BAO 3309: Principles of Disclosure for Financial Reporting Analysis

VerifiedAdded on 2022/10/11

|14

|3343

|7

Report

AI Summary

This report examines the principles of disclosure in financial reporting, focusing on the International Accounting Standards Board's (IASB) efforts to improve communication within financial statements. It addresses the 'disclosure problem,' which encompasses a lack of relevant information, an excess of irrelevant information, and ineffective communication. The report details IASB's initiatives, including amendments to IAS 1 (Presentation of Financial Statements) and IAS 7 (Statement of Cash Flows), as well as the publication of IFRS Practice Statement 2. It explores the concept of materiality, its qualitative and quantitative aspects, and its impact on information presentation and disclosure. The report also discusses issues related to the content and arrangement of primary financial statements, and how IASB has responded to these concerns through the use of primary financial reports and performance measures. This report provides a comprehensive overview of the IASB's actions to enhance the clarity, relevance, and effectiveness of financial reporting.

Running head: PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN

FINANCIAL REPORTING

Principles of Disclosure: Better Communication in Financial Reporting

Name of the Student

Name of the University

Author’s Note

FINANCIAL REPORTING

Principles of Disclosure: Better Communication in Financial Reporting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

Table of Contents

Requirement 1............................................................................................................................2

Requirement 2............................................................................................................................2

Requirement 3............................................................................................................................4

Requirement 4............................................................................................................................5

Requirement 5............................................................................................................................6

Requirement 6............................................................................................................................7

References................................................................................................................................12

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

Table of Contents

Requirement 1............................................................................................................................2

Requirement 2............................................................................................................................2

Requirement 3............................................................................................................................4

Requirement 4............................................................................................................................5

Requirement 5............................................................................................................................6

Requirement 6............................................................................................................................7

References................................................................................................................................12

2

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

Requirement 1

It needs to be mentioned that the International Accounting Standards Board (IASB)

has undertaken the initiative for prioritizing improvements in the communication of the

present information given in the financial reports; and there are certain reasons for this plan.

It can be seen that IASB has provided certain significant reasons for the plan for brining

enhancement in the communication of information given in the financial reports (ifrs.org

2019).

According to IASB, investors can oversee the most relevant information for making

investment related decisions in the presence of poor communication of information provided

in the financial reports; in fact, unsuccessful communication of financial information can

make the investors unable in recognizing the association between the portions of information

in various portions of the financial reports of the corporations. Undertaking inappropriate

investment decision is the main outcome of the above-mentioned aspects (ifrs.org 2019).

In the presence of poor communication of the financial information, reduction in the

comprehensiveness of the financial reports can be seen and this is a major factor that

enhances doubt among the perception of the investors regarding the financial position and

financial performance of the companies. These largely contribute to higher cost of capital for

the business entities. Better decisions related to investment and reduced cost of capital is the

main outcomes of effective communication of financial information in the financial reports

(ifrs.org 2019).

IASB has also mentioned that the approach of ‘tick the box’ disclosure along with

ineffectively organized as well as presented financial statements hide the relevant and

valuable information. In the presence of this, it becomes difficult for the investors to obtain

the required information easily from the financial statements. In order to present this, IASB

has undertaken the initiative to consider assessing the processes to display the financial

information in the financial statements. IASB has the intention of contributing towards

making the financial information more relevant and real. For this reason, the initiative of

IASB named “Better Communication in Financial Reporting” will provide major motivation

in bringing enhancement in the communication of financial information in the coming years

(ifrs.org 2019).

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

Requirement 1

It needs to be mentioned that the International Accounting Standards Board (IASB)

has undertaken the initiative for prioritizing improvements in the communication of the

present information given in the financial reports; and there are certain reasons for this plan.

It can be seen that IASB has provided certain significant reasons for the plan for brining

enhancement in the communication of information given in the financial reports (ifrs.org

2019).

According to IASB, investors can oversee the most relevant information for making

investment related decisions in the presence of poor communication of information provided

in the financial reports; in fact, unsuccessful communication of financial information can

make the investors unable in recognizing the association between the portions of information

in various portions of the financial reports of the corporations. Undertaking inappropriate

investment decision is the main outcome of the above-mentioned aspects (ifrs.org 2019).

In the presence of poor communication of the financial information, reduction in the

comprehensiveness of the financial reports can be seen and this is a major factor that

enhances doubt among the perception of the investors regarding the financial position and

financial performance of the companies. These largely contribute to higher cost of capital for

the business entities. Better decisions related to investment and reduced cost of capital is the

main outcomes of effective communication of financial information in the financial reports

(ifrs.org 2019).

IASB has also mentioned that the approach of ‘tick the box’ disclosure along with

ineffectively organized as well as presented financial statements hide the relevant and

valuable information. In the presence of this, it becomes difficult for the investors to obtain

the required information easily from the financial statements. In order to present this, IASB

has undertaken the initiative to consider assessing the processes to display the financial

information in the financial statements. IASB has the intention of contributing towards

making the financial information more relevant and real. For this reason, the initiative of

IASB named “Better Communication in Financial Reporting” will provide major motivation

in bringing enhancement in the communication of financial information in the coming years

(ifrs.org 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

Requirement 2

IASB invited the feedbacks from the stakeholders regarding the disclosure initiatives.

