Solution: ECOM058 Principles of Accounting Online Exam, 2020

VerifiedAdded on 2022/11/29

|13

|2595

|496

Homework Assignment

AI Summary

This document presents a comprehensive solution to an accounting exam, addressing key concepts and practical applications. It begins with an adjusted trial balance for the year ending December 31, 2020, including detailed workings for depreciation calculations and provisions. The solution then delves into inventory valuation using both FIFO and LIFO methods, providing step-by-step calculations for cost of goods sold and closing inventory. A cash flow statement is constructed, analyzing operating, investing, and financing activities. Furthermore, the document includes a financial ratio analysis, comparing liquidity and solvency ratios for 2019 and 2020. Finally, it differentiates between accounting concepts, accounting standards, and accounting policies, clarifying their roles in financial reporting.

ECOM058 PRINCIPLES OF

ACCOUNTING ONLINE

EXAM

ACCOUNTING ONLINE

EXAM

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION- 1.................................................................................................................................1

Adjusted trial balance as at 31st December, 2020.......................................................................1

QUESTION- 2.................................................................................................................................2

a) Inventory valuation by FIFO method......................................................................................2

b) Inventory valuation by LIFO method......................................................................................3

c) Cost of goods sold and closing inventory are different in FIFO and LIFO methods..............5

QUESTION 3...................................................................................................................................6

QUESTION 4...................................................................................................................................9

REFERENCES..............................................................................................................................11

QUESTION- 1.................................................................................................................................1

Adjusted trial balance as at 31st December, 2020.......................................................................1

QUESTION- 2.................................................................................................................................2

a) Inventory valuation by FIFO method......................................................................................2

b) Inventory valuation by LIFO method......................................................................................3

c) Cost of goods sold and closing inventory are different in FIFO and LIFO methods..............5

QUESTION 3...................................................................................................................................6

QUESTION 4...................................................................................................................................9

REFERENCES..............................................................................................................................11

