ECO504 Principles of Economics: Market Structures and Revenue

VerifiedAdded on 2023/06/15

|23

|3932

|463

Homework Assignment

AI Summary

This assignment solution for Principles of Economics (ECO504) covers key concepts including the difference between change in supply and change in quantity supplied, the impact of geopolitical events on markets, and the effects of electric car adoption on related industries. It delves into unit sales subsidies and their relationship with price elasticity of demand, using examples like wheat and precious metals. The assignment further discusses perfect competition, the role of average total costs, and the decision-making process for qualified accountants regarding cost minimization. It also explores the price elasticity of demand for alcohol and tobacco in Australia, competitive behaviors in different market structures, and the relationship between total revenue and marginal revenue. The document provides detailed explanations, diagrams, and examples to illustrate these economic principles.

Running head: PRINCIPLES OF ECONOMICS

Unit Code: ECO504

Unit Title: Principles of Economics

Assessment Title: Assessment Task 3

Type of Assessment: Written

Name of the Student:

Name of the University:

Author’s Note:

Unit Code: ECO504

Unit Title: Principles of Economics

Assessment Title: Assessment Task 3

Type of Assessment: Written

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PRINCIPLES OF ECONOMICS

Table of Contents

Question 1..........................................................................................................................3

Part 1a)...........................................................................................................................3

Part 1b)...........................................................................................................................4

Part 1c)...........................................................................................................................4

Question 2..........................................................................................................................5

Part 2a)...........................................................................................................................5

Part 2b)...........................................................................................................................5

Part 2c)...........................................................................................................................7

Question 3..........................................................................................................................8

Part 3a)...........................................................................................................................8

Part 3b)...........................................................................................................................9

Part 3c).........................................................................................................................10

Question 4........................................................................................................................10

Part 4a).........................................................................................................................10

Part 4b).........................................................................................................................10

Question 5........................................................................................................................11

Part 5a).........................................................................................................................11

Part 5b).........................................................................................................................12

Part 5c).........................................................................................................................12

Question 6........................................................................................................................13

Part 6a).........................................................................................................................13

Part 6b).........................................................................................................................13

Part 6c).........................................................................................................................14

Table of Contents

Question 1..........................................................................................................................3

Part 1a)...........................................................................................................................3

Part 1b)...........................................................................................................................4

Part 1c)...........................................................................................................................4

Question 2..........................................................................................................................5

Part 2a)...........................................................................................................................5

Part 2b)...........................................................................................................................5

Part 2c)...........................................................................................................................7

Question 3..........................................................................................................................8

Part 3a)...........................................................................................................................8

Part 3b)...........................................................................................................................9

Part 3c).........................................................................................................................10

Question 4........................................................................................................................10

Part 4a).........................................................................................................................10

Part 4b).........................................................................................................................10

Question 5........................................................................................................................11

Part 5a).........................................................................................................................11

Part 5b).........................................................................................................................12

Part 5c).........................................................................................................................12

Question 6........................................................................................................................13

Part 6a).........................................................................................................................13

Part 6b).........................................................................................................................13

Part 6c).........................................................................................................................14

PRINCIPLES OF ECONOMICS

Part 6d).........................................................................................................................15

Question 7........................................................................................................................17

References.......................................................................................................................19

Part 6d).........................................................................................................................15

Question 7........................................................................................................................17

References.......................................................................................................................19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Extension

Q* Q2Q1

SS

SS”

SS’

