types of lender forms, the information required to support a loan application, and the crucial stages and features of the loan settlement process. It further describes the essential aspects of the loan application, lender requirements and guidelines, and the types of security lenders typically require. The report also covers third party report activity, the research task, and includes references to support the information provided. The report aims to provide a comprehensive guide to preparing effective loan applications for finance and mortgage broking clients, covering topics from legislative frameworks to security requirements.

FNSFMB401 PREPARE LOAN

APPLICATION ON BEHALF OF

FINANCE OR MORTGAGE

BROKING CLIENTS

APPLICATION ON BEHALF OF

FINANCE OR MORTGAGE

BROKING CLIENTS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TASK.........................................................................................................................................3

1. Key features of the current legislation and codes of practice relating to finance and

mortgage broking...................................................................................................................3

2. Different types of relevant lender forms............................................................................3

3. Information required to support a loan application............................................................3

4. Key stages and features of the loan settlement process......................................................4

5. Description.........................................................................................................................5

6. Features of the process.......................................................................................................6

7. Lender requirements and guidelines for loan applications and securing a loan.................6

8. Types of security required by the lenders..........................................................................7

THIRD PARTY REPORT ACTIVITY.....................................................................................7

Prepare a loan application......................................................................................................7

RESEARCH TASK AND WRITTEN/ORAL QUESTIONS..................................................10

REFERENCES.........................................................................................................................14

TASK.........................................................................................................................................3

1. Key features of the current legislation and codes of practice relating to finance and

mortgage broking...................................................................................................................3

2. Different types of relevant lender forms............................................................................3

3. Information required to support a loan application............................................................3

4. Key stages and features of the loan settlement process......................................................4

5. Description.........................................................................................................................5

6. Features of the process.......................................................................................................6

7. Lender requirements and guidelines for loan applications and securing a loan.................6

8. Types of security required by the lenders..........................................................................7

THIRD PARTY REPORT ACTIVITY.....................................................................................7

Prepare a loan application......................................................................................................7

RESEARCH TASK AND WRITTEN/ORAL QUESTIONS..................................................10

REFERENCES.........................................................................................................................14

TASK

1. Key features of the current legislation and codes of practice relating to finance and

mortgage broking

There are various laws and the code of practice that has been established in relation

to the finance and the mortgage broking which are commenced to regulate the industry. There

is a mandatory credit licensing regime that has to be followed by those who are undertaking

the activity. There are strict regulations over the sanctioning process and the enhancement

powers which provide for the dispute resolution system. There are also the credit service

intermediaries that are governed by the codes of practice. And lastly some important

regulatory bodies that assume the responsibility of the credit control process.

2. Different types of relevant lender forms

There can be two relevant lender forms that are used in the sanctioning of the loans

by the lender:- Loan estimate- This is one type of the form that is to be mandatorily be provided by

the lender to the borrower within the three business working days. It shall hep the

companies with the comparison of the different loan offers that are provided to them.

Among these the best alternative shall be selected.

Closing disclosure- This is the final and the closing document that is issued by the

lender that shall be specifying the various costs of the loan that is sanctioned and the

total cost that shall be applicable against receiving the loan. This is also issued in no

less than the three working days of business.

3. Information required to support a loan application

In order to prepare for an efficient loan application which is self-sufficient it must

disclose all the relevant information of the borrower which might be needed by the lender or

is required to convince regarding sanctioning of loan amount. The compilation of the loan

application can be divided into various sections:- Cover sheet- It shall be showing the name of the applicant, business name, address of

the sender and the receiver. It shall be depicting that the application is successfully

sent to the bank to whom the loan is applied (Lau, 2020). Cover letter- This part of the loan application consists of the three paragraphs, the

first one contains the request regarding the consideration for the loan, the second para

shall be describing the business of the applicant and the last para shall be disclosing

the future plans of the business.

1. Key features of the current legislation and codes of practice relating to finance and

mortgage broking

There are various laws and the code of practice that has been established in relation

to the finance and the mortgage broking which are commenced to regulate the industry. There

is a mandatory credit licensing regime that has to be followed by those who are undertaking

the activity. There are strict regulations over the sanctioning process and the enhancement

powers which provide for the dispute resolution system. There are also the credit service

intermediaries that are governed by the codes of practice. And lastly some important

regulatory bodies that assume the responsibility of the credit control process.

2. Different types of relevant lender forms

There can be two relevant lender forms that are used in the sanctioning of the loans

by the lender:- Loan estimate- This is one type of the form that is to be mandatorily be provided by

the lender to the borrower within the three business working days. It shall hep the

companies with the comparison of the different loan offers that are provided to them.

Among these the best alternative shall be selected.

Closing disclosure- This is the final and the closing document that is issued by the

lender that shall be specifying the various costs of the loan that is sanctioned and the

total cost that shall be applicable against receiving the loan. This is also issued in no

less than the three working days of business.

