Financial Reporting Analysis: Primax Electronics Ltd Performance

VerifiedAdded on 2020/11/12

|17

|3408

|97

Report

AI Summary

This report provides a detailed financial reporting analysis, beginning with an introduction to financial reporting's purpose and context, including regulatory and conceptual frameworks, and identifying stakeholders and their benefits. The report explores the importance of financial reporting for organizational growth and objectives, followed by a reflection on financial statements, including the statement of profit and loss, changes in equity, and financial position, along with a comparison of cash flow with financial position and income statements. The report analyzes and interprets the financial performance of Primax Electronics Ltd using profitability, liquidity, solvency, efficiency, and investment ratios for the years 2016 and 2017. The differences between IFRS and IAS are also discussed, along with the advantages of IFRS and factors impacting compliance. The report concludes with a summary of the findings and provides references.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

1. Outlining the purpose and context of financial reporting.......................................................1

2. Explaining regulatory and conceptual framework with its purpose, key principles and

qualitative characteristics............................................................................................................1

3. Determining stakeholders with their benefit through financial information...........................3

4. Importance of financial reporting for accomplishing organizational growth and objectives. 4

5. Reflecting financial statements...............................................................................................5

a. Statement of Profit and loss....................................................................................................5

6. Explaining and interpreting financial performance of Primax Electronics Ltd......................8

7. Difference among IFRS and IAS..........................................................................................10

8. Evaluating advantages of IFRS.............................................................................................10

9. Identifying degree of compliance with context of IFRS along with factors which impact

compliance................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

1. Outlining the purpose and context of financial reporting.......................................................1

2. Explaining regulatory and conceptual framework with its purpose, key principles and

qualitative characteristics............................................................................................................1

3. Determining stakeholders with their benefit through financial information...........................3

4. Importance of financial reporting for accomplishing organizational growth and objectives. 4

5. Reflecting financial statements...............................................................................................5

a. Statement of Profit and loss....................................................................................................5

6. Explaining and interpreting financial performance of Primax Electronics Ltd......................8

7. Difference among IFRS and IAS..........................................................................................10

8. Evaluating advantages of IFRS.............................................................................................10

9. Identifying degree of compliance with context of IFRS along with factors which impact

compliance................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Financial reporting is disclosure of financial outcome and information to stakeholders

and management. It gives vital information on basis of financial activities and health of

organization to its stakeholders such as potential investors, government regulators, shareholders

and consumers. The present report will give brief discussion with reference to conceptual and

regulatory framework and interpreting financial performance of Primax Electronics Limited.

1. Outlining the purpose and context of financial reporting

Financial reporting are referred as records and documents which are collaborated for

tracking and reviewing about money to make business. The main objective of financial reporting

is to delivering information about share owners and lenders of business. It is a contributing as

essential contract among business as investors and lenders will be gaining right to know about

money spent or not. In the present economy, financial reporting has very huge role and

contributes to corporate governance. It serves for two primary objective as it provides help to

management for involving in effective decision making concerning to objectives of business

entity along with overall strategies. There will be appropriate disclosure in reports for helping

management to discern with its weaknesses and strength of business entity and overall health as

well.

In the similar aspect it is referred as mode for purpose of ensuring that business is

operating in efficient manner or not. In case, company is traded publicly then it is subject for

multiple strict regulations as they are enforced through Securities and exchange Commission. In

order for acquiring needs of users of its financial statements, organizations have to implement

system of accounting for giving the required information. It is very important for regulated

system for purpose of ensuring required information to its particular users in specific format. It is

very useful on basis of informational requirement as it is attained via framework of financial

reporting on basis of conceptual framework (Chen, Zhang and Zhou, 2018).

2. Explaining regulatory and conceptual framework with its purpose, key principles and

qualitative characteristics

The auditors, shareholders and directors are referred as main party with context of

traditional corporate model. The regulatory framework helps in setting regulations and rules for

accounting and at international level, IAS board provides very wide regulatory framework on

basis of International accounting standards. It will directly imply to each European listed

1

Financial reporting is disclosure of financial outcome and information to stakeholders

and management. It gives vital information on basis of financial activities and health of

organization to its stakeholders such as potential investors, government regulators, shareholders

and consumers. The present report will give brief discussion with reference to conceptual and

regulatory framework and interpreting financial performance of Primax Electronics Limited.

1. Outlining the purpose and context of financial reporting

Financial reporting are referred as records and documents which are collaborated for

tracking and reviewing about money to make business. The main objective of financial reporting

is to delivering information about share owners and lenders of business. It is a contributing as

essential contract among business as investors and lenders will be gaining right to know about

money spent or not. In the present economy, financial reporting has very huge role and

contributes to corporate governance. It serves for two primary objective as it provides help to

management for involving in effective decision making concerning to objectives of business

entity along with overall strategies. There will be appropriate disclosure in reports for helping

management to discern with its weaknesses and strength of business entity and overall health as

well.

In the similar aspect it is referred as mode for purpose of ensuring that business is

operating in efficient manner or not. In case, company is traded publicly then it is subject for

multiple strict regulations as they are enforced through Securities and exchange Commission. In

order for acquiring needs of users of its financial statements, organizations have to implement

system of accounting for giving the required information. It is very important for regulated

system for purpose of ensuring required information to its particular users in specific format. It is

very useful on basis of informational requirement as it is attained via framework of financial

reporting on basis of conceptual framework (Chen, Zhang and Zhou, 2018).

2. Explaining regulatory and conceptual framework with its purpose, key principles and

qualitative characteristics

The auditors, shareholders and directors are referred as main party with context of

traditional corporate model. The regulatory framework helps in setting regulations and rules for

accounting and at international level, IAS board provides very wide regulatory framework on

basis of International accounting standards. It will directly imply to each European listed

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organization especially companies of UK as there are two main sources such as accounting

standards and Companies act. The International accounting standards has directly issued

conceptual framework along with sets of financial reporting concepts as it sets out its objective,

describing reporting entity and with its boundary whereas qualitative characteristics of useful

financial information. This would be defining liability, asset, income, expenses and equity. The

criteria for considering liabilities and asset in recognition or financial statements and guidance

for ridding de-recognition. This will be measuring guidance and bases with the application along

with guidance and concepts on disclosure and presentation. Its principles are stated below:

Information given through financial statements must be reliable and relevant where its

choice exists among approaches which are relevant and reliable which is mutually

exclusive.