From this, IASB has encountered three key concerns related to the disclosure of financial

information in the financial reports; and these three concerns related to disclosure are jointly

identified as the ‘disclosure problem’ (ifrs.org 2019). These are discussed below:

1. Absence of adequate relevant information – Information is considered as relevant in

case it has the capability to create dissimilarity in the decisions of the most important users of

the financial reports. In case the financial statements fail in providing the adequate relevant

information, the financial report users may end up in making wrong decision related to

investment or lending (ifrs.org 2019).

2. Presence of excessive irrelevant information – The presence of irrelevant information is

another major concern related to discourse of information. Irrelevant information is

considered as unwanted because of two reasons. First, it creates confusion in the financial

statements so that the investors oversee the relevant financial information or they face

difficulty in finding relevant financial information; all these increase the difficulty in

comprehending the financial statements. Second, irrelevant information can lead to the

addition of needless continuing costs in the procedures to prepare the financial statements

(ey.com 2019).

3. Poor communication of the provided information – Ineffective communication is the

third concern associated with information disclosure. In the presence of ineffective

communication of financial information, it becomes difficult to comprehend the financial

statements while taking much time for analysing them. Moreover, this can lead to overlook

the pertinent financial information by the financial report users or they can unsuccessful in

the recognition of the underlying connection between dissimilar fragments of information in

the financial reports (iasplus.com 2019).

Apart from the above, there are certain causes that lead to these issues. Business

entities are required to use judgments at the time to make decisions on particular information

they need to be unveiled in the financial reports and what the mainly appropriate manner is of

organizing and communicating it. The key reason that contributes to the problem related to

disclosure is the struggle to apply this judgement. According to the received feedback of the

board, the struggles to apply judgments are frequently behavioural where the IFRS standards

requirements have nothing to contribute. Another major cause for the disclosure problem in

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

Requirement 2

IASB invited the feedbacks from the stakeholders regarding the disclosure initiatives.

From this, IASB has encountered three key concerns related to the disclosure of financial

information in the financial reports; and these three concerns related to disclosure are jointly

identified as the ‘disclosure problem’ (ifrs.org 2019). These are discussed below:

1. Absence of adequate relevant information – Information is considered as relevant in

case it has the capability to create dissimilarity in the decisions of the most important users of

the financial reports. In case the financial statements fail in providing the adequate relevant

information, the financial report users may end up in making wrong decision related to

investment or lending (ifrs.org 2019).

2. Presence of excessive irrelevant information – The presence of irrelevant information is

another major concern related to discourse of information. Irrelevant information is

considered as unwanted because of two reasons. First, it creates confusion in the financial

statements so that the investors oversee the relevant financial information or they face

difficulty in finding relevant financial information; all these increase the difficulty in

comprehending the financial statements. Second, irrelevant information can lead to the

addition of needless continuing costs in the procedures to prepare the financial statements

(ey.com 2019).

3. Poor communication of the provided information – Ineffective communication is the

third concern associated with information disclosure. In the presence of ineffective

communication of financial information, it becomes difficult to comprehend the financial

statements while taking much time for analysing them. Moreover, this can lead to overlook

the pertinent financial information by the financial report users or they can unsuccessful in

the recognition of the underlying connection between dissimilar fragments of information in

the financial reports (iasplus.com 2019).

Apart from the above, there are certain causes that lead to these issues. Business

entities are required to use judgments at the time to make decisions on particular information

they need to be unveiled in the financial reports and what the mainly appropriate manner is of

organizing and communicating it. The key reason that contributes to the problem related to

disclosure is the struggle to apply this judgement. According to the received feedback of the

board, the struggles to apply judgments are frequently behavioural where the IFRS standards

requirements have nothing to contribute. Another major cause for the disclosure problem in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

accordance with the feedback received by IASB is the absence of direction and guidance

related to the financial statements’ structure and guidance, especially related to the notes

disclosure which is major contributor of the behavioural difficulties. These are the main

caused identified by IASB that contribute to disclosure problem (ifrs.org 2019).

Requirement 3

In the year 2013, IASB launched the Disclosure Initiative for taking actions to the

feedback for improving the appropriateness of financial reports disclosures. Among all the

initiatives, two major initiatives of IASB are to bring amendments in IAS 1 Presentation of

Financial Statements and IAS 7 Statement of Cash Flows (ifrs.org 2019). These amendments

are discussed below:

Amendments in IAS 1 – IASB published modifications in IAS 1 in December 2014 with the

aim to eliminate obstacles in employing the judgments. It needs to be mentioned that the

amendments are associated with five aspects which are materiality, order of the notes to the

financial statements, policies of accounting, subtotals and disaggregation; and IASB designed

these amendments with the aim to encourage the business entities for applying professional

judgments for ascertaining the information that is required to be shown in the financial

reports (kjs.mof.gov.cn 2019). For instance, it is cleared by the amendments that the business

organizations are needed to apply materiality in the whole financial reports and the value of

the financial reports can be constrained due to the attachment of information that are not

material. Moreover, it is clarified by the amendments that professional judgements are

required to be utilized by the business entities with the aim to ascertain where the financial

information needs to be disclosed and which order needs to be used (iasplus.com 2019).