3. Information required to support a loan application

In order to prepare for an efficient loan application which is self-sufficient it must

disclose all the relevant information of the borrower which might be needed by the lender or

is required to convince regarding sanctioning of loan amount. The compilation of the loan

application can be divided into various sections:- Cover sheet- It shall be showing the name of the applicant, business name, address of

the sender and the receiver. It shall be depicting that the application is successfully

sent to the bank to whom the loan is applied (Lau, 2020). Cover letter- This part of the loan application consists of the three paragraphs, the

first one contains the request regarding the consideration for the loan, the second para

shall be describing the business of the applicant and the last para shall be disclosing

the future plans of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Amount and use of the loan- This part shall be specifying the amount of loan that is

required and the purpose for which such loan is being obtained like the capital

investment. History of the business- It shall be describing the facts about the business its legal

form, operations and the location where the operations of the company are conducted. Management team- It shall be providing the information related to management team

and their key personnels. They can be either be the permanent employees of the

company Marketing information- This section of the application form shows the market

information of the product and services that are offered by the business and also the

potential market that the company is targeting. Financial history- The financial history and position of the company are also the

important information that are required by the banker. This proves the credibility of

the business. Future projections- The data pertaining to the future of the company is also relevant

for the lender as he needs to evaluate the success of the plan and whether the enough

cash flows shall be generated so that the loan can be timely and efficiently be repaid

by the company. Collateral- The company shall have to list the available collateral security with them

and their fair market value against which the loan can be obtained. In case the

company is unable to pay back the loan then the banker shall be confiscating the

security. Personal financial statements- The bankers in order to accept the offer has to prior

check out the personal statements, tax returns and the net worth of the borrower for

the guarantee in the future.

Additional documents- These documents can be additional which shall be

determining the capability of the business in terms of the future contracts, credit

ratings, market research information etc.

4. Key stages and features of the loan settlement process

The loan settlement procedure involve certain steps that rae to be followed in order

tyo obtain the settlement as per required condition :- Pre qualification process – This is the first step that is used in the origination of the

lending process where the various id proofs, credit ratings and the various statements

required and the purpose for which such loan is being obtained like the capital

investment. History of the business- It shall be describing the facts about the business its legal

form, operations and the location where the operations of the company are conducted. Management team- It shall be providing the information related to management team

and their key personnels. They can be either be the permanent employees of the

company Marketing information- This section of the application form shows the market

information of the product and services that are offered by the business and also the

potential market that the company is targeting. Financial history- The financial history and position of the company are also the

important information that are required by the banker. This proves the credibility of

the business. Future projections- The data pertaining to the future of the company is also relevant

for the lender as he needs to evaluate the success of the plan and whether the enough

cash flows shall be generated so that the loan can be timely and efficiently be repaid

by the company. Collateral- The company shall have to list the available collateral security with them

and their fair market value against which the loan can be obtained. In case the

company is unable to pay back the loan then the banker shall be confiscating the

security. Personal financial statements- The bankers in order to accept the offer has to prior

check out the personal statements, tax returns and the net worth of the borrower for

the guarantee in the future.

Additional documents- These documents can be additional which shall be

determining the capability of the business in terms of the future contracts, credit

ratings, market research information etc.

4. Key stages and features of the loan settlement process

The loan settlement procedure involve certain steps that rae to be followed in order

tyo obtain the settlement as per required condition :- Pre qualification process – This is the first step that is used in the origination of the

lending process where the various id proofs, credit ratings and the various statements

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of the company are produced to lender to initiate the process by the borrower (Sen

and Rajagopal, 2020). Loan applications- Then the next step involves the creation of the loan application by

the borrower that shall be presenting the various important information of the

company to te lender sufficient for it to analyse the scope of the business and its credit

capacity. Application processing- This is the step where the lender shall be evaluating

regarding the accuracy and completeness of the data. They have the loan origination

system that is used for this purpose where the facts quoted by the business are verified

by the lender so that complete assurance can be obtained before the loan is sanctioned

by the banker. Underwriting process- Post the loan application is complete in all means the

underwriting process is applied on it which qualifies the borrower in terms of the

credit score, risk appetite and the payback capacity. They have their unique of

allotting the score. Credit decision- Finally based on all the conclusions the decision shall be made in

respect of whether the loan is to be accepted, rejected or is to be sent back to the

applicant for some further requirements that are remaining to be addressed. Quality check – This is the other quality control team that is appointed at the lenders

end who is responsible for analysing the critical variables, the rules and regulations

and the governance issues that could be faced by the banks. They are highly regulated

and controlled administration that is effected by the lender.

Loan funding – This is the last step in the loan settlement procedure which is related

to the funding of loans to the borrower. This is executed post all the documents have

been signed by both the parties and the collateral has been obtained against the loans

so funded.