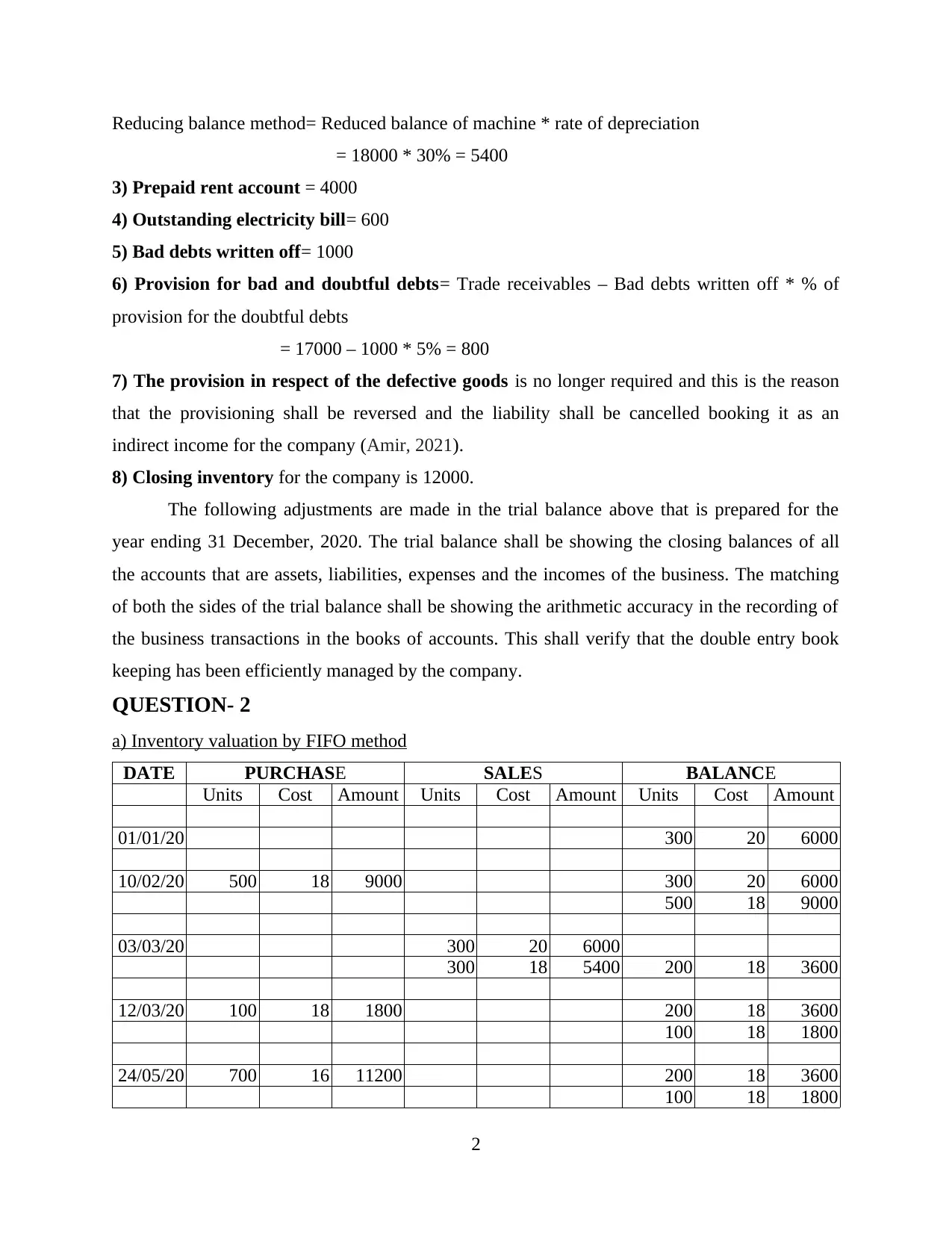

QUESTION- 1

Adjusted trial balance as at 31st December, 2020

S.NO PARTICULARS DEBIT CREDIT

1 Share Capital 30000

2 Cash 16000

3 Trade Receivables 16000

4 Building at cost 65000

5 Accumulated depreciation on building 40000

6 Sales Return 2000

7 Inventory 12000

8 Retained profits 32500

9 Discount received 1500

10 Provision for bad and doubtful debts 800

11 Purchase 35000

12 Sales 76000

13 Rent 13000

14 Prepaid Rent 6000

15 Electricity 4500

16 Electricity outstanding 600

17 Machinery 30000

18 Accumulated depreciation on machinery 17400

19 Bad debts written off 1000

20 Indirect income 2000

21 provision expenses 300

200800 200800

Working Note:-

1) Depreciation on building based on the straight line method:-

Building at cost= 65000

Residual value= 15000

Useful life= 25 years

Straight line method= Cost – Residual value / Useful life

= 65000 – 15000 / 25

= 2000

2) Depreciation on machinery based on the reducing balance method:-

Machinery at cost= 30000

Accumulated depreciation= 12000

Reduced value of machine= 30000 – 12000= 18000

1

Adjusted trial balance as at 31st December, 2020

S.NO PARTICULARS DEBIT CREDIT

1 Share Capital 30000

2 Cash 16000

3 Trade Receivables 16000

4 Building at cost 65000

5 Accumulated depreciation on building 40000

6 Sales Return 2000

7 Inventory 12000

8 Retained profits 32500

9 Discount received 1500

10 Provision for bad and doubtful debts 800

11 Purchase 35000

12 Sales 76000

13 Rent 13000

14 Prepaid Rent 6000

15 Electricity 4500

16 Electricity outstanding 600

17 Machinery 30000

18 Accumulated depreciation on machinery 17400

19 Bad debts written off 1000

20 Indirect income 2000

21 provision expenses 300

200800 200800

Working Note:-

1) Depreciation on building based on the straight line method:-

Building at cost= 65000

Residual value= 15000

Useful life= 25 years

Straight line method= Cost – Residual value / Useful life

= 65000 – 15000 / 25

= 2000

2) Depreciation on machinery based on the reducing balance method:-

Machinery at cost= 30000

Accumulated depreciation= 12000

Reduced value of machine= 30000 – 12000= 18000

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reducing balance method= Reduced balance of machine * rate of depreciation

= 18000 * 30% = 5400

3) Prepaid rent account = 4000

4) Outstanding electricity bill= 600

5) Bad debts written off= 1000

6) Provision for bad and doubtful debts= Trade receivables – Bad debts written off * % of

provision for the doubtful debts

= 17000 – 1000 * 5% = 800

7) The provision in respect of the defective goods is no longer required and this is the reason

that the provisioning shall be reversed and the liability shall be cancelled booking it as an

indirect income for the company (Amir, 2021).

8) Closing inventory for the company is 12000.

The following adjustments are made in the trial balance above that is prepared for the

year ending 31 December, 2020. The trial balance shall be showing the closing balances of all

the accounts that are assets, liabilities, expenses and the incomes of the business. The matching

of both the sides of the trial balance shall be showing the arithmetic accuracy in the recording of

the business transactions in the books of accounts. This shall verify that the double entry book

keeping has been efficiently managed by the company.

QUESTION- 2

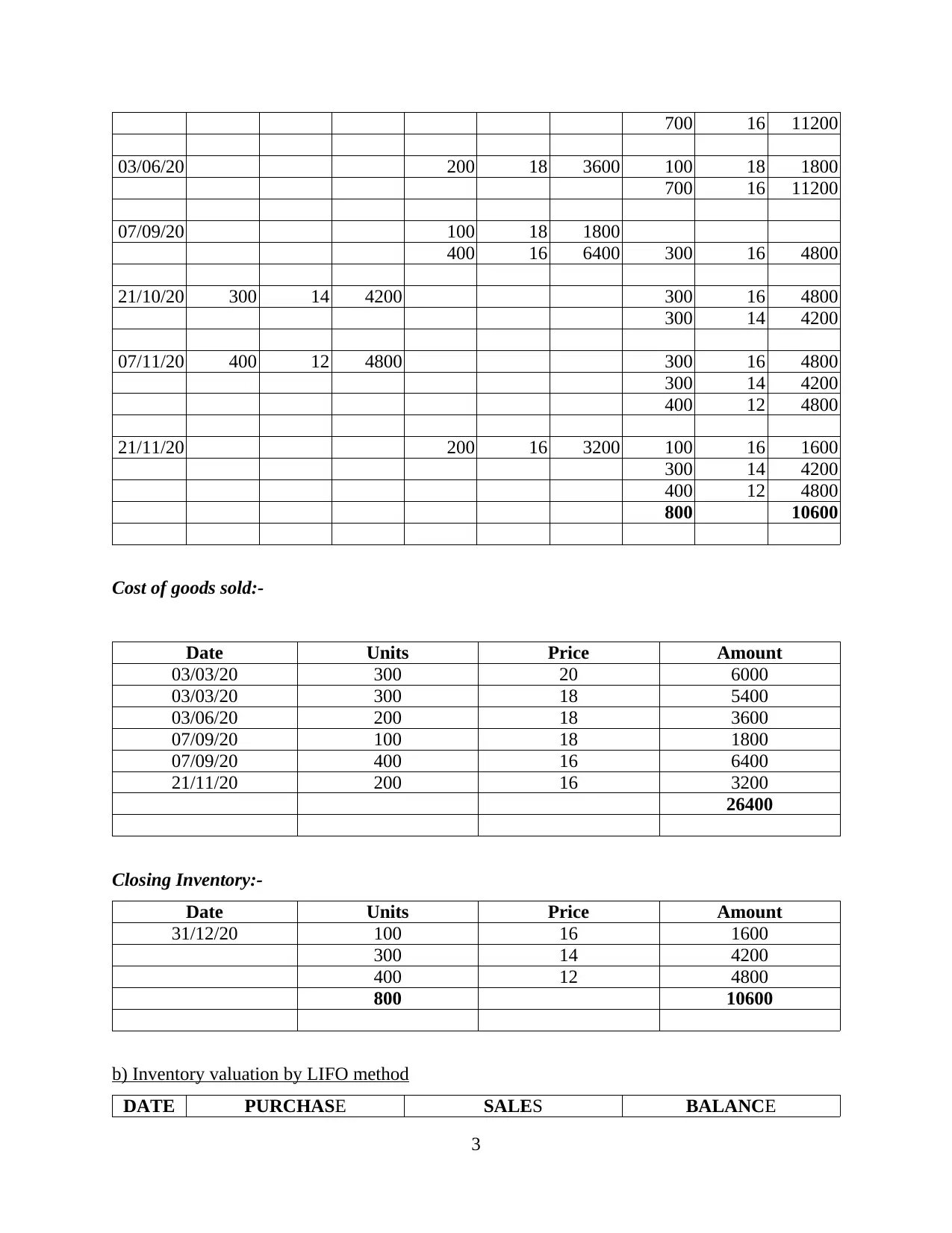

a) Inventory valuation by FIFO method

DATE PURCHASE SALES BALANCE

Units Cost Amount Units Cost Amount Units Cost Amount

01/01/20 300 20 6000

10/02/20 500 18 9000 300 20 6000

500 18 9000

03/03/20 300 20 6000

300 18 5400 200 18 3600

12/03/20 100 18 1800 200 18 3600

100 18 1800

24/05/20 700 16 11200 200 18 3600

100 18 1800

2

= 18000 * 30% = 5400

3) Prepaid rent account = 4000

4) Outstanding electricity bill= 600

5) Bad debts written off= 1000

6) Provision for bad and doubtful debts= Trade receivables – Bad debts written off * % of