P1

P2

P*

SS

Price

Quantity

supplied

Price

Quantity

supplied

Contraction

IncreaseDecrease

Figure 1a (i): Change in Quantity

Supplied

Figure 1a (ii): Chang in Supply

Q* Q2Q1

P*

PRINCIPLES OF ECONOMICS

Question 1

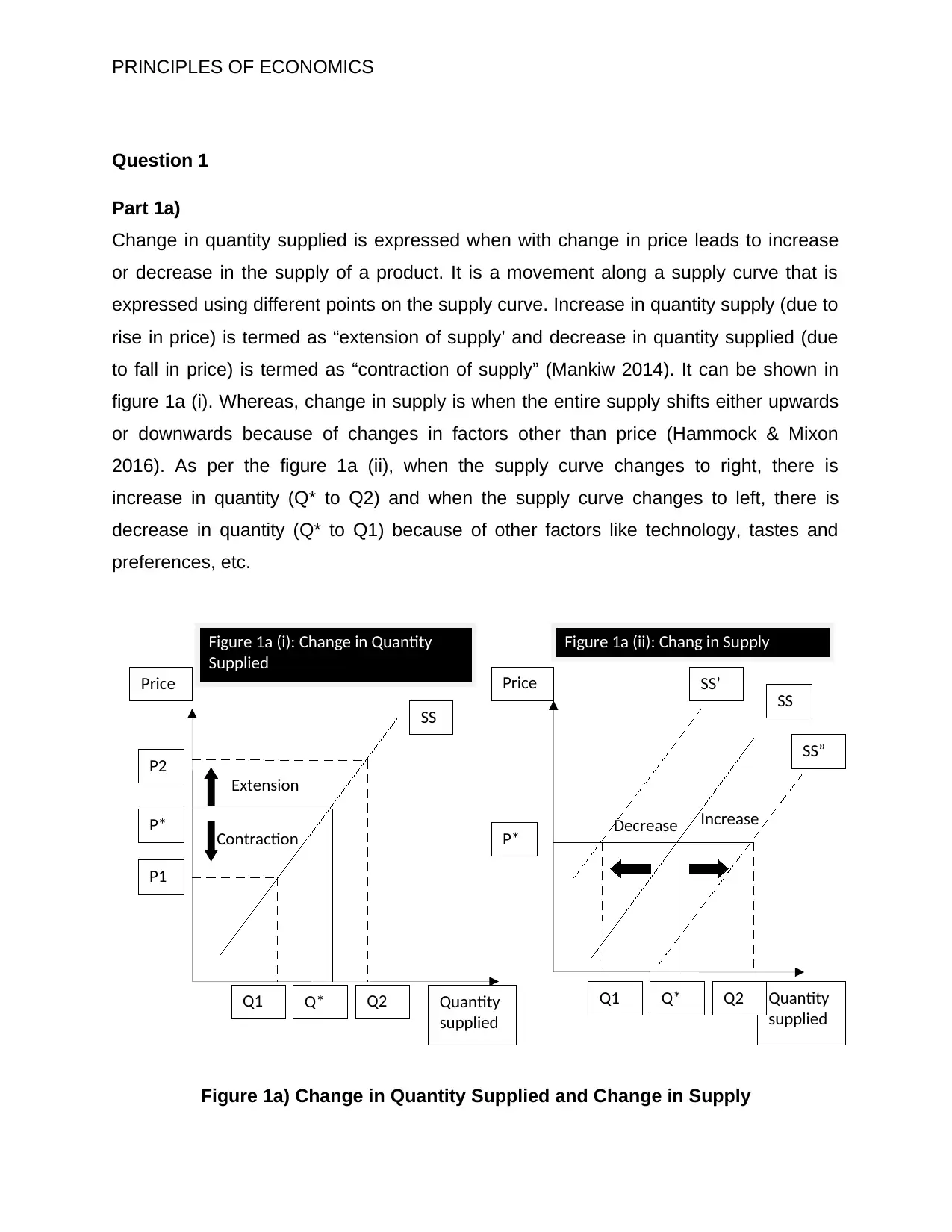

Part 1a)

Change in quantity supplied is expressed when with change in price leads to increase

or decrease in the supply of a product. It is a movement along a supply curve that is

expressed using different points on the supply curve. Increase in quantity supply (due to

rise in price) is termed as “extension of supply’ and decrease in quantity supplied (due

to fall in price) is termed as “contraction of supply” (Mankiw 2014). It can be shown in

figure 1a (i). Whereas, change in supply is when the entire supply shifts either upwards

or downwards because of changes in factors other than price (Hammock & Mixon

2016). As per the figure 1a (ii), when the supply curve changes to right, there is

increase in quantity (Q* to Q2) and when the supply curve changes to left, there is

decrease in quantity (Q* to Q1) because of other factors like technology, tastes and

preferences, etc.

Figure 1a) Change in Quantity Supplied and Change in Supply

Q* Q2Q1

SS

SS”

SS’

P1

P2

P*

SS

Price

Quantity

supplied

Price

Quantity

supplied

Contraction

IncreaseDecrease

Figure 1a (i): Change in Quantity

Supplied

Figure 1a (ii): Chang in Supply

Q* Q2Q1

P*

PRINCIPLES OF ECONOMICS

Question 1

Part 1a)

Change in quantity supplied is expressed when with change in price leads to increase

or decrease in the supply of a product. It is a movement along a supply curve that is

expressed using different points on the supply curve. Increase in quantity supply (due to

rise in price) is termed as “extension of supply’ and decrease in quantity supplied (due

to fall in price) is termed as “contraction of supply” (Mankiw 2014). It can be shown in

figure 1a (i). Whereas, change in supply is when the entire supply shifts either upwards

or downwards because of changes in factors other than price (Hammock & Mixon

2016). As per the figure 1a (ii), when the supply curve changes to right, there is

increase in quantity (Q* to Q2) and when the supply curve changes to left, there is

decrease in quantity (Q* to Q1) because of other factors like technology, tastes and

preferences, etc.