5. Description Term – The term in relation to the loan is the time period for which the loan is

sanctioned by the banker. This is the time period for which the company can use the

sum of money that is provided and as soon as this time period shall be expiring for the

company they are to repay the amount of loan with the interest charge that has been

imposed on it.

and Rajagopal, 2020). Loan applications- Then the next step involves the creation of the loan application by

the borrower that shall be presenting the various important information of the

company to te lender sufficient for it to analyse the scope of the business and its credit

capacity. Application processing- This is the step where the lender shall be evaluating

regarding the accuracy and completeness of the data. They have the loan origination

system that is used for this purpose where the facts quoted by the business are verified

by the lender so that complete assurance can be obtained before the loan is sanctioned

by the banker. Underwriting process- Post the loan application is complete in all means the

underwriting process is applied on it which qualifies the borrower in terms of the

credit score, risk appetite and the payback capacity. They have their unique of

allotting the score. Credit decision- Finally based on all the conclusions the decision shall be made in

respect of whether the loan is to be accepted, rejected or is to be sent back to the

applicant for some further requirements that are remaining to be addressed. Quality check – This is the other quality control team that is appointed at the lenders

end who is responsible for analysing the critical variables, the rules and regulations

and the governance issues that could be faced by the banks. They are highly regulated

and controlled administration that is effected by the lender.

Loan funding – This is the last step in the loan settlement procedure which is related

to the funding of loans to the borrower. This is executed post all the documents have

been signed by both the parties and the collateral has been obtained against the loans

so funded.

5. Description Term – The term in relation to the loan is the time period for which the loan is

sanctioned by the banker. This is the time period for which the company can use the

sum of money that is provided and as soon as this time period shall be expiring for the

company they are to repay the amount of loan with the interest charge that has been

imposed on it.

Interest rate- Interest rate is the percentage that is charged on the principal amount by

the lender from the borrower. This is the cost of the sum of money that is being used

by the borrower for some productive purpose. Amount- The amount can also be referred as the principal that is provided by the

lender to the borrower. This is the sum of money that has been sanctioned in the form

of loan by the banker.

Support documentation- The support documents in case of the granting a loan can be

the personal id proofs, credit score proofs, financial statements of the company,

address proof of the person. These can be used for verifying the details of the

company.

6. Features of the process

Loan management- The complete loan management process of the lending company

that is executed has some features which are to be essentially undertaken to extend a

safe and secure loan to the borrower (Saindane and et.al., 2021). The process starts

from the loan origination where the borrower applies for the loan to the lender and

this gets sanctioned by the bank. The next step is related to the servicing of the loans

and further the lender has to collect the debt that is due from the borrower either in the

form of principal amount or in the form of interest. The final step involves the

reporting and analytics.

Instructing valuers to assess the value of a property or other types of security- A

professional property valuer shall be ascertained who shall be valuing the property

such that the exact market value can be assessed by the valuation officer. The owner

should also be handled with the responsibility of valuing the asset so that the double

verification can take place. This shows that as soon as the loan is unable to be repaid

then in that case this security can be used to repay the amount.

7. Lender requirements and guidelines for loan applications and securing a loan

There are some lender requirements that are to be fulfilled by the borrowers in order

to secure the loan from the lenders. The major requirements are that they must know about

the purpose for which the loan is obtained by the borrower, the other is the business

experience and the history of the business, they must know the future business plans of the

business, the credit ratings and score of the business needs to be positive, all the personal

details about the business must be provided and with that the financial statements disclosing

the financial stability must be provided to the lender. Apart from that the other major

significance is of the collateral security and its market value.

the lender from the borrower. This is the cost of the sum of money that is being used

by the borrower for some productive purpose. Amount- The amount can also be referred as the principal that is provided by the

lender to the borrower. This is the sum of money that has been sanctioned in the form

of loan by the banker.

Support documentation- The support documents in case of the granting a loan can be

the personal id proofs, credit score proofs, financial statements of the company,

address proof of the person. These can be used for verifying the details of the

company.

6. Features of the process

Loan management- The complete loan management process of the lending company

that is executed has some features which are to be essentially undertaken to extend a

safe and secure loan to the borrower (Saindane and et.al., 2021). The process starts

from the loan origination where the borrower applies for the loan to the lender and

this gets sanctioned by the bank. The next step is related to the servicing of the loans

and further the lender has to collect the debt that is due from the borrower either in the

form of principal amount or in the form of interest. The final step involves the

reporting and analytics.

Instructing valuers to assess the value of a property or other types of security- A

professional property valuer shall be ascertained who shall be valuing the property

such that the exact market value can be assessed by the valuation officer. The owner

should also be handled with the responsibility of valuing the asset so that the double

verification can take place. This shows that as soon as the loan is unable to be repaid

then in that case this security can be used to repay the amount.