provision for the doubtful debts

= 17000 – 1000 * 5% = 800

7) The provision in respect of the defective goods is no longer required and this is the reason

that the provisioning shall be reversed and the liability shall be cancelled booking it as an

indirect income for the company (Amir, 2021).

8) Closing inventory for the company is 12000.

The following adjustments are made in the trial balance above that is prepared for the

year ending 31 December, 2020. The trial balance shall be showing the closing balances of all

the accounts that are assets, liabilities, expenses and the incomes of the business. The matching

of both the sides of the trial balance shall be showing the arithmetic accuracy in the recording of

the business transactions in the books of accounts. This shall verify that the double entry book

keeping has been efficiently managed by the company.

QUESTION- 2

a) Inventory valuation by FIFO method

DATE PURCHASE SALES BALANCE

Units Cost Amount Units Cost Amount Units Cost Amount

01/01/20 300 20 6000

10/02/20 500 18 9000 300 20 6000

500 18 9000

03/03/20 300 20 6000

300 18 5400 200 18 3600

12/03/20 100 18 1800 200 18 3600

100 18 1800

24/05/20 700 16 11200 200 18 3600

100 18 1800

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

700 16 11200

03/06/20 200 18 3600 100 18 1800

700 16 11200

07/09/20 100 18 1800

400 16 6400 300 16 4800

21/10/20 300 14 4200 300 16 4800

300 14 4200

07/11/20 400 12 4800 300 16 4800

300 14 4200

400 12 4800

21/11/20 200 16 3200 100 16 1600

300 14 4200

400 12 4800

800 10600

Cost of goods sold:-

Date Units Price Amount

03/03/20 300 20 6000

03/03/20 300 18 5400

03/06/20 200 18 3600

07/09/20 100 18 1800

07/09/20 400 16 6400

21/11/20 200 16 3200

26400

Closing Inventory:-

Date Units Price Amount

31/12/20 100 16 1600

300 14 4200

400 12 4800

800 10600

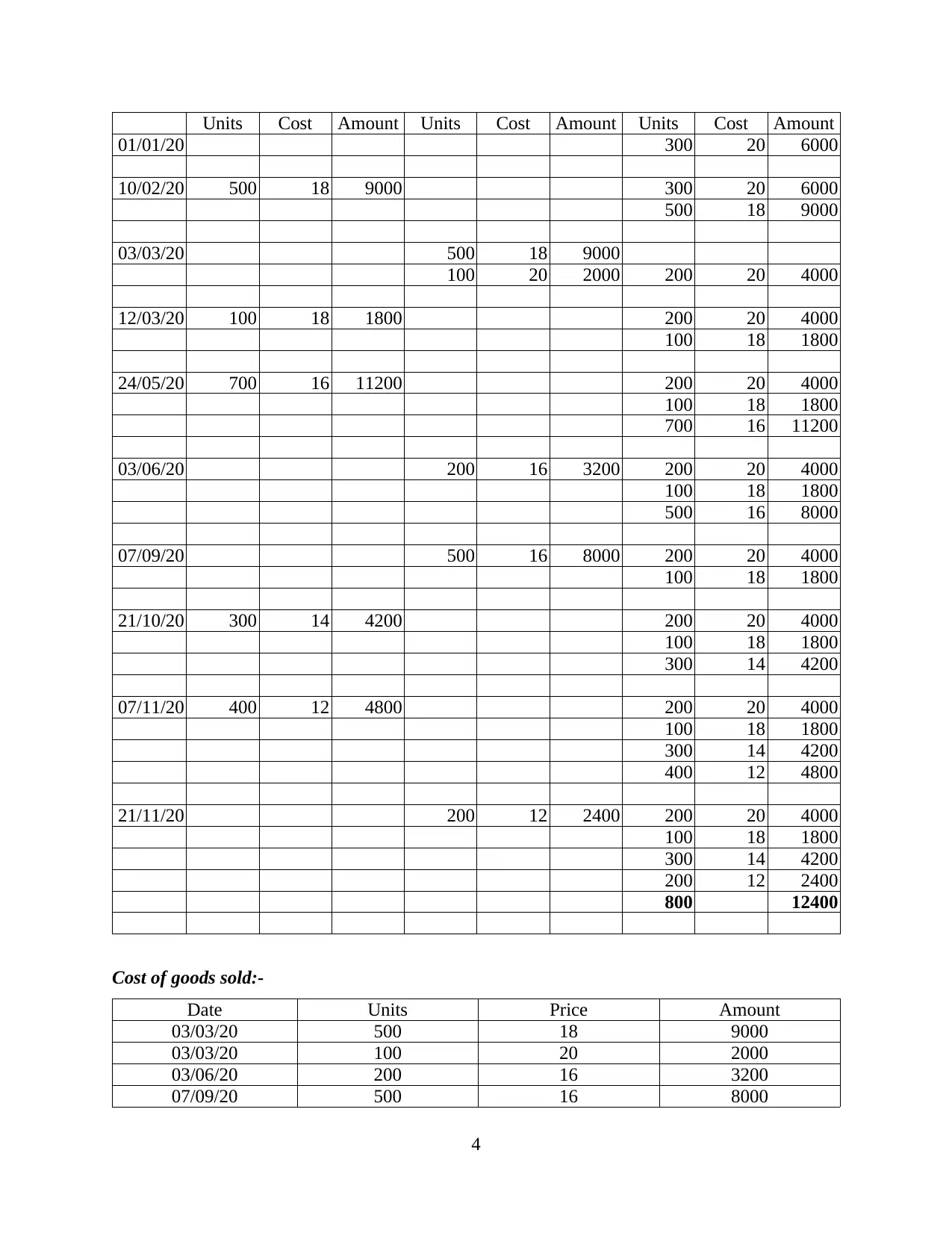

b) Inventory valuation by LIFO method

DATE PURCHASE SALES BALANCE

3

03/06/20 200 18 3600 100 18 1800

700 16 11200

07/09/20 100 18 1800

400 16 6400 300 16 4800

21/10/20 300 14 4200 300 16 4800

300 14 4200

07/11/20 400 12 4800 300 16 4800

300 14 4200

400 12 4800

21/11/20 200 16 3200 100 16 1600

300 14 4200

400 12 4800

800 10600

Cost of goods sold:-