Figure 1a) Change in Quantity Supplied and Change in Supply

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Q*Q1

P*

P1

Petrol

Price

DD

SS

SS1

Figure 1b (i): Effect on market for petrol

Q*Q1

P*

P1

Passenger cars with small engin

Price

DD

Figure 1b (ii): Effect on Passenger cars with small engines

SS1

SS

P2

Q2

PRINCIPLES OF ECONOMICS

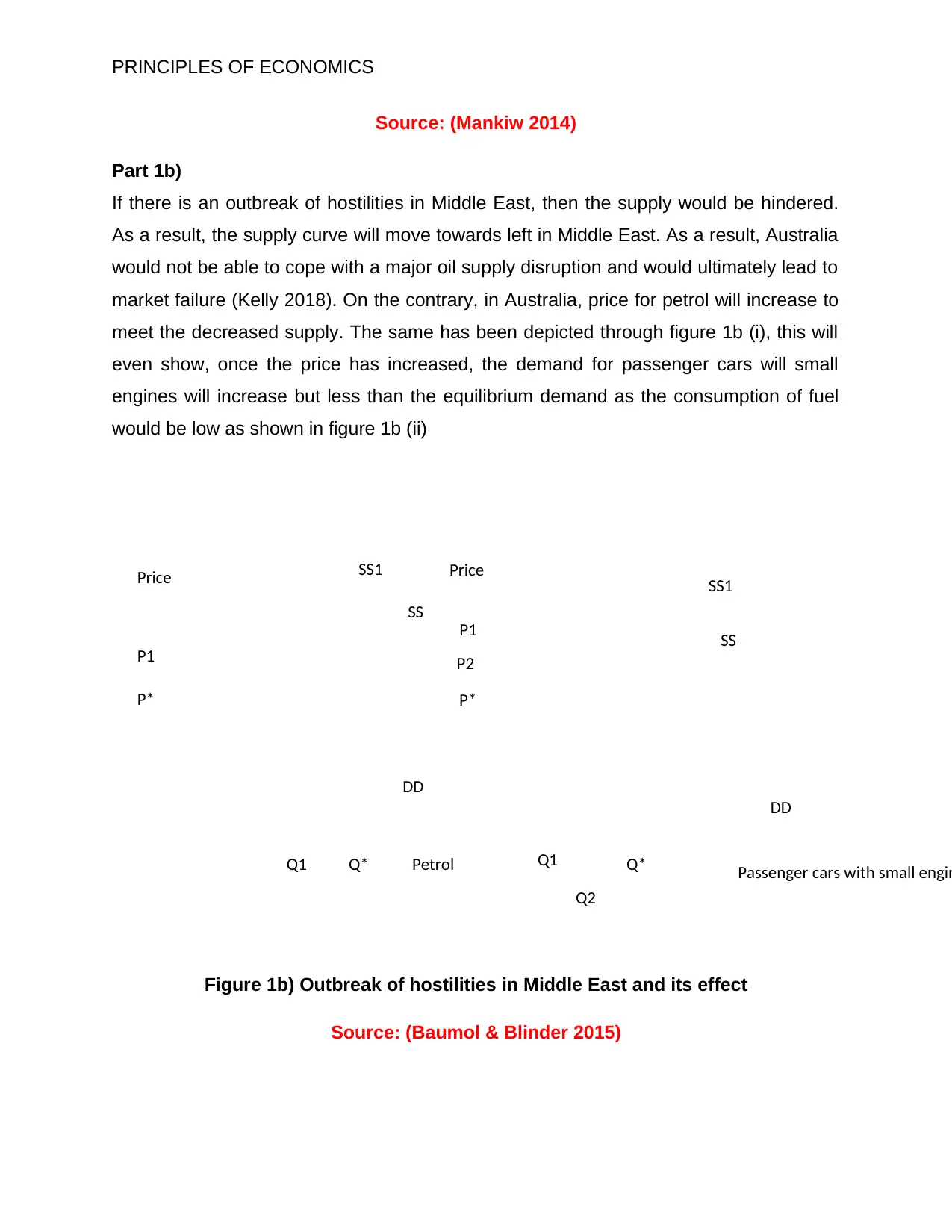

Source: (Mankiw 2014)

Part 1b)

If there is an outbreak of hostilities in Middle East, then the supply would be hindered.

As a result, the supply curve will move towards left in Middle East. As a result, Australia

would not be able to cope with a major oil supply disruption and would ultimately lead to

market failure (Kelly 2018). On the contrary, in Australia, price for petrol will increase to

meet the decreased supply. The same has been depicted through figure 1b (i), this will

even show, once the price has increased, the demand for passenger cars will small

engines will increase but less than the equilibrium demand as the consumption of fuel

would be low as shown in figure 1b (ii)

Figure 1b) Outbreak of hostilities in Middle East and its effect

Source: (Baumol & Blinder 2015)

P*

P1

Petrol

Price

DD

SS

SS1

Figure 1b (i): Effect on market for petrol

Q*Q1

P*

P1

Passenger cars with small engin

Price

DD

Figure 1b (ii): Effect on Passenger cars with small engines

SS1

SS

P2

Q2

PRINCIPLES OF ECONOMICS

Source: (Mankiw 2014)

Part 1b)

If there is an outbreak of hostilities in Middle East, then the supply would be hindered.

As a result, the supply curve will move towards left in Middle East. As a result, Australia

would not be able to cope with a major oil supply disruption and would ultimately lead to

market failure (Kelly 2018). On the contrary, in Australia, price for petrol will increase to

meet the decreased supply. The same has been depicted through figure 1b (i), this will

even show, once the price has increased, the demand for passenger cars will small

engines will increase but less than the equilibrium demand as the consumption of fuel

would be low as shown in figure 1b (ii)

Figure 1b) Outbreak of hostilities in Middle East and its effect

Source: (Baumol & Blinder 2015)

DD

SS

P*

Q*

P (Seller)

P (Buyer)

Price

Quantity

SUBSIDY

Figure 2a: Unit Sales Subsidy

PRINCIPLES OF ECONOMICS

Part 1c)

As per Carrington (2016), electric cars are assumed to be 35% of new car sales in

2040, such that every fourth car will be an electric car. With growing demand of electric

cars and assumption, the demand for battery powered bicycles will decrease (will shift

to left) as electric and battery are substitutes such that decease in prices for battery

bicycles will increase the demand for electric cars.