7. Lender requirements and guidelines for loan applications and securing a loan

There are some lender requirements that are to be fulfilled by the borrowers in order

to secure the loan from the lenders. The major requirements are that they must know about

the purpose for which the loan is obtained by the borrower, the other is the business

experience and the history of the business, they must know the future business plans of the

business, the credit ratings and score of the business needs to be positive, all the personal

details about the business must be provided and with that the financial statements disclosing

the financial stability must be provided to the lender. Apart from that the other major

significance is of the collateral security and its market value.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8. Types of security required by the lenders

There are various types of securities that may be required by the lender against the

loan that is sanctioned by the bankers. This is in the form of guarantee against the sum

provided by them that in case the repayment is not done timely then shall be confiscating the

security to recover the due amount from the auction. These are the types of securities that can

be provided to the lender:- Personal security- The personal security is a type of personal guarantee that is given

by the borrower himself or third party in the lead of pledging the tangible asset with

the banker. This guarantee is not easily provided as just the personal assurance is not

sufficient for the lender but this shall be accepted only in the case where there is high

financial solvency, social status, integrity and credibility of the party under concern

(Rath, Das and Acharya, 2021). Non-personal security- The non-personal security is one which can either be in the

form of movable or immovable property like the land, building or any other physical

commodities. They are comparatively safer than the personal securities as in case the

amount of loan is not repaid by the borrower then in that case the property can be sold

to recover the due amount.

Collateral security- If the banker thinks that the non-personal security that has been

collected is insufficient for the recovery f the loan in that case they may demand for

the additional collateral security. This shall be helping the lender to recover the dues

smoothly in case the situation occurs.

THIRD PARTY REPORT ACTIVITY

Prepare a loan application

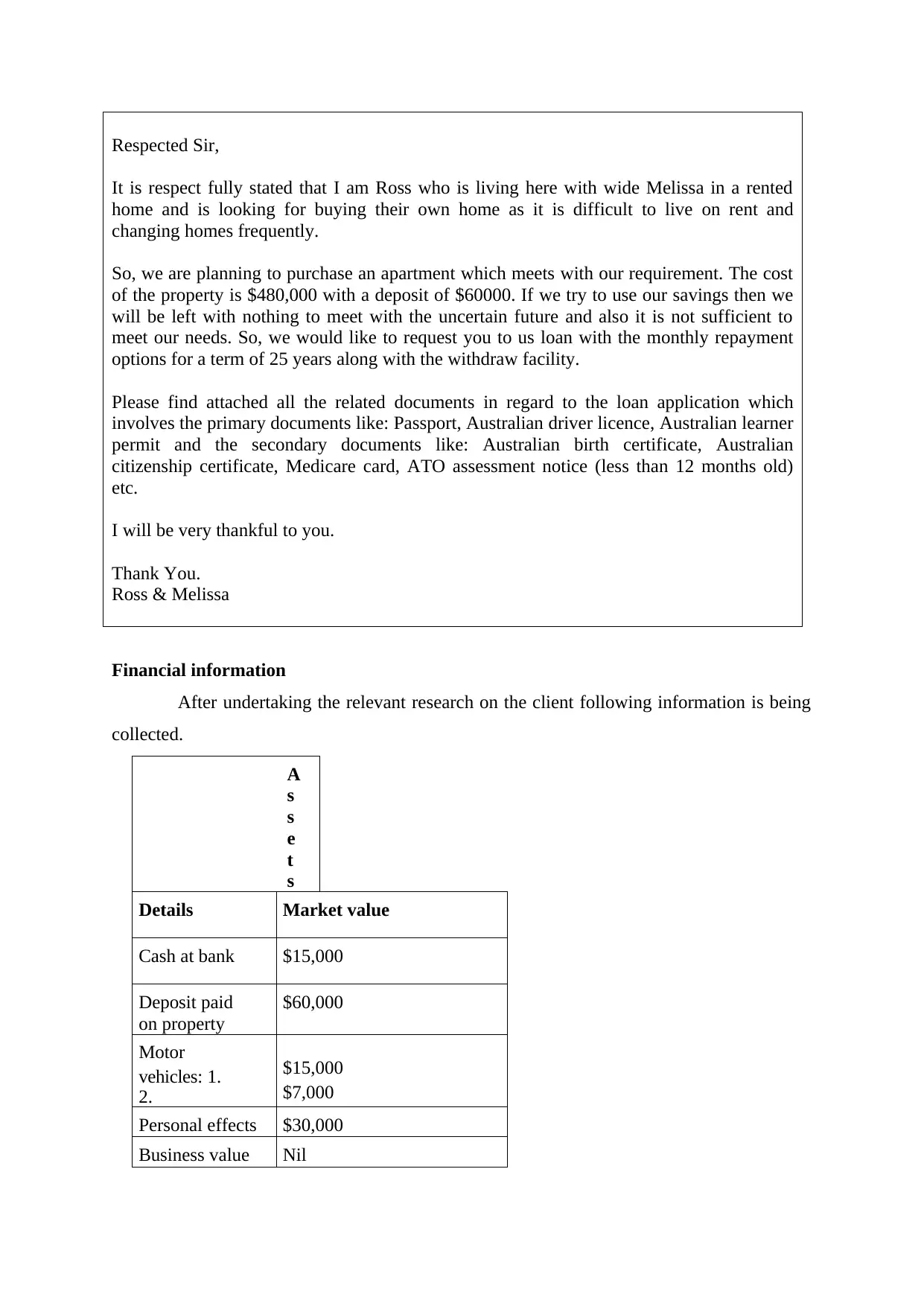

Ross and Melissa are a couple married for 5 years and is looking to buy their own

home After a month of searching they found a suitable apartment which meets their needs,

the purchase cost of the property is $480,000 and has also provided a deposit for the same

amounting to $60000. Ross is having a salary of $80000 and Melissa has a salary of $70000.