If information has capability for purpose of influencing economic decisions of users is

given on time for influencing those decisions.

It could be reliable as it is dependent on users for representing it faithfully and shows

substance of transactions along with other undertaken events.

Information could be comparable, understandable although it must be included in

financial statements in simple manner with its users (Amiram and et.al., 2018).

2

standards and Companies act. The International accounting standards has directly issued

conceptual framework along with sets of financial reporting concepts as it sets out its objective,

describing reporting entity and with its boundary whereas qualitative characteristics of useful

financial information. This would be defining liability, asset, income, expenses and equity. The

criteria for considering liabilities and asset in recognition or financial statements and guidance

for ridding de-recognition. This will be measuring guidance and bases with the application along

with guidance and concepts on disclosure and presentation. Its principles are stated below:

Information given through financial statements must be reliable and relevant where its

choice exists among approaches which are relevant and reliable which is mutually

exclusive.

If information has capability for purpose of influencing economic decisions of users is

given on time for influencing those decisions.

It could be reliable as it is dependent on users for representing it faithfully and shows

substance of transactions along with other undertaken events.

Information could be comparable, understandable although it must be included in

financial statements in simple manner with its users (Amiram and et.al., 2018).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

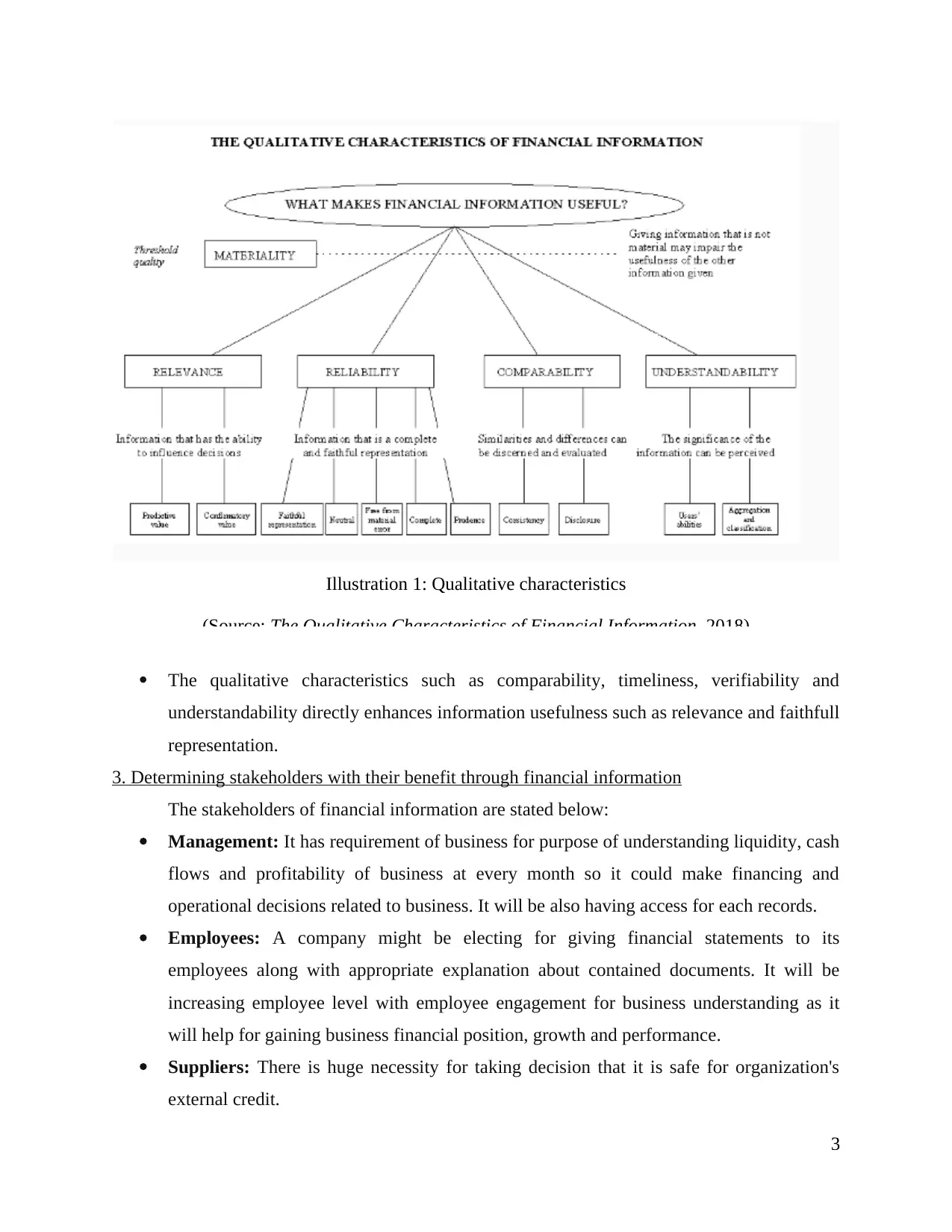

Illustration 1: Qualitative characteristics

(Source: The Qualitative Characteristics of Financial Information, 2018)

The qualitative characteristics such as comparability, timeliness, verifiability and

understandability directly enhances information usefulness such as relevance and faithfull

representation.

3. Determining stakeholders with their benefit through financial information

The stakeholders of financial information are stated below:

Management: It has requirement of business for purpose of understanding liquidity, cash

flows and profitability of business at every month so it could make financing and

operational decisions related to business. It will be also having access for each records.

Employees: A company might be electing for giving financial statements to its

employees along with appropriate explanation about contained documents. It will be

increasing employee level with employee engagement for business understanding as it

will help for gaining business financial position, growth and performance.