Question 2

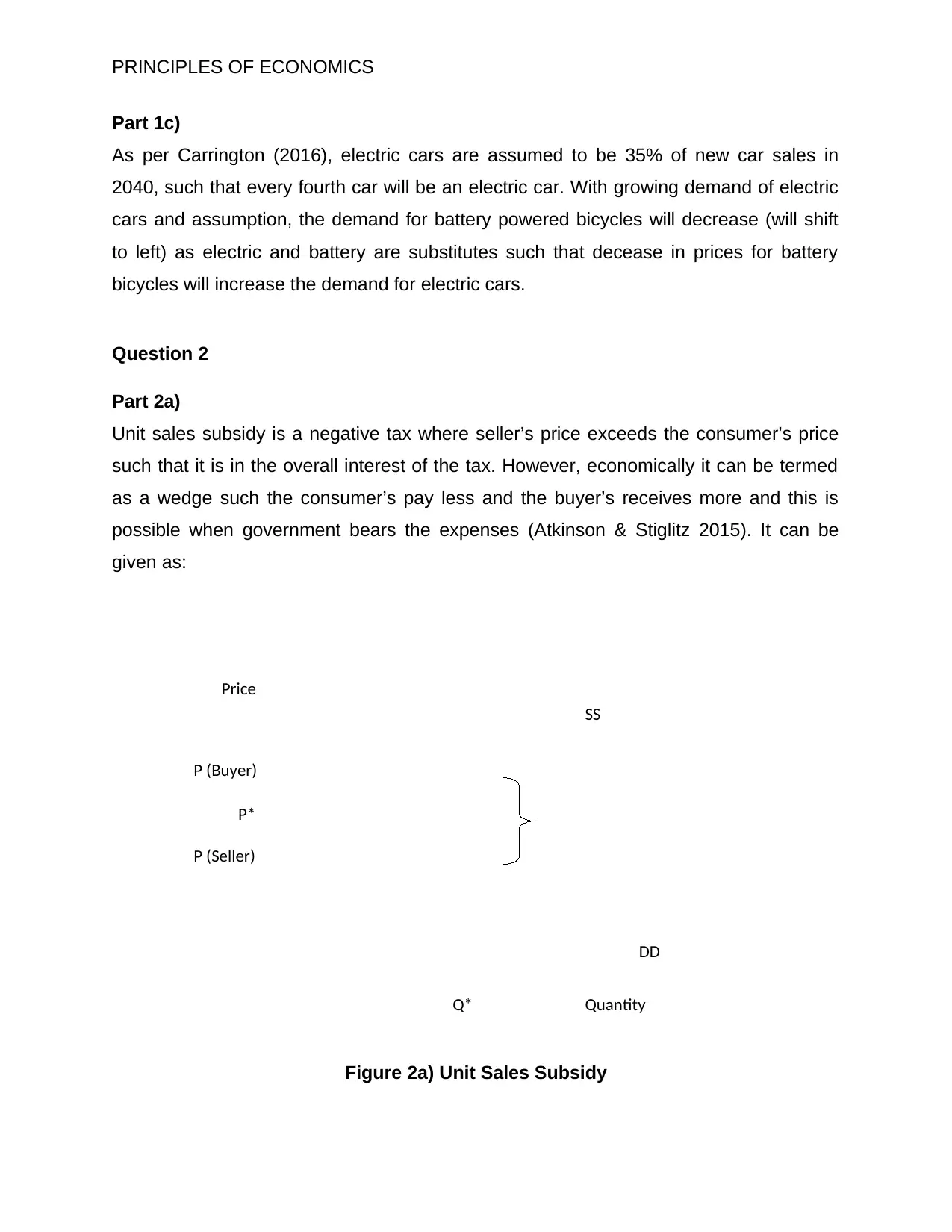

Part 2a)

Unit sales subsidy is a negative tax where seller’s price exceeds the consumer’s price

such that it is in the overall interest of the tax. However, economically it can be termed

as a wedge such the consumer’s pay less and the buyer’s receives more and this is

possible when government bears the expenses (Atkinson & Stiglitz 2015). It can be

given as:

Figure 2a) Unit Sales Subsidy

SS

P*

Q*

P (Seller)

P (Buyer)

Price

Quantity

SUBSIDY

Figure 2a: Unit Sales Subsidy

PRINCIPLES OF ECONOMICS

Part 1c)

As per Carrington (2016), electric cars are assumed to be 35% of new car sales in

2040, such that every fourth car will be an electric car. With growing demand of electric

cars and assumption, the demand for battery powered bicycles will decrease (will shift

to left) as electric and battery are substitutes such that decease in prices for battery

bicycles will increase the demand for electric cars.

Question 2

Part 2a)

Unit sales subsidy is a negative tax where seller’s price exceeds the consumer’s price

such that it is in the overall interest of the tax. However, economically it can be termed

as a wedge such the consumer’s pay less and the buyer’s receives more and this is

possible when government bears the expenses (Atkinson & Stiglitz 2015). It can be

given as:

Figure 2a) Unit Sales Subsidy

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DD

SS

P1

Q*

P2

Demand

Price

Subsidy

P* Price fall

Consumption does not increase drastically

Wheat

PRINCIPLES OF ECONOMICS

Source: (Atkinson & Stiglitz 2015)

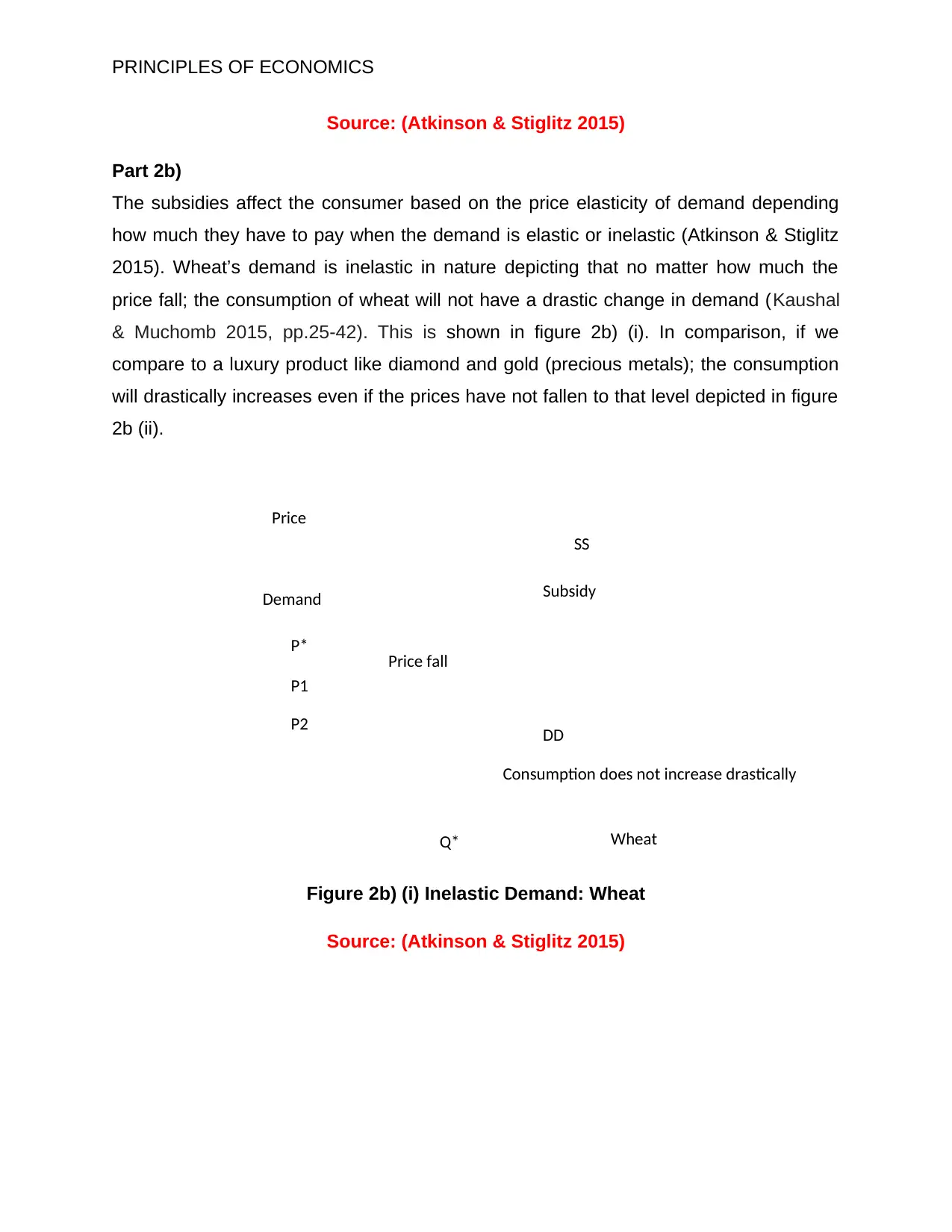

Part 2b)