The couple is looking for a term loan of 25 years.

Application for loan

To, XYZ ltd

Subject: Application for home loan

There are various types of securities that may be required by the lender against the

loan that is sanctioned by the bankers. This is in the form of guarantee against the sum

provided by them that in case the repayment is not done timely then shall be confiscating the

security to recover the due amount from the auction. These are the types of securities that can

be provided to the lender:- Personal security- The personal security is a type of personal guarantee that is given

by the borrower himself or third party in the lead of pledging the tangible asset with

the banker. This guarantee is not easily provided as just the personal assurance is not

sufficient for the lender but this shall be accepted only in the case where there is high

financial solvency, social status, integrity and credibility of the party under concern

(Rath, Das and Acharya, 2021). Non-personal security- The non-personal security is one which can either be in the

form of movable or immovable property like the land, building or any other physical

commodities. They are comparatively safer than the personal securities as in case the

amount of loan is not repaid by the borrower then in that case the property can be sold

to recover the due amount.

Collateral security- If the banker thinks that the non-personal security that has been

collected is insufficient for the recovery f the loan in that case they may demand for

the additional collateral security. This shall be helping the lender to recover the dues

smoothly in case the situation occurs.

THIRD PARTY REPORT ACTIVITY

Prepare a loan application

Ross and Melissa are a couple married for 5 years and is looking to buy their own

home After a month of searching they found a suitable apartment which meets their needs,

the purchase cost of the property is $480,000 and has also provided a deposit for the same

amounting to $60000. Ross is having a salary of $80000 and Melissa has a salary of $70000.

The couple is looking for a term loan of 25 years.

Application for loan

To, XYZ ltd

Subject: Application for home loan

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Respected Sir,

It is respect fully stated that I am Ross who is living here with wide Melissa in a rented

home and is looking for buying their own home as it is difficult to live on rent and

changing homes frequently.

So, we are planning to purchase an apartment which meets with our requirement. The cost

of the property is $480,000 with a deposit of $60000. If we try to use our savings then we

will be left with nothing to meet with the uncertain future and also it is not sufficient to

meet our needs. So, we would like to request you to us loan with the monthly repayment

options for a term of 25 years along with the withdraw facility.

Please find attached all the related documents in regard to the loan application which

involves the primary documents like: Passport, Australian driver licence, Australian learner

permit and the secondary documents like: Australian birth certificate, Australian

citizenship certificate, Medicare card, ATO assessment notice (less than 12 months old)

etc.

I will be very thankful to you.

Thank You.

Ross & Melissa

Financial information

After undertaking the relevant research on the client following information is being

collected.

A

s

s

e

t

s

Details Market value

Cash at bank $15,000

Deposit paid

on property

$60,000

Motor

vehicles: 1.

2.

$15,000

$7,000

Personal effects $30,000

Business value Nil

It is respect fully stated that I am Ross who is living here with wide Melissa in a rented

home and is looking for buying their own home as it is difficult to live on rent and

changing homes frequently.

So, we are planning to purchase an apartment which meets with our requirement. The cost

of the property is $480,000 with a deposit of $60000. If we try to use our savings then we

will be left with nothing to meet with the uncertain future and also it is not sufficient to

meet our needs. So, we would like to request you to us loan with the monthly repayment

options for a term of 25 years along with the withdraw facility.

Please find attached all the related documents in regard to the loan application which

involves the primary documents like: Passport, Australian driver licence, Australian learner

permit and the secondary documents like: Australian birth certificate, Australian

citizenship certificate, Medicare card, ATO assessment notice (less than 12 months old)

etc.

I will be very thankful to you.

Thank You.

Ross & Melissa

Financial information

After undertaking the relevant research on the client following information is being

collected.

A

s

s

e

t

s

Details Market value

Cash at bank $15,000

Deposit paid

on property

$60,000

Motor

vehicles: 1.

2.