Amendments in IAS 7 – Amendments in IAS 7 were published by IASB in January 2016

with the aim to bring enhancement in disclosures related to the changes in liabilities from

financing activities. As per these modifications, it is required for a business entity to deliver a

settlement of the amounts in the opening as well as closing balance sheet for every element

that is responsible for cash flows from financing activities in the statement of cash flows that

excluded items of equity (ey.com 2019). The following items need to be includes in the

reconciliation:

1. Opening balances in the financial position statements;

2. Movements in the time that includes financial cash flows changes, changes due to

losing or obtaining business subsidiaries, and changes in other non-cash items.

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

accordance with the feedback received by IASB is the absence of direction and guidance

related to the financial statements’ structure and guidance, especially related to the notes

disclosure which is major contributor of the behavioural difficulties. These are the main

caused identified by IASB that contribute to disclosure problem (ifrs.org 2019).

Requirement 3

In the year 2013, IASB launched the Disclosure Initiative for taking actions to the

feedback for improving the appropriateness of financial reports disclosures. Among all the

initiatives, two major initiatives of IASB are to bring amendments in IAS 1 Presentation of

Financial Statements and IAS 7 Statement of Cash Flows (ifrs.org 2019). These amendments

are discussed below:

Amendments in IAS 1 – IASB published modifications in IAS 1 in December 2014 with the

aim to eliminate obstacles in employing the judgments. It needs to be mentioned that the

amendments are associated with five aspects which are materiality, order of the notes to the

financial statements, policies of accounting, subtotals and disaggregation; and IASB designed

these amendments with the aim to encourage the business entities for applying professional

judgments for ascertaining the information that is required to be shown in the financial

reports (kjs.mof.gov.cn 2019). For instance, it is cleared by the amendments that the business

organizations are needed to apply materiality in the whole financial reports and the value of

the financial reports can be constrained due to the attachment of information that are not

material. Moreover, it is clarified by the amendments that professional judgements are

required to be utilized by the business entities with the aim to ascertain where the financial

information needs to be disclosed and which order needs to be used (iasplus.com 2019).

Amendments in IAS 7 – Amendments in IAS 7 were published by IASB in January 2016

with the aim to bring enhancement in disclosures related to the changes in liabilities from

financing activities. As per these modifications, it is required for a business entity to deliver a

settlement of the amounts in the opening as well as closing balance sheet for every element

that is responsible for cash flows from financing activities in the statement of cash flows that

excluded items of equity (ey.com 2019). The following items need to be includes in the

reconciliation:

1. Opening balances in the financial position statements;

2. Movements in the time that includes financial cash flows changes, changes due to

losing or obtaining business subsidiaries, and changes in other non-cash items.

5

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

3. Closing balances in the balance sheet (ifrs.org 2019).

Requirement 4

It needs to be mentioned that materiality affects the presentation as well as revelation

of financial statement related information. The following discussion shows the effects of

materiality in three contexts which are assessment of materiality, immaterial information and

aggregating and disaggregating information.

Assessment of Materiality – Two types of materiality assessment can be seen; they are

qualitative and quantitative assessment; and individual and collective assessment. Size and

nature judged in a certain situation of a business entity determines if the information is

material or not. It is needed to put emphasis on both qualitative and quantitative factors for

the assessment of materially. Quantitative factors such as carrying amount are not the sole

factors that need to be considered for the assessment of materiality because the entity-specific

factors known as qualitative factors are also needed to take into consideration for determining

whether the information is material or not. This indicates towards the crucial aspect that the

assessment of materiality is a sensitive matter that demands to undertake both the qualitative

and quantitative factors. In addition, both individual as well as collective basis needs to be

taken into consideration for assessing materiality (iaasb.org 2019).

Immaterial information – Delivery of immaterial information in the financial statements

may make the information doubtful and the financial reports may become less understandable

for this. For instance, it becomes difficult for the investors to find the material information in

case an entity provided detailed information on a matter having no material impact. Length of

the financial reports increases due to the disclosure of immaterial information while making

them less comprehensible and making the users to use additional resources to gain the

material information. There is not any restriction on the business entities from IASB on the

disclosure of immaterial information. However, in certain cases, business entities become

beneficial through disclosing the fact that a particular transaction or event is not material or

immaterial (ifrs.org 2019).