The subsidies affect the consumer based on the price elasticity of demand depending

how much they have to pay when the demand is elastic or inelastic (Atkinson & Stiglitz

2015). Wheat’s demand is inelastic in nature depicting that no matter how much the

price fall; the consumption of wheat will not have a drastic change in demand (Kaushal

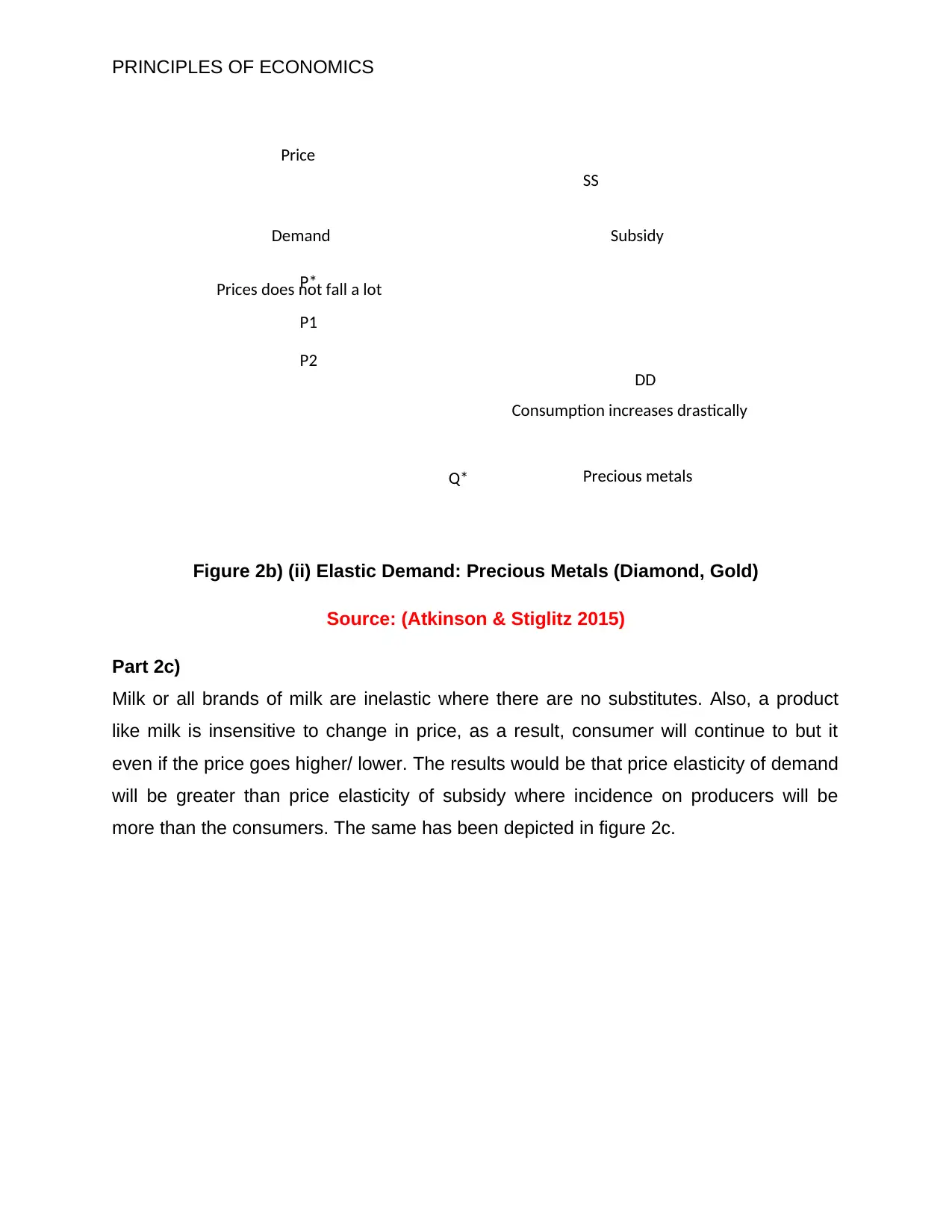

& Muchomb 2015, pp.25-42). This is shown in figure 2b) (i). In comparison, if we

compare to a luxury product like diamond and gold (precious metals); the consumption

will drastically increases even if the prices have not fallen to that level depicted in figure

2b (ii).

Figure 2b) (i) Inelastic Demand: Wheat

Source: (Atkinson & Stiglitz 2015)

SS

P1

Q*

P2

Demand

Price

Subsidy

P* Price fall

Consumption does not increase drastically

Wheat

PRINCIPLES OF ECONOMICS

Source: (Atkinson & Stiglitz 2015)

Part 2b)

The subsidies affect the consumer based on the price elasticity of demand depending

how much they have to pay when the demand is elastic or inelastic (Atkinson & Stiglitz

2015). Wheat’s demand is inelastic in nature depicting that no matter how much the

price fall; the consumption of wheat will not have a drastic change in demand (Kaushal

& Muchomb 2015, pp.25-42). This is shown in figure 2b) (i). In comparison, if we

compare to a luxury product like diamond and gold (precious metals); the consumption

will drastically increases even if the prices have not fallen to that level depicted in figure

2b (ii).