Suppliers: There is huge necessity for taking decision that it is safe for organization's

external credit.

3

(Source: The Qualitative Characteristics of Financial Information, 2018)

The qualitative characteristics such as comparability, timeliness, verifiability and

understandability directly enhances information usefulness such as relevance and faithfull

representation.

3. Determining stakeholders with their benefit through financial information

The stakeholders of financial information are stated below:

Management: It has requirement of business for purpose of understanding liquidity, cash

flows and profitability of business at every month so it could make financing and

operational decisions related to business. It will be also having access for each records.

Employees: A company might be electing for giving financial statements to its

employees along with appropriate explanation about contained documents. It will be

increasing employee level with employee engagement for business understanding as it

will help for gaining business financial position, growth and performance.

Suppliers: There is huge necessity for taking decision that it is safe for organization's

external credit.

3

Owners: The main objective of owners in financial statements is for assessing returns on

investment with its appearance for future. Generally, owners will get access to all

financial files and records.

Competitors: The organizations which are giving competition as business would be

attempting for gaining access to financial statements of its rivals for purpose of

evaluating financial position. It could be used for crafting necessary competitive

strategies.

Government: In which authority of organization is situated with request of financial

statements for identifying that payments related to business is right amount of taxes along

with adherence to relevant laws.

Creditors: Any organization for purpose of loaning money in business entity with need

of financial statements for estimating ability of borrower for paying back each loaned

funds on basis of charges related to interest expense (Users of Financial Statements,

2018).

4. Importance of financial reporting for accomplishing organizational growth and objectives

Financial reporting is valuable sources for informed decision making among the business

entity as it must be part of analytic strategy of company. Through leveraging financial reporting

and analysis must be directly integrated with solution of business management as it will be

capable for purpose of consolidating whole financial data in each location and subsidiaries,

drilling in its details and for extracting holistic view of data with objective of optimal financial

planning of business entity. This is huge requirement through law with tax perspective as

government uses report for ensuring about paying fair share of taxes. The business entities would

be using various management dashboards. In this aspect, the requirements of governments for

creation of documents has gathered whole industry of auditing firm as KPMG, PWC, Ernst &

Young and Deloitte which exist independently for purpose of reviewing financial reports where

process of auditing is legal requirement (Mayangsari, Murwaningsari and Lastanti, 2018).

During consideration of investing money in organization which will seem with

information to know about operation of business entity. It will be useful for investors as it

applies for banks and credit vendors with banks for purpose of considering company's lending

money. It is also mandatory for multiple stakeholders for owning firm's equity with appropriate

disclosure of liabilities and assets, cash cost and revenue of business entity. It serves as bedrock

4

investment with its appearance for future. Generally, owners will get access to all

financial files and records.

Competitors: The organizations which are giving competition as business would be

attempting for gaining access to financial statements of its rivals for purpose of

evaluating financial position. It could be used for crafting necessary competitive

strategies.

Government: In which authority of organization is situated with request of financial

statements for identifying that payments related to business is right amount of taxes along

with adherence to relevant laws.

Creditors: Any organization for purpose of loaning money in business entity with need

of financial statements for estimating ability of borrower for paying back each loaned

funds on basis of charges related to interest expense (Users of Financial Statements,

2018).

4. Importance of financial reporting for accomplishing organizational growth and objectives

Financial reporting is valuable sources for informed decision making among the business

entity as it must be part of analytic strategy of company. Through leveraging financial reporting

and analysis must be directly integrated with solution of business management as it will be

capable for purpose of consolidating whole financial data in each location and subsidiaries,

drilling in its details and for extracting holistic view of data with objective of optimal financial

planning of business entity. This is huge requirement through law with tax perspective as

government uses report for ensuring about paying fair share of taxes. The business entities would

be using various management dashboards. In this aspect, the requirements of governments for

creation of documents has gathered whole industry of auditing firm as KPMG, PWC, Ernst &

Young and Deloitte which exist independently for purpose of reviewing financial reports where

process of auditing is legal requirement (Mayangsari, Murwaningsari and Lastanti, 2018).

During consideration of investing money in organization which will seem with

information to know about operation of business entity. It will be useful for investors as it

applies for banks and credit vendors with banks for purpose of considering company's lending

money. It is also mandatory for multiple stakeholders for owning firm's equity with appropriate

disclosure of liabilities and assets, cash cost and revenue of business entity. It serves as bedrock

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

for other reports which should and can used for undertaking decisions. It is very crucial that

financial reports are highly accurate with its high possibility due to other management reports

based for ensuring decision. In this context, companies could trouble for using legacy method for

preparing financial reports and to observe benefits with use of financial dashboards.