Aggregating and Disaggregating information – It is required for a business entity to

distinctly present every material class of same substance and items with different functions

except they are material. Business entities are required to aggregate financial statements from

the processing of huge number of transactions into classes in accordance with their purpose

or character. The last stage in the aggregation process is to present the shortened and

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

3. Closing balances in the balance sheet (ifrs.org 2019).

Requirement 4

It needs to be mentioned that materiality affects the presentation as well as revelation

of financial statement related information. The following discussion shows the effects of

materiality in three contexts which are assessment of materiality, immaterial information and

aggregating and disaggregating information.

Assessment of Materiality – Two types of materiality assessment can be seen; they are

qualitative and quantitative assessment; and individual and collective assessment. Size and

nature judged in a certain situation of a business entity determines if the information is

material or not. It is needed to put emphasis on both qualitative and quantitative factors for

the assessment of materially. Quantitative factors such as carrying amount are not the sole

factors that need to be considered for the assessment of materiality because the entity-specific

factors known as qualitative factors are also needed to take into consideration for determining

whether the information is material or not. This indicates towards the crucial aspect that the

assessment of materiality is a sensitive matter that demands to undertake both the qualitative

and quantitative factors. In addition, both individual as well as collective basis needs to be

taken into consideration for assessing materiality (iaasb.org 2019).

Immaterial information – Delivery of immaterial information in the financial statements

may make the information doubtful and the financial reports may become less understandable

for this. For instance, it becomes difficult for the investors to find the material information in

case an entity provided detailed information on a matter having no material impact. Length of

the financial reports increases due to the disclosure of immaterial information while making

them less comprehensible and making the users to use additional resources to gain the

material information. There is not any restriction on the business entities from IASB on the

disclosure of immaterial information. However, in certain cases, business entities become

beneficial through disclosing the fact that a particular transaction or event is not material or

immaterial (ifrs.org 2019).

Aggregating and Disaggregating information – It is required for a business entity to

distinctly present every material class of same substance and items with different functions

except they are material. Business entities are required to aggregate financial statements from

the processing of huge number of transactions into classes in accordance with their purpose

or character. The last stage in the aggregation process is to present the shortened and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

classified date that lead to the development of financial statements’ line items. Moreover,

there is not any scope of additional disaggregation in case a specific substance in the financial

statement is not material in individual basis. Aggregating information refers to that the

specific information regarding a component is less detailed. For this reason, the managements

of the business entities assess if there would be loss of information by aggregation are

material at the time to take aggregation related decisions (ifrs.org 2019).

Requirement 5

It needs to be mentioned that there were certain issues expressed related to the content

and arrangement of the primary financial reports. These are mentioned below:

There were differences in the structure and content of the balance sheets of the

companies operating in the same industry.

Many companies were involved in presenting a subtotal of operating profit

communicating the EBIT when different methods were adopted for calculating these

subtotals.

Many entities were involved in presenting adjusted net profit in the presence of

difference in adjustments and in the absence of transparency.

There were variations in the commencement point to determine cash flow from

operating activities, in presentation of dividends and interest and in number of line

items related to the segment information (ifrs.org 2019).

It can be seen that there issues were considered by IASB with highest priority since the

board has responded to these concerns through two aspects; they are the functions of primary

financial reports as well as notes and the utilization of performance measures in financial

reports. These are mentioned below.

IASB has considered the fact that the users of the financial reports put more focus on

the primary financial reports than the notes as these provide the beginning of the financial

reports and give them with the impression on how the company is performing and what is the

asset as well as liability position of the company. Therefore, as per IASB, the primary

financial reports are the statement of financial position, statement of profit or loss, statement

of cash flows and statement of change in equity. IASB has also specified the direction on the

use of primary financial reports and notes in the Conceptual Framework (ifrs.org 2019).

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

classified date that lead to the development of financial statements’ line items. Moreover,

there is not any scope of additional disaggregation in case a specific substance in the financial

statement is not material in individual basis. Aggregating information refers to that the

specific information regarding a component is less detailed. For this reason, the managements

of the business entities assess if there would be loss of information by aggregation are

material at the time to take aggregation related decisions (ifrs.org 2019).

Requirement 5

It needs to be mentioned that there were certain issues expressed related to the content

and arrangement of the primary financial reports. These are mentioned below:

There were differences in the structure and content of the balance sheets of the

companies operating in the same industry.

Many companies were involved in presenting a subtotal of operating profit

communicating the EBIT when different methods were adopted for calculating these

subtotals.

Many entities were involved in presenting adjusted net profit in the presence of

difference in adjustments and in the absence of transparency.

There were variations in the commencement point to determine cash flow from

operating activities, in presentation of dividends and interest and in number of line

items related to the segment information (ifrs.org 2019).

It can be seen that there issues were considered by IASB with highest priority since the

board has responded to these concerns through two aspects; they are the functions of primary

financial reports as well as notes and the utilization of performance measures in financial

reports. These are mentioned below.