Date Units Price Amount

03/03/20 300 20 6000

03/03/20 300 18 5400

03/06/20 200 18 3600

07/09/20 100 18 1800

07/09/20 400 16 6400

21/11/20 200 16 3200

26400

Closing Inventory:-

Date Units Price Amount

31/12/20 100 16 1600

300 14 4200

400 12 4800

800 10600

b) Inventory valuation by LIFO method

DATE PURCHASE SALES BALANCE

3

Units Cost Amount Units Cost Amount Units Cost Amount

01/01/20 300 20 6000

10/02/20 500 18 9000 300 20 6000

500 18 9000

03/03/20 500 18 9000

100 20 2000 200 20 4000

12/03/20 100 18 1800 200 20 4000

100 18 1800

24/05/20 700 16 11200 200 20 4000

100 18 1800

700 16 11200

03/06/20 200 16 3200 200 20 4000

100 18 1800

500 16 8000

07/09/20 500 16 8000 200 20 4000

100 18 1800

21/10/20 300 14 4200 200 20 4000

100 18 1800

300 14 4200

07/11/20 400 12 4800 200 20 4000

100 18 1800

300 14 4200

400 12 4800

21/11/20 200 12 2400 200 20 4000

100 18 1800

300 14 4200

200 12 2400

800 12400

Cost of goods sold:-

Date Units Price Amount

03/03/20 500 18 9000

03/03/20 100 20 2000

03/06/20 200 16 3200

07/09/20 500 16 8000

4

01/01/20 300 20 6000

10/02/20 500 18 9000 300 20 6000

500 18 9000

03/03/20 500 18 9000

100 20 2000 200 20 4000

12/03/20 100 18 1800 200 20 4000

100 18 1800

24/05/20 700 16 11200 200 20 4000

100 18 1800

700 16 11200

03/06/20 200 16 3200 200 20 4000

100 18 1800

500 16 8000

07/09/20 500 16 8000 200 20 4000

100 18 1800

21/10/20 300 14 4200 200 20 4000

100 18 1800

300 14 4200

07/11/20 400 12 4800 200 20 4000

100 18 1800

300 14 4200

400 12 4800

21/11/20 200 12 2400 200 20 4000

100 18 1800

300 14 4200

200 12 2400

800 12400

Cost of goods sold:-

Date Units Price Amount

03/03/20 500 18 9000

03/03/20 100 20 2000

03/06/20 200 16 3200

07/09/20 500 16 8000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

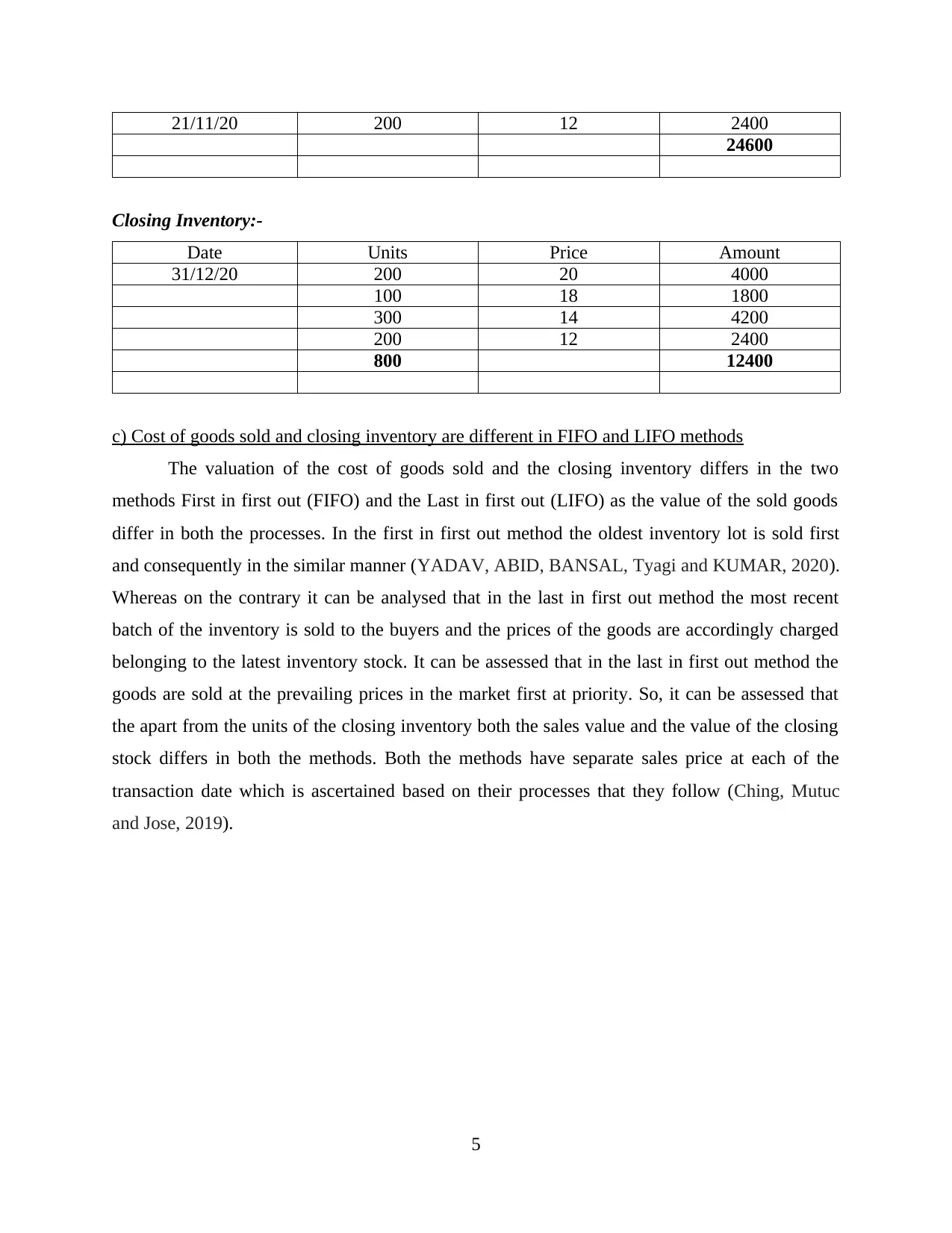

21/11/20 200 12 2400

24600

Closing Inventory:-

Date Units Price Amount

31/12/20 200 20 4000

100 18 1800

300 14 4200

200 12 2400

800 12400

c) Cost of goods sold and closing inventory are different in FIFO and LIFO methods

The valuation of the cost of goods sold and the closing inventory differs in the two

methods First in first out (FIFO) and the Last in first out (LIFO) as the value of the sold goods