Figure 2b) (i) Inelastic Demand: Wheat

Source: (Atkinson & Stiglitz 2015)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DD

SS

P1

Q*

P2

Demand

Price

Subsidy

P*Prices does not fall a lot

Consumption increases drastically

Precious metals

PRINCIPLES OF ECONOMICS

Figure 2b) (ii) Elastic Demand: Precious Metals (Diamond, Gold)

Source: (Atkinson & Stiglitz 2015)

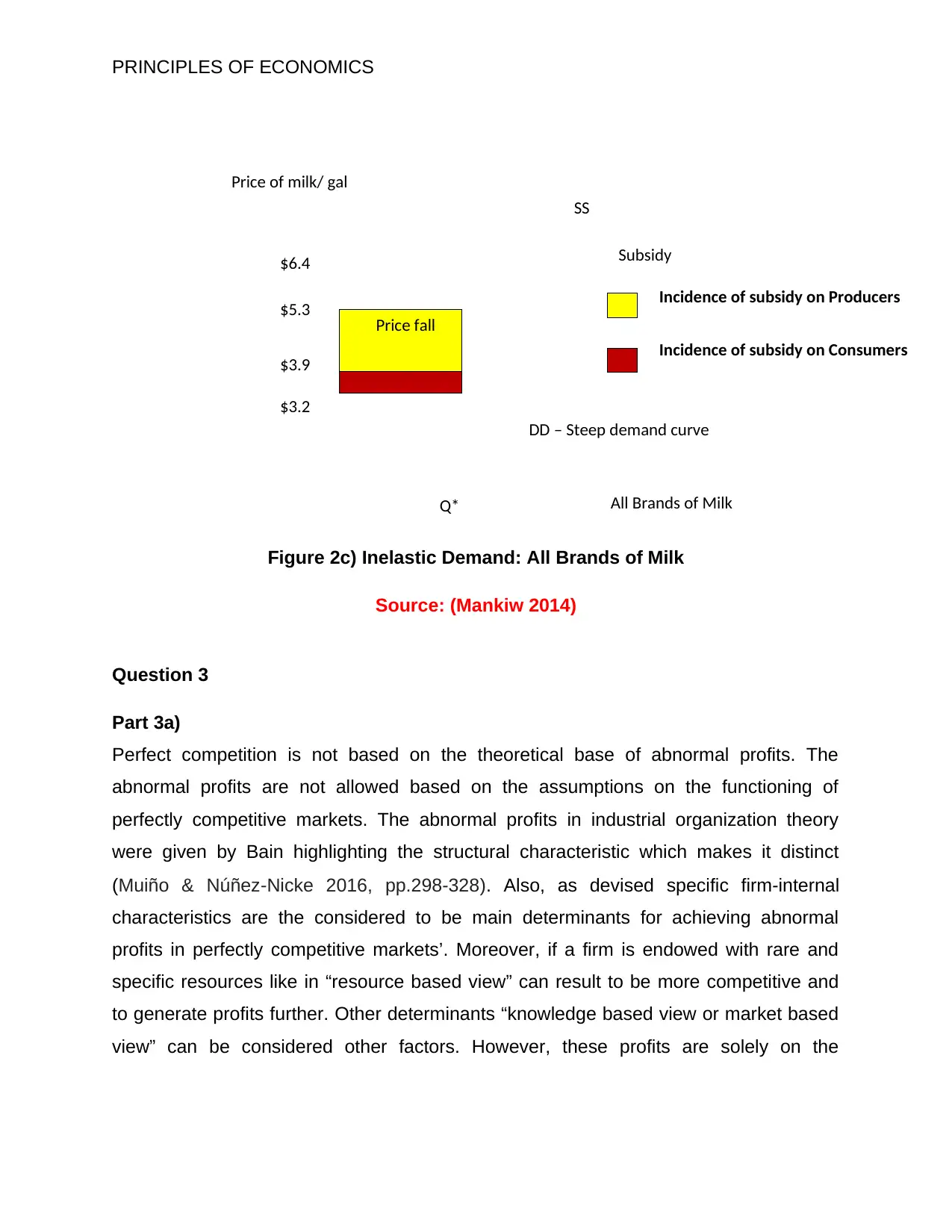

Part 2c)

Milk or all brands of milk are inelastic where there are no substitutes. Also, a product

like milk is insensitive to change in price, as a result, consumer will continue to but it

even if the price goes higher/ lower. The results would be that price elasticity of demand

will be greater than price elasticity of subsidy where incidence on producers will be

more than the consumers. The same has been depicted in figure 2c.

SS

P1

Q*

P2

Demand

Price

Subsidy

P*Prices does not fall a lot

Consumption increases drastically

Precious metals

PRINCIPLES OF ECONOMICS

Figure 2b) (ii) Elastic Demand: Precious Metals (Diamond, Gold)

Source: (Atkinson & Stiglitz 2015)

Part 2c)

Milk or all brands of milk are inelastic where there are no substitutes. Also, a product

like milk is insensitive to change in price, as a result, consumer will continue to but it

even if the price goes higher/ lower. The results would be that price elasticity of demand

will be greater than price elasticity of subsidy where incidence on producers will be

more than the consumers. The same has been depicted in figure 2c.

DD – Steep demand curve

SS

$3.9

Q*

$3.2

$6.4

Price of milk/ gal

Subsidy

$5.3 Price fall

All Brands of Milk

Incidence of subsidy on Producers

Incidence of subsidy on Consumers

PRINCIPLES OF ECONOMICS

Figure 2c) Inelastic Demand: All Brands of Milk

Source: (Mankiw 2014)

Question 3

Part 3a)

Perfect competition is not based on the theoretical base of abnormal profits. The

abnormal profits are not allowed based on the assumptions on the functioning of

perfectly competitive markets. The abnormal profits in industrial organization theory

were given by Bain highlighting the structural characteristic which makes it distinct

(Muiño & Núñez‐Nicke 2016, pp.298-328). Also, as devised specific firm-internal

characteristics are the considered to be main determinants for achieving abnormal

profits in perfectly competitive markets’. Moreover, if a firm is endowed with rare and

specific resources like in “resource based view” can result to be more competitive and

to generate profits further. Other determinants “knowledge based view or market based

view” can be considered other factors. However, these profits are solely on the

SS

$3.9

Q*

$3.2

$6.4

Price of milk/ gal

Subsidy

$5.3 Price fall

All Brands of Milk

Incidence of subsidy on Producers

Incidence of subsidy on Consumers

PRINCIPLES OF ECONOMICS

Figure 2c) Inelastic Demand: All Brands of Milk

Source: (Mankiw 2014)