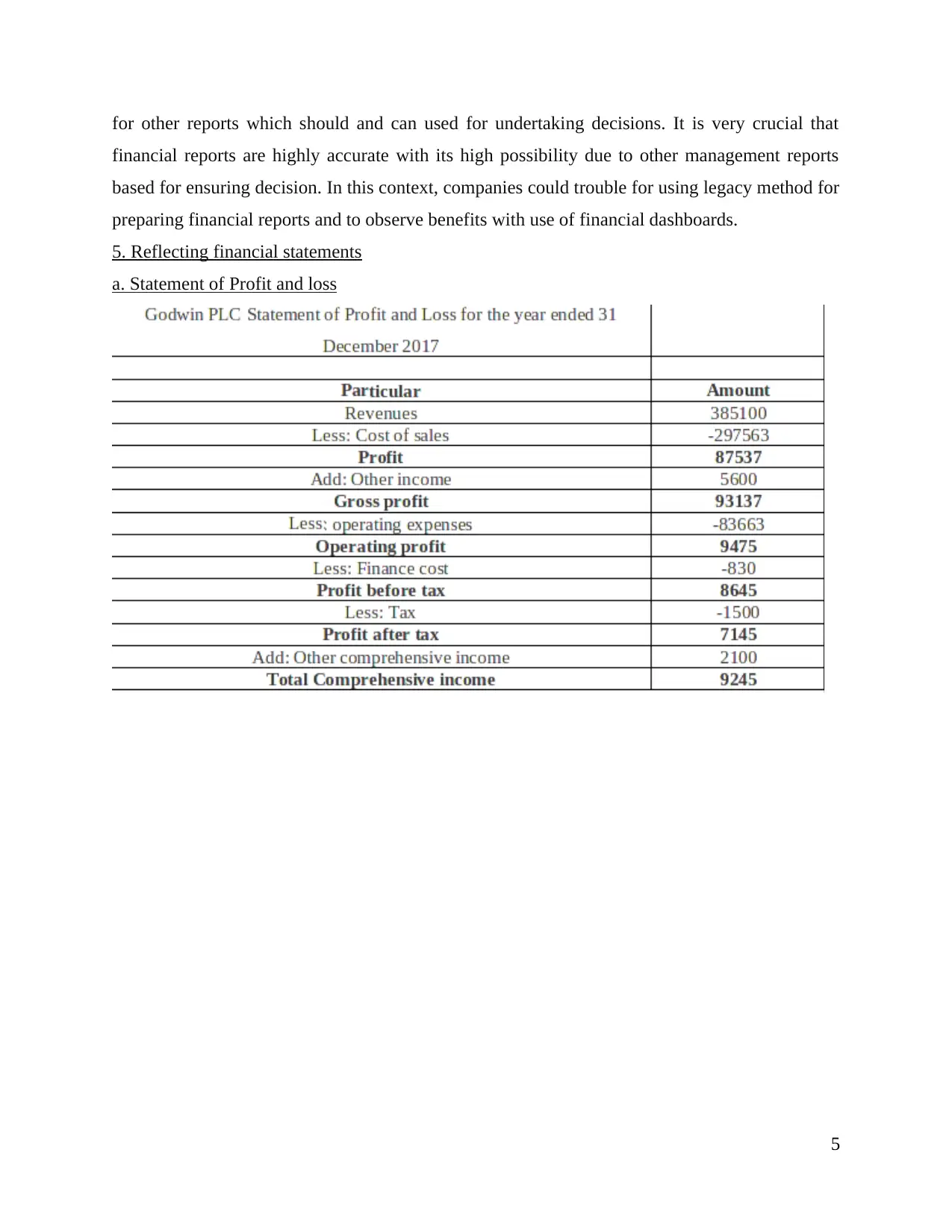

5. Reflecting financial statements

a. Statement of Profit and loss

5

financial reports are highly accurate with its high possibility due to other management reports

based for ensuring decision. In this context, companies could trouble for using legacy method for

preparing financial reports and to observe benefits with use of financial dashboards.