differ in both the processes. In the first in first out method the oldest inventory lot is sold first

and consequently in the similar manner (YADAV, ABID, BANSAL, Tyagi and KUMAR, 2020).

Whereas on the contrary it can be analysed that in the last in first out method the most recent

batch of the inventory is sold to the buyers and the prices of the goods are accordingly charged

belonging to the latest inventory stock. It can be assessed that in the last in first out method the

goods are sold at the prevailing prices in the market first at priority. So, it can be assessed that

the apart from the units of the closing inventory both the sales value and the value of the closing

stock differs in both the methods. Both the methods have separate sales price at each of the

transaction date which is ascertained based on their processes that they follow (Ching, Mutuc

and Jose, 2019).

5

24600

Closing Inventory:-

Date Units Price Amount

31/12/20 200 20 4000

100 18 1800

300 14 4200

200 12 2400

800 12400

c) Cost of goods sold and closing inventory are different in FIFO and LIFO methods

The valuation of the cost of goods sold and the closing inventory differs in the two

methods First in first out (FIFO) and the Last in first out (LIFO) as the value of the sold goods

differ in both the processes. In the first in first out method the oldest inventory lot is sold first

and consequently in the similar manner (YADAV, ABID, BANSAL, Tyagi and KUMAR, 2020).

Whereas on the contrary it can be analysed that in the last in first out method the most recent

batch of the inventory is sold to the buyers and the prices of the goods are accordingly charged

belonging to the latest inventory stock. It can be assessed that in the last in first out method the

goods are sold at the prevailing prices in the market first at priority. So, it can be assessed that

the apart from the units of the closing inventory both the sales value and the value of the closing

stock differs in both the methods. Both the methods have separate sales price at each of the

transaction date which is ascertained based on their processes that they follow (Ching, Mutuc

and Jose, 2019).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

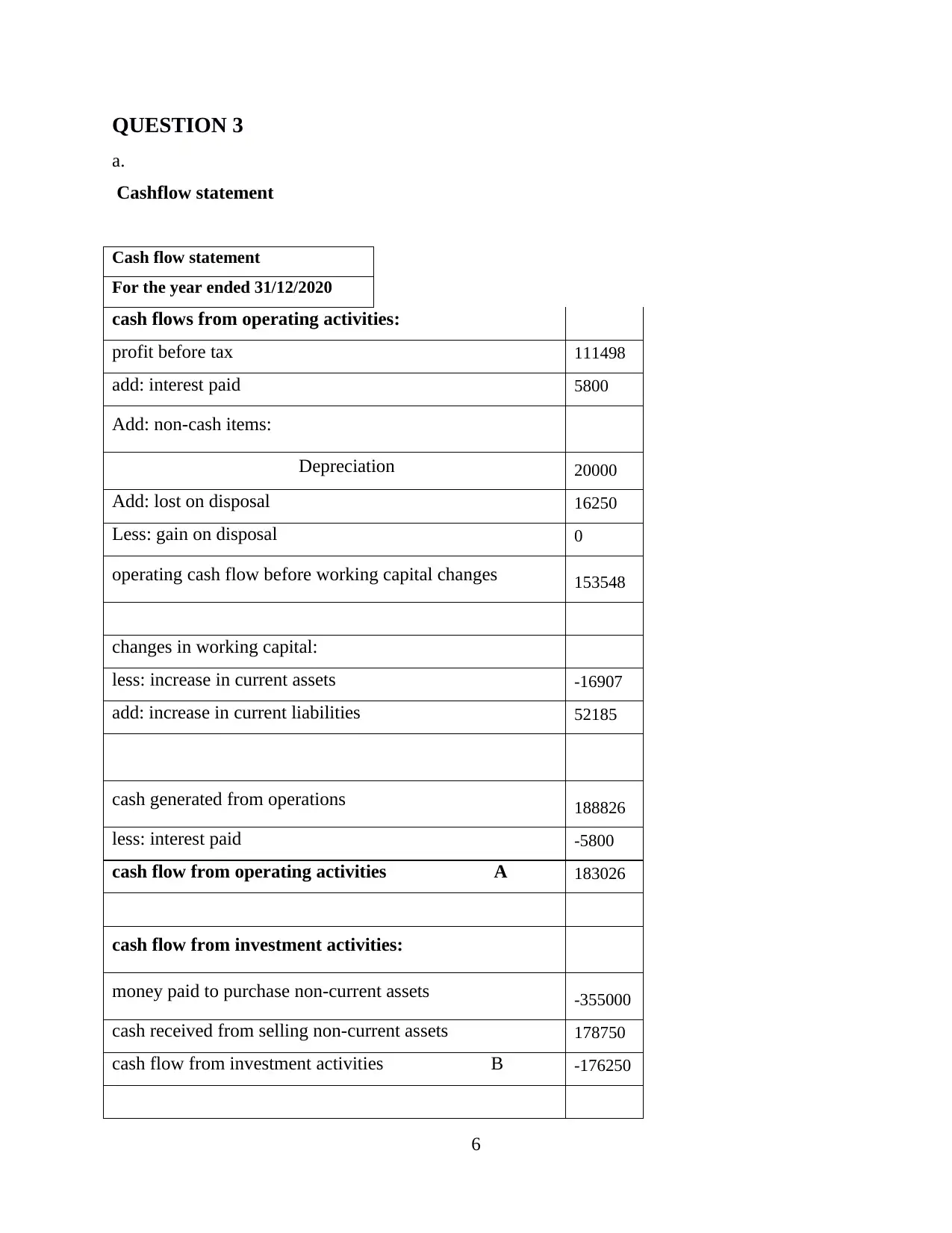

QUESTION 3

a.

