Analyzing Price Elasticity and Total Revenue: GB540 Economics Report

VerifiedAdded on 2022/10/17

|9

|1765

|5

Report

AI Summary

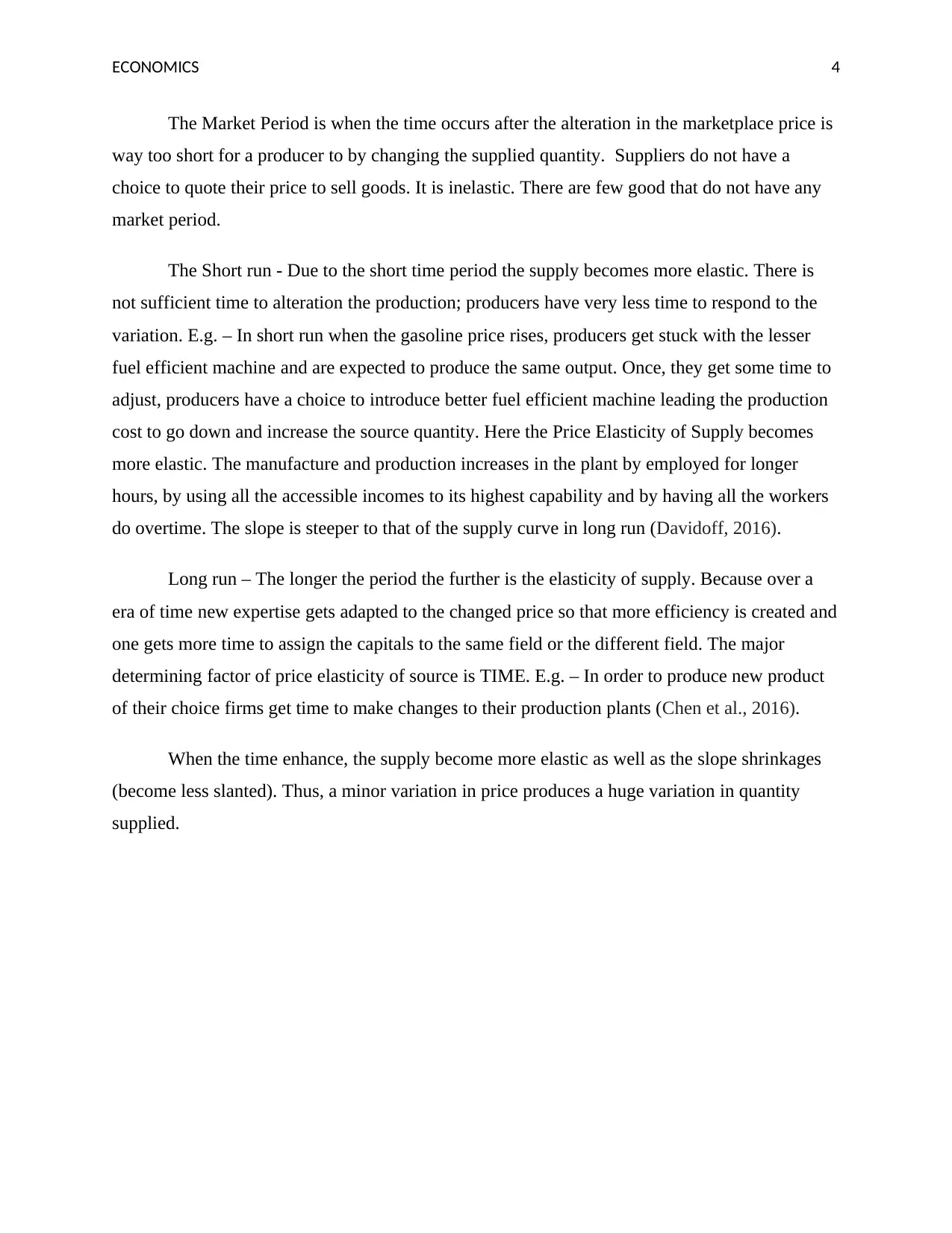

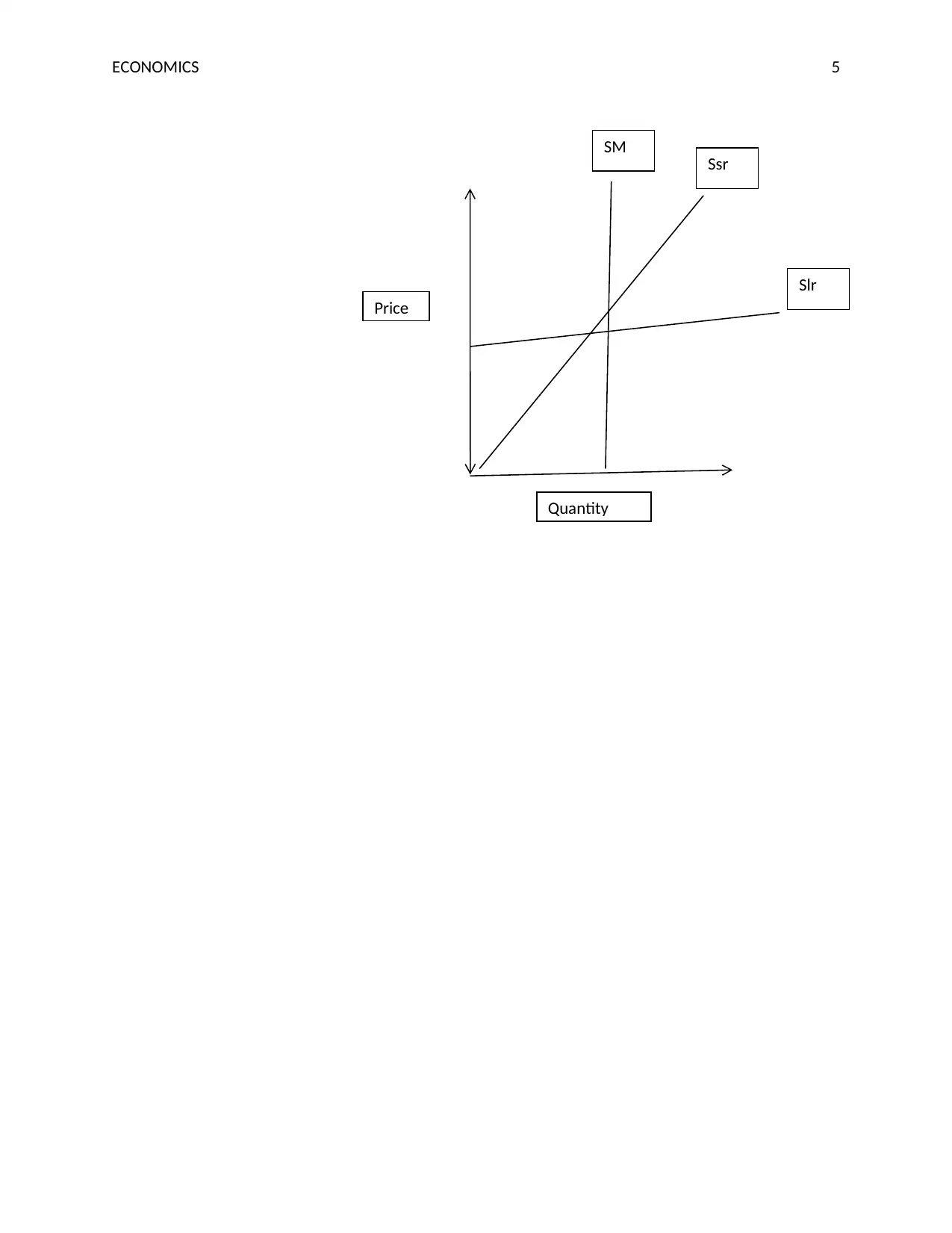

This report examines the relationship between price elasticity of demand and total revenue, crucial concepts in economics. It begins by explaining the laws of demand and supply, and then delves into price elasticity as a quantitative measure of consumer and producer behavior. The report details the connection between price elasticity and total revenue, demonstrating how businesses can use elasticity to optimize pricing strategies and maximize revenue. It discusses the concepts of market period, short run, and long run in supply, highlighting the factors that influence price elasticity of supply. Real-world examples, such as antiques and volatile gold prices, illustrate the practical applications of these economic principles. Furthermore, the report addresses government interventions in the market and their potential impacts on elasticity, including subsidies and price controls. Overall, the assignment provides a comprehensive analysis of these core economic concepts, supported by relevant references.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.