5. Reflecting financial statements

a. Statement of Profit and loss

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

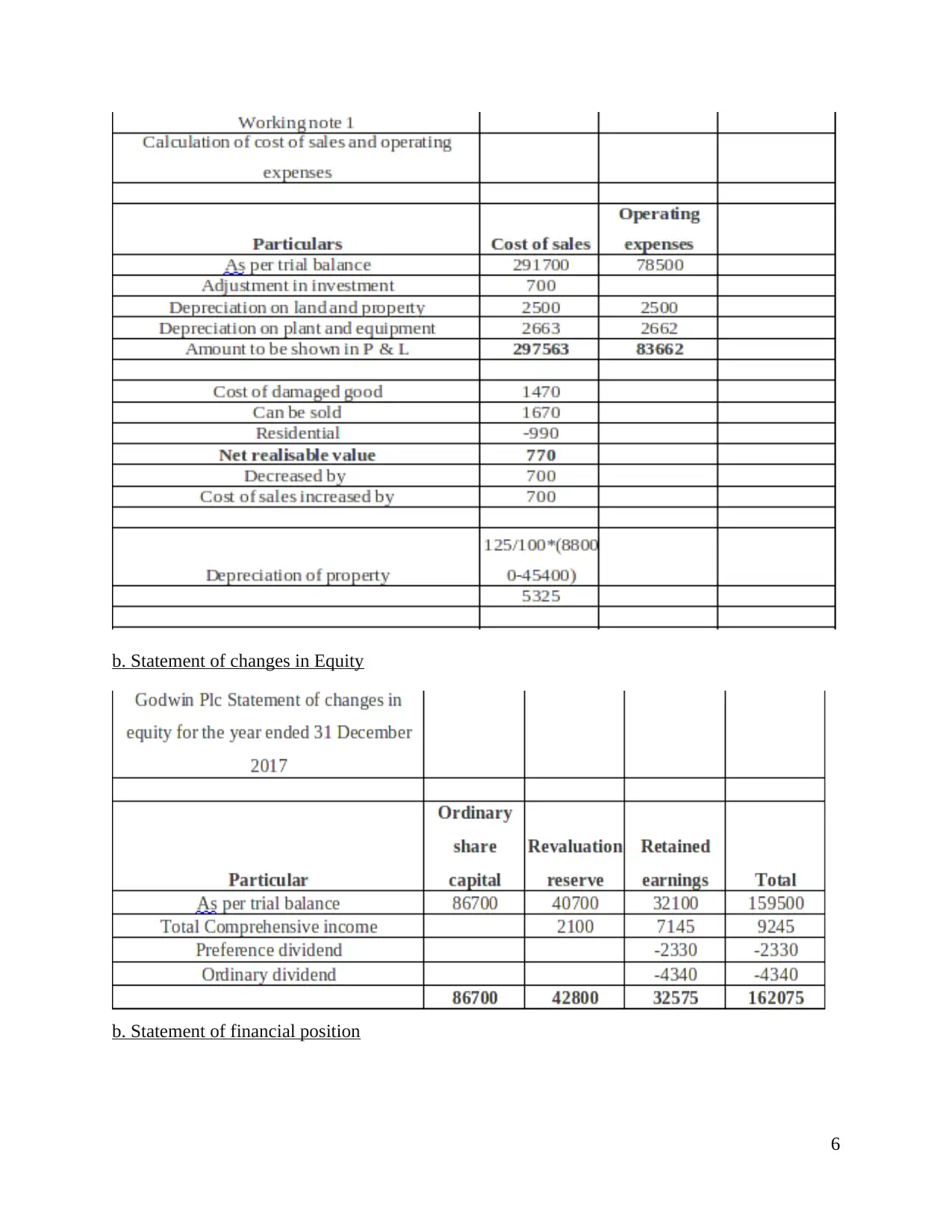

b. Statement of changes in Equity

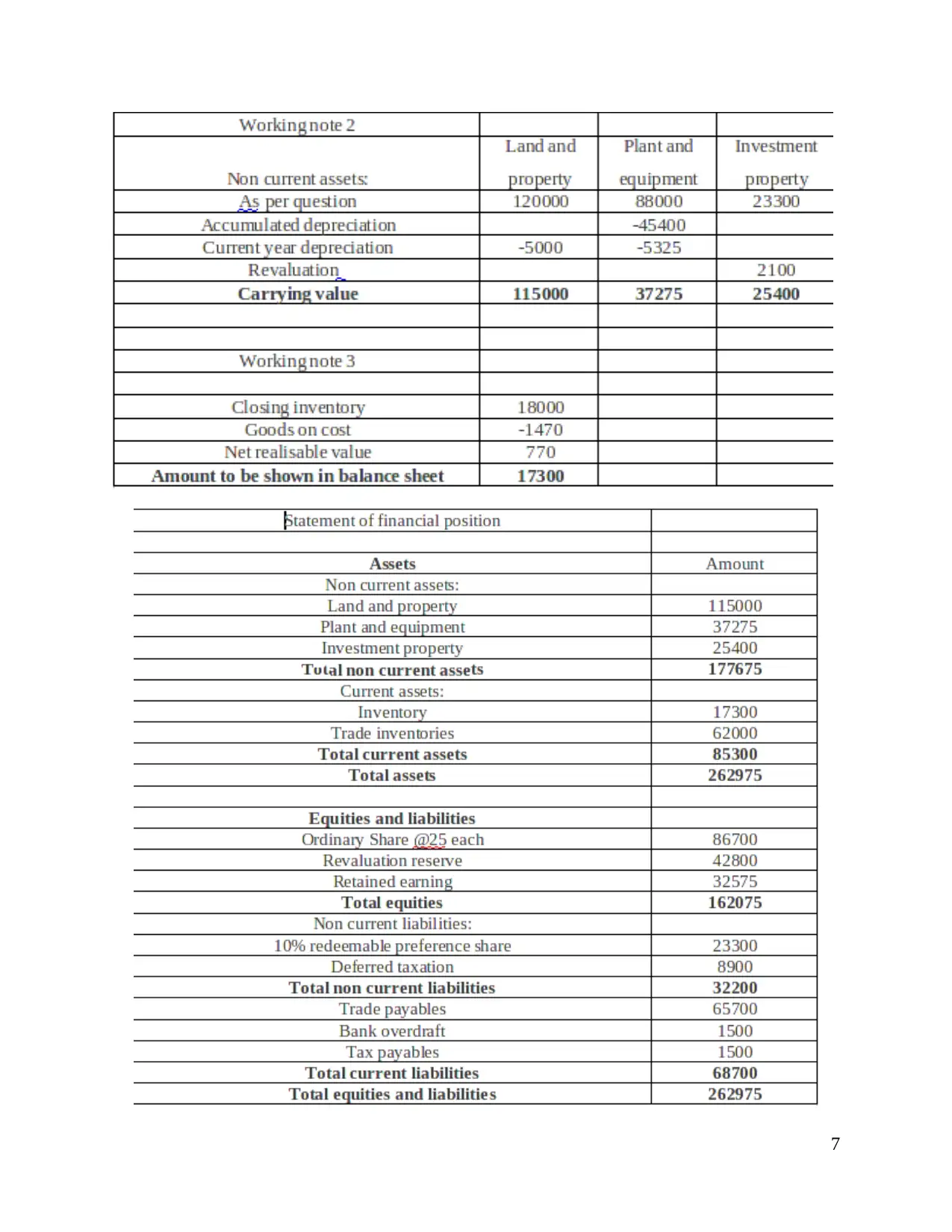

b. Statement of financial position

6

b. Statement of financial position

6

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

d. Difference in cash flow with financial position and income statement

Cash flow statement reflects about cash position of business entity whereas profit and

loss statement represents information related to income and expenses. Simultaneously, financial

position statements shows assets and liabilities belongs to organization.