$15,000

$7,000

Personal effects $30,000

Business value Nil

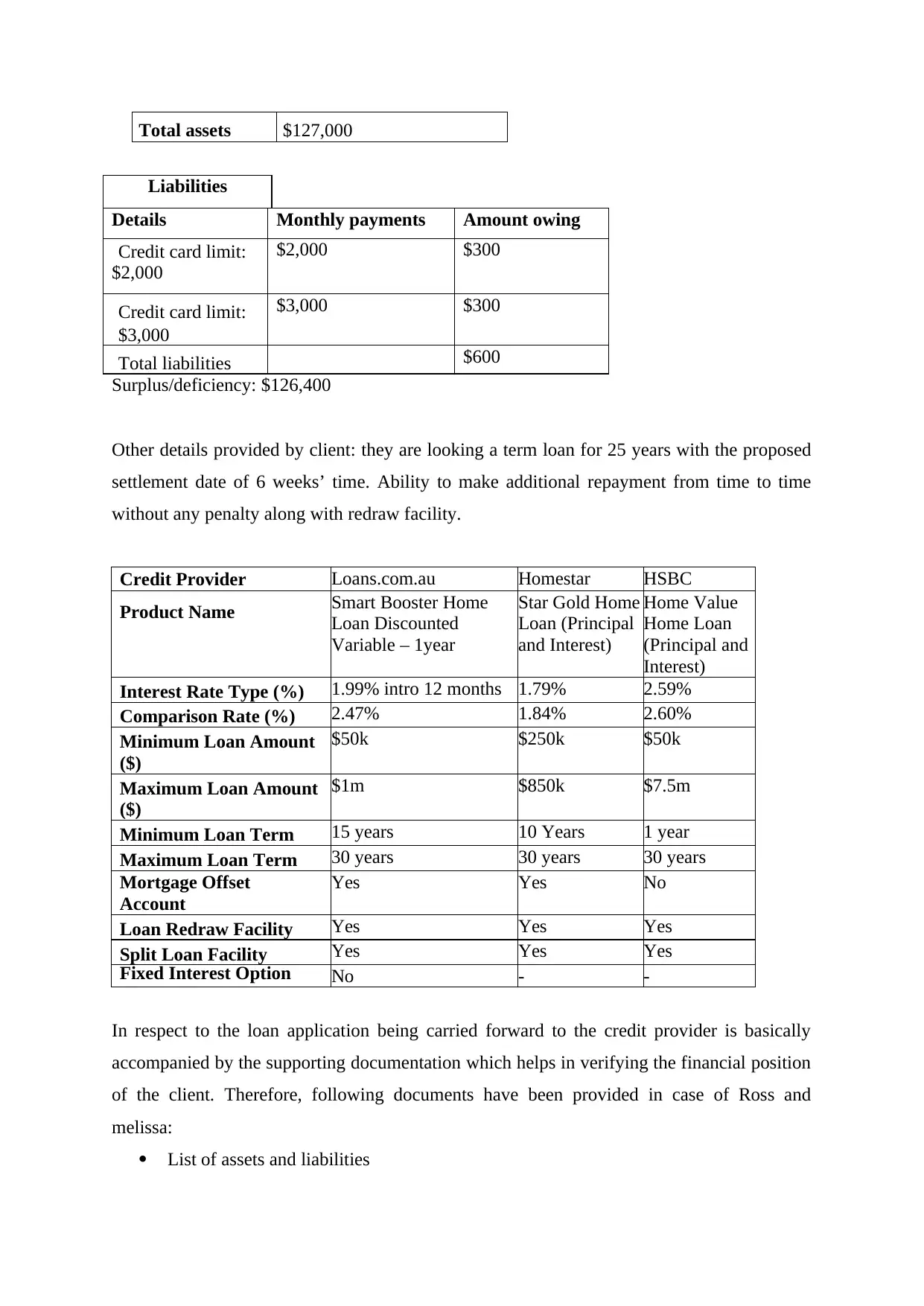

Total assets $127,000

Liabilities

Details Monthly payments Amount owing

Credit card limit:

$2,000

$2,000 $300

Credit card limit:

$3,000

$3,000 $300

Total liabilities $600

Surplus/deficiency: $126,400

Other details provided by client: they are looking a term loan for 25 years with the proposed

settlement date of 6 weeks’ time. Ability to make additional repayment from time to time

without any penalty along with redraw facility.

Credit Provider Loans.com.au Homestar HSBC

Product Name Smart Booster Home

Loan Discounted

Variable – 1year

Star Gold Home

Loan (Principal

and Interest)

Home Value

Home Loan

(Principal and

Interest)

Interest Rate Type (%) 1.99% intro 12 months 1.79% 2.59%

Comparison Rate (%) 2.47% 1.84% 2.60%

Minimum Loan Amount

($)

$50k $250k $50k

Maximum Loan Amount

($)

$1m $850k $7.5m

Minimum Loan Term 15 years 10 Years 1 year

Maximum Loan Term 30 years 30 years 30 years

Mortgage Offset

Account

Yes Yes No

Loan Redraw Facility Yes Yes Yes

Split Loan Facility Yes Yes Yes

Fixed Interest Option No - -

In respect to the loan application being carried forward to the credit provider is basically

accompanied by the supporting documentation which helps in verifying the financial position

of the client. Therefore, following documents have been provided in case of Ross and

melissa:

List of assets and liabilities

Liabilities

Details Monthly payments Amount owing

Credit card limit:

$2,000

$2,000 $300

Credit card limit:

$3,000

$3,000 $300

Total liabilities $600

Surplus/deficiency: $126,400

Other details provided by client: they are looking a term loan for 25 years with the proposed

settlement date of 6 weeks’ time. Ability to make additional repayment from time to time

without any penalty along with redraw facility.