IASB has considered the fact that the users of the financial reports put more focus on

the primary financial reports than the notes as these provide the beginning of the financial

reports and give them with the impression on how the company is performing and what is the

asset as well as liability position of the company. Therefore, as per IASB, the primary

financial reports are the statement of financial position, statement of profit or loss, statement

of cash flows and statement of change in equity. IASB has also specified the direction on the

use of primary financial reports and notes in the Conceptual Framework (ifrs.org 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

In addition, IASB has included certain performance measures in the financial reports

with the aim to formulate the financial statements and information more comprehensible to

their users. The instances of some of these performance measures are Earnings before

Interest, Tax, Depreciation and Amortization (EBITDA) and Earnings before Interest and

Tax (EBIT) (assets.kpmg 2019).

Requirement 6

Wesfarmers Ltd (Wesfarmers) has been selected for this part and the following

discussion shows the analysis of the 2014 and 2015 annual reports of the corporation.

i. The length of 2014 financial report of Wesfarmers is 52 pages starting from page 103

to page 154. The length of 2015 financial report is 52 pages starting from page 87 to

page 138 (wesfarmers.com.au 2019). It means there is not any reduction in the length

of the financial report of Wesfarmers from 2014 to 2015.

ii. The total notes in the financial report of Wesfarmers in 2014 and 2015 are 28 and 29

respectively. It implies that there is the reduction of only one note in the 2015

financial report as compared to the 2014 financial report (wesfarmers.com.au 2019).

iii. It is required for the business organizations to group the notes to the financial reports

into more rational and rational groups with the aim to make them more

comprehensible for the users of the financial reports. It can be observed from the 2014

and 2015 annual reports of Wesfarmers that there is not any difference in the grouping

of the notes in the financial reports. The management of Wesfarmers has grouped the

notes in logical flows as per their business and strategies. In the financial reports of

both the years, the company has divided the notes in six logical groups; they are Key

Numbers that includes information on income, expenses, financial assets and

liabilities; Capital that includes notes related to capital like capital management, EPS,

equity and reserves and others; Risk that includes notes to risk management like

hedging, impairment and others; Group Structure that includes notes on subsidiaries,

discontinued operations and others; Unrecognized Items that include commitment as

well as contingencies and others; and Others that includes notes on parent disclosure,

auditor’s remuneration and others (wesfarmers.com.au 2019).

iv. When comparing the notes disclosed in the financial report of Wesfarmers in 2014

and 2015, it can be seen that there is not any difference among them. Both the years

have six groups of notes that are key number, capital, risk, group structure,

unrecognized items and other. Moreover, both all the groups in 2014 and 2015 have

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

In addition, IASB has included certain performance measures in the financial reports

with the aim to formulate the financial statements and information more comprehensible to

their users. The instances of some of these performance measures are Earnings before

Interest, Tax, Depreciation and Amortization (EBITDA) and Earnings before Interest and

Tax (EBIT) (assets.kpmg 2019).

Requirement 6

Wesfarmers Ltd (Wesfarmers) has been selected for this part and the following

discussion shows the analysis of the 2014 and 2015 annual reports of the corporation.

i. The length of 2014 financial report of Wesfarmers is 52 pages starting from page 103

to page 154. The length of 2015 financial report is 52 pages starting from page 87 to

page 138 (wesfarmers.com.au 2019). It means there is not any reduction in the length

of the financial report of Wesfarmers from 2014 to 2015.

ii. The total notes in the financial report of Wesfarmers in 2014 and 2015 are 28 and 29

respectively. It implies that there is the reduction of only one note in the 2015

financial report as compared to the 2014 financial report (wesfarmers.com.au 2019).

iii. It is required for the business organizations to group the notes to the financial reports

into more rational and rational groups with the aim to make them more

comprehensible for the users of the financial reports. It can be observed from the 2014

and 2015 annual reports of Wesfarmers that there is not any difference in the grouping

of the notes in the financial reports. The management of Wesfarmers has grouped the

notes in logical flows as per their business and strategies. In the financial reports of

both the years, the company has divided the notes in six logical groups; they are Key

Numbers that includes information on income, expenses, financial assets and

liabilities; Capital that includes notes related to capital like capital management, EPS,

equity and reserves and others; Risk that includes notes to risk management like

hedging, impairment and others; Group Structure that includes notes on subsidiaries,

discontinued operations and others; Unrecognized Items that include commitment as

well as contingencies and others; and Others that includes notes on parent disclosure,

auditor’s remuneration and others (wesfarmers.com.au 2019).

iv. When comparing the notes disclosed in the financial report of Wesfarmers in 2014

and 2015, it can be seen that there is not any difference among them. Both the years

have six groups of notes that are key number, capital, risk, group structure,

unrecognized items and other. Moreover, both all the groups in 2014 and 2015 have

8

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

same notes that are discussed above. There is only one difference that is the exclusion

of ‘Discontinued operations’ in 2015 under ‘Group Structure’.

Table 1: Notes related to Property Plant and Equipment in 2014

(Source: wesfarmers.com.au 2019)

Table 2: Notes related to Property Plant and Equipment in 2015

(Source: wesfarmers.com.au 2019)

As per Table 2, the notes related to property, plant and equipment of Wesfarmers in

2014 and 2015. It is visible from the above that there is not any changes in the languages of

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

same notes that are discussed above. There is only one difference that is the exclusion

of ‘Discontinued operations’ in 2015 under ‘Group Structure’.