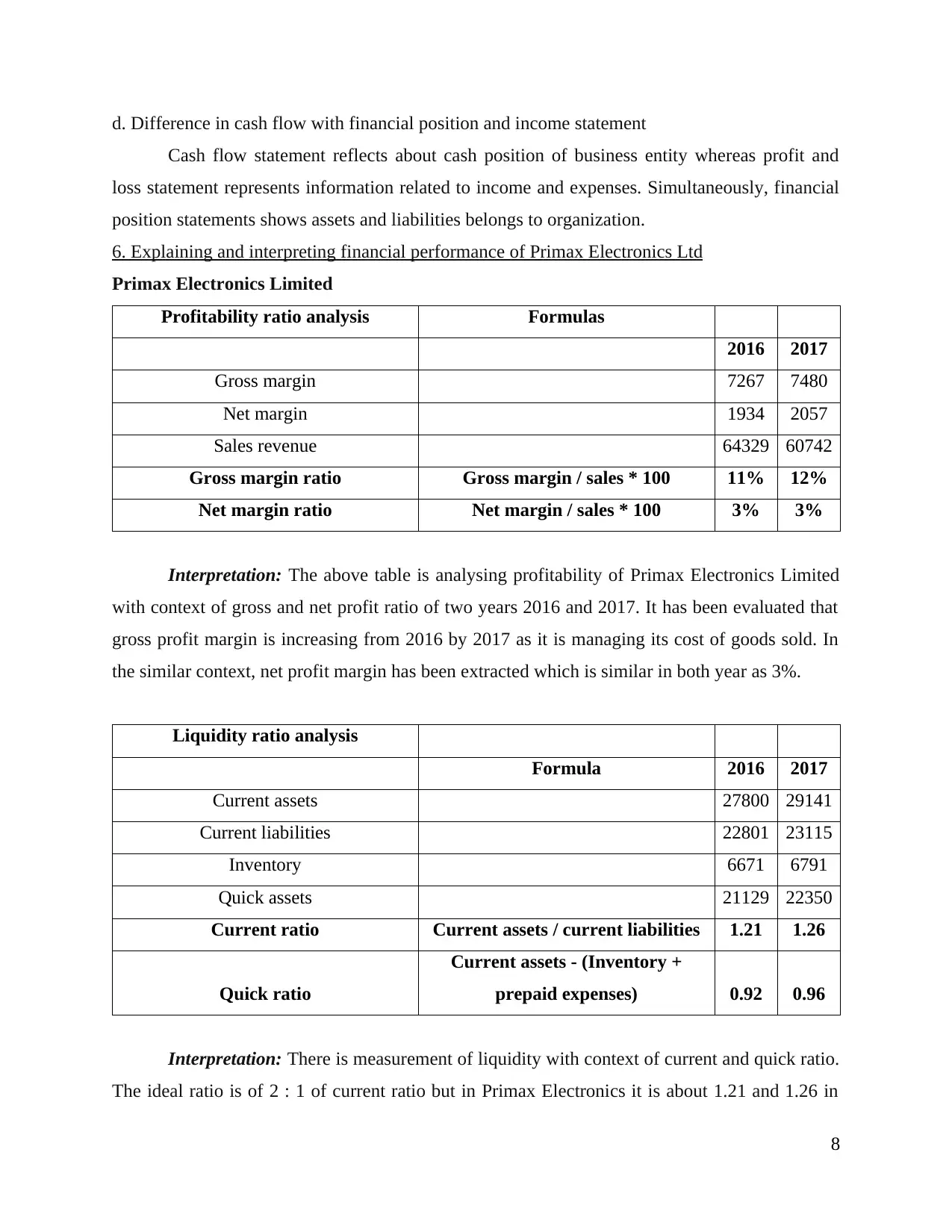

6. Explaining and interpreting financial performance of Primax Electronics Ltd

Primax Electronics Limited

Profitability ratio analysis Formulas

2016 2017

Gross margin 7267 7480

Net margin 1934 2057

Sales revenue 64329 60742

Gross margin ratio Gross margin / sales * 100 11% 12%

Net margin ratio Net margin / sales * 100 3% 3%

Interpretation: The above table is analysing profitability of Primax Electronics Limited

with context of gross and net profit ratio of two years 2016 and 2017. It has been evaluated that

gross profit margin is increasing from 2016 by 2017 as it is managing its cost of goods sold. In

the similar context, net profit margin has been extracted which is similar in both year as 3%.

Liquidity ratio analysis

Formula 2016 2017

Current assets 27800 29141

Current liabilities 22801 23115

Inventory 6671 6791

Quick assets 21129 22350

Current ratio Current assets / current liabilities 1.21 1.26

Quick ratio

Current assets - (Inventory +

prepaid expenses) 0.92 0.96

Interpretation: There is measurement of liquidity with context of current and quick ratio.

The ideal ratio is of 2 : 1 of current ratio but in Primax Electronics it is about 1.21 and 1.26 in

8

Cash flow statement reflects about cash position of business entity whereas profit and

loss statement represents information related to income and expenses. Simultaneously, financial

position statements shows assets and liabilities belongs to organization.

6. Explaining and interpreting financial performance of Primax Electronics Ltd

Primax Electronics Limited

Profitability ratio analysis Formulas

2016 2017

Gross margin 7267 7480

Net margin 1934 2057

Sales revenue 64329 60742

Gross margin ratio Gross margin / sales * 100 11% 12%

Net margin ratio Net margin / sales * 100 3% 3%

Interpretation: The above table is analysing profitability of Primax Electronics Limited

with context of gross and net profit ratio of two years 2016 and 2017. It has been evaluated that

gross profit margin is increasing from 2016 by 2017 as it is managing its cost of goods sold. In

the similar context, net profit margin has been extracted which is similar in both year as 3%.

Liquidity ratio analysis

Formula 2016 2017

Current assets 27800 29141

Current liabilities 22801 23115

Inventory 6671 6791

Quick assets 21129 22350

Current ratio Current assets / current liabilities 1.21 1.26

Quick ratio

Current assets - (Inventory +

prepaid expenses) 0.92 0.96

Interpretation: There is measurement of liquidity with context of current and quick ratio.

The ideal ratio is of 2 : 1 of current ratio but in Primax Electronics it is about 1.21 and 1.26 in