Question 3

Part 3a)

Perfect competition is not based on the theoretical base of abnormal profits. The

abnormal profits are not allowed based on the assumptions on the functioning of

perfectly competitive markets. The abnormal profits in industrial organization theory

were given by Bain highlighting the structural characteristic which makes it distinct

(Muiño & Núñez‐Nicke 2016, pp.298-328). Also, as devised specific firm-internal

characteristics are the considered to be main determinants for achieving abnormal

profits in perfectly competitive markets’. Moreover, if a firm is endowed with rare and

specific resources like in “resource based view” can result to be more competitive and

to generate profits further. Other determinants “knowledge based view or market based

view” can be considered other factors. However, these profits are solely on the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ATC

AFC

Q*

AVC

Cost

Output

“A”

PRINCIPLES OF ECONOMICS

dynamics of long run equilibrium value of the abnormal profits (Hirsch 2013, pp.741-

759).

Part 3b)

Average total costs are the total cost by number of units produced.

ATC = Total Cost/ Output but

ATC = AVC (Average Variable Cost) + AFC (Average Fixed Cost)

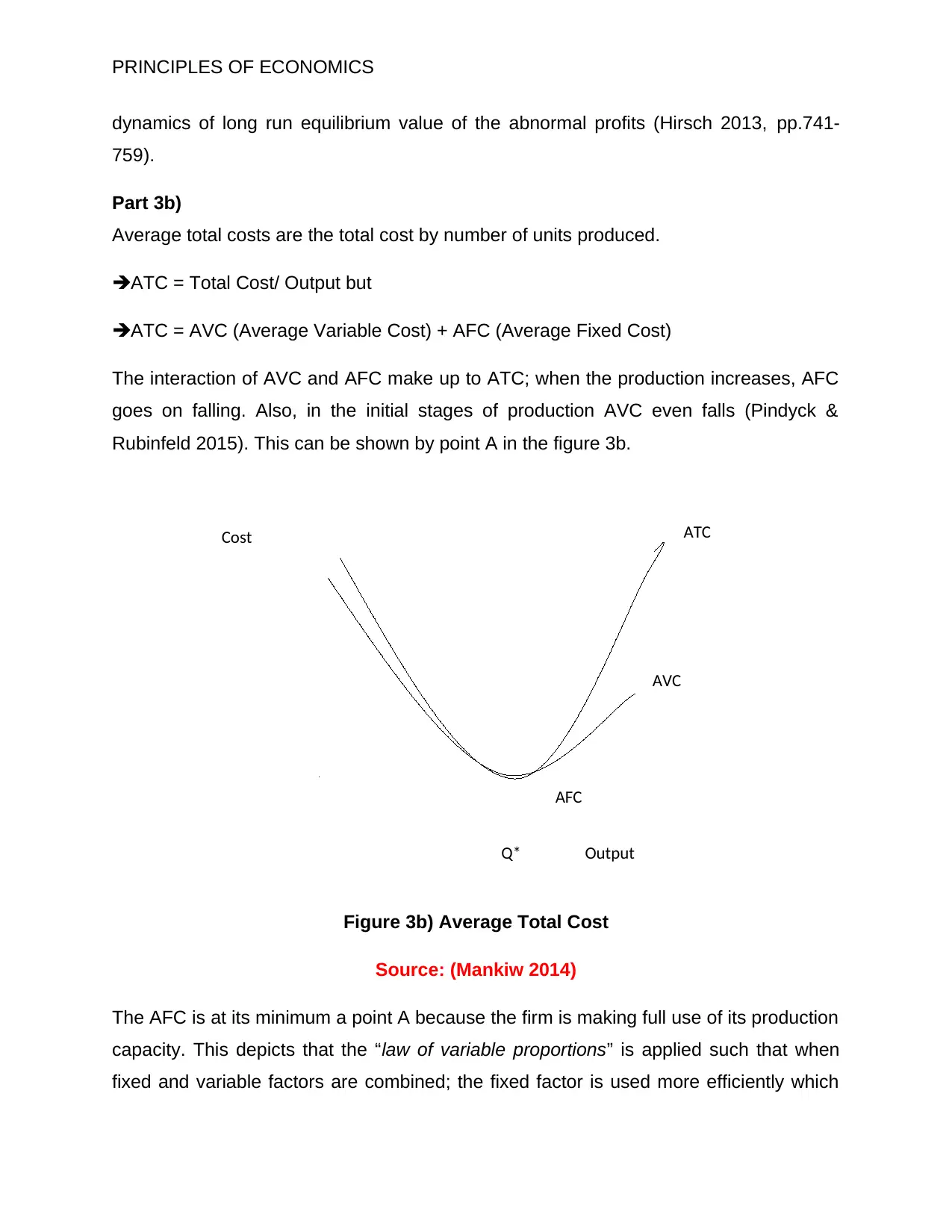

The interaction of AVC and AFC make up to ATC; when the production increases, AFC

goes on falling. Also, in the initial stages of production AVC even falls (Pindyck &

Rubinfeld 2015). This can be shown by point A in the figure 3b.

Figure 3b) Average Total Cost

Source: (Mankiw 2014)

The AFC is at its minimum a point A because the firm is making full use of its production

capacity. This depicts that the “law of variable proportions” is applied such that when

fixed and variable factors are combined; the fixed factor is used more efficiently which

AFC

Q*

AVC

Cost

Output

“A”

PRINCIPLES OF ECONOMICS

dynamics of long run equilibrium value of the abnormal profits (Hirsch 2013, pp.741-

759).

Part 3b)

Average total costs are the total cost by number of units produced.

ATC = Total Cost/ Output but

ATC = AVC (Average Variable Cost) + AFC (Average Fixed Cost)

The interaction of AVC and AFC make up to ATC; when the production increases, AFC

goes on falling. Also, in the initial stages of production AVC even falls (Pindyck &

Rubinfeld 2015). This can be shown by point A in the figure 3b.