Cashflow statement

Cash flow statement

For the year ended 31/12/2020

cash flows from operating activities:

profit before tax 111498

add: interest paid 5800

Add: non-cash items:

Depreciation 20000

Add: lost on disposal 16250

Less: gain on disposal 0

operating cash flow before working capital changes 153548

changes in working capital:

less: increase in current assets -16907

add: increase in current liabilities 52185

cash generated from operations 188826

less: interest paid -5800

cash flow from operating activities A 183026

cash flow from investment activities:

money paid to purchase non-current assets -355000

cash received from selling non-current assets 178750

cash flow from investment activities B -176250

6

a.

Cashflow statement

Cash flow statement

For the year ended 31/12/2020

cash flows from operating activities:

profit before tax 111498

add: interest paid 5800

Add: non-cash items:

Depreciation 20000

Add: lost on disposal 16250

Less: gain on disposal 0

operating cash flow before working capital changes 153548

changes in working capital:

less: increase in current assets -16907

add: increase in current liabilities 52185

cash generated from operations 188826

less: interest paid -5800

cash flow from operating activities A 183026

cash flow from investment activities:

money paid to purchase non-current assets -355000

cash received from selling non-current assets 178750

cash flow from investment activities B -176250

6

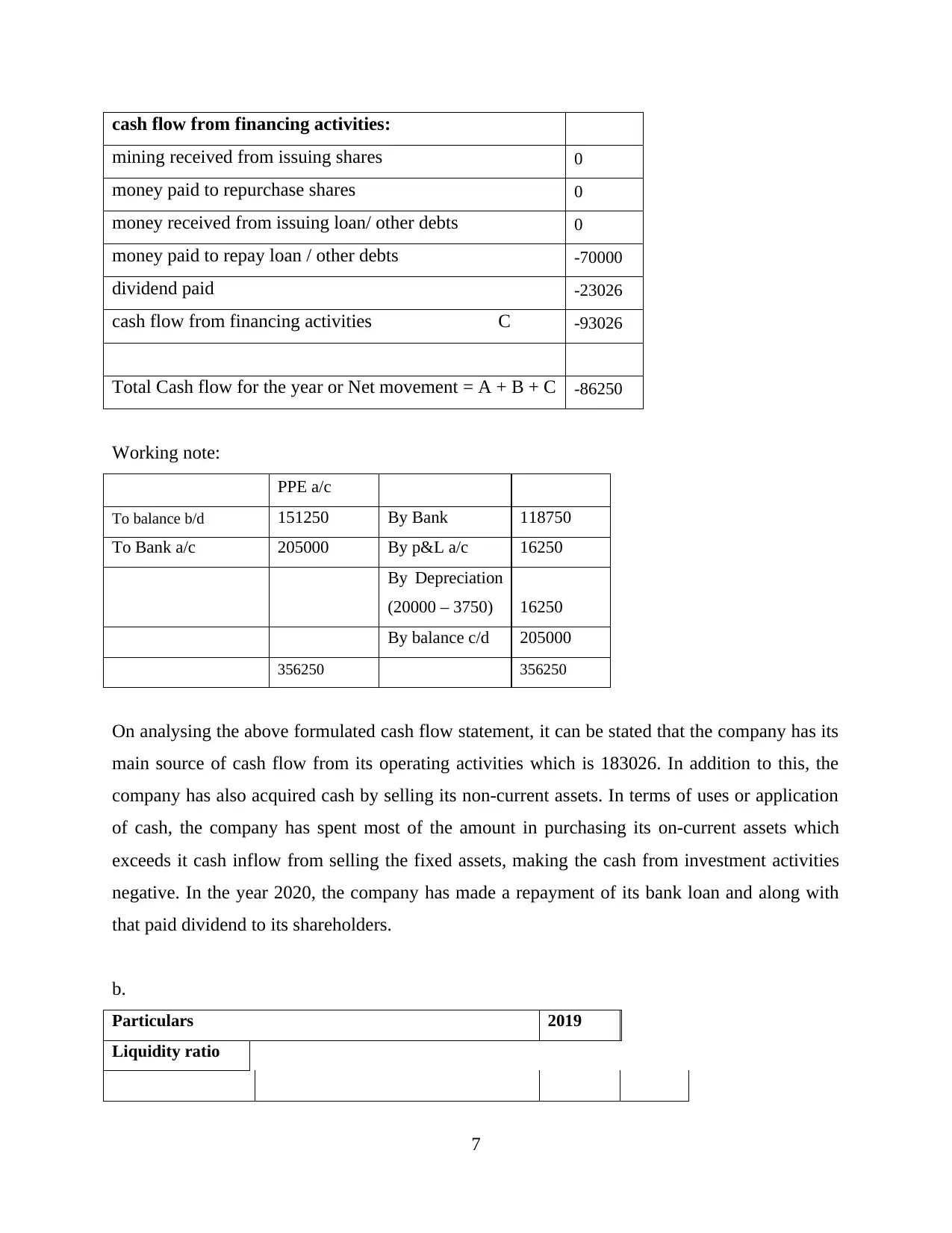

cash flow from financing activities:

mining received from issuing shares 0

money paid to repurchase shares 0

money received from issuing loan/ other debts 0

money paid to repay loan / other debts -70000

dividend paid -23026

cash flow from financing activities C -93026

Total Cash flow for the year or Net movement = A + B + C -86250

Working note:

PPE a/c

To balance b/d 151250 By Bank 118750

To Bank a/c 205000 By p&L a/c 16250

By Depreciation

(20000 – 3750) 16250

By balance c/d 205000

356250 356250

On analysing the above formulated cash flow statement, it can be stated that the company has its

main source of cash flow from its operating activities which is 183026. In addition to this, the

company has also acquired cash by selling its non-current assets. In terms of uses or application

of cash, the company has spent most of the amount in purchasing its on-current assets which

exceeds it cash inflow from selling the fixed assets, making the cash from investment activities

negative. In the year 2020, the company has made a repayment of its bank loan and along with

that paid dividend to its shareholders.

b.