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

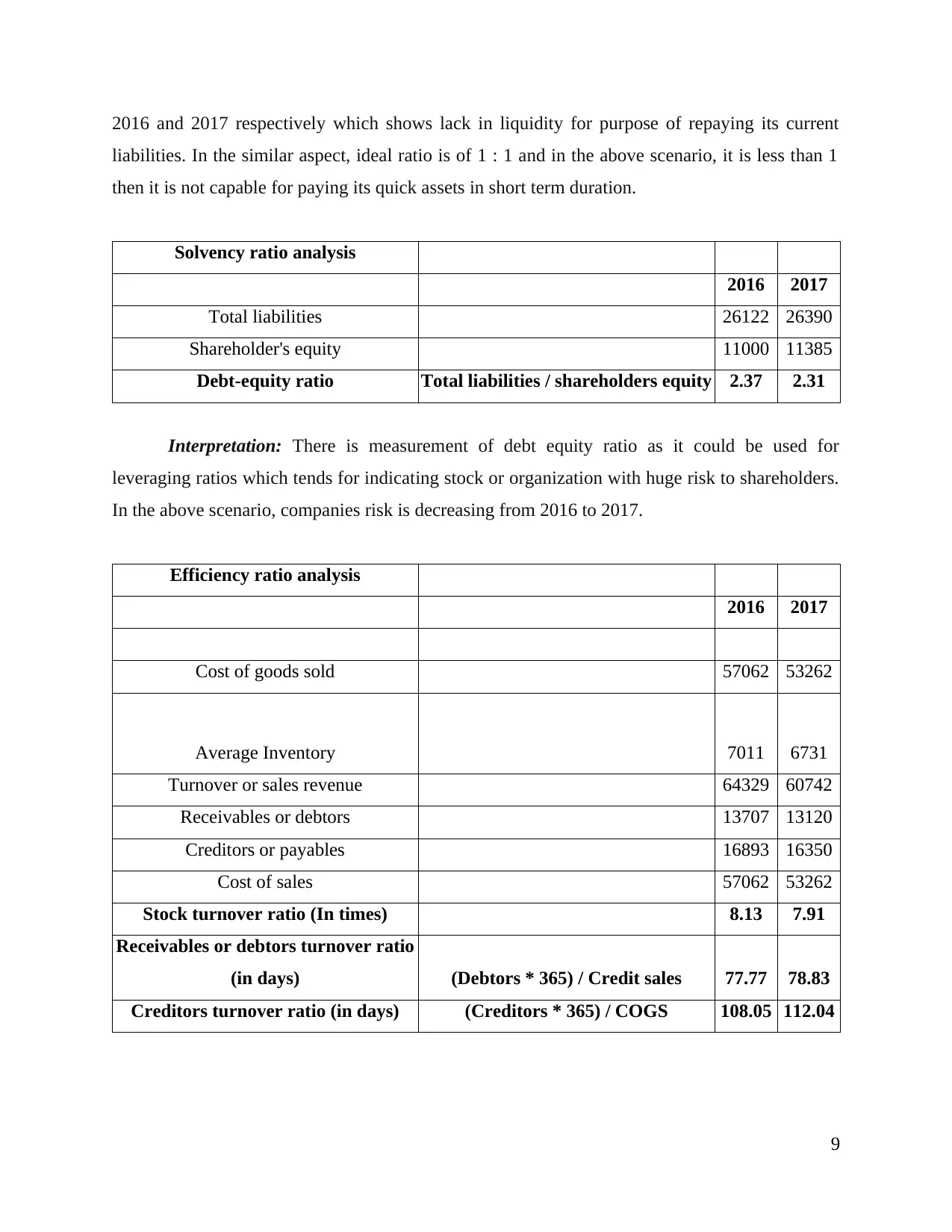

2016 and 2017 respectively which shows lack in liquidity for purpose of repaying its current

liabilities. In the similar aspect, ideal ratio is of 1 : 1 and in the above scenario, it is less than 1

then it is not capable for paying its quick assets in short term duration.

Solvency ratio analysis

2016 2017

Total liabilities 26122 26390

Shareholder's equity 11000 11385

Debt-equity ratio Total liabilities / shareholders equity 2.37 2.31

Interpretation: There is measurement of debt equity ratio as it could be used for

leveraging ratios which tends for indicating stock or organization with huge risk to shareholders.

In the above scenario, companies risk is decreasing from 2016 to 2017.

Efficiency ratio analysis

2016 2017

Cost of goods sold 57062 53262

Average Inventory 7011 6731

Turnover or sales revenue 64329 60742

Receivables or debtors 13707 13120

Creditors or payables 16893 16350

Cost of sales 57062 53262

Stock turnover ratio (In times) 8.13 7.91

Receivables or debtors turnover ratio

(in days) (Debtors * 365) / Credit sales 77.77 78.83

Creditors turnover ratio (in days) (Creditors * 365) / COGS 108.05 112.04

9

liabilities. In the similar aspect, ideal ratio is of 1 : 1 and in the above scenario, it is less than 1

then it is not capable for paying its quick assets in short term duration.

Solvency ratio analysis

2016 2017

Total liabilities 26122 26390

Shareholder's equity 11000 11385

Debt-equity ratio Total liabilities / shareholders equity 2.37 2.31

Interpretation: There is measurement of debt equity ratio as it could be used for

leveraging ratios which tends for indicating stock or organization with huge risk to shareholders.

In the above scenario, companies risk is decreasing from 2016 to 2017.