Figure 3b) Average Total Cost

Source: (Mankiw 2014)

The AFC is at its minimum a point A because the firm is making full use of its production

capacity. This depicts that the “law of variable proportions” is applied such that when

fixed and variable factors are combined; the fixed factor is used more efficiently which

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PRINCIPLES OF ECONOMICS

leads to fall in ATC in short run (Jacoby & Brooman 2017, pp. 65-95). The diagram

above depicts that the fixed factors are extensively used.

Part 3c)

Qualifies accountants are the ones who handle finances of a given product with

minimizing the costs and maximizing the profits. In short, run, when we analyse that

whether the accountants need to wash their car or not. They should evaluate that

initially; there will be fixed costs like maintenance, insurance and others (Posner 2014).

The variable costs would be labour and materials required during the car wash.

However, when ATC and AVC are at their low, the costs would be high, but it would be

higher if they go to service centre to get their car washed. As a result, initially, the

quality accountants should wash their cars on their own.

Question 4

Part 4a)

The price elasticity of demand for alcohol and tobacco in Australia is either inelastic or

elastic. Although, there have been a continuous debate whether these are substitutes or

are complements to each other but as per Subbarman (2017, pp.1399-1414), alcohol

and tobacco are both substitutes and complements in Australia. The results from

Australian National Drug Strategy shows that these two are not related rather are

substitutes because both and in NDSH are illicit drugs, if one’s price increases, so is the

demand of other increases but not equivalent to the first one (Substitutes for price). On

the contrary, if one’s price increases, the demand of other decreases (Complements for

usage). On the other hand, Wen, Hockenberry & Cummings (2014) had to say that

alcohol and tobacco are weak complements and Kelly & Rasaul (2014, pp.89-114)

mentioned it to be strong substitutes. However, demand for alcohol and tobacco has

increasingly become inelastic in the 21st century but the country like Australia has this

as an unidentified factor. The higher levels of per capita consumption relates to inelastic

demand which have the “own-price elasticity” of demand (Wong, Selvanathan &

Selvanathan 2017, pp.799-823).

leads to fall in ATC in short run (Jacoby & Brooman 2017, pp. 65-95). The diagram

above depicts that the fixed factors are extensively used.

Part 3c)

Qualifies accountants are the ones who handle finances of a given product with

minimizing the costs and maximizing the profits. In short, run, when we analyse that

whether the accountants need to wash their car or not. They should evaluate that

initially; there will be fixed costs like maintenance, insurance and others (Posner 2014).

The variable costs would be labour and materials required during the car wash.

However, when ATC and AVC are at their low, the costs would be high, but it would be

higher if they go to service centre to get their car washed. As a result, initially, the

quality accountants should wash their cars on their own.

Question 4

Part 4a)

The price elasticity of demand for alcohol and tobacco in Australia is either inelastic or

elastic. Although, there have been a continuous debate whether these are substitutes or

are complements to each other but as per Subbarman (2017, pp.1399-1414), alcohol

and tobacco are both substitutes and complements in Australia. The results from

Australian National Drug Strategy shows that these two are not related rather are

substitutes because both and in NDSH are illicit drugs, if one’s price increases, so is the

demand of other increases but not equivalent to the first one (Substitutes for price). On

the contrary, if one’s price increases, the demand of other decreases (Complements for

usage). On the other hand, Wen, Hockenberry & Cummings (2014) had to say that

alcohol and tobacco are weak complements and Kelly & Rasaul (2014, pp.89-114)

mentioned it to be strong substitutes. However, demand for alcohol and tobacco has

increasingly become inelastic in the 21st century but the country like Australia has this

as an unidentified factor. The higher levels of per capita consumption relates to inelastic

demand which have the “own-price elasticity” of demand (Wong, Selvanathan &

Selvanathan 2017, pp.799-823).

PRINCIPLES OF ECONOMICS

Part 4b)

Level of competition differs with each market. When analyzed from the perspective of

real markets then agriculture market faces a perfectly horizontal demand curves for

homogeneous proud in the industry with free entry and exit of firms. This market can be

termed as perfectly competitive market (Baumol & Blinder 2015). Nevertheless, other

markets are even highly competitive but they face high inelastic demand curves and

relatively not that easy to enter and exit the market. Moreover, in case of monopoly or

oligopoly, it implicitly or explicitly gets together in the setting prices and this does not

rule out competitive behavior (Pindyck & Rubinfeld 2015). To depict each market’s

competitive nature, figure 4b) is shown below from perfect competition to pure

monopoly.

Figure 4b) Competitive behaviours in each market

Source: (Pindyck & Rubinfeld 2015)

Question 5

Part 5a)

Total Revenue is the sum of all sales and marginal revenue is the addition to the total

revenue by making changes one unit per change in the output. Algebraically, MR and

TR can be given as:

TR = Price X Quantity; MR = Δ TR

Δ Q

MR for a ‘n’ units MRn = TRn – TRn-1

Part 4b)

Level of competition differs with each market. When analyzed from the perspective of

real markets then agriculture market faces a perfectly horizontal demand curves for

homogeneous proud in the industry with free entry and exit of firms. This market can be

termed as perfectly competitive market (Baumol & Blinder 2015). Nevertheless, other

markets are even highly competitive but they face high inelastic demand curves and

relatively not that easy to enter and exit the market. Moreover, in case of monopoly or

oligopoly, it implicitly or explicitly gets together in the setting prices and this does not

rule out competitive behavior (Pindyck & Rubinfeld 2015). To depict each market’s

competitive nature, figure 4b) is shown below from perfect competition to pure

monopoly.

Figure 4b) Competitive behaviours in each market

Source: (Pindyck & Rubinfeld 2015)

Question 5

Part 5a)

Total Revenue is the sum of all sales and marginal revenue is the addition to the total

revenue by making changes one unit per change in the output. Algebraically, MR and

TR can be given as:

TR = Price X Quantity; MR = Δ TR

Δ Q

MR for a ‘n’ units MRn = TRn – TRn-1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.