Particulars 2019

Liquidity ratio

7

mining received from issuing shares 0

money paid to repurchase shares 0

money received from issuing loan/ other debts 0

money paid to repay loan / other debts -70000

dividend paid -23026

cash flow from financing activities C -93026

Total Cash flow for the year or Net movement = A + B + C -86250

Working note:

PPE a/c

To balance b/d 151250 By Bank 118750

To Bank a/c 205000 By p&L a/c 16250

By Depreciation

(20000 – 3750) 16250

By balance c/d 205000

356250 356250

On analysing the above formulated cash flow statement, it can be stated that the company has its

main source of cash flow from its operating activities which is 183026. In addition to this, the

company has also acquired cash by selling its non-current assets. In terms of uses or application

of cash, the company has spent most of the amount in purchasing its on-current assets which

exceeds it cash inflow from selling the fixed assets, making the cash from investment activities

negative. In the year 2020, the company has made a repayment of its bank loan and along with

that paid dividend to its shareholders.

b.

Particulars 2019

Liquidity ratio

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

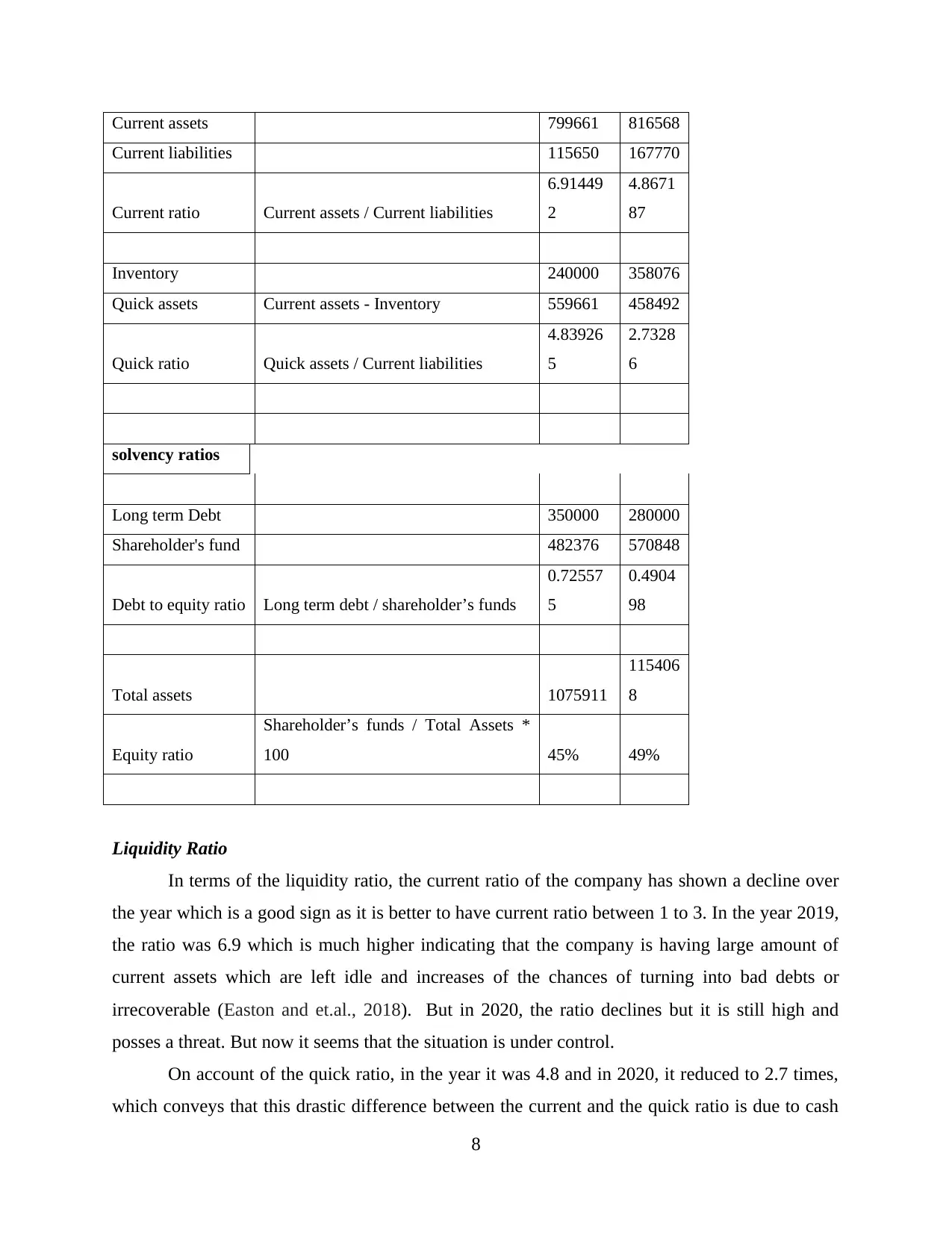

Current assets 799661 816568

Current liabilities 115650 167770

Current ratio Current assets / Current liabilities

6.91449

2

4.8671

87

Inventory 240000 358076

Quick assets Current assets - Inventory 559661 458492

Quick ratio Quick assets / Current liabilities

4.83926

5

2.7328

6

solvency ratios

Long term Debt 350000 280000

Shareholder's fund 482376 570848

Debt to equity ratio Long term debt / shareholder’s funds

0.72557

5

0.4904

98

Total assets 1075911

115406

8

Equity ratio

Shareholder’s funds / Total Assets *

100 45% 49%

Liquidity Ratio

In terms of the liquidity ratio, the current ratio of the company has shown a decline over

the year which is a good sign as it is better to have current ratio between 1 to 3. In the year 2019,

the ratio was 6.9 which is much higher indicating that the company is having large amount of

current assets which are left idle and increases of the chances of turning into bad debts or

irrecoverable (Easton and et.al., 2018). But in 2020, the ratio declines but it is still high and

posses a threat. But now it seems that the situation is under control.