Efficiency ratio analysis

2016 2017

Cost of goods sold 57062 53262

Average Inventory 7011 6731

Turnover or sales revenue 64329 60742

Receivables or debtors 13707 13120

Creditors or payables 16893 16350

Cost of sales 57062 53262

Stock turnover ratio (In times) 8.13 7.91

Receivables or debtors turnover ratio

(in days) (Debtors * 365) / Credit sales 77.77 78.83

Creditors turnover ratio (in days) (Creditors * 365) / COGS 108.05 112.04

9

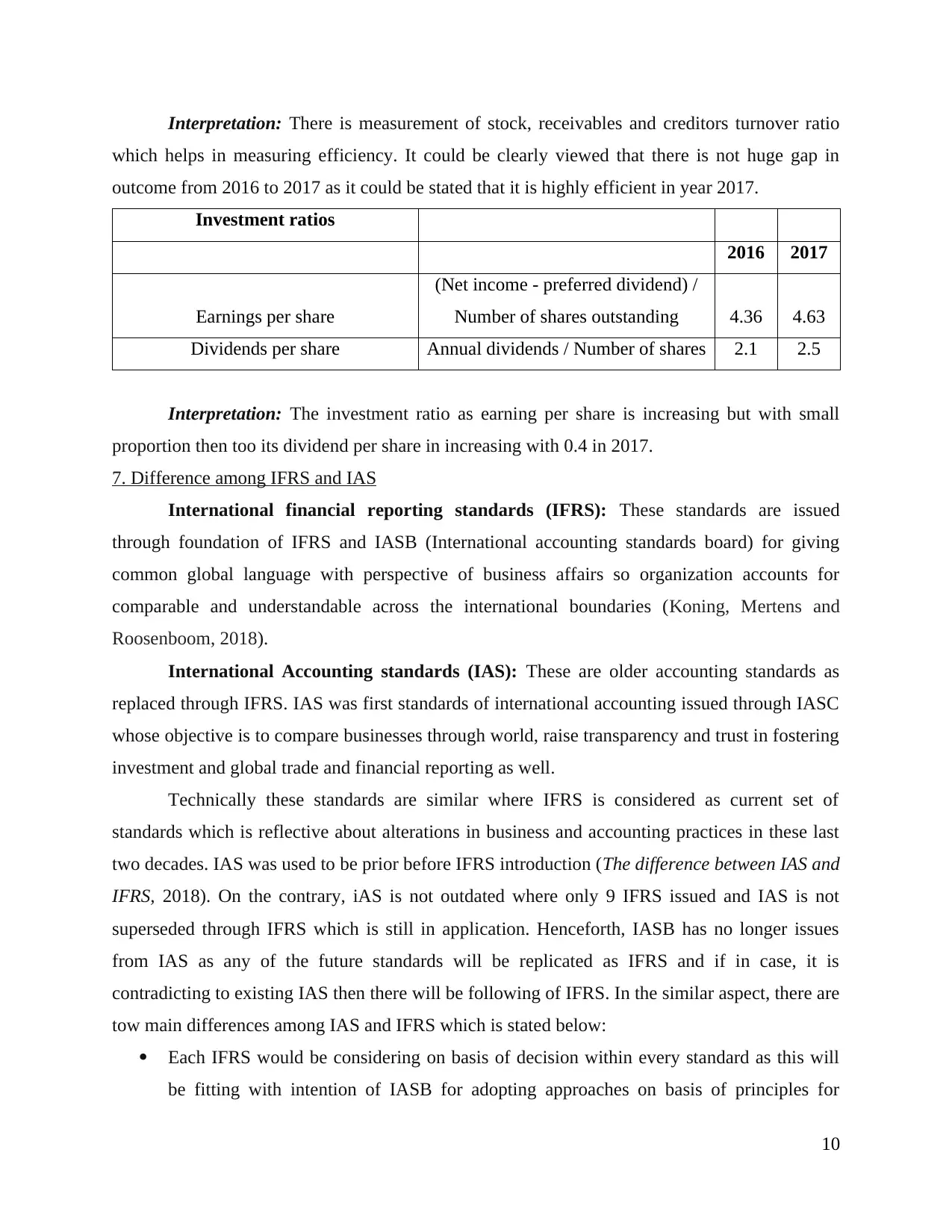

Interpretation: There is measurement of stock, receivables and creditors turnover ratio

which helps in measuring efficiency. It could be clearly viewed that there is not huge gap in

outcome from 2016 to 2017 as it could be stated that it is highly efficient in year 2017.

Investment ratios

2016 2017

Earnings per share

(Net income - preferred dividend) /

Number of shares outstanding 4.36 4.63

Dividends per share Annual dividends / Number of shares 2.1 2.5

Interpretation: The investment ratio as earning per share is increasing but with small

proportion then too its dividend per share in increasing with 0.4 in 2017.

7. Difference among IFRS and IAS

International financial reporting standards (IFRS): These standards are issued

through foundation of IFRS and IASB (International accounting standards board) for giving

common global language with perspective of business affairs so organization accounts for

comparable and understandable across the international boundaries (Koning, Mertens and

Roosenboom, 2018).

International Accounting standards (IAS): These are older accounting standards as

replaced through IFRS. IAS was first standards of international accounting issued through IASC

whose objective is to compare businesses through world, raise transparency and trust in fostering

investment and global trade and financial reporting as well.

Technically these standards are similar where IFRS is considered as current set of

standards which is reflective about alterations in business and accounting practices in these last

two decades. IAS was used to be prior before IFRS introduction (The difference between IAS and

IFRS, 2018). On the contrary, iAS is not outdated where only 9 IFRS issued and IAS is not

superseded through IFRS which is still in application. Henceforth, IASB has no longer issues

from IAS as any of the future standards will be replicated as IFRS and if in case, it is

contradicting to existing IAS then there will be following of IFRS. In the similar aspect, there are

tow main differences among IAS and IFRS which is stated below:

Each IFRS would be considering on basis of decision within every standard as this will

be fitting with intention of IASB for adopting approaches on basis of principles for

10

which helps in measuring efficiency. It could be clearly viewed that there is not huge gap in

outcome from 2016 to 2017 as it could be stated that it is highly efficient in year 2017.

Investment ratios

2016 2017

Earnings per share

(Net income - preferred dividend) /

Number of shares outstanding 4.36 4.63

Dividends per share Annual dividends / Number of shares 2.1 2.5

Interpretation: The investment ratio as earning per share is increasing but with small

proportion then too its dividend per share in increasing with 0.4 in 2017.

7. Difference among IFRS and IAS

International financial reporting standards (IFRS): These standards are issued

through foundation of IFRS and IASB (International accounting standards board) for giving

common global language with perspective of business affairs so organization accounts for

comparable and understandable across the international boundaries (Koning, Mertens and

Roosenboom, 2018).

International Accounting standards (IAS): These are older accounting standards as

replaced through IFRS. IAS was first standards of international accounting issued through IASC

whose objective is to compare businesses through world, raise transparency and trust in fostering

investment and global trade and financial reporting as well.

Technically these standards are similar where IFRS is considered as current set of

standards which is reflective about alterations in business and accounting practices in these last

two decades. IAS was used to be prior before IFRS introduction (The difference between IAS and

IFRS, 2018). On the contrary, iAS is not outdated where only 9 IFRS issued and IAS is not

superseded through IFRS which is still in application. Henceforth, IASB has no longer issues

from IAS as any of the future standards will be replicated as IFRS and if in case, it is

contradicting to existing IAS then there will be following of IFRS. In the similar aspect, there are

tow main differences among IAS and IFRS which is stated below:

Each IFRS would be considering on basis of decision within every standard as this will

be fitting with intention of IASB for adopting approaches on basis of principles for

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.