Table 1: Notes related to Property Plant and Equipment in 2014

(Source: wesfarmers.com.au 2019)

Table 2: Notes related to Property Plant and Equipment in 2015

(Source: wesfarmers.com.au 2019)

As per Table 2, the notes related to property, plant and equipment of Wesfarmers in

2014 and 2015. It is visible from the above that there is not any changes in the languages of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

these notes as they are almost the same. However, a simple language change can be seen

under ‘Derecognition’ part. Another example is provided in below.

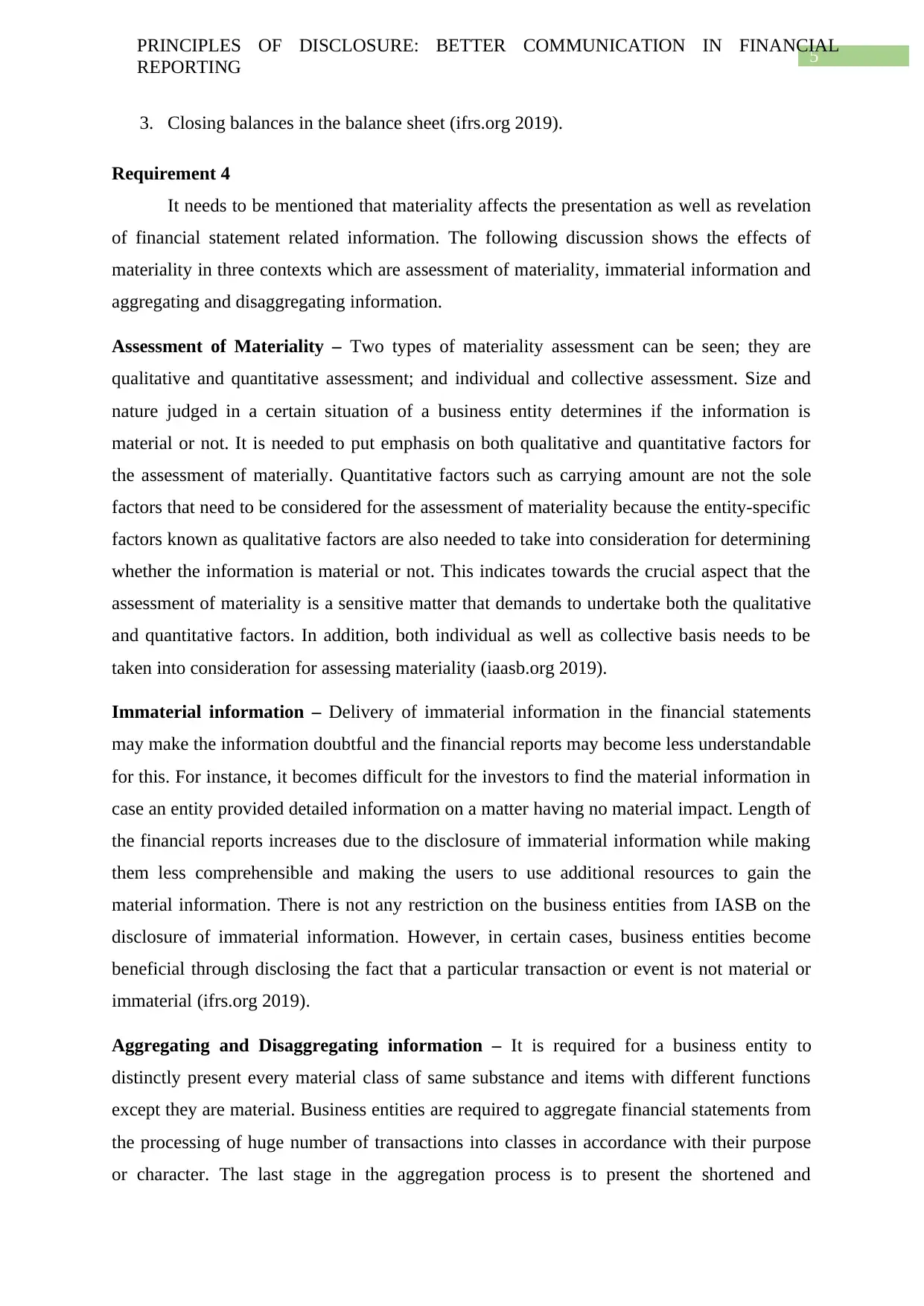

Table 3: Notes on Cash at Bank and on Deposits in 2014 and 2015

(Source: wesfarmers.com.au 2019)

It can also be seen from the above that there is hardly any change in the notes on the

recognition and measurement of cash at bank and on deposit. It implies that Wesfarmers has

used the same language in notes in 2014 and 2015.

v. Followings are the examples from the 2015 annual report of Wesfarmers that shows

the use of call out boxes for highlighting the information, material estimates and

judgments.