Credit Provider Loans.com.au Homestar HSBC

Product Name Smart Booster Home

Loan Discounted

Variable – 1year

Star Gold Home

Loan (Principal

and Interest)

Home Value

Home Loan

(Principal and

Interest)

Interest Rate Type (%) 1.99% intro 12 months 1.79% 2.59%

Comparison Rate (%) 2.47% 1.84% 2.60%

Minimum Loan Amount

($)

$50k $250k $50k

Maximum Loan Amount

($)

$1m $850k $7.5m

Minimum Loan Term 15 years 10 Years 1 year

Maximum Loan Term 30 years 30 years 30 years

Mortgage Offset

Account

Yes Yes No

Loan Redraw Facility Yes Yes Yes

Split Loan Facility Yes Yes Yes

Fixed Interest Option No - -

In respect to the loan application being carried forward to the credit provider is basically

accompanied by the supporting documentation which helps in verifying the financial position

of the client. Therefore, following documents have been provided in case of Ross and

melissa:

List of assets and liabilities

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Income every year

Number of dependents

Credit history statement

In order to effectively meet with the requirement of the client’s requirements, the above

stated various credit providers were identified with varying interest rate and other conditions.

Also, it is also advised to the clients to effectively make use of their right in respect to the

situation when the lender’s decision on an offer and non-offer (What documents are needed

for a home loan? 2018). The client is having the right to ask for the reason for rejection of

loan and can also ask for the copy of their credit report.

In addition to the above, proper mode of communication is being established which helps in

effectively communicating needs among the clients, lenders along with the other relevant

parties. All the relevant aspects have been covered which has resulted into gathering all the

relevant information accurately and also complies with the lenders guidelines and the

requirements. In addition to this, all the basic requirements of the loan has been fulfilled and

all the documentation has been done efficiently and in a confidential manner.

RESEARCH TASK AND WRITTEN/ORAL QUESTIONS

1.

The different types of forms which is needed to be completed for a loan application is a

completed guarantor or short loan application form, three form IDs like driver license,

passport, Medicare card etc. A signed and dated letter stating the credit history, The

Australian Business Number (ABN), 12 months business activity statement as per the

requirement.

2.

The loan document is witnessed by anyone above the age of 18 and not a party to the loan.

The application is being made online through the way of online portal and the signature

pertaining to the same is received in an online format with e-signature. Therefore, there is no

paper work.

3.

Two of the following original documents are required:

Birth or citizenship certificate

Centrelink pension card

Medicare card

Number of dependents

Credit history statement

In order to effectively meet with the requirement of the client’s requirements, the above

stated various credit providers were identified with varying interest rate and other conditions.

Also, it is also advised to the clients to effectively make use of their right in respect to the

situation when the lender’s decision on an offer and non-offer (What documents are needed

for a home loan? 2018). The client is having the right to ask for the reason for rejection of

loan and can also ask for the copy of their credit report.

In addition to the above, proper mode of communication is being established which helps in

effectively communicating needs among the clients, lenders along with the other relevant

parties. All the relevant aspects have been covered which has resulted into gathering all the

relevant information accurately and also complies with the lenders guidelines and the

requirements. In addition to this, all the basic requirements of the loan has been fulfilled and

all the documentation has been done efficiently and in a confidential manner.

RESEARCH TASK AND WRITTEN/ORAL QUESTIONS

1.

The different types of forms which is needed to be completed for a loan application is a

completed guarantor or short loan application form, three form IDs like driver license,

passport, Medicare card etc. A signed and dated letter stating the credit history, The

Australian Business Number (ABN), 12 months business activity statement as per the

requirement.

2.

The loan document is witnessed by anyone above the age of 18 and not a party to the loan.

The application is being made online through the way of online portal and the signature

pertaining to the same is received in an online format with e-signature. Therefore, there is no

paper work.

3.

Two of the following original documents are required:

Birth or citizenship certificate

Centrelink pension card

Medicare card

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Utilities bill (less than three months old)

Rates notice (less than three months old)

Tax assessment notice (less than 12 months old).

4.

The national credit code is a part of the larger reform process which introduced a licensing

regime for the lenders and brokers which also involves the responsibilities and obligations

like the responsible lending and mandatory membership of the AFCA. It mainly regulates all

the consumers lending involving new loans by non-corporate borrowers.

5.

In order to ensure financial accuracy of the clients in respect to the financial situation, it is

important for the brokers to carry out the effective risk assessment for each of the client. By

looking at the past financial statement of the client or their past debt obligations, credit score

and the level of income based upon which the decision is undertaken whether the financial

position of the client is sound or not.