On account of the quick ratio, in the year it was 4.8 and in 2020, it reduced to 2.7 times,

which conveys that this drastic difference between the current and the quick ratio is due to cash

8

Current liabilities 115650 167770

Current ratio Current assets / Current liabilities

6.91449

2

4.8671

87

Inventory 240000 358076

Quick assets Current assets - Inventory 559661 458492

Quick ratio Quick assets / Current liabilities

4.83926

5

2.7328

6

solvency ratios

Long term Debt 350000 280000

Shareholder's fund 482376 570848

Debt to equity ratio Long term debt / shareholder’s funds

0.72557

5

0.4904

98

Total assets 1075911

115406

8

Equity ratio

Shareholder’s funds / Total Assets *

100 45% 49%

Liquidity Ratio

In terms of the liquidity ratio, the current ratio of the company has shown a decline over

the year which is a good sign as it is better to have current ratio between 1 to 3. In the year 2019,

the ratio was 6.9 which is much higher indicating that the company is having large amount of

current assets which are left idle and increases of the chances of turning into bad debts or

irrecoverable (Easton and et.al., 2018). But in 2020, the ratio declines but it is still high and

posses a threat. But now it seems that the situation is under control.

On account of the quick ratio, in the year it was 4.8 and in 2020, it reduced to 2.7 times,

which conveys that this drastic difference between the current and the quick ratio is due to cash

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

blocked in the inventory of the company. This is a sign of danger for the company even though

the ratio is good which the reason behind it is not good. The company has increased its

investment in the inventory over the year. This ratio has declined over the period of time as the

company has started repaying its debt amount. This is a good sign in respect to the

Solvency ratio

In the context of debt to equity ratio, the ratio computed clearly depicts that the

company is having sufficient amount of equity funds in order to meet with its long term debt

obligations. This is a good sign and indicates less risky financial situation of the company.

In respect to the equity ratio, it determines the amount of capitalization currently

utilized by the company (Patil and Mohanthy, 2017). Higher the ratio better it is for the company

since it depicts the company is having sufficient amount of equity in order to support the

functions of the business entity. While the lower ratio indicates that the company is having large

amount of debt. In respect XYX company, the ratio is high which is good sign of financial

stability. This has increased during period from 2019 to 2020.

QUESTION 4

a.

Difference between accounting concepts, accounting standards and accounting policies

The accounting policies are basically the norms, rules or the methods which the

business decides for themselves. These policies are not universal in nature and can differ from

one company to another. The accounting policies mainly defines the way in which the

transactions should be accounted. For instance, one company decided to charge the depreciation

based on the straight-line method while some other company decided to do it by using written

down value method (Polzer, Grossi and Reichard, 2021). This is because, of the company policy

pertaining to charging of depreciation. But it is important to understand that the accounting

policies is not arbitrary or selected at random pick of card. Even if it differs from one person to

another, it still falls based upon an overall framework in order to be acceptable.

On the other hand, accounting concept refers to the basic assumption and the principles

which works as the base for recording the business transactions along with preparing the

accounts. The concept is based upon the assumption that the accounting purposes, business entity

9

the ratio is good which the reason behind it is not good. The company has increased its

investment in the inventory over the year. This ratio has declined over the period of time as the

company has started repaying its debt amount. This is a good sign in respect to the

Solvency ratio

In the context of debt to equity ratio, the ratio computed clearly depicts that the

company is having sufficient amount of equity funds in order to meet with its long term debt

obligations. This is a good sign and indicates less risky financial situation of the company.

In respect to the equity ratio, it determines the amount of capitalization currently

utilized by the company (Patil and Mohanthy, 2017). Higher the ratio better it is for the company

since it depicts the company is having sufficient amount of equity in order to support the

functions of the business entity. While the lower ratio indicates that the company is having large

amount of debt. In respect XYX company, the ratio is high which is good sign of financial

stability. This has increased during period from 2019 to 2020.

QUESTION 4

a.

Difference between accounting concepts, accounting standards and accounting policies

The accounting policies are basically the norms, rules or the methods which the

business decides for themselves. These policies are not universal in nature and can differ from

one company to another. The accounting policies mainly defines the way in which the

transactions should be accounted. For instance, one company decided to charge the depreciation

based on the straight-line method while some other company decided to do it by using written

down value method (Polzer, Grossi and Reichard, 2021). This is because, of the company policy

pertaining to charging of depreciation. But it is important to understand that the accounting

policies is not arbitrary or selected at random pick of card. Even if it differs from one person to

another, it still falls based upon an overall framework in order to be acceptable.

On the other hand, accounting concept refers to the basic assumption and the principles

which works as the base for recording the business transactions along with preparing the

accounts. The concept is based upon the assumption that the accounting purposes, business entity

9

and its owners are separate and independent from each other. In simple terms, accounting

concepts are the crucial conventions with which the accounting transactions are recorded.

Accounting standard are referred to as the uniform rules which all the assesses are

required to follow the accounting standards. The main or the primary objective of the accounting

standard is the correct measurement and disclosure. It defines the rules for treating different

types of transaction which helps in presenting the true picture of the financial accounts of the

company.

b.

Accrual concept

The accrual accounting principle is the accounting concept in which transactions ae being

recorded during the time period in which they occur irrespective of the fact whether actual cash

flow pertaining to the transaction is received or not (How to Use Accrual Accounting in Your

Growing Business. 2020). The main idea behind this principle that the financial events are

properly recognised by matching revenue to its expenses. For example, ABC company uses

accrual accounting principle for recording its transactions. it sends an invoice to a software

company for a monthly sales amount of $10000, of which 60% is paid in cash while rest on

credit. Thus, under this principle, the accountant treats the credit transaction as sales and

therefore, expenses will be deducted.

10

concepts are the crucial conventions with which the accounting transactions are recorded.

Accounting standard are referred to as the uniform rules which all the assesses are

required to follow the accounting standards. The main or the primary objective of the accounting

standard is the correct measurement and disclosure. It defines the rules for treating different

types of transaction which helps in presenting the true picture of the financial accounts of the

company.

b.

Accrual concept

The accrual accounting principle is the accounting concept in which transactions ae being

recorded during the time period in which they occur irrespective of the fact whether actual cash

flow pertaining to the transaction is received or not (How to Use Accrual Accounting in Your

Growing Business. 2020). The main idea behind this principle that the financial events are

properly recognised by matching revenue to its expenses. For example, ABC company uses

accrual accounting principle for recording its transactions. it sends an invoice to a software

company for a monthly sales amount of $10000, of which 60% is paid in cash while rest on

credit. Thus, under this principle, the accountant treats the credit transaction as sales and

therefore, expenses will be deducted.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.