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

these notes as they are almost the same. However, a simple language change can be seen

under ‘Derecognition’ part. Another example is provided in below.

Table 3: Notes on Cash at Bank and on Deposits in 2014 and 2015

(Source: wesfarmers.com.au 2019)

It can also be seen from the above that there is hardly any change in the notes on the

recognition and measurement of cash at bank and on deposit. It implies that Wesfarmers has

used the same language in notes in 2014 and 2015.

v. Followings are the examples from the 2015 annual report of Wesfarmers that shows

the use of call out boxes for highlighting the information, material estimates and

judgments.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

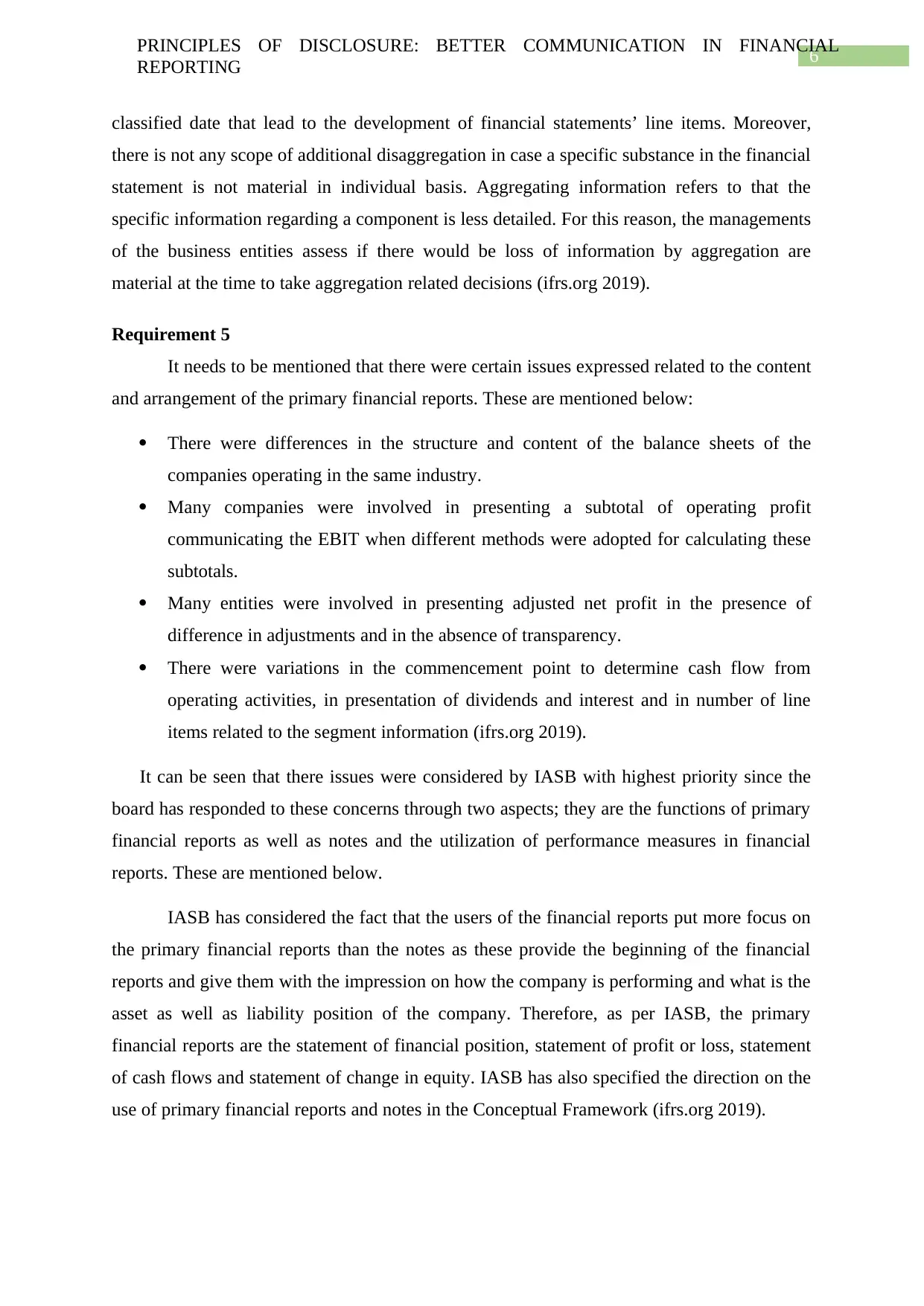

Table 4: Key Estimates on Inventory in 2015

(Source: wesfarmers.com.au 2019)

According to Table 4, call out box is used by Wesfarmers for highlighting accounting

estimates related to inventory.