6.

Depending upon the lender, there are various document which are required to be prepared for

loan application which mainly involves credit report, bank statement, budget and the future

cash flow forecasts, tax return, financial statements etc. However, the more the information,

the client can provide to the lender, more easier it becomes to get it approved.

7.

The basic requirements for loan are:

Type of borrower (age, residency, situation)

Type of employment (PAYG employee, self-employed)

Financial situation (income, expenses, credit score, assets, obligations, deposits)

Reason for loan

Amount of borrowings

8.

The types of interest rates that can be applied to a loan are: nominal interest rate is simply the

interest rate at which interest is computed. Effective interest rate considers compounding over

the full term of the loan. The real interest rate is useful while considering the impact of

inflation over the nominal interest rates.

9.

There are seven stages of loan management which are stated below:

1. Pre-Qualification Process

Rates notice (less than three months old)

Tax assessment notice (less than 12 months old).

4.

The national credit code is a part of the larger reform process which introduced a licensing

regime for the lenders and brokers which also involves the responsibilities and obligations

like the responsible lending and mandatory membership of the AFCA. It mainly regulates all

the consumers lending involving new loans by non-corporate borrowers.

5.

In order to ensure financial accuracy of the clients in respect to the financial situation, it is

important for the brokers to carry out the effective risk assessment for each of the client. By

looking at the past financial statement of the client or their past debt obligations, credit score

and the level of income based upon which the decision is undertaken whether the financial

position of the client is sound or not.

6.

Depending upon the lender, there are various document which are required to be prepared for

loan application which mainly involves credit report, bank statement, budget and the future

cash flow forecasts, tax return, financial statements etc. However, the more the information,

the client can provide to the lender, more easier it becomes to get it approved.

7.

The basic requirements for loan are:

Type of borrower (age, residency, situation)

Type of employment (PAYG employee, self-employed)

Financial situation (income, expenses, credit score, assets, obligations, deposits)

Reason for loan

Amount of borrowings

8.

The types of interest rates that can be applied to a loan are: nominal interest rate is simply the

interest rate at which interest is computed. Effective interest rate considers compounding over

the full term of the loan. The real interest rate is useful while considering the impact of

inflation over the nominal interest rates.

9.

There are seven stages of loan management which are stated below:

1. Pre-Qualification Process

2. Loan Application

3. Application Processing

4. Underwriting Process

5. Credit Decision

6. Quality Check

7. Loan Funding

10.

It is important to maximize the confidentiality of the loan application which can be done

through meeting with the broker about the same, understanding their privacy policy and the

way they hold the data of their clients. In addition to this, understanding what are the key

factors to be accounted for in the process of gathering and storing the information of the

clients. By gaining such crucial information helps in ensuring the data is secured or not.

11.

The client should be provided with the information pertaining to the loan application in

different timeframe as and when different stages are cleared. Along with the expected time

for getting the final result of the loan application and it might take a week or two.

12.

If the loan is rejected, the client is having the right to know the reason for the same. The

client should not apply incessantly which might prove harmful. By law, the client is entitled

to get a free copy of the credit report in case the loan application is rejected.

13.

In the loan and mortgage industry, a good flow of communication is very necessary which

makes a huge difference to the quality of loans processed. The lenders and the loan officers

are needed to encourage interaction with their borrowers in order to avoid any sort of

miscommunication and obstacles in the way.

14.

The additional information that might be required for loan application can be gathered

through, lawyers, accountants, tax department, immigration, past employers etc. The

information mainly involves the proof of the identity, financial situation, proof of residence

and income etc. based upon which the right information pertaining to loan can be given to

clients which meet their needs.

15.

3. Application Processing

4. Underwriting Process

5. Credit Decision

6. Quality Check

7. Loan Funding

10.

It is important to maximize the confidentiality of the loan application which can be done

through meeting with the broker about the same, understanding their privacy policy and the

way they hold the data of their clients. In addition to this, understanding what are the key

factors to be accounted for in the process of gathering and storing the information of the

clients. By gaining such crucial information helps in ensuring the data is secured or not.

11.

The client should be provided with the information pertaining to the loan application in

different timeframe as and when different stages are cleared. Along with the expected time

for getting the final result of the loan application and it might take a week or two.

12.

If the loan is rejected, the client is having the right to know the reason for the same. The

client should not apply incessantly which might prove harmful. By law, the client is entitled

to get a free copy of the credit report in case the loan application is rejected.

13.

In the loan and mortgage industry, a good flow of communication is very necessary which

makes a huge difference to the quality of loans processed. The lenders and the loan officers

are needed to encourage interaction with their borrowers in order to avoid any sort of

miscommunication and obstacles in the way.

14.

The additional information that might be required for loan application can be gathered

through, lawyers, accountants, tax department, immigration, past employers etc. The

information mainly involves the proof of the identity, financial situation, proof of residence

and income etc. based upon which the right information pertaining to loan can be given to

clients which meet their needs.

15.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.