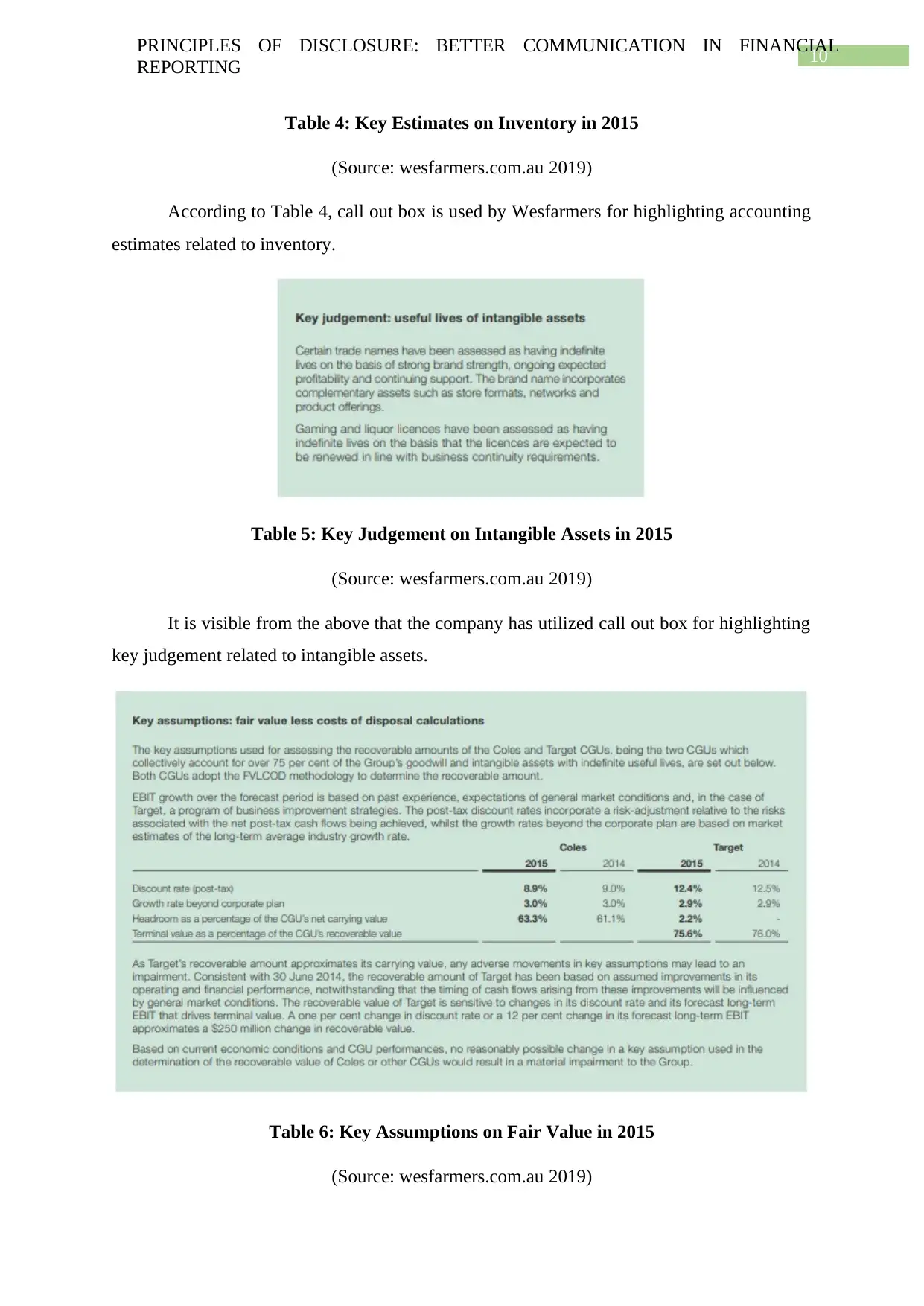

Table 5: Key Judgement on Intangible Assets in 2015

(Source: wesfarmers.com.au 2019)

It is visible from the above that the company has utilized call out box for highlighting

key judgement related to intangible assets.

Table 6: Key Assumptions on Fair Value in 2015

(Source: wesfarmers.com.au 2019)

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

Table 4: Key Estimates on Inventory in 2015

(Source: wesfarmers.com.au 2019)

According to Table 4, call out box is used by Wesfarmers for highlighting accounting

estimates related to inventory.

Table 5: Key Judgement on Intangible Assets in 2015

(Source: wesfarmers.com.au 2019)

It is visible from the above that the company has utilized call out box for highlighting

key judgement related to intangible assets.

Table 6: Key Assumptions on Fair Value in 2015

(Source: wesfarmers.com.au 2019)

11

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

According to the above, Wesfarmers has shown key assumptions on fair value with

the help of call out box. This indicates towards the large use of call out box by Wesfarmers

for highlighting crucial financial information, assumption and estimates in 2015.

PRINCIPLES OF DISCLOSURE: BETTER COMMUNICATION IN FINANCIAL

REPORTING

According to the above, Wesfarmers has shown key assumptions on fair value with

the help of call out box. This indicates towards the large use of call out box by Wesfarmers

for highlighting crucial financial information, assumption and estimates in 2015.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.